Sample Category Title

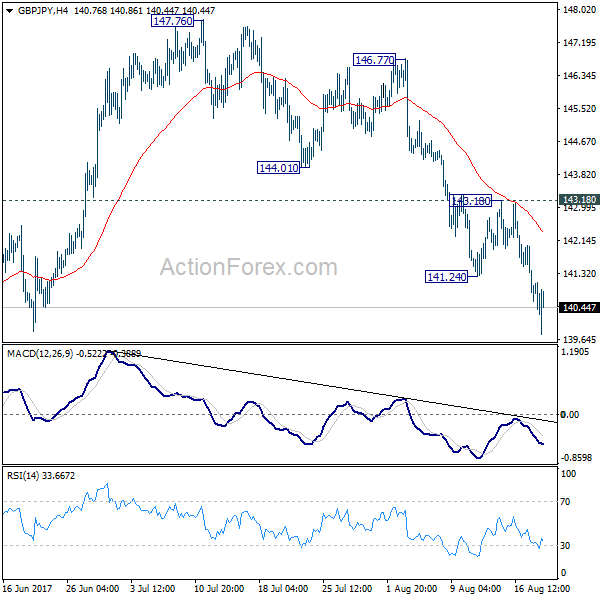

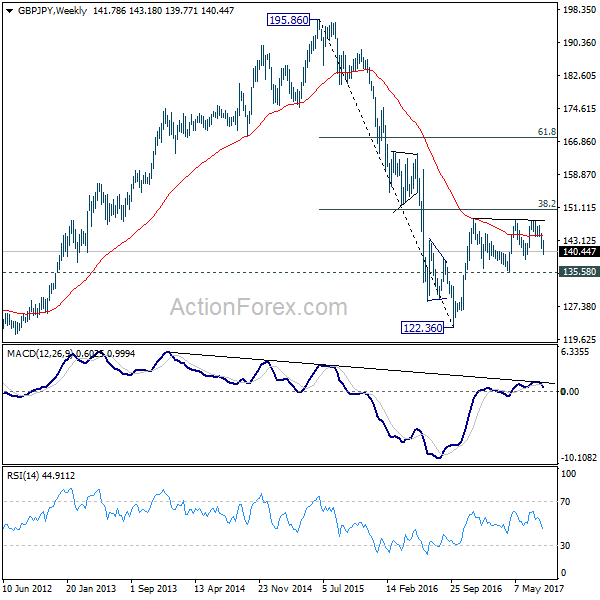

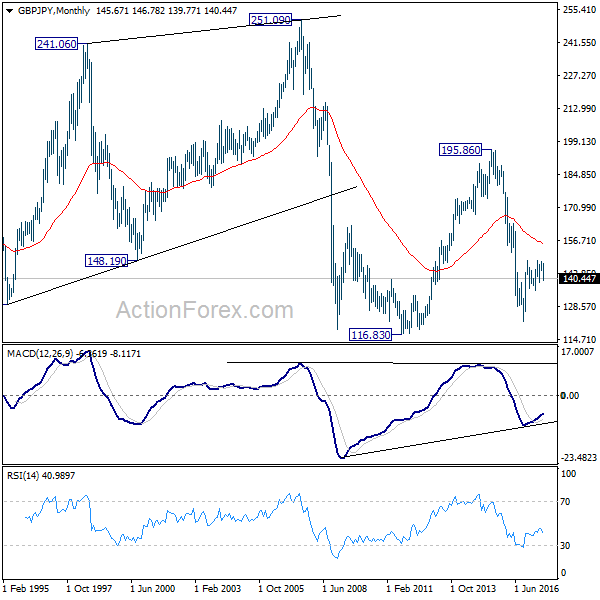

GBP/JPY Weekly Outlook

GBP/JPY's fall from 147.76 extended to as low as 139.77 last week. Initial bias remains on the downside this week for 138.65 support first. Break there will extend the decline to 135.58 key support level. At this point, price actions from 148.42 are seen as a sideway consolidation pattern. Hence, we'll expect strong support from 135.58 to contain downside and bring rebound. Nonetheless, break of 143.18 resistance is needed to indicate short term bottoming first. Otherwise, near term outlook will remain bearish in case of recovery.

In the bigger picture, the sideway pattern from 148.42 is extending with another leg. We'd expect strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside. Medium term rise from 122.36 is still expected to resume later. And break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. However, firm break of 135.58/39 will dampen the bullish view and turn focus back to 122.36 low.

In the longer term picture, it remains to be confirmed if whole down trend from 195.86 has completed at 122.36 already and there is no confirmation yet. But in any case, firm break of 38.2% retracement of 195.86 to 122.36 at 150.43 would pave the way to 61.8% retracement at 167.78. And with that, the 55 month EMA will be firmly taken out which suggests that price actions from 116.83 is indeed a sideway pattern that could last more than a decade.

Risk Aversion to Stay as Politics, Geopolitics and Central Bankers in Focus

Risk aversion was again the main theme in the financial markets last week. But this time, commodity currencies ended as the strongest ones. Sterling was hardest hit as disappointing inflation reading further killed the chance of an early BoE hike. Euro followed on report that ECB President Draghi won't address monetary policy in the upcoming Jackson Hole symposium this week. Also, the common currency was pressured as ECB minutes showed worries on Euro overshooting its strength. Dollar suffered much on the political turmoil in the White House but it ended slightly higher against most except Canadian Dollar and Australian Dollar. Meanwhile Yen and Swiss Franc failed to capitalize on risk aversion and ended the week mixed.

Economic data will take a back seat this week. Focus will firstly stay on the developments around US President Donald Trump's administration. Secondly, US will start a joint military exercise with South Korea between August 21 and 31 and that might escalate the tension with North Korea. Central bankers speeches in the Jackson Hole Symposium will be closely watched, in particular Fed Chair Janet Yellen and ECB President Mario Draghi. Risk aversion will likely stay as any wrong step by the leaders will trigger another selloff in the markets.

Dollar recovery could be temporary, vulnerable to the downside

The resilience in Dollar last week was mainly thanks to the pull back in Euro. A key factor providing support for the greenback was comments from New York Fed President William Dudley. Dudley, an influential member of FOMC, affirmed that he remained in "favor of doing another rate hike later this year". However, the recovery in Dollar clearly lacked sustainable strength as FOMC minutes showed that many policy makers "saw some likelihood that inflation might remain below 2 percent for longer than they currently expected". Also, "several indicated that the risks to the inflation outlook could be tilted to the downside."

Meanwhile, the dollar index continued to draw support from key support level at 91.91/3 cluster (38.2% retracement of 72.69 to 103.82 at 91.93). But the corrective price actions from 92.54 makes 91.91/3 very vulnerable. Outlook will stays bearish as long as 94.28 resistance holds. And we'd point out again that sustained break of 91.91/3 will extend whole correction from 103.82 to 50% retracement at 88.25 and below. Firm break of 94.28 should indicate that dollar index is finally staging a sustainable rebound.

Dow to test key support zone at 21491/593

Overall market risk sentiment will be a key factor in determining Dollar's fortune. DOW was under much pressure as business leader turned their back on Trump for his equating of Neo-Nazis with counter protestors. Selling intensified on rumor that Trump's top economic advisor Gary Cohn was following. Even though it's later clarified that Cohn is staying, the damage was already done. Trump's firing of chief strategist Stephen Bannon triggered a brief recovery in DOW but the index was quickly under pressure again. There is deep concern that if the root causes, that is Trump himself, is not addressed, more business and political leaders will turn their back on him. And some analysts see the chance of fiscal policy paralyze as significant.

At this point, we maintained that, comparing to other major global indices, it's still early to declare trend reversal in DOW yet. We anticipated deeper fall in DOW in near term as mentioned in last weekly and it did happen. Focus will stay on 55 day EMA (now at 21593.23) and 38.2% retracement of 20379.55 to 22179.11 at 21491.67. The up trend is still intact as long as this levels hold and another record high is in favor. However, firm break there will indicate that fall from 22179.11 is developing into a medium term correction for support zone at 20379.55/21169.11.

Commodity Yen crosses in consolidation only

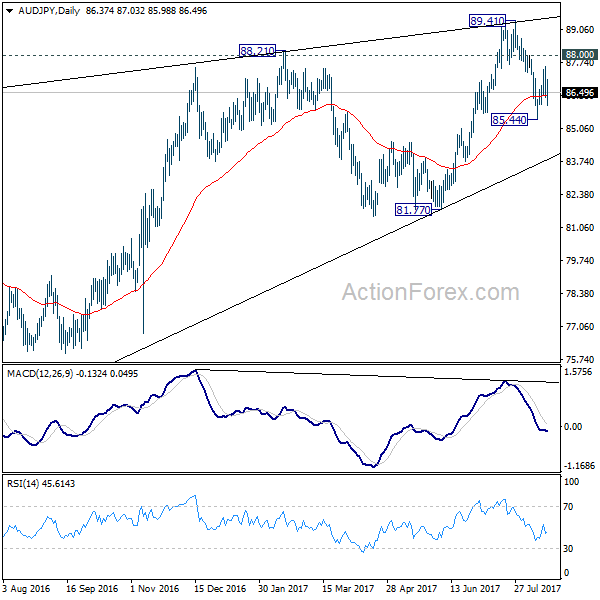

Commodity/yen crosses recovered last week even though markets were in risk averse mode. But such recovery was seen as corrective as the crosses were oversold in the prior week. AUD/JPY's recovery from 85.44 is clearly corrective looking and couldn't get rid of 55 day EMA cleanly. More importantly, the bearish divergence condition in daily MACD and wedge like price actions suggest the cross is losing medium term momentum too. We'll continue to favor more downside as long as 88.00 minor resistance holds. And break of 85.44 will target 81.77 key medium term support.

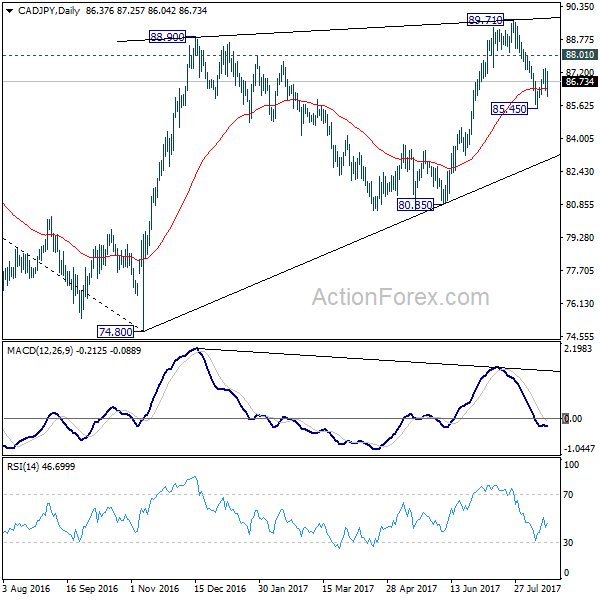

Similar picture is seen in CAD/JPY and further fall is expected as long as 88.01 minor resistance holds. Break of 85.45 will target 80.85 key support level.

Trading strategies

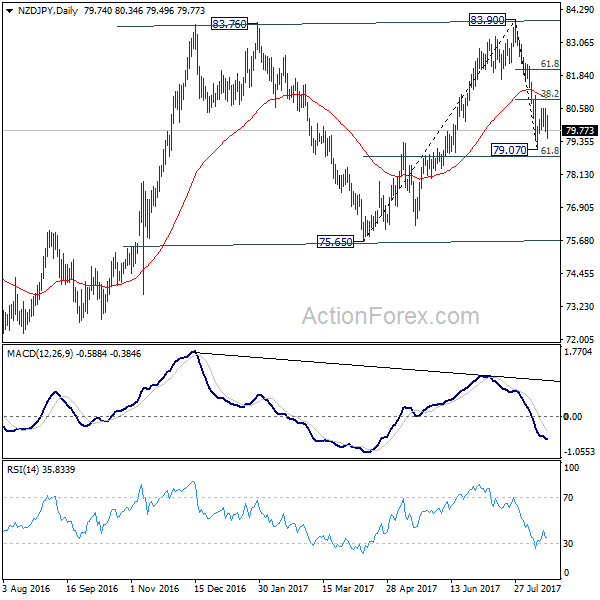

Regarding trading strategies, we closed our GBP/USD short (sold at 1.3030) at open at 1.3000 last week, before the pair finally took off and dived to 1.2830. It was clearly a wrong decision even though 30pt profits were made. Our sell NZD/JPY at 80.85 was not filled as the cross just recovered to 85.59. But as noted above, we generally still expect more downside in yen crosses. Hence, we'll just keep the order first. That is, sell NZD/JPY on recovery 80.85. 80.85 is slightly below 38.2% retracement of 83.90 to 79.07 at 80.91. Stop will be placed at 82.10, slightly above 61.8% retracement at 82.05. 75.65 will be the target.

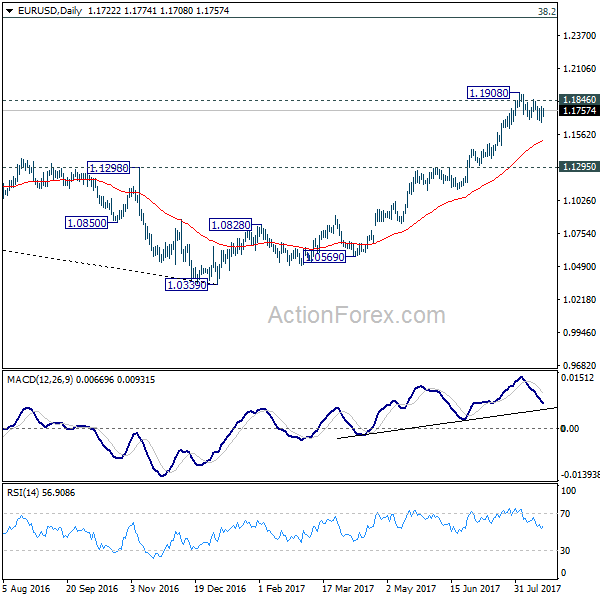

In addition to that, while dollar index is trying to draw support from above mentioned 91.91/3 level, it's looking more vulnerable. With EUR/USD consolidation from 1.1908 for three weeks already, it's about time for a breakout. Hence, we will buy EUR/USD on break of 1.1846 with stop at 1.1660. Target will be long term fibonacci level at 1.2516.

GBP/JPY Weekly Outlook

GBP/JPY's fall from 147.76 extended to as low as 139.77 last week. Initial bias remains on the downside this week for 138.65 support first. Break there will extend the decline to 135.58 key support level. At this point, price actions from 148.42 are seen as a sideway consolidation pattern. Hence, we'll expect strong support from 135.58 to contain downside and bring rebound. Nonetheless, break of 143.18 resistance is needed to indicate short term bottoming first. Otherwise, near term outlook will remain bearish in case of recovery.

In the bigger picture, the sideway pattern from 148.42 is extending with another leg. We'd expect strong support from 135.58 and 50% retracement of 122.36 to 148.42 at 135.39 to contain downside. Medium term rise from 122.36 is still expected to resume later. And break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. However, firm break of 135.58/39 will dampen the bullish view and turn focus back to 122.36 low.

In the longer term picture, it remains to be confirmed if whole down trend from 195.86 has completed at 122.36 already and there is no confirmation yet. But in any case, firm break of 38.2% retracement of 195.86 to 122.36 at 150.43 would pave the way to 61.8% retracement at 167.78. And with that, the 55 month EMA will be firmly taken out which suggests that price actions from 116.83 is indeed a sideway pattern that could last more than a decade.

Summary 8/21 – 8/25

Monday, Aug 21, 2017

[php_everywhere] [/php_everywhere]

Tuesday, Aug 22, 2017

[php_everywhere] [/php_everywhere]

Wednesday, Aug 23, 2017

[php_everywhere] [/php_everywhere]

Thursday, Aug 24, 2017

[php_everywhere] [/php_everywhere]

Friday, Aug 25, 2017

[php_everywhere] [/php_everywhere].

Weekly Economic and Financial Commentary: Central Banks No Longer All on the Same Page

U.S. Review

U.S. Economic Data Mixed This Week

- Retail sales provided the most positive piece of economic news in the United States this week. Sales topped expectations in July and, coupled with upward revisions to prior months, suggest a stronger pace of consumer spending than originally believed.

- Housing starts in July were a disappointment, however, as both starts and permits fell on the month. Starts have fallen in five out of seven months this year.

- Industrial production growth also came in below consensus in July, with much of the weakness concentrated in motor vehicles & parts.

U.S. Economic Data Mixed This Week

Economic data in the United States this week started out on a solid note with a robust retail sales print on Tuesday. Retail sales rose 0.6 percent to kick off the third quarter, topping expectations for a 0.3 percent gain. The strength in retail sales was broad based, with motor vehicle and parts dealers' sales increasing 1.2 percent and building material & garden equipment & supplies dealers' sales increasing 1.2 percent after registering a 1.1 percent gain in June. Even department stores sales, a sector that has been negatively affected by the eruption of online sales, posted a strong 1.0 percent increase for the month.

Perhaps equally as important, both June and May's data were upwardly revised, signaling that growth in July was faster off a higher base. This signals that, not only was personal consumption growth likely stronger in Q2 than initially reported in the advance GDP release, but expectations for personal consumption growth during Q3 are likely to be revised higher as well. For more on the consumer sector, see our Topic of the Week on page 7.

Despite a robust reading on home builder confidence on Tuesday, housing starts data released the next day for July were a disappointment. Starts declined 4.8 percent in July and have fallen in five of the past seven months. However, much of the weakness has been in the multifamily component, which should not be surprising given slowing fundamentals. Year-to-date, single-family starts are up 11.0 percent compared to the first seven months of last year. However, single-family starts still have not risen nearly as much as builder confidence has, reflecting the greater difficulty builders are having obtaining lots and labor relative to past cycles.

The minutes from the July FOMC meeting suggested that the Fed remains on track to announce balance sheet normalization plans at its September meeting. The message in the minutes on inflation was mixed. On the one hand, "many participants" noted that much of the recent decline in inflation had probably reflected idiosyncratic factors. On the other, "several" participants indicated that the risks to inflation were tilted to the downside, while participants "differed" in their assessments of whether inflation expectations were well anchored. The inflation readings over the next few months will likely determine whether or not the Fed elects to once again cap the year with a December rate hike.

Like housing starts, industrial production growth in July was underwhelming. Manufacturing output, which comprises three quarters of total industrial output, fell 0.1 percent on the month. The automobile sector was a key driver of the miss, with monthly output declining 3.6 percent. Seasonal factors can sometimes wreak havoc on the July figures in this sector due to summer shutdowns at auto plants, but the fourth decline in five months suggests a genuine downward trend in production rather than just seasonal noise. Through the monthly volatility, manufacturing production as a whole is up 1.3 percent on a yearover- year basis, consistent with our forecast for modest but steady growth in the sector more broadly.

U.S. Outlook

New Home Sales • Wednesday

The modest rise in new home sales in June was encouraging, with a 0.8 percent increase to a 610,000-unit pace. Revisions to earlier months removed 27,000 sales, however, which dulled the June reading. On the bright side, some readings suggest inventory pressures eased slightly. Inventory of homes for sale rose, and the median price fell 4.2 percent—which resulted from a shift toward lower-priced homes benefiting first-time homebuyers. Most of the increase in June was for homes that had not yet started construction.

Construction of new residential homes provided a major boost to economic growth in the first quarter, but was softer in Q2 GDP. Much of this data story resulted from unusual weather patterns and the associated correction. Residential investment in the third quarter should be more supportive to GDP growth, as demand for new homes remains solid.

Previous: 610K Wells Fargo: 617K Consensus: 610K

Existing Home Sales • Thursday

Persistently lean inventories continued to restrain resales in June, with existing home sales falling 1.8 percent to a 5.52 million-unit pace. We noted last month that the housing market appears to be woefully out of balance. Would-be homebuyers face a dearth of available inventory, particularly at lower price points. Developers are optimistic about demand for new stock, but available lots are lacking amid increasingly prohibitive construction costs, which are exacerbated by a shortage of construction labor. These pressures not only inhibit new home sales, but existing homeowners are understandably reluctant to put their homes on the market and risk not finding trade-up homes in their price range. Home prices continue to reach record highs.

July may have proved more conducive for homebuyers as pending sales rose in June, which tend to lead existing sales by 1-2 months.

Previous: 5.52M Wells Fargo: 5.49M Consensus: 5.56M

Durable Goods • Friday

The headline reading on durable goods orders in June was skewed to the upside by the notoriously volatile aircraft component, which bumped the monthly gain to 6.4 percent in June. Boeing orders were down in July, which suggests headline durable goods orders growth will likely follow suit. Excluding transportation, orders rose 0.2 percent in June while May was revised up to 0.6 percent. Core capital goods, ex aircraft, fell 0.1 percent after a strong May gain. Core goods shipments were also soft in June, and both were running at the softest 3-month annualized pace of 2017.

Worth noting is that looking beyond the aircraft component, factory sector conditions have been largely stable in recent months. Our call for a slow and steady positive trend continues to play out in the data.

Previous: 6.4% Wells Fargo: -6.1% Consensus: -5.8% (Month-over-Month)

Global Review

You Can Go Your Own Way

- For the past several years, the world's major central banks have broadly embraced very accommodative monetary policy. More recently, policy has started to go in different directions.

- In this week's Global Review, we break down the latest figures on inflation for the United Kingdom and Canada and the second quarter GDP number for Japan, and we consider what these numbers mean in the context of monetary policy for these different corners of the global economy.

Central Banks No Longer All on the Same Page

Japan's economy expanded at an annualized pace of 4.0 percent in the second quarter, and in so doing it extended the number of consecutive quarterly expansions to six—the longest winning streak in more than a decade.

Domestic demand picked up substantially in the second quarter as growth was driven by consumer spending as well as business fixed investment spending. Both components posted their largest quarterly increases in years and together boosted the headline GDP growth rate offsetting a modest drag from trade.

The Bank of Japan (BoJ) is not quite in synch with the world's major foreign central banks at present. The Fed is in a rate tightening cycle, the Bank of Canada raised rates in July with another hike expected this year. The European Central Bank is widely expected to announce plans to dial back its asset purchase program as early as this autumn. Despite this backdrop, which can be collectively described as "less accommodative," the Bank of Japan has not budged in terms of its intended course.

At its July meeting, the BoJ made no change to that stance and even lowered its inflation forecast. As we describe in the international outlook section on the next page, CPI figures for July will print next week. With inflation still well-below target, we do not expect the BoJ to signal any substantive change in its comprehensive package of monetary policy accommodation.

Another consideration on the topic of large central banks is the Bank of England. The Monetary Policy Committee (MPC) is also in a situation where a rate hike could be justified. Indeed, in the past few meetings, there has been growing dissent with some members expressing a desire to raise rates sooner rather than later. The main catalyst for this pressure to hike is the fact that inflation is running a little hot. This week brought the latest reading for CPI inflation in the United Kingdom, and we learned that the year-over-year rate of inflation held steady at 2.6 percent, just shy of the consensus expectation for 2.7 percent. Some of the upward pressure on prices has to do with the marked depreciation of sterling in the wake of last year's Brexit referendum.

The MPC looks for this pass-through effect to continue to push inflation higher in the coming months and to peak at around 3 percent in October before the effect begins to fade. If the U.K.'s economy picks up over the next 18 months as we expect, the BoE could raise rates as soon as next spring.

We mentioned earlier that the Bank of Canada (BOC) is expected to raise rates again this year. The BoC targets inflation between 1 percent and 3 percent and as close as possible to the midpoint of that range. We learned this week that CPI inflation for July increased to a year-over-year rate of 1.2 percent from 1.0 percent the prior month. The BoC's three remaining meetings are in September, October and December. The September meeting occurs just before the FOMC meeting that month, so we expect the October meeting to be the first realistic opportunity for the BoC to hike rates.

Global Outlook

Germany ZEW • Tuesday

Recent market uneasiness regarding a potential slowdown in the German economy will probably be put to the test when the August ZEW index is released on Tuesday. Although the current situation index slipped marginally, from 88.0 in June to 86.4 in July, data on the German economy have remained relatively strong lately. Thus, an improvement in the August reading will help cement the notion that the German economy remains in good shape. Meanwhile, the ZEW expectations index has weakened since June. After a 20.6 reading in May, the index printed 18.6 in June and 17.5 in July. This weakening probably helped to make the case of a slowdown in the German economy. Thus, a rebound for this index in August would be a positive sign for the German economy as well as for the Eurozone economy. On Friday, we will also get the release of the IFO business climate, current assessment, and expectations indices. This overall index recorded a series high in July.

Previous: 86.4 Consensus: 85.3

Eurozone Manufacturing PMI • Wednesday

Another index that has contributed to the view that the German and the Eurozone economies were slowing down was the Markit Manufacturing PMI index for July. After hitting an index high of 59.6 for Germany and 57.4 for the Eurozone in June, both indices came down marginally, to 58.1 in Germany and 56.6 for the Eurozone, in July. Thus, the release of the preliminary August Markit manufacturing PMI on Wednesday has the potential to move the market as a further decline in the index will help cement the slowing-down view while a recovery will tend to confirm what other data on the region have been indicating.

Markets will also have an opportunity to look at the service side of the economy, both in Germany and the Eurozone, when the services PMIs are released on Wednesday. This index hit a series high in April for the Eurozone while it has been trending down since June for Germany.

Previous: 56.6 Consensus: 56.3

Japan CPI • Thursday

After the strong Japanese Q2 GDP reported last week, the release of the CPI number for July on Thursday will carry a little more weight than normal in a country that has had its issues with keeping inflation close to or above its pledged target of 2 percent. The yearover- year CPI rate has stabilized at 0.4 percent since April of this year and our forecast July is for the rate to remain unchanged at 0.4 percent.

Thus, as we argued on our report "Q: What G-7 Economy had Fastest GDP Growth in Q2? A: Japan," which is available on our website, we do not expect the Bank of Japan to change its view regarding monetary policy any time soon even if other developed countries' central banks have either started to take monetary accommodation away or are moving in that direction.

Previous: 0.4% Wells Fargo: 0.4% Consensus: 0.4% (Year-over-Year)

Point of View

Interest Rate Watch

It Is Beginning to Feel Like August

Hot, muggy weather and daily thunderstorms are not the only things August is known for. Financial market volatility also tends to increase and did once again, as new questions about U.S. political leadership and the future course of fiscal policy have been added to questions about an impending shift in monetary policy, both in the U.S. and abroad, despite persistent low inflation around much of the globe. As if this were not enough, Thursday's dreadful terrorist attacks in Spain reminded everyone of the ever present geopolitical concerns hanging over the global economy and financial markets.

Bond yields pulled back, as stock prices sold off on Thursday. Economic data have, for the most part, come in on the strong side. One notable exception is motor vehicle sales and production, which have weakened due to an onslaught of used vehicles hitting the market and some deterioration in household finances. Home sales and new home construction also remain disappointing, largely due to supply constraints and the winding down of the apartment boom. Inflation remains perplexingly low, despite a tightening labor market and weakening dollar.

Bond yields declined this week, as rising geopolitical concerns and Thursday's sharp sell-off in equity prices triggered a flight to safety. Minutes from the Fed's September FOMC meeting raised additional doubts about whether the Fed will raise the federal funds rate again in 2017 but appear to confirm that most FOMC members remain firmly committed to beginning to draw down the Fed's balance sheet this fall.

Fed Chair Janet Yellen should provide some additional insight into the Fed's intentions when she speaks at the Kansas City Fed's annual Jackson Hole shindig, which is focused this year on "Fostering a Dynamic Global Economy." Her remarks will center on promoting financial stability. The Jackson Hole conference will be the highlight of a light week of economic data but likely will not change views on the timing of the Fed's next move or give new insights into the Fed's plans for unwinding their balance sheet.

Credit Market Insights

Mortgage Credit Growth Continues

Recently released data from the Mortgage Bankers Association (MBA) showed a 0.3 percent increase in the Mortgage Credit Availability Index for July. Updated underwriting standards for adjustable-rate mortgages (ARMs) have pushed their availability closer to that of traditional mortgages, helping drive the increase for the month according to the report.

Both fixed and adjustable mortgage rates have increased over the past year; however, adjustable rates are typically lower than fixed rates. As home prices continue to climb while inventories remain low, this rate differential could be pushing borrowers to forego fixed rates for lower adjustable rates. The MBA's Mortgage Application Survey supports this shift, with ARMs at 15 percent of the total value of loan applications for the week of August 11th, up 28 percent year-over-year.

While mortgage credit continues to grow, mortgage delinquencies are maintaining their downward trend, now at only 1.5 percent of balances at least 90 days past due in Q2, compared to almost 9 percent in 2010. Lower delinquencies may position borrowers to better withstand rate increases on the horizon, especially for those with ARMs sensitive to interest rate changes. We look for one more Fed rate hike in 2017 and three in 2018. Data to be released next week on new and existing home sales should reinforce the extent to which mortgage credit growth is displayed in the housing market as of late.

Topic of the Week

Consumers Tap Rainy Day Fund

Consumer confidence surged after the surprise U.S. presidential election result last fall. The Conference Board's consumer confidence index soared roughly 25 percent between October 2016 and March 2017, with much of the gain coming in the expectations component. This shift in sentiment suggested consumers were poised to ramp up their spending in the first half of the year. Despite the gain, real personal expenditures growth was ho-hum in the first half, continuing to trudge along at roughly 2.5 percent year-over-year (top chart). Was the surge in confidence a false start?

To keep consumption growth humming along, consumers dipped into their savings. The personal savings rate fell from 5.7 percent in September 2016 to 3.8 percent in June 2017 (bottom chart). Consumers had been keeping their powder dry heading into the end of last year and evidently felt confident enough to alter their saving behavior in the wake of the election. This drawdown can only keep growth going for so long, however, and if employment growth gradually slows over the next year, as we expect, it will take fatter paychecks to keep growth steady in the consumer sector.

Wage growth has been a perennial challenge in this cycle, and with slack in the labor market continuing to diminish, continued weak income growth presents a significant risk to the outlook. Personal consumption accounts for about 70 percent of GDP, making it far and away the largest component of the economy. As a result, the outlook for the consumer will play a key role in driving economic growth in the quarters ahead. For now, our outlook is for personal consumption growth to be more or less stable during the second half of the year. Retail sales kicked off the third quarter on a positive note, and average hourly earnings growth was solid in July, encouraging signs for second half activity.

The Weekly Bottom Line: U.S. – Good Data Overwhelmed By Geopolitical Concerns

U.S. Highlights

- A relatively good week for economic data was overshadowed by geopolitical events. Volatility spiked late in the week, the Dow suffered its largest one day loss since May on Thursday, and the 10-Year Treasury rallied to 2.17%.

- Investor nervousness is understandable, but there is little reason to doubt the ongoing economic expansion. U.S. retail sales rose by a robust 0.6% in July and were upwardly revised in June.

- Minutes from the FOMC's July 26 rate announcement showed a Fed looking for proof that inflation is moving toward target, and agreeing that balance sheet reduction should begin soon (likely in September).

Canadian Highlights

- The Canadian housing market slowed for the fourth consecutive month in July on the back of government policy changes as well as deteriorated affordability related to elevated prices and rising mortgage rates.

- Other sectors of the economy are expected to help offset the economic impact from a slowdown in housing, but real GDP growth will likely slow from 3.7% in Q2 to 1.7% in Q3.

- The full year performance of the Canadian economy will remain solid, and economic slack soon fully absorbed. At the same time, inflation is starting to tick-up, which should keep the Bank of Canada on track to continue raising interest rates.

U.S. - Good Data Overwhelmed By Geopolitical Concerns

A relatively good week for economic data was overshadowed by geopolitical events and concerns about the economic leadership within the Trump administration. On Thursday, volatility spiked, equites saw their biggest declines since May (the Dow down 1.2%) and Treasuries rallied (U.S. 10-year fell to 2.19%) as investors sought the protection of safe assets.

The understandable nervousness among investors notwithstanding, there is little reason to doubt the ongoing economic expansion. Retail sales rose by a robust 0.6% in July and were upwardly revised in June. The details were encouraging with broad-based strength across categories. Given consistently strong job growth, accelerating wage growth and benign inflation, consumer spending should remain healthy over the second half of the year. We expect personal spending to rise by 3.0% in the third quarter. With additional support from business spending, real GDP should rise by about as much.

On the topic of inflation, the minutes from the Federal Open Market Committee's July 25-26 meeting gave additional detail on how monetary policymakers are responding to its recent misses. The dilemma for policymakers is how to explain the continued downward drift in inflation in spite of ongoing tightening in the labor market. The minutes offered several possible explanations: a weakened relationship between resource slack and inflation, a lower natural rate of unemployment, greater lags in the relationship between economic tightening and inflation, and restraints on pricing power due to technology and globalization.

Overall, their faith is being tested, but it has not been lost. "Most participants thought that the [Phillips curve] framework remained valid" and still believe that inflation will return to target over the medium term. At a minimum however, they will need to see some proof that inflation is moving toward target in order to continue to push up policy rates.

The one area where the Fed was in general agreement was in the need to begin normalizing the balance sheet. While there was little new on this front in the discussions, the minutes confirmed previous announcements and statements by several Fed members. Importantly, the Fed does not see balance sheet normalization as substituting for increases in the federal funds rate, but rather hopes to proceed as inconspicuously as possible. Nonetheless, just as asset purchases helped to bring down yields, the unwinding of purchases is likely to put modest upward pressure on longer-term yields. Our forecast for Treasury yields over the next two years embeds a 10 to 20 basis point rise stemming directly from balance sheet reduction.

All of this assumes that the political situation in Washington remains stable. September will be a busy month for Congress, who has to pass an increase in the statutory debt ceiling and find a way to continue funding the government and avoid a shutdown. At the same time the administration will continue to push for personal and corporate tax reform. If Congress fails to reach accord on either the debt ceiling or government funding, we would expect increased volatility and additional losses in equity markets that still appear priced for perfection. As it has in the past, the financial and political damage would likely move politicians to quickly fall into line.

Canada - Soft Landing in Progress

It looks like it's a wrap for Canada's most recent housing boom. Existing home sales have now fallen for four consecutive months. The average existing home price declined 8.8% between its March peak and July, while home prices on a quality adjusted basis are down by 1.6% during the same timeframe.

Almost 80% of the decline in activity has occurred in Ontario. Existing home sales are down 44% in the GTA from their peak, and home values (on a quality adjusted basis) are down 5.3%. The sales-to-new listings ratio (a measure of supply-demand balance in the market) in the GTA has been sitting just above 40 for three months now, suggesting it was one of the softest markets across Canada, with prices typically declining in the GTA once this ratio dips below 45.

While the downturn in Ontario can be timed with the introduction of the Fair Housing Plan, it can also be attributed to a sharp deterioration in housing affordability over the last year due to rapid home price appreciations. Home prices in Ontario appreciated by an average of 6.0% per year since 1980, but rose by 15.6% in 2016 alone. These price gains were unsustainable set against income growth of just 4% per year, and the market was expected to moderate even without further housing policy changes.

Set against lofty valuations, the 40 basis point rise in 5-year mortgage rates since early July is likely going to keep the market from bouncing back even once the impact of policy rules wear out. As such, we anticipate that the Greater Toronto Area market is headed for a sustained 6% decline in average home prices next year. The recoveries that took hold earlier this year in Montreal, Vancouver, Calgary and Edmonton are also losing steam along with higher mortgage rates.

The housing slowdown expected over the rest of 2017 and into 2018 is expected to help contribute to a moderation in Canadian economic growth, but won't derail it. For one, credit channels remain healthy and households continue to spend on a wide range on goods and services, despite having scaled back demand for housing. The manufacturing shipments report this week showed that sales have eased heading into the third quarter, but from lofty levels in Q2, with international trade is still expected to help contribute positively to economic growth throughout the rest of the year.

Once you put it all together, economic growth is expected to ease to 1.7% in Q3, following a solid print of 3.7% in the prior two quarters. This performance still puts Canada on track for average economic growth of 3.2% between Q3 2016 and Q3 2017 with the economy having now fully mopped up any economic slack that had accumulated since oil prices plummeted in 2014. This is starting to become evident in inflation data, with two of the three core inflation measures produced by the Bank of Canada ticking up moderately in July. As such, a slowing housing market is unlikely to push the Bank of Canada onto the sidelines in the near-term should it remain a soft-landing scenario.

Canada: Upcoming Key Economic Releases

Canadian Retail Sales - June

Release Date: August 22, 2017

Previous Result: 0.6% m/m, ex-autos -0.1% m/m

TD Forecast: -0.4% m/m, ex-autos -0.6% m/m

Consensus: N/A

Retail sales are forecast to give back 0.4% in June following a number of upbeat retail reports. Gasoline station sales should serve as the primary catalyst for the pullback after another sizeable decline in the price at the pump, while motor vehicle sales could see an incremental gain from record levels. This should leave ex-auto sales weaker at -0.6% m/m, though much of that is driven by the aforementioned drop in gasoline sales. Broader measures of retail sales should see little change though household furnishings are likely to decline from May on the slowdown in the Toronto housing market. However, we do not think this will have a wider spillover to total retail sales given its isolated geographical impact and the fact that measures of consumer sentiment have remained upbeat. Because seasonally adjusted consumer prices were unchanged in June, real retail sales should come in near the nominal print.

Gold Hits Hits $1300 after Barcelona Attack

Gold prices continue to push higher. In the Friday session, gold punched past the $1300 level, before retracting. In North American trade, spot gold is trading at $1287.15, down 0.04% on the day. On the release front, it's a quiet end to the week, with just one key event on the schedule. UoM Consumer Sentiment improved to 97.6, beating the estimate of 94.0 points.

Geopolitical crises often have a strong impact on gold, which, as a safe haven asset, tends to rise when risk appetite is down. This was the case this week, with gold showing considerable volatility. Early in the week, gold prices dropped, as tensions between the US and North Korea eased. The crisis reached a fever pitch last week, as the saber-rattling between Washington and Pyongyang sent gold prices higher. Gold finds itself again in demand following a deadly car-ramming attack in Barcelona, Spain on Thursday. The terror attack killed 12 and wounded dozens, and the flight from risk towards gold sent the metal above the symbolic $1300 level on Friday, for the first time since November 2016.

In the US, political risk continues to rise, which is weighing on the US dollar. President Trump's administration continues to spend most of its focus and energy on damage control, and has failed to pass any major legislation through Congress, even though the Republicans control both the House and the Senate. The latest fiasco for Trump has been the alt-right protest in Charlottesville, where one protester was killed by a suspected white supremacist. Trump's belated condemnation of white supremacists and his insistence on blaming the violence on both the white supremacists and the counter-protesters has drawn wall-to-wall criticism from both Democrat and Republican lawmakers. Trump remains defiant and continues to attack his critics, but the events around Charlottesville have only served to tarnish his image and raised growing concerns about his presidency.

Yen Gains Ground on Barcelona Jitters

USD/JPY has edged lower in the Friday session. In North American trade, the pair is trading at 109.11, down 0.25% on the day. On the release front, UoM Consumer Sentiment improved to 97.6, beating the estimate of 94.0 points. There are no Japanese events on the schedule.

It's been a busy week for the Japanese yen, which has showed volatility in response to geopolitical events. The yen lost ground early in the week, as tensions between the US and North Korea eased after reaching a fever pitch last week. This trend didn't last long, however, as investors have once again snapped up the safe-haven yen following a deadly car-ramming attack in Barcelona on Thursday. The terror attack killed 12 and wounded dozens, and the yen responded with gains on Thursday.

In the US, political risk continues to weigh on the dollar. President Trump's administration continues to spend most of its focus and energy on damage control, and the latest fiasco for Trump has been the alt-right protest in Charlottesville, where one protester was killed by a suspected white supremacist. Trump's belated condemnation of white supremacists and his insistence on blaming the violence on both the white supremacists and the counter-protesters has drawn wall-to-wall criticism from both Democrat and Republican lawmakers. Trump remains defiant and continues to attack his critics, but the events around Charlottesville have only served to tarnish his image and raised growing concerns about his presidency.

The Japanese economy continues to show improvement in 2017, and this was underscored as Preliminary GDP in Q2 gained 1.0%. Japan has now posted a sixth consecutive of growth, marking the longest expansion in over a decade. A stronger global economy has boosted the export sector and domestic demand has rebounded. With a tight labor market and the business sector confident about economic conditions, better times could continue in 2017. The fly in the ointment remains inflation, as BoJ's ultra-easy monetary policy has failed to eliminate the threat of deflation. The BoJ has insisted that it will not tighten policy before inflation climbs closer to the bank's inflation target of 2%, but clearly this goal is unrealistic in the short term, and the BoJ may have to lower its inflation target.

Draghi Returns to Jackson Hole With a Dovish Message

Key points

- ECB president Draghi is returning from summer holidays and will speak at Jackson Hole for the first time since his 'QE hint' in 2014

- We expect a continued dovish stance from Draghi as the euro appreciation will dominate factors suggesting a more hawkish stance

- The ECB minutes revealed concerns about the euro overshooting which once again suggests the ECB's exit will be very gradual

- We expect the ECB to focus on the stock instead of the flow argument when revealing its QE strategy for 2018

The ECB president Mario Draghi is returning from summer holidays next week and all eyes will be on his communication following strong economic data but also a significant euro appreciation. Draghi is scheduled to give a keynote speech in Germany on Wednesday followed by his participation at the US Jackson Hole Symposium on 24-26 August. Market participants have speculated on Draghi seizing the opportunity to hint at QE tapering at Jackson Hole, which would be very symbolic following his indirect QE announcement at the symposium three years ago.

The speculation about Draghi signalling some kind of QE tapering at Jackson Hole was sparked after his hawkish twist at the ECB Forum on Central Banking in Sintra in June. Since then, a number of factors have supported the case for a hawkish view. First, the deflation risk has abated further while the stronger growth momentum - which Draghi was very focused on at Sintra - has continued. Second, the ECB's purchase pattern still suggests the QE restrictions are binding, implying the ECB could be looking for some sort of excuse to taper the purchases as the pressure for changing the restrictions again is likely to be muted given the above. Finally, Draghi will be among global central bank colleagues, which has on previous occasions resulted in him expressing a more hawkish stance as also seen at the ECB Forum in Sintra.

On the other hand, there are arguments for a continued dovish stance and in our view, they will dominate, implying Draghi will not send a new signal about QE tapering. The main argument why Draghi will not turn hawkish and signal QE tapering is that this could fuel the euro appreciation, thereby putting downward pressure on the outlook for growth and inflation, see Euro Area Research: Stronger EUR keeping inflation far from the ECB's target, 27 July 2017. This is in line with the communication in the ECB minutes from the meeting in July where 'concerns were expressed about a possible overshooting in the repricing by financial markets, notably the foreign exchange market' and that 'favourable financing conditions could not be taken for granted'.

Another argument for a continued dovish stance from Draghi is that any hints about the future of QE next week will be against the latest communication that this will be considered 'in the autumn', hence it could spark renewed criticism of Draghi's leadership style. Following Draghi's hint at QE at the Jackson Hole symposium in 2014, some Governing Council members criticised Draghi for erratic communication and urged him to act more collegially, see Reuters, 4 November 2014. Since then, Draghi's communication has been more cautious and we do not expect him to deviate from the communication at the ECB meeting in July where he said regarding the QE programme 'our discussion should take place in the autumn'.

Additionally, according to Reuters, sources familiar with the situation said this week that Draghi will not deliver a new policy message at Jackson Hole. According to the sources he will instead focus on the symposium theme 'fostering a dynamic global economy'. Moreover, the sources said that October is the most likely date for the most substantial decision given the incoming data schedule, particularly on wages (see chart 5), see Reuters, 16 August 2017. This is in line with our view that the ECB will announce a QE extension at the October meeting with some signalling of it in September.

A continued dovish stance will again be consistent with the ECB minutes from July which once again suggested the ECB's exit from its extraordinary monetary policy will be very gradual. As an example of this, the ECB decided in July not to give an incremental adjustment in the forward guidance as 'it was generally judged paramount at this stage to avoid sending signals that could be prone to over-interpretation and might prove premature'.

In addition, the minutes turned attention to the total stock of the QE programme versus the monthly flow effects of the QE purchases. When the ECB reveals its strategy for QE purchases beyond the currently communicated horizon we believe it will argue that it is adding more easing (higher stock), although we look for a slower pace of monthly purchases of EUR40bn (lower flow). Hence, we expect the ECB's communication to be anchored around the stock consideration in line with the announcement in December 2016, when the ECB extended QE by nine months but continued at a monthly pace of EUR60bn down from EUR80bn (see Chart 4). Furthermore, the ECB is likely to embrace the flow effect from the reinvestments when (as we expect) it reduces the monthly purchases.

Fixed income: a dovish message supportive for periphery bonds

If we see a dovish message from Draghi it should be supportive for European fixed income. Periphery bond markets in particular should benefit, as the risk of the PSPP purchases being tapered aggressively should be lower. We continue to favour the carry seen in the Italian and Spanish curves and to see the 5Y points as the 'sweet-spot'. But Bunds should also see support from a dovish Draghi, and a further Bund-spread widening should be expected. The lack of Bunds will increasingly be a market theme. The fixed-income market will also scrutinise any possible comments on how to reinvest in 2018.

FX: rangebound now - but more 'central-bank exit pricing' later

What does it mean for the FX market that the ECB (and other central bankers) are now starting to retreat a bit from the early-summer hawkishness. Looking back, central-bank communication during the month of June - topped by messages at the Sintra conference late in the month - turned notably more hawkish which we interpreted as a growing acceptance of USD weakness ahead, see e.g. FX Forecast Update: A Sintra accord? 14 July 2017. But since early August this has reversed somewhat with first the BoE keeping a dovish tone in August, then the Fed voicing very explicit concerns over inflation, and most recently the ECB sounding rather concerned regarding the risk of the euro rising too much too fast. Thus, it is back to trial-and-error mode - notably with respect to how communication affects currencies - for central banks in how they signal around their exit strategies - and this is set to continue well into a 'policy normalisation' process. In our view, for the near term this means both EUR/USD and EUR/GBP will stay within the recently established (higher) ranges, and we still see the former rangebound between 1.15 and 1.20 in 1-3M and EUR/GBP in the 0.90-0.92 interval near term. In the Scandi sphere, the situation is slightly different with notably the Riksbank looking into (temporarily) higher inflation prints; that said, we deem it is still too early for the FX market to price Scandi strength on a wider scale. In this week's FX Forecast Update: Taking a breather before next leg of 'central-bank exit pricing', 16 August 2017, we stress that we see ranges in many currency pairs near term but that the next leg of central-bank (ECB in particular) exit pricing will materialise later this year - and that EUR/USD in particular is headed for a firm move above 1.20 into 2018.

Week Ahead – Yellen and Draghi at Jackson Hole to Take Centre Stage in Quiet Data Week

All eyes will be on the central bankers gathering in Jackson Hole, Wyoming in the United States where the heads of the Federal Reserve and the European Central Bank will be making keynote speeches. The event will likely dominate traders' attention in an otherwise muted week for data releases. The main data to watch out for will be flash PMIs out of the Eurozone, Japanese inflation figures and durable goods orders in the US.

Eurozone business surveys in focus

It will be a loaded week for Eurozone business surveys as the closely watched flash PMI readings are released alongside the German ZEW and Ifo reports. Starting things off is the German ZEW survey on Tuesday. The ZEW economic sentiment index is expected to continue to retreat from May's two-year highs, though not straying too far from those levels. The current conditions index is also forecast to ease. The IHS Markit flash PMIs for August will follow on Wednesday. Activity in the euro area has been moderating from the six-year highs set in April according to the PMIs and this trend is expected to continue in August. The composite PMI is forecast to drop marginally from 55.7 to 55.5 in August. Rounding up the week on Friday will be the Ifo business sentiment gauge, which is not expected to buck the trend either and is also forecast to deteriorate slightly in August.

Japanese inflation to make another miniscule leap towards target

The Bank of Japan is expected to make another painstakingly slow progress towards its inflation goal with annual CPI excluding fresh foods inching up to 0.5% in July from 0.4%. However, this would still be a far distant from the 2% target and the data, due on Thursday, is unlikely to get much of a reaction in the forex markets as the BoJ is not seen to be withdrawing stimulus anytime soon. In the meantime, the latest bout of risk aversion that has generated fresh safe-have flows towards the yen could complicate the BoJ's efforts. Also to watch out of Japan next week is the flash Nikkei/Markit manufacturing PMI on Wednesday.

Canadian retail sales to stay strong

Buoyant consumer spending was one of the reasons why the Bank of Canada raised rates in July as retail sales have beaten expectations for the past three months. June retail sales numbers are out on Tuesday and another positive reading could help the Canadian dollar strengthen further as the loonie attempts to move back towards July's two-year peaks against the greenback after the recent correction.

UK GDP to remain unrevised

The UK will have a very quiet calendar week with the only major data being the second estimate of GDP growth for the second quarter. Growth is forecast to remain unrevised at a quarterly rate of 0.3%, having ended the first half with the slowest pace of expansion since 2012. The second reading will include a breakdown of business investment growth. A slowdown or a negative number would likely fuel fears that the Brexit uncertainty is hurting business spending just as UK consumers are feeling the pinch of living costs increasing faster than wages. Any downside surprises or negative aspects of the data could push sterling to fresh multi-month lows versus the euro.

Yellen and Draghi speeches eyed for market direction

Next week's US data is not expected to attract much headlines with the only major release being the durable goods orders on Friday. Durable goods orders are forecast to decline by 5.5% month-on-month in July, reversing much of the 6.4% gain from June. Before that, the flash manufacturing and services PMIs from IHS Markit will come into focus on Wednesday, along with new home sales. There will be more housing data on Thursday with existing home sales.

Fed Chair Janet Yellen and ECB President Mario Draghi could add some much-needed excitement to the week when they give speeches at the annual Jackson Hole Symposium on August 24-26. Both Yellen and Draghi are due to speak on Friday. Yellen is set to speak on financial stability, and contrary to market rumours, Draghi will not use his address to signal ECB tapering in the autumn. There had been speculation that Draghi would use his appearance at the conference to telegraph a possible tapering of the ECB's asset purchases. Back in 2014 when Draghi last attended the event, he had set the ground for the launch of the ECB's massive stimulus program. But according to a Reuters report, ECB sources have played down the prospect of Draghi delivering any new policy messages. Still, with the Fed getting ready to begin its balance sheet reduction and the ECB preparing to scale back its bond purchases, investors will be eagerly looking for fresh policy signals from the world's two most powerful central banks.

Weekly Market Outlook: Jackson Hole Economic Symposium, Key Data in Focus

Next week's market movers

- In the US, the annual Jackson Hole economic symposium will kick off. Keynote speakers include Fed Chair Yellen and ECB President Draghi, which suggests that the financial world will be tuned in for any fresh policy signals.

- In Japan, core inflation is expected to accelerate slightly. Even though that would be encouraging for the BoJ, we think it is far too early for speculation regarding a potential reduction in stimulus.

- We also get key economic data from Germany, Norway, the Eurozone, the UK, and the US.

On Monday, we have a relatively quiet day, with no major events or indicators on the economic agenda.

On Tuesday, Germany will release its ZEW survey for August, while on Friday, we get the nation's Ifo survey for the same month. The forecast is for all of these indices to decline slightly, but to still remain at healthy levels. Even though the ZEW expectations index declined somewhat in recent months, the survey's current conditions print remained near all-time highs. Meanwhile, the Ifo composite index hit a new record high in July for the third consecutive month, indicating that "sentiment among German businesses is euphoric", as the Ifo institute phrased it. As such, we doubt that any minor decline in these figures will be particularly worrisome for ECB policymakers.

On Wednesday, Eurozone's preliminary manufacturing and services PMIs for August will take center stage. The forecast is for the manufacturing index to slip somewhat, while the services print is expected to hold steady. These indices pulled back somewhat in the past few months, though they still remain at relatively elevated levels compared to recent years, suggesting that the bloc's economic recovery is continuing at a solid pace. Thus, we believe that even in case of a modest tumble in the manufacturing print, as long as these figures remain at healthy levels, they are unlikely to derail the ECB's policy plans. We still see the case for an announcement regarding a reduction in stimulus at one of the upcoming policy meetings (see below).

On Thursday, in the US, the annual Jackson Hole economic symposium will commence (24th - 26th). Organized by the Kansas Fed, this is a major event where the world's top policymakers gather to exchange ideas. This time will be no different, with two of the keynote speakers being ECB President Mario Draghi and Fed Chair Janet Yellen, both of which speak on Friday.

Kicking off with Draghi, ahead of this gathering there were expectations that he was going to use this speech to provide some hints about an eventual exit from QE. However, on Wednesday, a media report familiar with ECB sources suggested that he will not deliver a fresh policy message, but will instead focus on the theme of the symposium; fostering a dynamic global economy. It's not all discouraging news for EUR-bulls though. Since Draghi is unlikely to deliver major policy signals, that means he is also less likely to use this speech as an opportunity to jawbone the euro. In any case, despite this report, we still believe that investors will be hanging on Draghi's lips for any potential policy comments. "ECB sources" do not carry the same credibility as official ECB communication, implying there is still a probability (albeit a modest one) that Draghi does mention ECB policy and/or the euro in his remarks. If he does, we think it is likely to be a moderate message that avoids hinting directly at tapering, in order to avoid further euro appreciation and an unwanted tightening of financial conditions.

As for the bigger picture, the ECB remains set to make an announcement around QE tweaks in the "autumn", which suggests we will probably get fresh signals at the September or October meetings. Although incoming data will likely play a critical role, we think that a realistic scenario is one where the Bank removes it QE easing bias in September, thereby paving the way for a formal announcement in October that the pace of QE purchases may be reduced by the turn of the year.

With regards to Fed Chair Yellen, her speech will center on financial stability and as such, any comments on the pace of future rate hikes appear somewhat unlikely. That said, same as with Draghi, her remarks will still be watched closely as she could always make a reference to the outlook of the US economy that indirectly conveys her policy view. Should she echo recent comments from New York Fed President William Dudley and hint that she could vote in favor of another rate hike this year, markets could reprice the likelihood for such action. The probability for another hike this year declined further recently, after the July FOMC minutes showed more officials being concerned with low inflation, and now rests at 40% according to the Fed funds futures.

In the UK, the 2nd estimate of GDP for Q2 is due out. The forecast is for the 2nd reading to confirm the preliminary one and show that UK growth was only +0.3% qoq. If we were to see any revision, we think that it could be to the upside, as the only major indicator for Q2 released after the first GDP estimate was industrial production for June, which was stronger than expected. Besides the GDP print, this data set will also include business investment data for Q2, which we expect to attract a lot of attention. Back in June, BoE Governor Mark Carney noted that a BoE rate hike may depend mainly on whether weaker consumption growth is offset by stronger business investment, and on whether wages begin to firm. Given that wages have shown little-to-no signs of firming in recent months, a pick up in business investment may be needed to keep alive some speculation for a BoE hike. If we were to see investment moderating as well, then the market probability for a rate increase this year could drift towards 0%, from 20% currently according to the UK OIS.

In Norway, GDP data for Q2 will be in focus, though no forecast is available. We see the case for the nation's growth rate (mainland) to have held steady, with risks skewed to the downside. On the bright side, the unemployment rate continued to drop throughout the quarter, while manufacturing production was stronger compared to Q1. However, retail sales were somewhat weaker than the previous quarter, making us believe that the robust +0.6% qoq growth rate in Q1 may not necessarily be sustained, as the Norges Bank anticipates in its latest forecasts. Having said that, even if growth slows slightly, as long as it remains close to the NB's own estimate, we don't expect this to lead to a dovish shift in the Bank's bias.

Finally on Friday, Japan's CPI data for July will be in the spotlight. No forecast is available for the headline print, while the core CPI rate is expected to have ticked up. Our own view is that the headline rate could rise as well, something that we base on the nation's forward-looking Tokyo CPIs for the month, where both the headline and the core rates moved higher. Even though further progress in the inflation outlook would undoubtedly be encouraging news for BoJ policymakers, we think it is far too early for speculation regarding a potential reduction in stimulus. Under its QQE with yield curve control framework, the Bank has explicitly committed not only to achieve its 2% inflation target, but to actually overshoot it. Thus, even in case the CPI rates rise somewhat further, as long as they remain so far from the target, we maintain our view that the BoJ is likely to keep its ultra-loose policy framework in place.

From the US, we get durable goods orders for July. The consensus is for the headline rate to have dropped notably following an astonishing 6.4% mom increase in June, while no forecast is available for the core rate. Our own view is that we could see the core rate dip as well, something that we base on the nation's ISM manufacturing PMI for the month, where the New Orders sub-index declined.