Sample Category Title

BoC Sends CAD Soaring With Shock Rate Hike

Does the BoC Have More Hikes in Store?

The Bank of Canada unexpectedly raised interest rates on Wednesday by 25 basis points, triggering a sharp appreciation in the Canadian dollar and taking it to more than two-year lows against the greenback.

Having only raised interest rates for the first time since 2010 at the last meeting, traders were clearly of the belief that the BoC would hold off today and take a more cautious approach to tightening. Especially as there appeared no urgent need to do so, with inflation still well below target at 1.2%. Clearly policy makers at the central bank did not share this view, raising the overnight target rate to 1% and citing the stronger than expected economy in the process.

Interestingly, the BoC did also reference elevated household indebtedness and the impact that these rate rises could have on it. Perhaps the role of the consumer in the strong performance of the economy, driven by debt, is at least part of the reason the central bank is taking such pre-emptive action, despite price pressures not warranting it.

Given how sudden and drastic - by recent standards - the BoC's moves have been, traders may now be wondering what more we can expect from the central bank. Today's rally in the loonie may not just represent surprise at this particular decision but also a recalculation of what the central bank may do going forward. Two rate hikes in a row after such a sustained period of none is a bold move and traders may now be expecting more in the months ahead.

USDCAD

GBPCAD

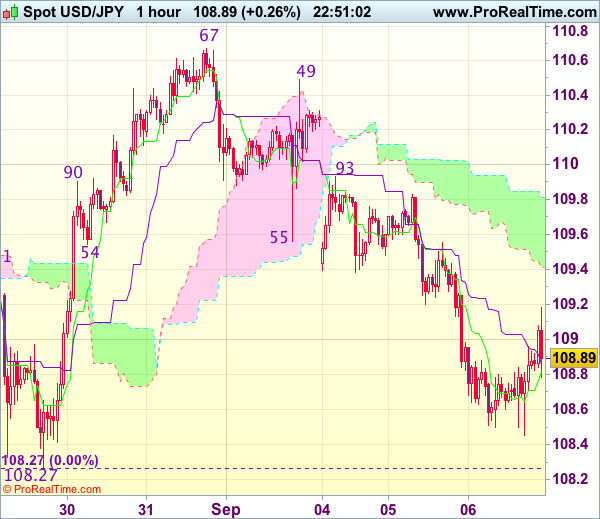

Trade Idea Wrap-up: USD/JPY – Sell at 109.55

USD/JPY - 108.88

Most recent candlesticks pattern : N/A

Trend : Sideways

Tenkan-Sen level : 108.82

Kijun-Sen level : 108.86

Ichimoku cloud top : 109.81

Ichimoku cloud bottom : 109.41

Original strategy :

Sell at 109.40, Target: 108.40, Stop: 109.75

Position : -

Target : -

Stop : -

New strategy :

Sell at 109.55, Target: 108.55, Stop: 109.90

Position : -

Target : -

Stop : -

As dollar has recovered after falling to 108.45, suggesting consolidation above this level would be seen and corrective bounce to 109.40 cannot be ruled out, however, reckon upside would be limited to 109.55-60 and bring another decline, below said support would extend weakness towards last week’s low at 108.27 but break there is needed to retain bearishness and extend the fall from 114.50 to another previous chart support at 108.13, having said that, the greenback needs to penetrate this chart support to confirm early selloff from 118.66 has resumed for subsequent weakness to 107.70-75 which is likely to hold from here.

In view of this, we are looking to sell dollar on further recovery as 109.55-60 should limit upside and bring another decline later. Above 109.80-83 would abort and signal low is formed instead, bring a stronger rebound to 110.00-05 but price should falter well below resistance at 110.49.

BOC Surprisingly Hikes Rate For Second Consecutive Meeting

In a surprising move, BOC increased the policy rate by +25 bps to 1% in September, following a rate hike in July. Policymakers cited the better-than-expected economic developments as a key reason for the removal of stimuli from the market. However, they remained cautious over a number of issues including excess capacity, subdued inflation, geopolitical risks and the strength in Canadian dollar. On the future tightening path, the central bank stressed that it is "not predetermined" and "will be guided by incoming economic data and financial market developments as they inform the outlook for inflation". We believe the progress of NAFTA renegotiations and other trade-related issues, the inflation outlook, the housing market developments and the Fed's balance sheet reduction would be key factors driving BOC's rate decision.

Real GDP growth accelerated to +4.5% in 2Q17, form +3.7% in the prior quarter, marking the best 4-quarter performance since 2006 and well above BOC's estimate of 3%. Contribution to growth came mainly from private consumption and gross capital formation. As BOC noted in the accompanying statement, "recent economic data have been stronger than expected, supporting the Bank's view that growth in Canada is becoming more broadly-based and self-sustaining". It also acknowledged that consumer spending was robust. Yet, BOC maintained a cautious note, signaling "a moderation in the pace of economic growth in the second half of 2017".

While admitting weak inflation, policymakers acknowledged "a slight increase in both total CPI and the Bank's core measures of inflation, consistent with the dissipating negative impact of temporary price shocks and the absorption of economic slack". They continued to caution over the "excess capacity" in the job market, as well as the subdued growth in "wage and price pressures"

While raising the policy rates for two consecutive meetings, BOC stressed that "future monetary policy decisions are not predetermined and will be guided by incoming economic data and financial market developments as they inform the outlook for inflation". It emphasized that "particular focus will be given to the evolution of the economy's potential", the "labour market conditions" and "the sensitivity of the economy to higher interest rates".

Outlook

In our opinions, BOC's future monetary decision would be dependent on the following issues. First, the third and fourth rounds of NAFTA renegotiations would take place in end-September and end-October respecitlvely. The highly uncertain outcomes signal the centla bank would be cautious. As an export-oriented economy with the US the biggest trading partner, the new trade relations would affect Canada's economic growth outlook. Exchange rate would be closely watched too. Although Canadian dollar has risen about +8% against US dollar since the beginning of the year, the trade-weighted index is still not elevated. Therefore, we do not see exchange rate a threat to the coutry's exports for now. Second, although BOC noted the imporvement in inflation, both headline and core readings have styaed far below the +2% target. Further stregnth in the loonie might cotinue to weigh on inflaiton. Third, there have been signs of a softer housing market as a report by tge Canadian Real Estate Association shows that national home sales dropped for a fourth consecutive month, by-2.1% m/m in July. Finally, BOC would be paying close attention to the Fed balance sheet reduction plan. In July, the Fed indicated that balance sheet reduction would begin "relatively soon". We expect a formal announcement would come in the upcoming meeting on September 20.

Dollar Struggles, But Few Additional Losses

- European equities opened weaker today, copying yesterday's weakness on Wall Street, but turned positive afterwards in an uneventful trading session. US stock markets gain around 0.3% at the start of dealings.

- US Non-manufacturing ISM rebounded in August to 55.3 from 53.9 in July when the index fell sharply. The outcome was near expectations.

- Bank of Canada raised its official rate for a second meeting in a row to 1% from 0.75%. Consensus was divided over the outcome. As a result in a first reaction the Canadian dollar rose 2 big figures against the US dollar.

- Hungary and Slovakia suffered blows as the EU's top court dismissed their objections to the EU's refugee quota plan, paving the way for an intensifying conflict between Brussels and eastern member states who have ruled out complying with the law.

- Germany's finance minister has called for the ECB to dump its bond buying programme and negative interest rates, saying the eurozone's recovery was now strong enough to support a return to "normal" monetary policy.

- The Catalan parliament is expected to approve plans for a referendum to break away from Spain, setting it on a collision course with the Spanish government which has vowed to stop it. Lawmakers are set to vote on the law approving an October 1 referendum in the coming hours, and it is likely to be approved as the pro-independence parties have a majority in the regional parliament.

- France plans to pass legislation by the end of 2017 to phase out all oil and gas exploration and production on its mainland and overseas territories by 2040, becoming the first country to do so, according to a draft bill presented on Wednesday.

- Hurricane Irma, one of the most powerful Atlantic storms in a century, churned across northern Caribbean islands with a potentially catastrophic mix of fierce winds, surf and rain, en route to a possible Florida landfall at the weekend.

Rates

Waiting game

Global core bonds lost slightly ground today with Bunds marginally underperforming US Treasuries. Positively oriented stock markets after a weak opening and a surge in oil prices ($53/barrel to $54/barrel) explain the (modest) decline. Rumours about an explosion near North Korea caused a temporary hick-up, but it was rapidly erased. The EMU eco calendar was empty while a smaller than forecast US Trade deficit didn't bother traders. The upcoming US non-manufacturing ISM and Bank of Canada rate decision remain wildcards, but ahead of tomorrow's ECB meeting many investors will probably remain sidelined.

At the time of writing, the German yield curve bear flattens with yields up to 1.6 bps (2-yr) higher. US yields shift up to 0.8 bps (10-yr) higher. From a technical point of view, the US 5-yr (1.69%), 10-yr (2.10%) and 30-yr (2.68%) yields fail to regain yesterday's lost support levels for now. On intra-EMU bond markets, 10-yr yield spreads versus Germany are nearly unchanged with Spain slightly underperforming (+2 bps) ahead of tomorrow's auction.

The German Finanzagentur tapped the on the run 5-yr Bobl (€3B 0% Oct2022). Total bids amounted to €3.94B, slightly above the €3.7B average at the previous 4 Bobl auctions. This amount of bids remains rather low. The Bundesbank set aside €0.56B for secondary market operations resulting in an official bid cover 1.6. The auction tailed 1 cent.

Currencies

Dollar struggles, but few additional losses

The dollar remains in the defensive across the board as global uncertainty and political noise from Washington deprive the US currency from highly needed interest rate support. That said, for now, the US currency hasn't broken any technically relevant levels yet. EUR/USD trades in the 1.1935 area. USD/JPY hovers in the high 108 area.

This morning, Asian equities traded mixed to slightly lower, but the losses were limited given the volatility in the US yesterday. The yen held near recent highs against the dollar (108.65/70 area). EUR/USD showed no consistent reaction on recent global uncertainty. The pair was little changed at around 1.1915. Other euro cross rates (EUR/JPY, EUR/GBP, …) felt some stronger headwinds.

In Europe, there was again no dominant theme to guide trading in the major USD or euro cross rates. Several economic and non-economic issues (Korea, US political and budget issues, tomorrow's ECB decision) swirled and clouded investors' outlook. There was no clear cross market directional trend. German factory orders were slightly softer than expected, but this wasn't the market's focus. The US trade deficit was almost as expected. Global uncertainty caused European markets to open with a slight risk-off bias. Core yields held near the recent lows but didn't decline any further. The same applies for USD/euro interest rate differentials. Global uncertainty kept the dollar in the defensive against the euro and the yen. USD/JPY hovered in the mid 108 area in early European dealings, but regained a few ticks as equity sentiment improved slightly later in the session. EUR/USD kept a cautious upward bias and settled in the lower half of the 1.19 big figure. The recent top (low of the dollar) remains on the radar.

After the close of this report, the US non-manufacturing ISM will be published. Later this evening, the Fed's Beige book is scheduled for release. For now, the assessment on the dollar hasn't changed. The US currency remains in the defensive. Good eco data might help, but the dollar needs renewed interest rate support and an easing in global and domestic (political) uncertainty. On the euro side of the story, the question is whether Draghi can/wants to convince markets that a strong euro will cause a slower path of ECB policy normalisation. This last question should be answered by tomorrow evening.

Sterling technical rebound continues

There was again hardly any economic news from the UK. Over the previous days, no news was good enough news to support a technical sterling rebound and this pattern continued today. EUR/GBP held near the recent lows even as EUR/USD remains well bid. EUR/GBP trades in the 0.9140 area. Sterling also gained a few more ticks against the dollar. Cable trades in the mid 1.30 area. There was again plenty of Brexit noise from politicians on both sides of the English channel. However, it didn't prevent a further sterling short squeeze.

BoC: Robust Data Drives Poloz to Tighten

Markets had put the odds of a rate hike this morning at about 50/50, but in the event, the Bank of Canada increased its key overnight lending rate 25bp, to 1.00%. Unsurprisingly, the short statement accompanying the decision struck a decidedly hawkish tone.

Recent economic data have been stronger than the Bank of Canada expected, and growth is seen as becoming "self-sustaining". Strength in all major expenditure categories, except housing, has left the level of output above the Bank's previous expectations. Global growth is seen as becoming more synchronized, although uncertainties persist.

That statement did acknowledge that excess capacity remains in labour markets, and that wage and price pressures are more subdued than historical relationships would suggest.

The Bank of Canada ultimately decided that the removal of some of the "considerable" monetary stimulus was warranted, but added that future rate moves are not predetermined, and will depend on how incoming data and financial market developments are likely to affect the path for inflation. Moreover, the Bank also acknowledged the level of the loonie, and the sensitivity of the economy to rising rates in the context of elevated indebtedness.

Key Implications

Today's decision could have easily gone either way, but the robust run of economic growth left the Bank of Canada moving to remove some of the stimulus right away, rather than waiting for the communication opportunities that would have been afforded at their next decision, six weeks from now.

Indeed, Canada's economy has been coming in hot of late, with emergency level interest rates no longer warranted. While an argument could be made that holding off a few weeks for the opportunity to more fulsomely explain how the outlook for the economy has evolved, this clearly did not hold sway in Ottawa today.

Interestingly, the short statement included an explicit reference to the recent appreciation of Canadian dollar (which rose further in the wake of the announcement, resulting in a roughly 3% rise against the U.S. dollar over the past month, or a nearly 14% climb from the April low). This somewhat unusual inclusion suggests that currency moves will be monitored closely as part of the data dependency expressed again today.

Indeed, the evolution of the outlook will be crucial for the future path of the policy interest rate. With slowing but still above-potential growth likely, this implies that absent a significant shock, today's rate increase will be part of a larger and longer march towards interest rate normalization.

BoC Hikes Rates, Flatfoots the Market

BoC flat footed the market and hiked +25 bps to +1% on stronger growth data.

Canadian Q2 data warranted the removal of "considerable" stimulus from the economy.

This marked the second consecutive meeting that the BoC has increased its main interest rate, after being on hold for seven years.

The market had expected Governor Poloz to leave its policy rate unchanged, while signalling gradual rises over the coming quarters. Recent indicators, such as Q2 GDP rose by a whopping + 4.5% annualized rate in the April-to-June period, support "the bank's view that growth in Canada is becoming more broadly-based and self-sustaining ."

The loonie quickly printed a new two-year high (C$1,2140) outright following the surprise rate hike.

The chance of a rate hike today was viewed as a coin toss. The BoC noted that geopolitical risks and uncertainties around international trade have led to a weaker U.S dollar, while helping to appreciate the Canadian dollar.

U.S. Trade Deficit Broadly Unchanged in July

The U.S. international trade deficit remained broadly unchanged in July, widening slightly to $43.7 bn (market consensus $44.6bn). June's data was revised very little, with the trade deficit slightly smaller than previously reported ($43.5 bn versus $43.6 bn previously).

After two months of gains, exports fell back 0.3% on a month-on-month (m/m) basis in July. Declines in automotive (-4.4%) and consumer goods (-4.1%) worked to offset gains in food and beverage (+3.0%) and capital goods (+2.1%). Services exports fell 0.2% in July, the first monthly decline of 2017.

Imports declined for the third consecutive month in July, falling 0.2% m/m. Declines in automotive (-2.7%) and industrial supplies (-1.7%) worked to offset gains in food and beverage imports (+1.7%) and capital goods (+2.4%). Service imports were unchanged.

Adjusting for price changes, export volumes fell 0.6%, partially reversing gains in the past two months. The volume of imports was unchanged in July.

Trade deficits with its major trading partners shifted in composition in July, as the widening in the trade deficit in dollar terms with Canada was more than offset by a narrowing of the trade deficit with Mexico. On a year-to-date basis, U.S. maintains the largest trade deficits with China (-$204 bn), Europe (-$96.3 bn), and Mexico ($-41.2 bn).

Key Implications

Today's trade report erases some of the optimism on exports that the past two trade reports implied for the third quarter. Nevertheless, given a continuation of subdued growth in import volumes, net trade is on track to contribute positively to economic activity for the third consecutive quarter. Strong global demand is likely helping to boost foreign demand for U.S. goods, and a weaker U.S. dollar in trade-weighted terms should provide some support in upcoming months.

Hurricane Harvey will likely contribute to volatility in trade statistics in upcoming months, particularly concerning petroleum imports and refinery exports. However, any trade-related impacts are likely to be contained to the third quarter.

NAFTA renegotiations are just one of a few uncertainties that cloud the outlook for trade. Recent media reports suggest that NAFTA renegotiation is proceeding at a slower than anticipated pace, leaving it highly uncertain that the U.S. administration can conclude negotiations before year-end. Moreover, threats of a complete withdrawal from NAFTA, even if only temporary, only works to layer further uncertainty upon a world dealing with elevated geopolitical tensions. Policy and economic uncertainty has been linked to a lower propensity of businesses to invest in new machinery and equipment. As such, it implies that a prolonged period of uncertainty may in fact be deterring firms from making the necessary investments to improve their productivity.

Trade Idea: EUR/GBP – Sell at 0.9210

EUR/GBP - 0.9136

Original strategy :

Sell at 0.9265, Target: 0.9115, Stop: 0.9305

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9265, Target: 0.9115, Stop: 0.9305

Position : -

Target : -

Stop : -

As euro’s retreat from 0.9307 (last week’s high) has kept price under pressure, adding credence to our view that temporary top has possibly been formed there and consolidation with mild downside bias is seen for correction of recent upmove to 0.9095-00 (50% Fibonacci retracement of 0.8892-0.9307, however, near term oversold condition should prevent sharp fall below 0.9050 (61.8% Fibonacci retracement) and price should stay well above support at 0.9008.

In view of this, we are inclined to sell euro on recovery as 0.9210-20 should limit upside. Above 0.9240-50 would suggest low is formed instead, bring a stronger rebound to 0.9270 but only above said resistance at 0.9307 would revive bullishness and extend recent upmove to 0.9325-30 and possibly towards 0.9350, however, loss of upward momentum should limit upside and price should falter below 0.9390-00.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Canada’s Trade Deficit Narrowed But Still Wide in July

Highlights:

- Canada's nominal merchandise trade deficit improved to $3.0 billion in July.

- Much of both a 4.9% export drop and 6.0% import drop reflected lower prices although both also declined in volume terms.Non-energy export volumes were down from a year-ago for the first time since February. Import volumes were still up 5.0% from last July with the year-over-year gain led by the equipment components.

Our Take:

The July deficit improved slightly more than markets expected ahead of the report but the $3.0 billion shortfall is still historically large. Part of a 1.6% drop in July export volumes reflected transitory factors with traditional July factory shutdowns in the auto sector lasting longer than usual this year. Nonetheless, the drop leaves early risk that export growth in Q3 will retrace at least part of a 10% (annualized) Q2 gain with non-energy export volumes falling below year-ago levels for the first time since February. The import picture was more encouraging. Overall import volumes fell 2.5% in July but with most of the drop from a large 33% decline in the often-volatile aircraft component. Overall import volumes were still up 5.0% from a year ago. That increase subtracts from the net trade balance but is a positive indicator for domestic demand. Import growth has been encouragingly led by Industrial and electrical equipment imports which both rose further in July and were up 13% from a year ago. That provides further evidence that business investment growth in the first half of the year extended into Q3.

Weakness in exports - were it to persist - could be a concern for the Bank of Canada but the data is volatile and the import data remains consistent with a stronger domestic economic backdrop, particularly for business investment. We continue to think the economy looks strong enough to absorb further rate hikes, although we expect the next 25 basis point increase will come in October rather than in the Bank of Canada's rate announcement later this morning.

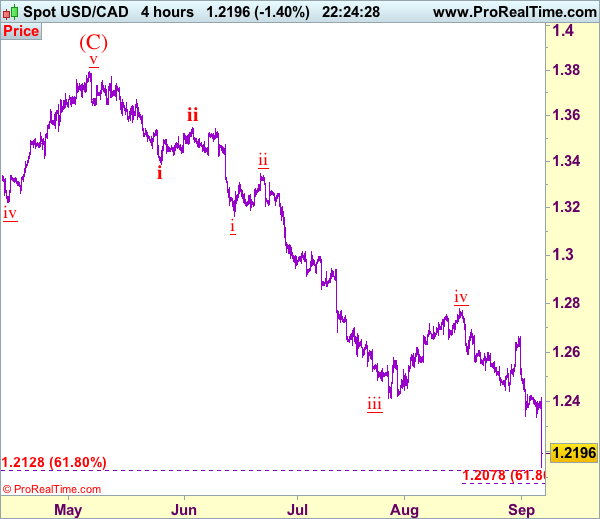

Trade Idea: USD/CAD – Sell at 1.2285

USD/CAD - 1.2206

Trend: Down

Original strategy :

Sell at 1.2490, Target: 1.2340, Stop: 1.2550

Position: -

Target: -

Stop: -

New strategy :

Sell at 1.2285, Target: 1.2100, Stop: 1.2345

Position: -

Target: -

Stop:-

Current selloff adds credence to our bearish view that recent decline is still in progress and downside bias remains for this wave v of larger degree wave iii to extend weakness to 1.2125-30, then 1.2100, however, near term oversold condition should prevent sharp fall below 1.2075-80 (61.8% projection of 1.3547-1.2414 measuring from 1.2778) and price should stay above psychological support at 1.2000, bring rebound later. We are keeping our count that wave v as well as wave (C) ended at 1.3794 and impulsive wave (i ii, i ii) is now unfolding with minor wave iii ended at 1.2414, followed by wave iv correction ended at 1.2778, wave v has reached our initial downside target at 1.2200 and may extend to 1.2100.

In view o this, would not chase this fall here and would be prudent to sell on recovery as 1.2290-00 should limit upside. Above 1.2335-40 would defer and risk a stronger rebound to 1.2390-00 but only break of resistance at 1.2429 would signal low is formed, bring retracement of recent decline to 1.2490-00.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.