Sample Category Title

(FED) Chair Janet L. Yellen – Financial Stability a Decade after the Onset of the Crisis

A decade has passed since the beginnings of a global financial crisis that resulted in the most severe financial panic and largest contraction in economic activity in the United States since the Great Depression. Already, for some, memories of this experience may be fading--memories of just how costly the financial crisis was and of why certain steps were taken in response. Today I will look back at the crisis and discuss the reforms policymakers in the United States and around the world have made to improve financial regulation to limit both the probability and the adverse consequences of future financial crises.

A resilient financial system is critical to a dynamic global economy--the subject of this conference. A well-functioning financial system facilitates productive investment and new business formation and helps new and existing businesses weather the ups and downs of the business cycle. Prudent borrowing enables households to improve their standard of living by purchasing a home, investing in education, or starting a business. Because of the reforms that strengthened our financial system, and with support from monetary and other policies, credit is available on good terms, and lending has advanced broadly in line with economic activity in recent years, contributing to today's strong economy.

At the same time, reforms have boosted the resilience of the financial system. Banks are safer. The risk of runs owing to maturity transformation is reduced. Efforts to enhance the resolvability of systemic firms have promoted market discipline and reduced the problem of too-big-to-fail. And a system is in place to more effectively monitor and address risks that arise outside the regulatory perimeter.

Nonetheless, the scope and complexity of financial regulatory reforms demand that policymakers and researchers remain alert to both areas for improvement and unexpected side effects. The Federal Reserve is committed to continuing to evaluate the effects of regulation on financial stability and on the broader economy and to making appropriate adjustments.

I will start by reviewing where we were 10 years ago. I will then walk through some key reforms our country has put in place to diminish the chances of another severe crisis and limit damage during times of financial instability. After reviewing these steps, I will summarize indicators and research that show the improved resilience of the U.S. financial system--resilience that is due importantly to regulatory reform as well as actions taken by the private sector. I will then turn to the evidence regarding how financial regulatory reform has affected economic growth, credit availability, and market liquidity.

Developments 10 Years Ago

The U.S. and global financial system was in a dangerous place 10 years ago. U.S. house prices had peaked in 2006, and strains in the subprime mortgage market grew acute over the first half of 2007. By August, liquidity in money markets had deteriorated enough to require the Federal Reserve to take steps to support it. And yet the discussion here at Jackson Hole in August 2007, with a few notable exceptions, was fairly optimistic about the possible economic fallout from the stresses apparent in the financial system.

As we now know, the deterioration of liquidity and solvency within the financial sector continued over the next 13 months. Accumulating strains across the financial system, including the collapse of Bear Stearns in March 2008, made it clear that vulnerabilities had risen across the system. As a result, policymakers took extraordinary measures: The Federal Open Market Committee (FOMC) sharply cut the federal funds rate, and the Federal Reserve, in coordination with the Treasury Department and other agencies, extended liquidity facilities beyond the traditional banking sector, applying to the modern structure of U.S. money markets the dictum of Walter Bagehot, conceived in the 19th century, to lend freely against good collateral at a penalty rate. Still, the deterioration in the financial sector continued, with Fannie Mae and Freddie Mac failing in early September.

But the deterioration from early 2007 until early September 2008‑‑already the worst financial disruption in the United States in many decades‑‑was a slow trickle compared with the tidal wave that nearly wiped out the financial sector that September and led to a plunge in economic activity in the following months. Not long after Fannie and Freddie were placed in government conservatorship, Lehman Brothers collapsed, setting off a week in which American International Group, Inc. (AIG), came to the brink of failure and required large loans from the Federal Reserve to mitigate the systemic fallout; a large money market fund "broke the buck" (that is, was unable to maintain a net asset value of $1 per share) and runs on other money funds accelerated, requiring the Treasury to provide a guarantee of money fund liabilities; global dollar funding markets nearly collapsed, necessitating coordinated action by central banks around the world; the two remaining large investment banks became bank holding companies, thereby ending the era of large independent investment banks in the United States; and the Treasury proposed a rescue of the financial sector. Within several weeks, the Congress passed--and President Bush signed into law--the Emergency Economic Stabilization Act of 2008, which established the $700 billion Troubled Asset Relief Program; the Federal Reserve initiated further emergency lending programs; and the Federal Deposit Insurance Corporation (FDIC) guaranteed a broad range of bank debt. Facing similar challenges in their own jurisdictions, many foreign governments also undertook aggressive measures to support the functioning of credit markets, including large-scale capital injections into banks, expansions of deposit insurance programs, and guarantees of some forms of bank debt.

Despite the forceful policy responses by the Treasury, the Congress, the FDIC, and the Federal Reserve as well as authorities abroad, the crisis continued to intensify: The vulnerabilities in the U.S. and global economies had grown too large, and the subsequent damage was enormous. From the beginning of 2008 to early 2010, nearly 9 million jobs, on net, were lost in the United States. Millions of Americans lost their homes. And distress was not limited to the U.S. economy: Global trade and economic activity contracted to a degree that had not been seen since the 1930s. The economic recovery that followed, despite extraordinary policy actions, was painfully slow.

What the Crisis Revealed and How Policymakers Have Responded

These painful events renewed efforts to guard against financial instability. The Congress, the Administration, and regulatory agencies implemented new laws, regulations, and supervisory practices to limit the risk of another crisis, in coordination with policymakers around the world.

The vulnerabilities within the financial system in the mid-2000s were numerous and, in hindsight, familiar from past financial panics. Financial institutions had assumed too much risk, especially related to the housing market, through mortgage lending standards that were far too lax and contributed to substantial overborrowing. Repeating a familiar pattern, the "madness of crowds" had contributed to a bubble, in which investors and households expected rapid appreciation in house prices. The long period of economic stability beginning in the 1980s had led to complacency about potential risks, and the buildup of risk was not widely recognized. As a result, market and supervisory discipline was lacking, and financial institutions were allowed to take on high levels of leverage. This leverage was facilitated by short-term wholesale borrowing, owing in part to market-based vehicles, such as money market mutual funds and asset-backed commercial paper programs that allowed the rapid expansion of liquidity transformation outside of the regulated depository sector. Finally, a self-reinforcing loop developed, in which all of the factors I have just cited intensified as investors sought ways to gain exposure to the rising prices of assets linked to housing and the financial sector. As a result, securitization and the development of complex derivatives products distributed risk across institutions in ways that were opaque and ultimately destabilizing.

In response, policymakers around the world have put in place measures to limit a future buildup of similar vulnerabilities. The United States, through coordinated regulatory action and legislation, moved very rapidly to begin reforming our financial system, and the speed with which our banking system returned to health provides evidence of the effectiveness of that strategy. Moreover, U.S. leadership of global efforts through bodies such as the Basel Committee on Banking Supervision, the Financial Stability Board (FSB), and the Group of Twenty has contributed to the development of standards that promote financial stability around the world, thereby supporting global growth while protecting the U.S. financial system from adverse developments abroad. Preeminent among these domestic and global efforts have been steps to increase the loss-absorbing capacity of banks, regulations to limit both maturity transformation in short-term funding markets and liquidity mismatches within banks, and new authorities to facilitate the resolution of large financial institutions and to subject systemically important firms to more stringent prudential regulation.

Several important reforms have increased the loss-absorbing capacity of global banks. First, the quantity and quality of capital required relative to risk-weighted assets have been increased substantially. In addition, a simple leverage ratio provides a backstop, reflecting the lesson imparted by past crises that risk weights are imperfect and a minimum amount of equity capital should fund a firm's total assets. Moreover, both the risk-weighted and simple leverage requirements are higher for the largest, most systemic firms, which lowers the risk of distress at such firms and encourages them to limit activities that could threaten financial stability. Finally, the largest U.S. banks participate in the annual Comprehensive Capital Analysis and Review (CCAR)‑‑the stress tests. In addition to contributing to greater loss-absorbing capacity, the CCAR improves public understanding of risks at large banking firms, provides a forward-looking examination of firms' potential losses during severely adverse economic conditions, and has contributed to significant improvements in risk management.

Reforms have also addressed the risks associated with maturity transformation. The fragility created by deposit-like liabilities outside the traditional banking sector has been mitigated by regulations promulgated by the Securities and Exchange Commission affecting prime institutional money market funds. These rules require these prime funds to use a floating net asset value, among other changes, a shift that has made these funds less attractive as cash-management vehicles. The changes at money funds have also helped reduce banks' reliance on unsecured short-term wholesale funding, since prime institutional funds were significant investors in those bank liabilities. Liquidity risk at large banks has been further mitigated by a new liquidity coverage ratio and a capital surcharge for global systemically important banks (G-SIBs). The liquidity coverage ratio requires that banks hold liquid assets to cover potential net cash outflows over a 30-day stress period. The capital surcharge for U.S. G-SIBs links the required level of capital for the largest banks to their reliance on short-term wholesale funding.

While improvements in capital and liquidity regulation will limit the reemergence of the risks that grew substantially in the mid-2000s, the failure of Lehman Brothers demonstrated how the absence of an adequate resolution process for dealing with a failing systemic firm left policymakers with only the terrible choices of a bailout or allowing a destabilizing collapse. In recognition of this shortcoming, the Congress adopted the orderly liquidation authority in Title II of the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act) to provide an alternative resolution mechanism for systemically important firms to be used instead of bankruptcy proceedings when necessary to preserve financial stability. The orderly liquidation authority contains a number of tools, including liquidity resources and temporary stays on the termination of financial contracts, that would help protect the financial system and economy from the severe adverse spillovers that could occur if a systemic firm failed. Importantly, any losses incurred by the government in an Orderly Liquidation Authority resolution would not be at the expense of taxpayers, since the statute provides that all such losses must be borne by other large financial firms through subsequent assessments. In addition, the Congress required that the largest banks submit living wills that describe how they could be resolved under bankruptcy. And the Federal Reserve has mandated that systemically important banks meet total loss-absorbing capacity requirements, which require these firms to maintain long-term debt adequate to absorb losses and recapitalize the firm in resolution. These enhancements in resolvability protect financial stability and help ensure that the shareholders and creditors of failing firms bear losses. Moreover, these steps promote market discipline, as creditors--knowing full well that they will bear losses in the event of distress--demand prudent risk-taking, thereby limiting the problem of too-big-to-fail.

Financial stability risks can also grow large outside the regulated banking sector, as amply demonstrated by the events of 2007 and 2008. In response, a number of regulatory changes affecting what is commonly referred to as the shadow banking sector have been instituted. A specific example of such risks, illustrative of broader developments, was the buildup of large counterparty exposures through derivatives between market participants and AIG that were both inappropriately risk-managed and opaque. To mitigate the potential for such risks to arise again, new standards require central clearing of standardized over-the-counter derivatives, enhanced reporting requirements for all derivatives, and higher capital as well as margin requirements for noncentrally cleared derivatives transactions.

Another important step was the Congress's creation of the Financial Stability Oversight Council (FSOC). The council is responsible for identifying risks to financial stability and for designating those financial institutions that are systemically important and thus subject to prudential regulation by the Federal Reserve. Both of these responsibilities are important to help guard against the risk that vulnerabilities outside the existing regulatory perimeter grow to levels that jeopardize financial stability.

The Financial System Is Safer

The evidence shows that reforms since the crisis have made the financial system substantially safer. Loss-absorbing capacity among the largest banks is significantly higher, with Tier 1 common equity capital more than doubling from early 2009 to now. The annual stress-testing exercises in recent years have led to improvements in the capital positions and risk-management processes among participating banks. Large banks have cut their reliance on short-term wholesale funding essentially in half and hold significantly more high-quality, liquid assets. Assets under management at prime institutional money market funds that proved susceptible to runs in the crisis have decreased substantially. And the ability of regulators to resolve a large institution has improved, reflecting both new authorities and tangible steps taken by institutions to adjust their organizational and capital structure in a manner that enhances their resolvability and significantly reduces the problem of too-big-to-fail.

The progress evident in regulatory and supervisory metrics has been accompanied by shifts in private-sector assessments that also suggest enhanced financial stability. Investors have recognized the progress achieved toward ending too-big-to-fail, and several rating agencies have removed the government support rating uplift that they once accorded to the largest banks. Credit default swaps for the large banks also suggest that market participants assign a low probability to the distress of a large U.S. banking firm. Market-based assessments of the loss-absorbing capacity of large U.S. banks have moved up in recent years, and market-based measures of equity now lie in the range of book estimates of equity. To be sure, market-based measures may not reflect true risks--they certainly did not in the mid-2000s--and hence the observed improvements should not be overemphasized. But supervisory metrics are not perfect, either, and policymakers and investors should continue to monitor a range of supervisory and market-based indicators of financial system resilience.

Economic research provides further support for the notion that reforms have made the system safer. Studies have demonstrated that higher levels of bank capital mitigate the risk and adverse effects of financial crises. Moreover, researchers have highlighted how liquidity regulation supports financial stability by complementing capital regulation. Economic models of the resilience of the financial sector--so called top-down stress-testing models--reinforce the message from supervisory stress tests that the riskiness of large banks has diminished over the past decade. Similarly, model-based analyses indicate that the risk of adverse fire sale spillovers across banks or broker-dealers have been substantially mitigated.

Is This Safer System Supporting Growth?

I suspect many in this audience would agree with the narrative of my remarks so far: The events of the crisis demanded action, needed reforms were implemented, and these reforms have made the system safer. Now--a decade from the onset of the crisis and nearly seven years since the passage of the Dodd-Frank Act and international agreement on the key banking reforms--a new question is being asked: Have reforms gone too far, resulting in a financial system that is too burdened to support prudent risk-taking and economic growth?

The Federal Reserve is committed individually, and in coordination with other U.S. government agencies through forums such as the FSOC and internationally through bodies such as the Basel Committee on Banking Supervision and the FSB, to evaluating the effects of financial market regulations and considering appropriate adjustments. Furthermore, the Federal Reserve has independently taken steps to evaluate potential adjustments to its regulatory and supervisory practices. For example, the Federal Reserve initiated a review of its stress tests following the 2015 cycle, and this review suggested changes to reduce the burden on participating institutions, especially smaller institutions, and to better align the supervisory stress tests with regulatory capital requirements. In addition, a broader set of changes to the new financial regulatory framework may deserve consideration. Such changes include adjustments that may simplify regulations applying to small and medium-sized banks and enhance resolution planning.

More broadly, we continue to monitor economic conditions, and to review and conduct research, to better understand the effect of regulatory reforms and possible implications for regulation. I will briefly summarize the current state of play in two areas: the effect of regulation on credit availability and on changes in market liquidity.

The effects of capital regulation on credit availability have been investigated extensively. Some studies suggest that higher capital weighs on banks' lending, while others suggest that higher capital supports lending. Such conflicting results in academic research are not altogether surprising. It is difficult to identify the effects of regulatory capital requirements on lending because material changes to capital requirements are rare and are often precipitated, as in the recent case, by financial crises that also have large effects on lending.

Given the uncertainty regarding the effect of capital regulation on lending, rulemakings of the Federal Reserve and other agencies were informed by analyses that balanced the possible stability gains from greater loss-absorbing capacity against the possible adverse effects on lending and economic growth. This ex ante assessment pointed to sizable net benefits to economic growth from higher capital standards--and subsequent research supports this assessment. The steps to improve the capital positions of banks promptly and significantly following the crisis, beginning with the 2009 Supervisory Capital Assessment Program, have resulted in a return of lending growth and profitability among U.S. banks more quickly than among their global peers.

While material adverse effects of capital regulation on broad measures of lending are not readily apparent, credit may be less available to some borrowers, especially homebuyers with less-than-perfect credit histories and, perhaps, small businesses. In retrospect, mortgage borrowing was clearly too easy for some households in the mid-2000s, resulting in debt burdens that were unsustainable and ultimately damaging to the financial system. Currently, many factors are likely affecting mortgage lending, including changes in market perceptions of the risk associated with mortgage lending; changes in practices at the government-sponsored enterprises and the Federal Housing Administration; changes in technology that may be contributing to entry by nonbank lenders; changes in consumer protection regulations; and, perhaps to a limited degree, changes in capital and liquidity regulations within the banking sector. These issues are complex and interact with a broader set of challenges related to the domestic housing finance system.

Credit appears broadly available to small businesses with solid credit histories, although indicators point to some difficulties facing firms with weak credit scores and insufficient credit histories. Small business formation is critical to economic dynamism and growth. Smaller firms rely disproportionately on lending from smaller banks, and the Federal Reserve has been taking steps and examining additional steps to reduce unnecessary complexity in regulations affecting smaller banks.

Finally, many financial market participants have expressed concerns about the ability to transact in volume at low cost--that is, about market liquidity, particularly in certain fixed-income markets such as that for corporate bonds. Market liquidity for corporate bonds remains robust overall, and the healthy condition of the market is apparent in low bid-ask spreads and the large volume of corporate bond issuance in recent years. That said, liquidity conditions are clearly evolving. Large dealers appear to devote less of their balance sheets to holding inventories of securities to facilitate trades and instead increasingly facilitate trades by directly matching buyers and sellers. In addition, algorithmic traders and institutional investors are a larger presence in various markets than previously, and the willingness of these institutions to support liquidity in stressful conditions is uncertain. While no single factor appears to be the predominant cause of the evolution of market liquidity, some regulations may be affecting market liquidity somewhat. There may be benefits to simplifying aspects of the Volcker rule, which limits proprietary trading by banking firms, and to reviewing the interaction of the enhanced supplementary leverage ratio with risk-based capital requirements. At the same time, the new regulatory framework overall has made dealers more resilient to shocks, and, in the past, distress at dealers following adverse shocks has been an important factor driving market illiquidity. As a result, any adjustments to the regulatory framework should be modest and preserve the increase in resilience at large dealers and banks associated with the reforms put in place in recent years.

Remaining Challenges

So where do we stand a decade after the onset of the most severe financial crisis since the Great Depression? Substantial progress has been made toward the Federal Reserve's economic objectives of maximum employment and price stability, in putting in place a regulatory and supervisory structure that is well designed to lower the risks to financial stability, and in actually achieving a stronger financial system. Our more resilient financial system is better prepared to absorb, rather than amplify, adverse shocks, as has been illustrated during periods of market turbulence in recent years. Enhanced resilience supports the ability of banks and other financial institutions to lend, thereby supporting economic growth through good times and bad.

Nonetheless, there is more work to do. The balance of research suggests that the core reforms we have put in place have substantially boosted resilience without unduly limiting credit availability or economic growth. But many reforms have been implemented only fairly recently, markets continue to adjust, and research remains limited. The Federal Reserve is committed to evaluating where reforms are working and where improvements are needed to most efficiently maintain a resilient financial system.

Moreover, I expect that the evolution of the financial system in response to global economic forces, technology, and, yes, regulation will result sooner or later in the all-too-familiar risks of excessive optimism, leverage, and maturity transformation reemerging in new ways that require policy responses. We relearned this lesson through the pain inflicted by the crisis. We can never be sure that new crises will not occur, but if we keep this lesson fresh in our memories--along with the painful cost that was exacted by the recent crisis--and act accordingly, we have reason to hope that the financial system and economy will experience fewer crises and recover from any future crisis more quickly, sparing households and businesses some of the pain they endured during the crisis that struck a decade ago.

Nosedive in Durable Goods Orders Mostly Aircraft

July durable goods orders more than reversed the aircraft-fueled surge of June amid continued weakness in the auto sector. Core capital goods orders, however, strengthened and bode well for Q3 equipment spending.

Transportation Troubles

Durable goods orders fell 6.8 percent in July, which was a bit worse than the 6.0 percent drop expected by consensus. We knew following last month's 129 percent surge in nondefense aircraft orders that there would be payback in August. Sure enough, civilian aircraft orders tumbled 71 percent, dragging down the headline. Fortunately for aircraft manufacturers, orders for defense-related aircraft and parts rose 48 percent in July.

In addition to a pullback in nondefense aircraft, the transportation sector was held down by the continued soft patch in autos. Orders for new vehicles and parts fell 1.2 percent. Seasonal adjustment in the auto sector can be difficult this time of year given the changing pattern of summer shutdowns, but orders have now fallen in five of the first seven months of the year. Inventories at auto dealers have been piling up amid slower sales, so the pullback in orders and production is not terribly surprising.

Outside a volatile month for an already volatile part of the report, orders were stronger. Excluding transportation, orders came in a shade better than expected, increasing 0.5 percent.

Similarly, our preferred bellwether for equipment spending posted a healthy increase. Nondefense capital goods orders excluding aircraft rose 0.4 percent in July. Core orders are now rising at a three-month average annualized pace of 4.6 percent, the strongest clip since March.

When looking at shipments, equipment spending for the current quarter looks to be off to a solid start. Nondefense capital goods shipments rose 2.0 percent on top of a meaningful upward revision to June. The July shipments numbers combined with recent core orders suggest another positive quarter for equipment outlays. We currently expect equipment spending to rise about 6 percent in the current quarter.

Modest Build in Inventories Could Have Mammoth Impact in Q3

In a report published earlier this week "Inventories: The Tail That Wags the Dog in Q3?", we highlighted that it will only take a small move in inventories to have a big impact on the third quarter's topline GDP figure. Today's durables report supplies the first input data into the BEA's estimates. Inventories rose 0.3 percent, bringing the three-month average annualized pace up to 3.6 percent.

While durable goods represent only a slice of nonfarm inventories (also included are wholesale, retail and nondurable manufactured goods), and this is only the first monthly reading of the quarter, today's gain lends support to our call for inventory growth to pick up in the third quarter and boost headline GDP.

GOLD More Upside In View

Price is moving in rage right above the 38.2% retracement level and tries to resume the upside movement. Is still trapped within the extended sideways movement, so only a valid breakout will bring us a clear direction. Technically is still expected to resume the upside movement, but remains to see if will have enough directional energy to do this after the false breakout above the 23.6% retracement level.

Gold registered some gains today as the USDX goes down ahead the US data release and most important ahead the FED Chair Yellen's speech, the ECB President will speak as well tonight.

The yellow metal will lose altitude if the USD will jump higher in the upcoming hours, the Core Durable Goods Orders could increase by 0.4%, while the Durable Goods Orders may drop by 6.0% in July versus a 6.4% growth in the former reading period.

Price is narrowing before will start an impressive movement, remains to see the direction because anything could happen after the Jackson Hole Symposium speeches. Technically was somehow expected to breakout from this range, but the buyers were too exhausted. Maintains a bullish bias as long as is trading above the 38.2% retracement level. The false breakout above the 23.6% retracement level signaled another leg lower, but this scenario will take shape only if the USDX will jump and will stabilize above the 93.81 static resistance.

GBP/JPY Sharp Increase Expected

GBP/JPY has turned to the upside after the failure to reach the major downside target from the first warning line (WL1) of the ascending pitchfork. We have a breakout in play, it has climbed above the median line (ml) of the minor descending pitchfork, a valid breakout will send it towards the upper median line (uml).

Technically should increase also because has failed once again to reach and retest the lower median line (lml) of the minor descending pitchfork. Price climbs higher as the Nikkei stock index failed to make new lows and now has turned to the upside.

EUR/GBP Another Leg Lower?

The EUR/GBP slipped lower today and resumed the yesterday's bearish candle. The bulls seem too exhausted on the short term, so the bears could take the full control. Should come to retest the median line (ml) of the blue ascending pitchfork after the rejection from the 0.9226 static resistance. Technically should drop aggressively after the failure to reach and retest the upper median line (UML) of the major ascending pitchfork, but is premature to say this because it could still retest this dynamic resistance.

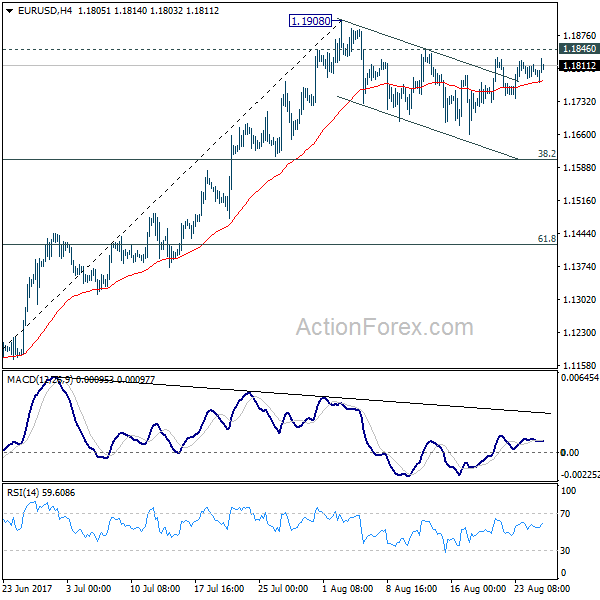

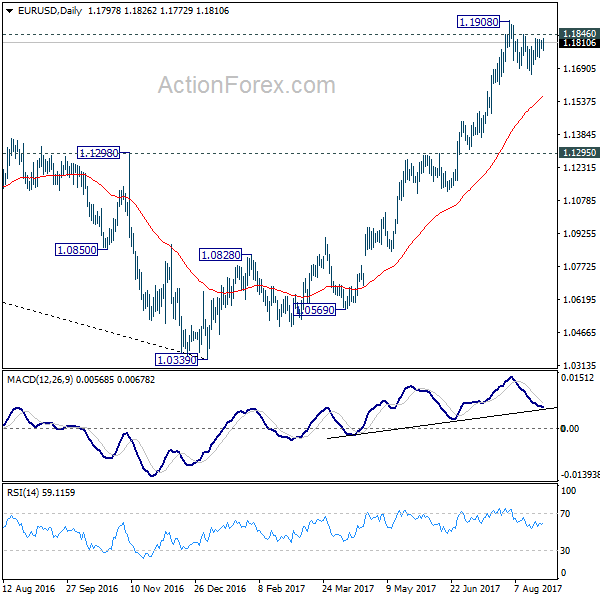

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1782; (P) 1.1800 (R1) 1.1816; More...

Intraday bias in EUR/USD remains neutral as consolidation from 1.1908 is still in progress. In case of another fall, downside should be contained by 38.2% retracement of 1.1119 to 1.1908 at 1.1606 to bring up trend resumption. Break of 1.1846 minor resistance will argue that larger rise from 1.0339 is resuming for 1.2042 long term support turned resistance next.

In the bigger picture, an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Sustained trading above 55 month EMA (now at 1.1768) will pave the way to key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. While rise from 1.0339 is strong, there is no confirmation that it's developing into a long term up trend yet. Hence, we'll be cautious on strong resistance from 1.2516 to limit upside. But for now, medium term outlook will remain bullish as long as 1.1295 support holds, in case of pull back.

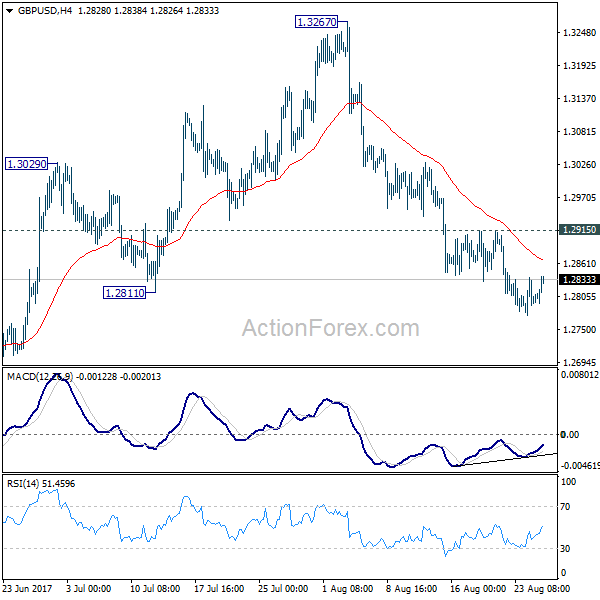

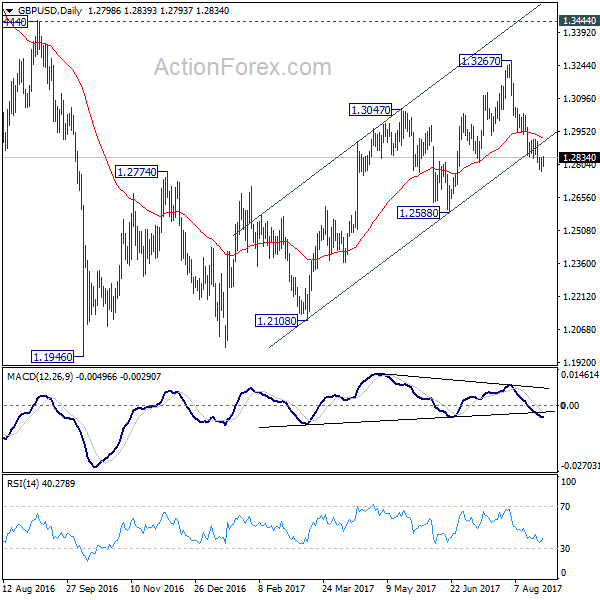

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2769; (P) 1.2803; (R1) 1.2832; More...

GBP/USD continues to lose downside momentum as seen in 4 hour MACD. But with 1.2915 resistance intact, deeper decline is expected. Current fall from 1.3267 should be targeting to 1.2588 key near term support. As noted before, we're favoring the case that correction from 1.1946 is completed at 1.3267. Decisive break of 1.2588 will confirm our view and target a test on 1.1946 low. Though, break of 1.2915 will indicate short term bottoming and bring stronger rebound.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern. While further rise cannot be ruled out, larger outlook remains bearish as long as 1.3444 key resistance holds. Down trend from 1.7190 (2014 high) is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

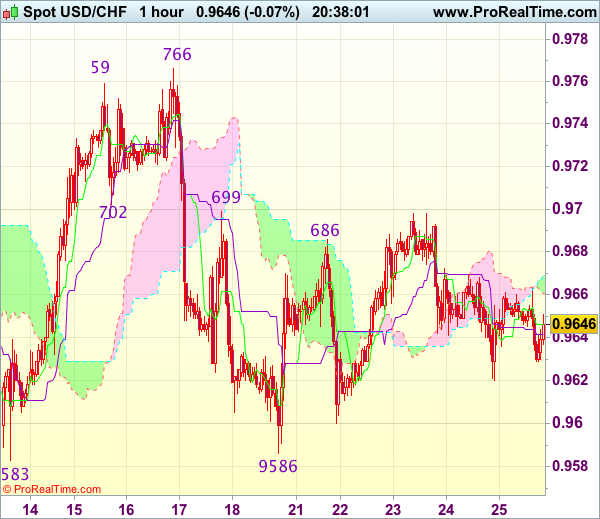

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9626; (P) 0.9647; (R1) 0.9674; More....

USD/CHF is still staying in range of 0.9582/9772 and intraday bias remains neutral. On the upside, decisive break of 0.9772 resistance will revive the bullish case of reversal. That is, whole decline from 1.0342 has completed at 0.9437 after defending 0.9443 support. USD/CHF should then target channel resistance (now at 0.9849) next. Meanwhile, the pair is bounded inside medium term falling channel and limited below 38.2% retracement of 1.0342 to 0.9437 at 0.9783 for the moment. Break of 0.9582 will turn bias back to the downside for 0.9437. This could also extend the fall from 1.0342 through 0.9437/43 key support level.

In the bigger picture, we're slightly favoring the case that USD/CHF has successfully defended 0.9443 key support level. And long term range trading in 0.9443/1.0342 is extending with another rise. At this point, there is no sign of an up trend yet. Hence, while further rise is expected in USD/CHF, we'll start to be cautious on loss of momentum above 61.8% retracement of 1.0342 to 0.9437 at 0.9996. However, firm break of 0.9443 will carry larger bearish implication and would target next key support at 0.9072.

Trade Idea Update: USD/CHF – Hold long entered at 0.9620

USD/CHF - 0.9649

Original strategy :

Bought at 0.9620, Target: 0.9720, Stop: 0.9595

Position : - Long at 0.9620

Target : - 0.9720

Stop : - 0.9595

New strategy :

Hold long entered at 0.9620, Target: 0.9720, Stop: 0.9595

Position : - Long at 0.9620

Target : - 0.9720

Stop : - 0.9595

Although the greenback retreated after faltering below resistance at 0.9699, outlook remains consolidative and reckon yesterday’s low at 0.9620 would limit downside, bring another rebound later, above indicated resistance at 0.9699 would signal the fall from 0.9766 has ended at 0.9586 last week and mild upside bias is seen for gain to 0.9720, then 0.9740, having said that, reckon resistance at 0.9766-73 would cap upside and bring further consolidation. Only a break of 0.9773 would retain bullishness and signal early rise from 0.9438 has resumed and extend gain to 0.9800.

In view of this, we are holding on to our long position entered at 0.9620. Below 0.9600 would risk test of strong support at 0.9583-86 but only break there would signal a downside break of recent broad range has occurred, bring subsequent fall to 0.9550.

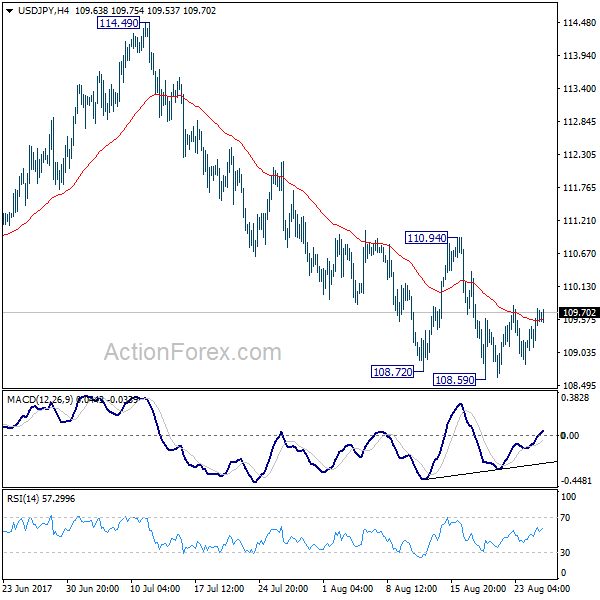

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.05; (P) 109.33; (R1) 109.81; More...

USD/JPY recovers mildly today but it's staying well below 110.94 resistance. Intraday bias remains neutral with bearish outlook. Deeper decline is still expected. Break of 108.59 will target a test on 108.12 low. Whole corrective decline from 118.65 is possibly resuming and break of 108.12 will target 61.8% retracement of 98.97 to 118.65 at 106.48. Nonetheless, firm break of 110.94 will indicate short term bottoming and turn bias back to the upside.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, downside should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.