Sample Category Title

Uncertainty Reigns

Uncertainty Reigns

The uptick in rising US yields is underpinning USDJPY, but it was the gains in equities as all three major U.S. stock indexes clocked in all-time closing highs that provided the major overnight sentiment gauge. Ultimately this buoyant risk sentiment should be cheered, but FX traders remain in the Nervous Nellie camp waiting for the next chaotic patch given the evolving narratives. A word of caution to those enjoying this unexpected sea of tranquillity, the next few weeks and months come with significant risk

It's incredible just how quickly the sentiment around the USD has changed this week as deeply ingrained attitudes to fade the dollar rallies has given way to traders awaiting a deeper position squeeze on short dollar positioning. But from my seat, however, it feels like the bulk of the squeeze has occurred and that this current resounding risk rally is stoking the USDJPY fires as CrossJPY continues to race higher. But indeed, the large short dollar positions into the weekend and the surging US yields on Monday provided the primary drivers behind this remarkable USD revival.

However, the long dollar position is not without considerable risk as Fed market positioning suggests this dollar revival is little more than a respite.Tepid wage and inflation numbers are posing a conundrum for the Fed and of course, the dollar will remain an endangered species as dealers await the next Trump administration gaff.

One issue that is being discussed in market circles is that as far as US economic data is concerned, the Hurricane effect may give rise for the Feds to look through inflation data as the storm surges has likely stretched the feds window to dismiss data

The only things that appear certain today is uncertainty itself

The Euro

In the absence of any Euro particular set of drivers and lieu of the current dollar correction, the shooting star reversal is not all that surprising.But despite the sell off from massively overbought levels above 1.2000 the Euro bulls are not giving up the game quickly and remain firm buyers on dips

The Yen

From here, all roads lead to the US CPI on Thursday, which has been a key driver of dollar sentiment all year. ON a solid print the dollar rally extends to 111.25, but on a wrong impression we're quickly back to the 109's as there should be a massive wave of USD selling across the board

Chinese Yuan

After all that has been said and done the logical explanation for the Reserve Requirement shift was that the Pboc are concerned about the pace of depreciation of USD/China. The authorities intend to create more two way flows as hedger will now come back to cover USD exposures with as the authorities hope that more price stability will naturally occur. But from my seat, I think this recent move will provide an excellent opportunity to increase RMB exposure as all things China continues to look Rosy

EM Asia

USDAsia has stuck in a range bound rut despite general USD strength in the market. The market positioning remains relatively light on either side of the coin after Friday rally and subsequent correction Monday. But so far the Asia EMfx has been somewhat immune to the recent USD rally as risk appetite is buttressing local sentiment.

Pound Soars, USD Gains Further

A surprise rise in UK inflation put a BOE hike back on the table while the US dollar bounce continued. The pound was the top performer while the yen lagged. Japanese PPI and the quarter business conditions index is due up next. Our GBPUSD Premium trade is +200 pips in the green, while the GBPJPY was stopped out due to combination of rapid JPY weakness and run-away GBP strength. A new Premium video focusing on yesterday's new trade balances time and price.

The pound showed what a sliver of inflation can do after CPI rose 3.9% y/y compared to 3.7% expected on Tuesday. Cable climbed 120 pips and GBP/JPY rose nearly 250 pips. The rally in GBP/USD broke the August high and 1.3298 was the best in nearly a year. Wednesday's UK jobs figures could help sway Thursday's MPC voting from 2 to 3 hawkish dissenters.

The BOC showed what can happen to a currency when a central bank changes gears and the suspicion in markets is that Carney may finally get to hike rates. The BoE's OIS market is now pricing a 35% chance of a November hike, climbing to 44% in December.

In economic news, US JOLTS job openings were at 6.17m compared to 6.00m expected in another sliver of good economic news for the United States. The main drivers of dollar strength continued to be relief about Irma and momentum.

USD/JPY is now flat on the month after a brutal start, but more broadly it's a mixed picture. The dollar is struggling to hold gains against the euro and cable begins to gain momentum.

Looking ahead, the Asia-Pacific calendar sports a few highlights including Japanese PPI for August. It's expected to rise a healthy 3.0% when it's released at 2350 GMT. In a release at the same time, the MoF's survey of large manufacturers for Q3 is forecast at +5.0 from -2.9.

Gold Pauses After Sharp Losses Kick Off Week

Gold is unchanged in the Tuesday session, after starting the week with considerable losses. In the North American session, the spot price for an ounce of gold is $1327.47, up 0.07%. On the release front, JOLTS Job Openings improved to 6.17 million, easily beating the forecast of 5.96 million. On Wednesday, the US will publish PPI, which is expected to improve to 0.3%.

As one of the most popular safe-haven assets, gold prices have moved higher in recent weeks, as tensions have ratcheted upwards over North Korea's nuclear program. The country has launched missiles over Japan and tested a hydrogen bomb, which has send nervous investors flocking to gold as risk appetite as waned. The markets were prepared for more fireworks over the weekend, as North Korea celebrated its independence day, raising fears that Pyongyang would use the occasion to flex some muscle and test a nuclear bomb or missile. Last year, the country celebrated its anniversary by exploding its fifth nuclear test. With the crisis appearing to ease, stock markets are up and gold prices are down this week, as investors have regained their appetite for risk.

The US economy has generally looked positive in the second quarter of 2017. Preliminary GDP came in at a sizzling 3.0%, and the labor market remains close to capacity. Still, the Achilles heel of the economy remains stubbornly low inflation levels. Wage pressure has been limited, despite the fact that many businesses cannot fill job openings. Weak inflation has hampered the Fed's plans to raise interest rates a third time this year, and the odds of a December hike have dipped to just 31%, as the markets are increasingly doubtful that the Fed will make a move before next year. Will the inflation picture improve? We could see better numbers this week for August inflation – PPI is expected to improve to 0.3% on Tuesday, and the same gain is forecast for CPI on Wednesday. Both estimates are higher than the July readings.

Dollar Rally Continues as North Korea Tensions Ease

USD/JPY has posted gains in the Tuesday session, continuing the upward movement which started the week. In North American trade, the pair is trading at 109.98, up 0.54% on the day. In the US, JOLTS Job Openings improved to 6.17 million, easily beating the forecast of 5.96 million. Later in the day, Japan releases manufacturing and inflation reports. On Wednesday, the US will publish PPI, which is expected to improve to 0.3%.

After a week of increased tensions in the Korean peninsula, an easing in the crisis between North Korea and neighboring Japan and South Korea has seen an exit from safe-haven assets, such as the Japanese yen. USD/JPY has jumped 1.6% this week, erasing last week's losses. With North Korea celebrating its 69th anniversary of its founding, there were concerns that Pyongyang would use the occasion to flex some muscle and test a nuclear bomb or missile. North Korea marked last year's anniversary by exploding its fifth nuclear test. There were no incidents over the weekend, although the US, along with its allies Japan and South Korea, remain on alert for further provocations from the north. The volatility which has marked the Japanese currency is testament to its safe-haven status, as investors have snapped up the yen when the North Korean crisis, one of the world's geopolitical hot spots, heats up.

The US economy has been performing well in the second quarter. Preliminary GDP came in at a sizzling 3.0%, and the labor market remains close to capacity. Still, the Achilles heel of the economy remains stubbornly low inflation levels. Wage pressure has been limited, despite the fact that many businesses cannot fill job openings. Weak inflation has hampered the Fed's plans to raise interest rates a third time this year, and the odds of a December hike have dipped to just 31%, as the markets are increasingly doubtful that the Fed will make a move before next year. Will the inflation picture improve? We could see better numbers this week for August inflation – PPI is expected to improve to 0.3% on Tuesday, and the same gain is forecast for CPI on Wednesday. Both estimates are higher than the July readings.

Pound Soars to 1-Year High after Inflation Beat; Dollar also Up, Euro Under Pressure

The British pound surged to a one-year high in European trading on Tuesday as traders bet on a more hawkish Bank of England following stronger-than-expected UK inflation data. The US dollar extended yesterday's impressive gains against the yen but the euro struggled. The New Zealand dollar was another major gainer, while gold reversed its earlier losses following fresh threats from North Korea.

The main data in today's European session was the August inflation release out of the UK. Headline inflation rose back to May's four-year high of 2.9% year-on-year in August, beating expectations of 2.8% and up from July's 2.6% rate. Core inflation was also stronger-than-expected, rising to 2.7% y/y – its highest since November 2012. Forecasts were for core CPI to rise from 2.4% to 2.5% in August.

In a further sign that the inflation upswing from the weaker pound has yet to peak, input and output prices both came in above their top estimates. The figures will likely strengthen the argument for the Bank of England hawks that interest rates need to go up. The Bank will announce its latest policy decision on Thursday and expectations have been increasing in recent days that the MPC is heading for another split vote, with more members likely to vote for a rate hike.

The pound shot to a one-year high of $1.3287 after the data, and was last trading at $1.3265, up 0.8% on the day. It was also up sharply against the euro and the yen, jumping to a more than one-month high against both currencies. The euro breached the key 0.90 level to hit a session low of 0.8981 pounds, while against the yen, the pound hit a high of 145.94.

The euro was under pressure against the resurgent dollar for a second day, sliding to as low as $1.1924 in mid-session. A converging of views by ECB policymakers that the central bank is moving towards tighter monetary policy failed to lift the single currency. Several ECB officials spoke in favour of policy normalization yesterday, though comments that the process will be gradual, as well as the potential impact of a "persistent exchange rate shock" weighed on the euro.

However, the euro later ticked higher, rising to $1.1955, as ECB Vice President Vitor Constancio started speaking. Speaking in Frankfurt, Constancio defended the ECB's unconventional policy tools and said he was confident inflation will eventually hit the target.

The greenback continued to benefit from the improving risk-on sentiment, brought on by investor relief that the impact of Hurricane Irma was less destructive than initially feared, as well as by North Korea's inaction over the weekend. The dollar briefly broke above 110 yen before dropping slightly to around 109.85 yen. The dollar index was also unable to retain a key level, slipping below 92.0 after climbing above the level for the first time this week.

The only data out of the US today was the latest JOLTS job openings. The number of job openings rose to 6.170 million in July from a downwardly revised 6.116 million in June.

The yen's and the Swiss franc's weakness were notable against all major currencies, though gold found support from ongoing unease about tensions in the Korean peninsula. North Korea issued a new threat against the United States today following the UN's decision yesterday to adopt tougher sanctions on the hermit state. The precious metal recovered from a 1½-week low of $1322.15 an ounce to rise to around $1328 an ounce in late European trading.

In other currencies, the New Zealand dollar got a boost from the latest election polls in New Zealand that put the ruling National party ahead of the Labour party. The polls lifted the kiwi to a high of $0.7320 earlier in the session before easing to around $0.7290. The kiwi has come under pressure in recent weeks from Labour's strong performance in the polls, whose campaign pledge includes scrapping the National party's planned tax cuts.

Crude oil was on track for a second day of gains as prices were boosted after OPEC raised its forecasts for demand for 2018. The group also said it had cut output in August, giving the commodity a much-needed reprieve following the dip in demand seen as a result of the refineries closures in the US due to the hurricanes.

WTI crude was last trading up 0.4% on the day at $48.26 a barrel and Brent crude was 0.8% higher at $54.29 a barrel. The API's weekly inventory report expected later today should shed more light on the impact of the hurricanes on US stock levels.

Higher Inflation in UK May Force Bank of England to Raise Rates

The euro keeps falling against the US dollar due to increased interest in risky assets. Greenback bulls were supported by positive data from the NFIB small business index that improved to 105.3 in August against an expected decline to 104.8. At the same time, JOLTS Job openings report shows that the number of open vacancies in America in July grew to 6.17 million versus an anticipated decline to 5.96 million. Overall we are seeing positive tendencies from the labour market, which is likely to lead to wage growth and as a result to more consumer spending which remains the basis of economic expansion in the US.

Strong data from the UK pushed the GBP/USD price to the 1-year maximum. Traders reacted positively to the report on consumer price growth in August to 2.9% that is by 0.1% more than forecasted and higher than July's 2.6% rise in inflation. Sterling bulls were buoyed by the news as it increases the probability of hawkish rhetoric by Bank of England officials that will vote on interest rates on Thursday. Volatility for the pair is likely to remain high tomorrow on the background of British labour market data release.

The Australian dollar today was under pressure following the decline in the NAB business confidence index that in August dropped to 5 against 12 in July. Lower prices for commodities also have a negative impact on traders' sentiment. A slight spike in volatility is possible after the release of the Westpac report on Australia's consumer sentiment tomorrow at 00:30 GMT.

EUR/USD

The EUR/USD quotes were able to break through the inclined support line and overcoming the 1.1925 mark may become a confirmation for a sell signal with potential targets at 1.1825 and 1.1750. On the other hand, in case of the price crossing the SMA100 in the 15-minute chart, we may see growth resume with immediate goals at 1.2000 and 1.2070.

GBP/USD

The British pound demonstrated confident growth within the ascending channel and the recent break through the resistance at 1.3250 may result in a continued increase to the next target price at 1.3400. A change in trend is possible after leaving the limits of the channel and breaking through support at 1.3150. The MACD signal line is falling and that may be a signal for a continued downward correction to the lower limit of the channel.

AUD/USD

The AUD/USD resumed its decline after the recent rebound from the psychologically important 0.8000 mark. In case of breaking through this support line, the closest targets will be located at 0.7950 and 0.7870. In this case the stop should be set above the local maximum at 0.8050. It's not likely that we will see growth resuming today.

US: Small Business Confidence Remains Upbeat

The NFIB's small business optimism index rose 0.1 points to 105.3. The August headline print came in above market expectations, which called for a slight pullback to 104.9. Readings above the 105 level have been recorded only during select periods, such as in the mid-2000s and 1983, with today's print near record levels.

Movements among the sub-components were mixed with four posting a gain, five declining, and one remaining unchanged. Gains in expectations for higher sales led the way (+5 to 27 percent), followed by the belief that now is a good time to expand (+4 to 27 percent), and capital outlay plans (+4 to 32 percent). The latter marks the strongest reading since 2006. Moreover, earnings trends eased off one point but remained elevated at -11.

Most labor market indicators eased off on the month, but continued to hold up at a high level. Small businesses added jobs at a solid pace in August with the average change in employment per firm at +0.18 m/m, while plans to increase employment pulled back slightly (-1 to 18 percent). When stacked against past performance, both indicators are showing some of the best prints since the mid-2000s.

Job openings also pulled back, dropping 4 points on the month. But this followed a 5-point increase in the month prior, leaving the level of job openings at 31 percent - still one of the best showings since 2000. Over half of businesses seeking workers (52 percent) had few or no qualitied applicants, with 'quality of labor' concerns being the second most significant headwind to expansion (19 percent), right after taxes (20 percent).

Given already tight conditions, businesses continued to boost worker compensation (+1 to 28 percent). But plans to do so in the next three months pulled back for a second consecutive month, falling 1 point to 15 percent in August. The latter is still a decent reading but somewhat softer compared to the 18 percent recorded between March and June.

The net percent of owners raising average selling prices increased one point, rising to a net 9 percent - the highest level since 2014, while plans to do so in the near future fell back three points to a still-decent 20 percent.

Key Implications

Small business confidence has managed hold on to the post-election gains. While an improved view of future conditions has certainly played a part, the boost in optimism has not been solely due to a shift in the forward-looking indicators. In fact, businesses have also been reporting better nominal sales and earnings trends. This is in line with stronger demand and improved economic growth recently, particularly through the consumer spending channel.

The improvement in capital expenditure plans is particularly encouraging given that it marks the strongest reading since 2006. It appears that improved optimism is finally trickling down to investment intentions - a trend that if sustained is likely to boost business investment and lead to improved productivity.

On the other hand, the slightly softer trend in worker compensation plans is a disappointing signal for wage growth. Still, given increasingly tight labor market conditions, it is unlikely to continue. Moreover, the 'share of owners that are raising prices' that is now back at highest level since 2014 is another encouraging sign regarding inflation.

Disruptions from Hurricane Harvey do not appear to have played a large part in today's report, given that the storm made landfall in Southeast Texas late in the month. Nonetheless, we anticipate some distortions to the data ahead, with the added impact of Hurricane Irma to augment volatility. Overall, downbeat sentiment among affected businesses is likely to weigh on the headline measure in the near-term, with a subsequent boost to economic activity as reconstruction efforts and a gradual return to normalcy work in the opposite direction.

Pound Climbs to 12-Month High on Inflation Jump

The British pound has posted strong gains in the Tuesday session. In North American trade, GBP/USD is trading at 1.3264, up 0.80% on the day. On the release front, British CPI picked up speed, climbing 2.9% in August. This beat the estimate of 2.9%. In the US, JOLTS Job Openings improved to 6.17 million, easily beating the forecast of 5.96 million. On Wednesday, the UK releases wage growth, while the US will publish PPI.

The pound posted a strong gain of 1.7% last week, and the rally has resumed on Tuesday. Earlier in the Tuesday, session, the pair jumped to 1.3288, its highest level since September 2017. The pound was buoyed by strong inflation data, as CPI improved to 2.9% in August, up from 2.6% a month earlier. CPI, the primary gauge of consumer inflation, jumped on higher clothing and fuel prices. With inflation remaining above the BoE's target of 2.0%, policymakers will be under renewed pressure to raise interest rates. However, the economy has lost steam in 2017, and rate hike could hurt the economy. How will this play out at the BoE? Policymakers won't have much time to mull over the latest inflation readings, as the BoE holds its monthly policy meeting on Thursday. Whether the bank opts to raise rates or stay on the sidelines, traders should be prepared for some movement from the pound.

Bexit negotiations are grinding slowly, with plenty of major gaps between Britain and the European Union. Britain must take legislative measures to untangle itself from the continent, and the May government took a first step in that direction on Monday, as parliament voted on the EU Withdrawal Bill. The bill, which will convert all existing EU legislation into UK law, passed its second stage, with the government winning the vote by 326-290. However, the bill is far from done, with many MPs, including Conservatives, tabling amendments. Prime Minister May, still smarting from a disastrous June election, the vote is a small victory on the long journey of navigating Britain out of Brexit. The US economy has been performing well in the second quarter. Preliminary GDP came in at a sizzling 3.0%, and the labor market remains close to capacity. Still, the Achilles heel of the economy remains stubbornly low inflation levels. Wage pressure has been limited, despite the fact that many businesses cannot fill job openings. Weak inflation has hampered the Fed's plans to raise interest rates a third time this year, and the odds of a December hike have dipped to just 31%, as the markets are increasingly doubtful that the Fed will make a move before next year. Will the inflation picture improve? We could see better numbers this week for August inflation – PPI is expected to improve to 0.3% on Tuesday, and the same gain is forecast for CPI on Wednesday. Both estimates are higher than the July readings.

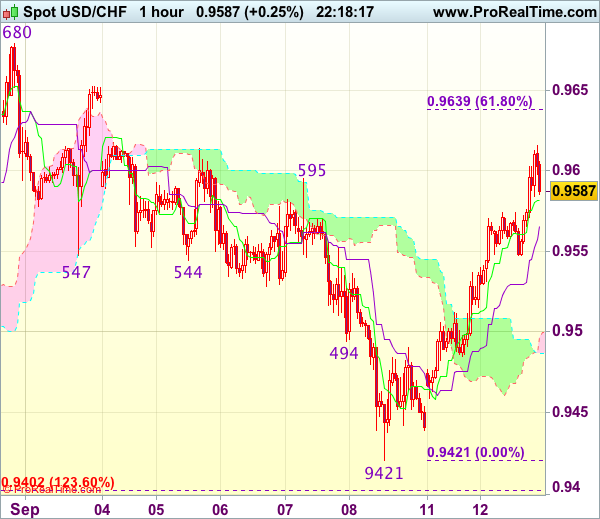

Trade Idea Wrap-up: USD/CHF – Buy at 0.9540

USD/CHF - 0.9592

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 0.9582

Kijun-Sen level : 0.9566

Ichimoku cloud top : 0.9500

Ichimoku cloud bottom : 0.9487

Original strategy :

Buy at 0.9550, Target: 0.9650, Stop: 0.9515

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9540, Target: 0.9640, Stop: 0.9505

Position : -

Target : -

Stop : -

The greenback extended the rebound from 0.9421 (last week’s low) in line with our bullish expectations, this anticipated rise together with the breach of previous resistance at 0.9595 add credence to our view that low has been formed at 0.9421 and consolidation with upside bias remains for further gain to 0.9635-40 (61.8% Fibonacci retracement of 0.9773-0.9421), however, near term overbought condition would limit upside and reckon resistance at 0.9680 would remain intact.

In view of this, we are looking to reinstate long on dips as 0.9550-55 should limit downside and bring another upmove later. Below 0.9525-30 would defer and risk correction to 0.9500 but downside should be limited and 0.9450-60 would remain intact, bring another rebound later.

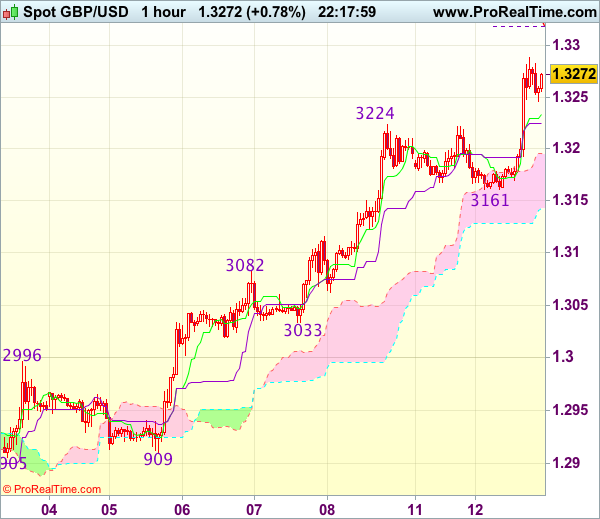

Trade Idea Wrap-up: GBP/USD – Buy at 1.3175

GBP/USD - 1.3266

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3241

Kijun-Sen level : 1.3225

Ichimoku cloud top : 1.3195

Ichimoku cloud bottom : 1.3143

Original strategy :

Buy at 1.3175, Target: 1.3275, Stop: 1.3140

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.3175, Target: 1.3275, Stop: 1.3140

Position : -

Target : -

Stop : -

Cable’s intra-day breach of previous chart resistance at 1.3269 confirms medium term upmove has resumed and bullishness remains for further gain to 1.3290-00, however, loss of near term upward momentum should prevent sharp move beyond 1.3330 and reckon 1.3350-60 (61.8% projection of 1.2909-1.3224 measuring from 1.3161) would hold from here, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise at current level and would be prudent to buy cable on subsequent pullback as support at 1.3161 should contain downside and bring another upmove. Below 1.3145-50 would defer and risk correction to 1.3115-20 but downside should be limited and support at 1.3082 (previous resistance) should remain intact.