Sample Category Title

Canadian Dollar Soars on Surprised BoC Rate Hike

Canadian Dollar soars sharply in early US session after BoC shocked the markets by raising overnight rate by 25bps to 1.00%. Correspondingly, the Bank rate is lifted to 1.25% and deposit rate to 0.75%. While there were speculations of a rate hike, markets generally believed that BoC will hold their hands till October, as it has just raised interest rate back in July. Nonetheless, after the rate hike, BoC remains open to further tightening It noted that "future monetary policy decisions are not predetermined and will be guided by incoming economic data and financial market developments as they inform the outlook for inflation." Meanwhile, it doesn't sound concerned with strength of the Canadian Dollar as it is "reflecting the relative strength of Canada's economy."

BoC noted that "recent economic data have been stronger than expected, supporting the Bank's view that growth in Canada is becoming more broadly-based and self-sustaining." While BoC still anticipate moderation of growth in second half, "the level of GDP is now higher than the Bank had expected." Inflation remains below 2% target but recent pick up is "consistent with the dissipating negative impact of temporary price shocks and the absorption of economic slack." Overall, given the stronger-than-expected economic performance, Governing Council judges that today's removal of some of the considerable monetary policy stimulus in place is warranted.

Germany piles up pressure for ECB stimulus exit

Just ahead of the highly anticipated ECB policy decision and press conference. Germany is piling up pressure for the central bank to start exiting its massive stimulus. German Finance Minister Wolfgang Schäuble said that "unusual monetary policy implies it is not usual or normal - we should get back to a normal monetary policy." And he also pointed out that "we have come back to a normal situation much quicker than people thought."

Deutsche Bank chief executive John Cryan called on the central bank to end the ultra low interest rate policy. He urged in a conference that "the era of cheap money in Europe should come to an end – despite the strong euro." He pointed out that "the real economy is doing well, the market is expecting I think an increase in interest rates or a reduction in the negative nature of interest rates… Let's start doing that."At the same time, ECB's policies has battered bank's profitability for some time. And Cryan said that "it can't be forever that deposit taking is a loss making… for banks."

UK post immigration plan attracts criticism

In UK, the leaked document regarding the government's post-Brexit immigration plan attracted much criticism from businesses. The chief executive of the British Hospitality Association, Ufi Ibrahim, warned that "if these proposals are implemented it could be catastrophic for the UK hospitality industry." Director general of Food and Drink Federation said that "if this does represent the government's thinking it shows a deep lack of understanding of the vital contribution that EU migrant workers make – at all skill levels – across the food chain." Manufacturers' organization EEE's director of employment and skills said "we would have grave concerns that at lower skill levels accessing EU workers will be on a completely different basis." CBI managing director for people and infrastructure Neil Carberry urged that "an open approach to our closest trading partners is vital for business, as it attracts investment to the UK."

A draft document on UK's plan for post-Brexit immigration system was leaked to the Guardian and published. The proposals in the document are to be endorsed by ministers and subject to negotiation with EU. But it's also triggered much controversies as some believed that it targets low skilled EU migrants. Some MPs reacted furiously to the document as criticized it as a "mean and cynical approach". Chair of the home affairs select committee Yvette Copper said the document "seems to contradicts the home secretary's decision just over a month ago". Meanwhile, German MEP Elmar Brok, who's one of European Parliament's Brexit officials, warned that the proposal will " increase the lack of credibility and deepen mistrust". It would make it even harder to reach agreement on divorce by October.

Form currency head Watanabe urges BoJ not to be caught by 2% target

In Japan, former currency head at the Finance Ministry, Hiroshi Watanabe, said that there is no reason for BoJ to wait for inflation to hit target before exiting stimulus. And he criticized that BoJ is "caught on its own trap by insisting inflation has to exceed 2 percent on a consistent basis." He pointed out that the 2% target "isn't legally binding", and it's not something BoJ should "strictly adhere to". He said that "just as an endless intravenous drip becomes ineffective, monetary policy should be changed to reduce stimulus once the economy is no longer facing any headwinds." And that would create a "buffer for future needs". Watanabe emphasized that "there is absolutely no reason to deter such a decision by saying we have to wait for inflation to reach 2 percent."

On the data front

US ISM services rose to 55.3 in August, up from 53.9 but missed expectation of 55.5. Trade deficit widened slightly to USD -3.7b in July. Canada trade deficit narrowed to CAD -3.0b in July. Labor productivity dropped -0.1% qoq in Q2. Eurozone retail PMI dropped to 50.8 in August. German factory orders dropped -0.7% mom in July. Japan labor cash earnings dropped -0.3% yoy in July. Australia GDP grew 0.8% qoq in Q2, in line with expectation.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2333; (P) 1.2375; (R1) 1.2415; More....

USD/CAD dives to as low as 1.2146 after BoC rate hike, as recent decline extends. Intraday bias stays on the downside. Fall from 1.3793 should target target next long term fibonacci level at 1.2048. Downside momentum as seen in daily MACD is picking up again. Firm break of 1.2048 will carry larger bearish implication and target 61.8% projection of 1.3793 to 1.2412 from 1.2777 at 1.1924 next. On the upside, above 1.2335 minor resistance will turn intraday bias neutral first. But out look will remain bearish as long as 1.2662 resistance holds.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. Such corrective fall is expected to extend to 50% retracement of 0.9406 to 1.4869 at 1.2048. At this point, we'd look for strong support from there to contain downside and bring rebound. Break of 1.2777 resistance will indicate reversal and turn outlook bullish for 1.3793 key resistance. However, sustained break of 1.2048 will dampen this view and carry larger bearish implications and bring deeper decline to 61.8% retracement at 1.1424 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | JPY | Labor Cash Earnings Y/Y Jul | -0.30% | 0.50% | -0.40% | |

| 01:30 | AUD | GDP Q/Q Q2 | 0.80% | 0.80% | 0.30% | |

| 06:00 | EUR | German Factory Orders M/M Jul | -0.70% | 0.20% | 1.00% | 0.90% |

| 08:10 | EUR | Eurozone Retail PMI Aug | 50.8 | 51 | ||

| 12:30 | CAD | Labor Productivity Q/Q Q2 | -0.10% | 0.90% | 1.40% | 1.30% |

| 12:30 | CAD | International Merchandise Trade (CAD) Jul | -3.0B | -3.8B | -3.6B | -3.8B |

| 12:30 | USD | Trade Balance Jul | -43.7B | -44.6B | -43.6B | -43.5B |

| 13:45 | USD | US Services PMI Aug F | 56 | 56.9 | 56.9 | |

| 14:00 | CAD | BoC Rate Decision | 1.00% | 0.75% | 0.75% | |

| 14:00 | USD | ISM Services/Non-Manufacturing Composite Aug | 55.3 | 55.5 | 53.9 | |

| 18:00 | USD | Federal Reserve Beige Book |

(BOC) Bank of Canada Increases Overnight Rate Target to 1 Per cent

The Bank of Canada is raising its target for the overnight rate to 1 per cent. The Bank Rate is correspondingly 1 1/4 per cent and the deposit rate is 3/4 per cent.

Recent economic data have been stronger than expected, supporting the Bank's view that growth in Canada is becoming more broadly-based and self-sustaining. Consumer spending remains robust, underpinned by continued solid employment and income growth. There has also been more widespread strength in business investment and in exports. Meanwhile, the housing sector appears to be cooling in some markets in response to recent changes in tax and housing finance policies. The Bank continues to expect a moderation in the pace of economic growth in the second half of 2017, for the reasons described in the July Monetary Policy Report (MPR), but the level of GDP is now higher than the Bank had expected.

The global economic expansion is becoming more synchronous, as anticipated in July, with stronger-than-expected indicators of growth, including higher industrial commodity prices. However, significant geopolitical risks and uncertainties around international trade and fiscal policies remain, leading to a weaker US dollar against many major currencies. In this context, the Canadian dollar has appreciated, also reflecting the relative strength of Canada's economy.

While inflation remains below the 2 per cent target, it has evolved largely as expected in July. There has been a slight increase in both total CPI and the Bank's core measures of inflation, consistent with the dissipating negative impact of temporary price shocks and the absorption of economic slack. Nonetheless, there remains some excess capacity in Canada's labour market, and wage and price pressures are still more subdued than historical relationships would suggest, as observed in some other advanced economies.

Given the stronger-than-expected economic performance, Governing Council judges that today's removal of some of the considerable monetary policy stimulus in place is warranted. Future monetary policy decisions are not predetermined and will be guided by incoming economic data and financial market developments as they inform the outlook for inflation. Particular focus will be given to the evolution of the economy's potential, and to labour market conditions. Furthermore, given elevated household indebtedness, close attention will be paid to the sensitivity of the economy to higher interest rates.

Information note

The next scheduled date for announcing the overnight rate target is October 25, 2017. The next full update of the Bank's outlook for the economy and inflation, including risks to the projection, will be published in the MPR at the same time.

Canada’s Trade Deficit Narrowed in July

Canada's trade deficit narrowed to $3.0B in July (from $3.8B in June), as the 6% drop in imports outpaced the 4.9% decline in exports. In real terms, imports were down 2.3%, while exports slid by 1.1%.

The decline in exports was widespread, led by aircraft (-18%) and motor vehicles and parts (-10%). Metal ores and non-metallic minerals (+12%) was the only commodity group to record a rise during the month.

The drop in imports was also broad based, with aircraft (-35%), metal ores and non-metallic minerals (-19%) and energy products (-15%) all recording double digit declines during the month.

Canada's trade surplus with the U.S. widened to $2.9B in July (from $1.8B), as imports (-6.7%) fell more than exports (-3.2%). Canada's trade deficit with the rest of the world rose to $5.9B (preciously $5.6B) as exports were down 10% and imports slid 4.7%.

Key Implications

Export volumes have fallen for two consecutive months now, which provides a weak handoff for the third quarter. Overall, Q3 growth is tracking about 2.4% now. This is a marked deceleration from the robust 4.5% seen in Q2, but is still a solid pace of growth.

Going forward, while the recent strength in the Canadian dollar, which has pushed just above 80 US cents, has somewhat reduced competitiveness of Canadian exporters, demand for Canadian-made goods should gain some support from healthy U.S. economic growth. Of course NAFTA negotiations pose some risk to the future trade relationship between Canada and the U.S., however, it appears as though a deal is still a long way off.

All told, the Canadian economy is still going strong and we expect the Bank of Canada to continue its rate hiking cycle. While a move is possible this morning, we expect the Bank will hold off until October.

CAC Ticks Higher as Investors on Sidelines Ahead of ECB Decision

The CAC index continues to have a quiet week. Currently, the index is at 5,094.30, up 0.15% on the day. On the release front, German Factory Orders dropped 0.7%, well off the forecast of a 0.2% gain. Eurozone Retail PMI edged lower to 50.8 points. On Thursday, the ECB holds a policy meeting and will release a rate statement, followed by a press conference with ECB President Mario Draghi. As well, France publishes Trade Balance and the eurozone releases Revised GDP.

The streaking euro remains close to the symbolic 1.20 level, and has gained 13% against the dollar in 2017, with two main reasons for the appreciation. First, economic growth has rebounded this year, led by robust growth in Germany. Second, there is increasing speculation that the ECB will taper its asset purchase program (QE), which is scheduled to terminate in December. The ECB is yet to decide what to do next, and analysts do not the details of the new program to be announced until October or possibly December. ECB policymakers must weigh competing interests – Germany would like nothing more than the ECB to simply exit the program, which was brought in as an emergency measure to begin with. However, France and other eurozone members, which are not enjoying German-style growth, favor a gradual tapering of the program, perhaps lowering monthly asset purchases from EUR 60 billion to EUR 45 billion. The stronger euro is equivalent to a raise in interest rates and has resulted in monetary tightening, so the ECB may favor a slow exit. Aside from the headache of a stronger euro, ECB policymakers must wrestle with the dilemma of a stronger economy that remains gripped by very low inflation. Will the ECB address these concerns at the Thursday meeting? Any hints about a change in monetary policy could have a sharp impact on European stock markets.

Britain's departure from the European Union promises to have a significant impact on the Eurozone financial sector, and stock markets will also be affected. One issue under discussion relates to clearing houses based in Britain, specifically over euro-denominated trades. The European Commission is working on a draft law that would see joint supervision between the EU and Britain over such transactions, but France wants the European Securities and Markets Authority (ESMA) to have greater authority, such as a veto, over these transactions. This is one more example of the immense difficulty in untangling the British financial sector from the continent, and there will likely be intense wrangling between the two sides at the Brexit negotiations. as Britain tries to minimize the damage to London, which is set to lose its status as the premier financial hub in Europe.

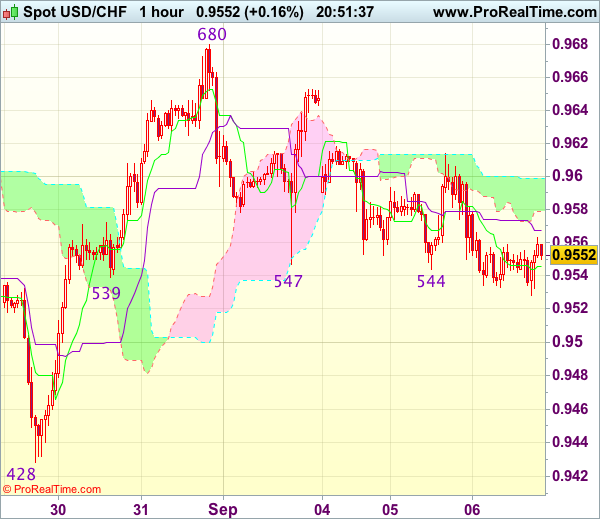

Trade Idea Update: USD/CHF – Buy at 0.9500

USD/CHF - 0.9554

Original strategy :

Buy at 0.9500, Target: 0.9600, Stop: 0.9465

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9500, Target: 0.9600, Stop: 0.9465

Position : -

Target : -

Stop : -

As the greenback has remained under near term pressure and consolidation with initial downside bias remains, hence weakness to 0.9520-25 cannot be ruled out, however, if our view that low has been formed at 0.9428 last week is correct, downside would be limited to 0.9500 and bring another rebound later. Above 0.9615-20 would suggest low is possibly formed, bring test of 0.9653-55 resistance, break there would bring another rise to 0.9680 but break there is needed to add credence to this view and extend gain to resistance at 0.9698-99.

In view of this, we are inclined to buy dollar on further subsequent decline. Below 0.9490-00 would risk weakness to 0.9470 but still reckon downside would be limited to 0.9450 and said support at 0.9428 should remain intact, bring another rebound later.

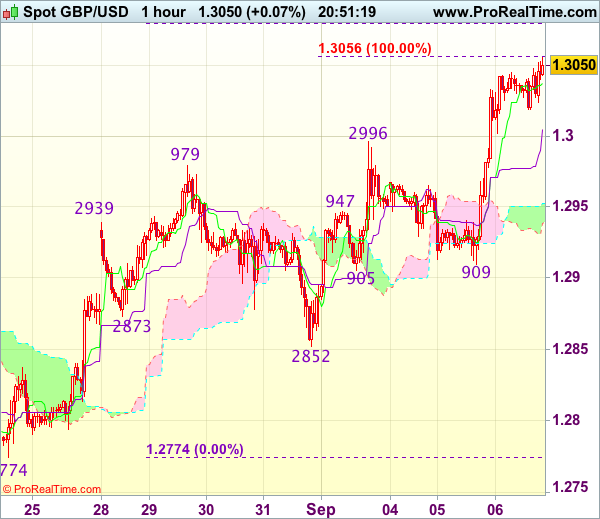

Trade Idea Update: GBP/USD – Buy at 1.2970

GBP/USD - 1.3047

Original strategy :

Buy at 1.2970, Target: 1.3070, Stop: 1.2935

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2970, Target: 1.3070, Stop: 1.2935

Position : -

Target : -

Stop : -

Yesterday’s rally above previous resistance at 1.3032 confirms recent rise from 1.2774 has resumed and mild upside bias remains for this move to extend further gain to 1.3055-60 (100% projection of 1.2774-1.2979 measuring from 1.2852), then towards 1.3080 (61.8% Fibonacci retracement of 1.3269-1.2774) but near term overbought condition would prevent sharp move beyond 1.3100, risk from there is seen for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy cable on pullback as 1.2970 should limit downside and bring another rise. Below the upper Kumo (now at 1.2951) would defer and risk weakness to the lower Kumo (now at 1.2935) but only break of support at 1.2905-09 would signal top is formed.

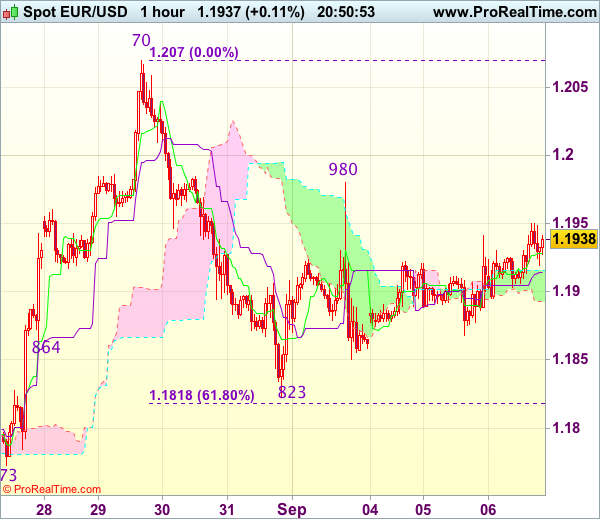

Trade Idea Update: EUR/USD – Sell at 1.1980

EUR/USD - 1.1932

Original strategy :

Sell at 1.1980, Target: 1.1880, Stop: 1.2015

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1980, Target: 1.1880, Stop: 1.2015

Position : -

Target : -

Stop : -

Yesterday’s cable-led rebound suggests consolidation with initial upside bias would be seen and gain to 1.1950-55 cannot be ruled out, however, reckon upside would be limited to resistance at 1.1980 and bring another decline later. Below 1.1885-90 would bring weakness to 1.1850, break there would signal the rebound from 1.1823 has ended, then test of this level would follow, break there would add credence to our view that top has been formed at 1.2070 earlier and extend the fall from there to 1.1815-18 (61.8% Fibonacci retracement of 1.1662-1.2070), then 1.1790-00 but downside should be limited to previous support at 1.1773.

In view of this, we are looking to sell euro again on recovery as 1.1980 resistance should limit upside. Only a firm break above said resistance at 1.1980 would abort and signal the fall from 1.2070 has ended at 1.1823, bring further gain to 1.2000 and possibly towards 1.2025-30.

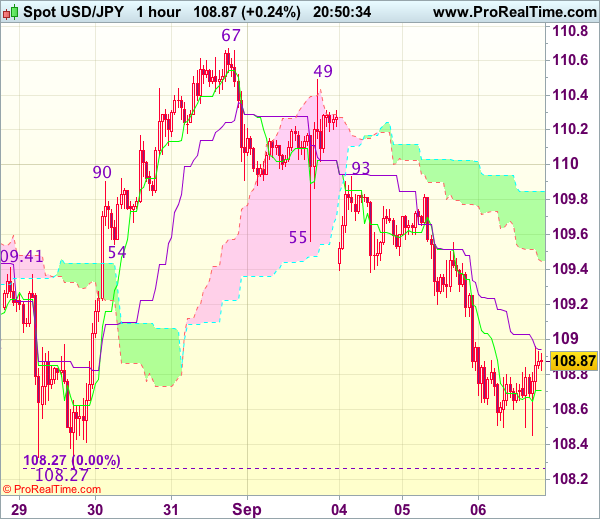

Trade Idea Update: USD/JPY – Sell at 109.40

USD/JPY - 108.86

Original strategy :

Sell at 109.40, Target: 108.40, Stop: 109.75

Position : -

Target : -

Stop : -

New strategy :

Sell at 109.40, Target: 108.40, Stop: 109.75

Position : -

Target : -

Stop : -

As dollar has remained under pressure after yesterday’s selloff, adding credence to our view that the fall from 110.67 is still in progress and may extend weakness towards previous support at 108.27, however, break there is needed to retain bearishness and extend the fall from 114.50 to another previous chart support at 108.13, having said that, the greenback needs to penetrate this chart support to confirm early selloff from 118.66 has resumed for subsequent weakness to 107.70-75 which is likely to hold from here.

In view of this, we are looking to sell dollar on recovery as 109.40-50 should limit upside and bring another decline later. Above 109.80-83 would abort and signal an intra-day low is formed instead, bring a stronger rebound to 110.00-05 but price should falter well below resistance at 110.49.

EURUSD Remains Vulnerable To The Downside Below Key Resistance

EURUSD: With the pair continuing to retain its downside pressure on correction, more weakness is likely despite present price hesitation. Resistance comes in at 1.1950 level with a cut through here opening the door for more upside towards the 1.2000 level. Further up, resistance lies at the 1.2050 level where a break will expose the 1.2100 level. Conversely, support lies at the 1.1900 level where a violation will aim at the 1.1850 level. A break of here will aim at the 1.1800 level. All in all, EURUSD faces further downside pressure on correction.

USD/CAD Is The Corrective Phase Completed?

The USD/CAD posted some gains in the first part of the day, but what will come is more important. The economic calendar is filled with high impact data, which will have a huge impact on the price action. Price continues to be under immense selling pressure because is located under some important resistance levels (support turned into resistance).

USD/CAD increased even if the dollar index has decreased further, we'll be important to see how will react after the Canadian and the US data will be sent to the public. The USDX is trading near an important support zone, but remains under pressure.

The BOC is expected to leave the rate unchanged today, at 0.75%, could announce a rate hike in the upcoming month. The Canadian Trade Balance could increase from -3.6B to -3.2B, while the Labor Productivity could increase by 0.9%. The greenback needs a helping hand from the US economy, but remains to see if will receive one.

Price is on a declining path and maintains a bearish perspective. Has dropped again below the median line (ml) of the minor descending pitchfork and under the lower median line (lml) of the black descending pitchfork. Only a false breakdown below these levels will signal a reversal in the upcoming weeks.

USD/CAD failed once again to reach and retest the lower median line (LML) of the major descending pitchfork, signaling an oversold. However, is premature to say that the corrective phase is completed, because the fundamental factors could demolish any bullish perspective.

Technically, a retest of the lower median line (lml) of the minor ascending pitchfork will confirm a further increase in the upcoming period.