Sample Category Title

Trade Idea : EUR/USD – Sell at 1.1940 or buy at 1.1855

EUR/USD - 1.1887

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.1880

Kijun-Sen level : 1.1931

Ichimoku cloud top : 1.1978

Ichimoku cloud bottom : 1.1968

Original strategy :

Sell at 1.1940, Target: 1.1840, Stop: 1.1975

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1940, Target: 1.1840, Stop: 1.1975

O.C.O.

Buy at 1.1855, Target:1.1955, Stop: 1.1820

Position : -

Target : -

Stop : -

As the single currency has remained under pressure after yesterday’s selloff from 1.1995, adding credence to our view that the decline from 1.2093 top is still in progress, hence downside bias remains for this move to bring retracement of early upmove to 1.1850 support, however, loss of near term downward momentum would limit downside and reckon another previous support at 1.1823 would hold, bring rebound later.

In view of this, whilst we are still looking to sell euro on recovery, we are inclined to turn long on next decline as 1.1850 support should hold. Below 1.1823 would extend weakness to 1.1800 but still reckon downside would be limited. Above the Ichimoku cloud top (now at 1.1978) would abort and signal low is formed instead, bring a stronger rebound to said resistance at 1.1995 first.

European Open Briefing: Asian Equity Markets Were Mostly Flat On Thursday

Global Markets:

- Asian stock markets: Nikkei lost 0.31 %, Shanghai Composite fell 0.17 %, Hang Seng down 0.47 %, ASX 200 fell 0.11 %

- Commodities: Gold at $1326.79 (-0.09 %), Silver at $17.78 (-0.45 %), WTI Oil at $49.23 (-0.14 %), Brent Oil at $55.02 (-0.25%)

- Rates: US 10-year yield at 2.18, UK 10-year yield at 1.14, German 10-year yield at 0.40

News & Data:

- (AUD) Employment Change 54.2 vs 17.5 K expected

- (AUD) Unemployment Rate 5.6 % vs 5.6 % expected

- (CNY) Industrial Production y/y 6.0 % vs 6.6 % expected

- (CNY) Fixed Asset Investment ytd/y 7.8 % vs 8.2 % expected

- (USD) PPI m/m 0.2 % vs 0.3 % expected

- (USD) Core PPI m/m 0.1 % vs 0.2 % expected

- (USD) Crude Oil Inventories 5.9 M vs 4.1 M expected

- (GBP) Average Earnings Index 3m/y 2.1 % vs 2.3 % expected

- (GBP) Claimant Count Change -2.8 K vs 0.8 K expected

- (GBP) Unemployment Rate 4.3 % vs 4.4 % expected

- (CHF) PPI m/m 0.3 % vs 0.2 % expected

Markets Update:

Asian Equity markets were mostly flat on Thursday trading down from 10-year highs after disappointing economic data out of China and investors awaiting a rate decision from the Bank of England. Markets also digested the rise in U.S. Treasury yields overnight following tax reform headlines out of Washington, although the dollar's advance paused.

USD/JPY is currently seen trading at 110.45 down from the highs of 110.70. The pair had a very small dip in late NY/early Asia with NBC tweeting that North Korea was seen to be prepping for a missile launch. However, the dollar continues to extend gains against the Yen, gaining over 0.3 percent on Wednesday.

The Australian Dollar had a very active session, following a slight drop towards 0.7970 ahead of the Jobs report, the Aussie jumped as high as 0.8016 against the US Dollar after positive jobs data. AUDUSD is currently seen trading at around 0.8000 losing some of its earlier gains as Movements in the Aussie dollar are influenced by China data due to Australia's dependence on exports.

EUR/USD is currently seen trading at 1.1875 losing around 0.1 percent earlier in the session, following a 0.7 percent drop the previous day. The dollar index measured against a basket of six major currencies is currently valued at 92.47 after touching 92.530 overnight, its highest since Sept. 5.

Upcoming Events:

- 07:30 GMT – (CHF) Libor Rate

- 07:30 GMT – (CHF) SNB Monetary Policy Assessment

- 11:00GMT – (GBP) MPC Official Bank Rate Votes

- 11:00GMT – (GBP) Monetary Policy Summary

- 11:00GMT – (GBP) Official Bank Rate

- 12:30 GMT – (USD) CPI m/m

- 12:30 GMT – (USD) Core CPI m/m

- 12:30 GMT – (USD) Unemployment Claims

- 15:30 GMT – (EUR) German Buba President Weidmann Speaks

- 22:30 GMT – (NZD) Business NZ Manufacturing Index

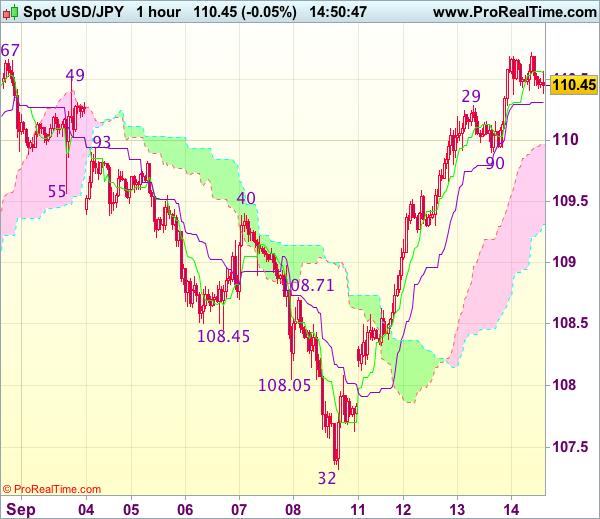

Trade Idea : USD/JPY – Buy at 109.65

USD/JPY - 110.45

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 110.56

Kijun-Sen level : 110.32

Ichimoku cloud top : 109.96

Ichimoku cloud bottom : 109.31

Original strategy :

Buy at 109.65, Target: 110.65, Stop: 109.30

Position : -

Target : -

Stop : -

New strategy :

Buy at 109.65, Target: 110.65, Stop: 109.30

Position : -

Target : -

Stop : -

As the greenback has maintained a firm undertone after this week’s rally, suggesting bullishness remains for the rise from 107.32 low to extend further gain towards previous resistance at 110.95-05, however, break there is needed to retain upside bias and encourage for headway to 111.30, having said that, near term overbought condition should prevent sharp move beyond another previous resistance at 111.71, bring retreat later.

In view of this, would not chase this rise here and would be prudent to buy dollar on subsequent pullback as 109.50-60 should limit upside. Below previous resistance at 109.40 would risk test of the lower Kumo (now at 109.31) but only break there would abort and signal top is formed instead, bring weakness to 109.00 first.

BoE Preview

The Bank of England faces a dilemma when it meets on Thursday between getting inflation in check and supporting the flagging post-Brexit economy.

With the central bank significantly overshooting its 2% inflation target – CPI rose to 2.9% in August – the answer may appear simple but with policy makers divided, that is clearly not the case.

The depreciation of sterling has played a major role in the inflation rise over the last year and with the currency having bottomed last October, it is plausible that once the base effects drop out of the annual comparison, inflation will fall closer to target. But can policy makers rely on that?

As we can see from recent voting, there is a growing belief that this cannot be relied upon. The important question therefore becomes, will enough policy makers decide they can't rely on it before the data starts to correct itself?

With only two policy makers – Ian McCafferty and Michael Saunders – having voted at the previous meeting to raise interest rates and a ninth member having since joined the Monetary Policy Committee, it seems unlikely that the hike threshold will be passed this week.

That said, the pound did not necessarily rally over the last couple of weeks on the expectation that the BoE will raise interest rates on Thursday, rather on the expectation that it is getting closer. The inflation reading on Tuesday further fuelled the expectation while Wednesday's wage data tempered it slightly.

What Can We Expect on Thursday?

While a rate hike at the meeting is very unlikely, central banks have surprised us in the past and given how other central banks (ECB, Bank of Canada) are exploring tighter monetary policy, it remains a possibility, albeit a small one I would say.

What traders are most interested in is what impact the August inflation number had on those policy makers that have been borderline hike voters but remained with the majority until now. There is also one new policy maker on the committee this month – Sir David Ramsden – and another that only joined in July – Silvana Tenreyro – who's views we still know little about.

It may not take as much as we thought to sway the vote in favour of a rate hike, at which point I would expect to see a sharp move higher in the pound, as that is not priced in.

What's more likely is the voting will either be unchanged – with only McCafferty and Saunders voting for a hike – or perhaps one more policy maker will join them. This may even be enough to provide some upside for the pound in the near term.

The minutes will be of interest to traders, particularly if they allude to inflation becoming a concern to policy makers or some policy makers being tempted to vote for a hike. That would suggest any further uptick in inflation going forward could result in higher rates.

Australia’s Unemployment Rate Remained Steady In August, Job Growth Surged The Most In Nearly 2 Years In The Same...

For the 24 hours to 23:00 GMT, the AUD declined 0.42% against the USD and closed at 0.7985.

LME Copper prices declined 1.1% or $74.5/MT to $6527.0/MT. Aluminium prices traded flat at $2083.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.8005, with the AUD trading 0.25% higher against the USD from yesterday's close, following robust Australian jobs report.

Early morning data indicated that Australia's seasonally adjusted unemployment rate remained unchanged at 5.6% in August, meeting market expectations. Further, the number of people employed in Australia climbed by 54.2K in August, recording the biggest jump since October 2015 and following a revised advance of 29.3K in the previous month. Meanwhile, markets had anticipated the number of people employed to advance 20.0K.

On the contrary, the nation's consumer inflation expectations declined to 3.8% in September, after recording a level of 4.2% in the previous month.

Elsewhere in China, Australia's largest trading partner, industrial production climbed 6.0% on an annual basis in August, rising at its weakest pace in nine months and undershooting market expectations for a rise of 6.6%. In the previous month, industrial production had recorded a rise of 6.4%. Moreover, the nation's retail sales posted its slowest rise in six months, after it climbed 10.1% YoY in August, compared to market consensus for a rise of 10.5%. In the previous month, retail sales had recorded a rise of 10.4%.

The pair is expected to find support at 0.7969, and a fall through could take it to the next support level of 0.7934. The pair is expected to find its first resistance at 0.8042, and a rise through could take it to the next resistance level of 0.8080.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Euro-Zone’s Industrial Output Rebounded As Expected In August

For the 24 hours to 23:00 GMT, the EUR declined 0.65% against the USD and closed at 1.1893.

On the data front, the Euro-zone's seasonally adjusted industrial production rebounded 0.1% MoM in July, meeting market expectations and following a sharp drop of 0.6% in the previous month.

Separately, Germany's final consumer price index (CPI) registered a rise of 1.8% on an annual basis in August, confirming the preliminary print. The CPI had risen 1.7% in the previous month.

Data released in the US indicated that mortgage applications rose 9.9% in the week ended 08 September, jumping to its strongest level in 10 months and following a gain of 3.3% in the prior week. Further, the nation's producer prices rose slightly less-than-expected by 0.2% on a monthly basis in August, compared to a drop of 0.1% in the prior month. Meanwhile, the nation's budget deficit widened less-than-anticipated to a level of $108.0 billion in August, compared to market consensus for a deficit of $119.5 billion. The nation had registered a budget deficit of $42.9 billion in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.1878, with the EUR trading 0.13% lower against the USD from yesterday's close.

The pair is expected to find support at 1.1834, and a fall through could take it to the next support level of 1.1791. The pair is expected to find its first resistance at 1.1958, and a rise through could take it to the next resistance level of 1.2039.

Amid no major macroeconomic releases in the Euro-zone today, investors will focus on the US consumer inflation for August and weekly initial jobless claims data, both due to release later in the day.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

UK’s Unemployment Rate Lowest Since 1975 In The Three Months Through July But Wage Growth Remained Sluggish In The...

For the 24 hours to 23:00 GMT, the GBP declined 0.61% against the USD and closed at 1.3215, after the latest labour market report painted a bleak picture of Britain's wage growth.

Data showed that UK's average earnings including bonus recorded a rise of 2.1% on an annual basis in the three months to July, falling short of market consensus for an advance of 2.3%, thus suggesting that consumers might further retrench as earnings have failed to keep pace with rising inflation. The average earnings including bonus had registered a rise of 2.1% in the April-June period.

However, the nation's ILO unemployment rate unexpectedly eased to 4.3% in the May-July 2017 period, dropping to its lowest level in forty-two years, while markets were expecting the ILO unemployment rate to remain steady at 4.4%. Further, the number of people employed in the nation advanced more-than-anticipated by 181.0K in the three months through July, rising by the most since the end of 2015. Market participants had envisaged for an increase of 154.0K, after registering a gain of 125.0K in the April-June period.

In the Asian session, at GMT0300, the pair is trading at 1.3203, with the GBP trading 0.09% lower against the USD from yesterday's close.

Overnight data revealed that the nation's RICS house price balance surprisingly climbed to 6.0 in August, compared to market expectations for a flat reading. House price balance had recorded a level of 1.0 in the previous month.

The pair is expected to find support at 1.3149, and a fall through could take it to the next support level of 1.3095. The pair is expected to find its first resistance at 1.3293, and a rise through could take it to the next resistance level of 1.3383.

Trading trend in the Pound today is expected to be determined by the Bank of England's interest rate decision, due later today. The central bank is widely expected to leave interest rates unchanged.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Japanese Industrial Production Retreated As Initially Estimated In July

For the 24 hours to 23:00 GMT, the USD rose 0.25% against the JPY and closed at 110.49.

In the Asian session, at GMT0300, the pair is trading at 110.52, with the USD trading slightly higher against the JPY from yesterday’s close.

Earlier in the session, data showed that Japan’s final industrial production slid 0.8% MoM in July, confirming the flash estimate. Industrial production had recorded a rise of 2.2% in the previous month.

The pair is expected to find support at 110.04, and a fall through could take it to the next support level of 109.57. The pair is expected to find its first resistance at 110.86, and a rise through could take it to the next resistance level of 111.21.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Swiss Franc Trading Lower, Ahead Of SNB’s Monetary Policy Decision

.

For the 24 hours to 23:00 GMT, the USD rose 0.35% against the CHF and closed at 0.9632.

On the macro front, Switzerland's producer and import price index rose more-than-expected by 0.3% MoM in August, compared to a flat reading in the previous month, while markets were anticipating the index to gain 0.2%.

In the Asian session, at GMT0300, the pair is trading at 0.9646, with the USD trading 0.15% higher against the CHF from yesterday's close.

The pair is expected to find support at 0.9600, and a fall through could take it to the next support level of 0.9553. The pair is expected to find its first resistance at 0.9677, and a rise through could take it to the next resistance level of 0.9707.

Ahead in the day, all eyes will be on the Swiss National Bank's (SNB) interest rate decision.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Loonie Trading On Weaker Footing In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.15% against the CAD and closed at 1.2162.

Macroeconomic data revealed that Canada's Teranet/National Bank house price index climbed 0.6% in August, after recording a rise of 2.0% in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.2177, with the USD trading 0.12% higher against the CAD from yesterday's close.

The pair is expected to find support at 1.2132, and a fall through could take it to the next support level of 1.2087. The pair is expected to find its first resistance at 1.2221, and a rise through could take it to the next resistance level of 1.2265.

Going ahead, market participants will keep a close watch on Canada's new housing price index data for July, set to release later in the day.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.