Sample Category Title

Sterling Heads Up as UK Unemployment Hits 42-Year Low; Dollar Reaches Fresh Three-Week High

With North Korea and the US pulling back from their confrontation stance, the focus turned back to economic releases. The dollar followed an upward path despite weaker housing data, while better than expected labor figures in the UK pushed sterling higher. The lowered US crude inventories published during late European session lifted oil prices.

The dollar index peaked at a fresh three-week high of 94.14 during the European session, ignoring today's disappointing US data on building permits and housing starts. In July 1,223 million new buildings were authorized to be constructed, a number that was below the forecast of 1,250m and the previous reading of 1,275m. Relative to the previous month, this translates to a negative change of 4.1%, while expectations were for a 2% reduction. This followed a boost of 9.2% in June which was the highest monthly rate experienced since November 2015.

New residential buildings rose by 1,155m (annualized), falling short of 1,220m expected and 1,213m observed in the previous month. On a monthly basis, housing starts shrank by 4.8% compared to a growth of 7.4% in June and a 0.5% rise projected.

Now, the US economic calendar is pending the Fed meeting minutes. Those will be released today at 1800 GMT. The minutes are expected to shed some light on the reasons Fed policymakers held their policy steady and give more details on whether the central bank will proceed with another rate hike, justifying the New York Fed President William Dudley who claimed that a third hike might be needed before the year ends. In addition, investors will look for clues on the timing the Fed will start unwinding its balance sheet. Besides that, investors will keep a close eye on any developments in the NAFTA negotiations which kicked off today and expected to end on August 20.

The safe havens yen and gold continued their downtrend for the third day after risks of a nuclear war was played down, motivating investors to buy back riskier assets. Dollar/yen was last trading at 110.76, while the yellow metal was last seen at $1271.83 per ounce.

Meanwhile, in the UK, the Office for National Statistics published better than expected labor data, giving some support to sterling. According to the numbers, the unemployment rate edged down by 0.1 percentage points to 4.4% in June, better than the 4.5% that was expected by the forecasters. This was the lowest level reported since 1975 and was below the BOE's threshold of 4.5%. The office also released the change in the number of unemployed people for the month of July. Unemployed people surprisingly reduced by 4,200 for the first time after four months of rises, while analysts anticipated an increase by 3,700. In June, the figure had climbed by 3,500 (a downward revision from 6,000).

Moreover, weekly average earnings (three months) including bonuses in the three months to June grew unexpectedly by 2.1% y/y, compared to 1.9% in May (upwardly revised from 1.8%), while forecasts were for a rise of 1.8%. Excluding bonuses, earnings were up by 2.1% and above the forecast of 2%, which was also May's reading. Although wages started strengthening, British consumers could still feel inflationary pressures in their spending as prices grew faster than earnings. This also weighed on economic expansion which dropped this year and motivated BOE policymakers to lower GDP growth forecasts for the next two years.

As a response to the above, sterling jumped immediately by 0.36% to an intra-day high of $1.2901. However, its gains were short-lived as cable fell back to $1.2857 in late European session. Versus the euro, sterling climbed by 0.42% with euro/sterling sinking to 0.9099.

The euro reversed yesterday's gains against the greenback as media sources announced that the ECB chief Mario Draghi would not use the US Fed's Jackson Hole conference next Friday to deliver a message about the ECB's strategy to tighten monetary policy. Given the positive economic climate in the block, investors expected Draghi to take the opportunity and signal the start of unwinding the banks' ultra-loose monetary policy despite him saying in the last policy meeting he would hold off on the discussion until autumn. Before the news spread out, the euro was struggling to find support on preliminary GDP data out of the Eurozone. The GDP growth prints showed that eurozone's output expanded slightly by 0.1 percentage points in the second quarter to 2.2% y/y, surpassing the forecast of 2.1%. On a quarterly basis, the output growth remained unchanged at 0.6% as expected.

The euro changed hands with the dollar at $1.1694.

In the commodity markets, oil prices rose after the EIA report showed that US crude oil inventories fell by 8,945 million barrels last week, while expectations were for a drop of 3,058 million barrels. This reduction was the largest tracked since September 2016. In the preceding week ending, inventories were down by 6,451 million. On the day, WTI crude was 0.5% down at $47.33 per barrel, while Brent was up on the margin at $50.82 per barrel.

The commodity-linked loonie reacted positively to the EIA report, with dollar/loonie falling by 0. 50% to 1.2691.

Gold Halts Slide, FOMC Minutes Next

Gold has posted slight gains in the Wednesday session, following two consecutive days of losses. In North American trade, spot gold is trading at $1273.64, up 0.18% on the day. On the release front, housing numbers were weaker than expected. Building Permits dipped to 1.22 million shy of the forecast of 1.25 million. Housing Starts slowed to 1.16 million, missing the estimate of 1.22 million. Later in the day, the FOMC will release the minutes of its July policy meeting. On Thursday, there are two major events in the US – unemployment claims and the Philly Fed Manufacturing Index.

There was positive news from the consumer front, as Retail Sales and Core Retail Sales both beat their estimates, with gains of 0.6% and 0.5%, respectively. Consumer spending numbers are closely watched, as they are a key driver of economic growth. The strong gains in retail sales have helped raise investor risk appetite, which took a hit last week over the crisis in the Korean peninsula. This has boosted the stock markets, but hurt gold prices. Last week, tensions soared between the two enemies, sending gold about 2.4%, as investors dumped shares and snapped up the safe-haven metal. With the tension temperature dropping this week, risk appetite has returned, and gold prices have dropped 1.2% so far this week.

The Federal Reserve releases its July minutes later on Wednesday, and the markets will be listening closely. Although the minutes might not shed light on the likelihood of a rate hike before the end of the year, analysts will be looking for further details about the Fed's balance sheet, which has ballooned to $4.2 trillion. At the June policy meeting, the Fed outlined plans to begin reducing the balance sheet, but shied away from providing any details regarding the size of the reductions or a start time for the plan. Analysts expect September will be the start date, and the Fed could start the process by slowing its asset purchases by a modest amount, such as $10 billion/mth. Once the reductions start, the US dollar stands to gain ground for two reasons. First, the move would mark a vote of confidence in the US economy. Second, a reduction of $60 billion is expected to have the same effect as a quarter-point rate hike, which would make the dollar a more attractive asset for investors. In turn, this could weigh on gold prices.

Housing Starts Disappoint in July

Housing starts fell 4.8 percent to a 1.16 million-unit pace in July. Weakness was largely concentrated in multifamily, which fell 15.3 percent, while single-family slipped 0.5 percent. Permits fell 4.1 percent.

Single-Family Starts Better Than Monthly Print Implies

At first glance, today's housing starts report appears to extend a weak string of monthly reports only interrupted by the downwardly-revised gain in June. Moreover, given the ebullient builder sentiment reading yesterday, weakness in housing starts and permits during the month is a bit confounding. Indeed, housing starts have fallen in five of the last six months. However, much of the weakness has been in the multifamily component, which should not be surprising given slowing fundamentals.

To illustrate, starts are down 5.6 percent relative to a year earlier, but all of the weakness is concentrated in multifamily (5+units) which fell 35.2 percent in July, while single-family was up almost 11 percent. We find a similar trend with permits, which are forward-looking. On a year-ago basis, overall permits are up 4.1 percent, but the gain is in single-family and multifamily units with 2-4 units, while five or more units is down.

At the same time, builder sentiment jumped 4 points in August to 68, which is in line with the six-month moving average, with all components registering gains during the month. In our National Association of Home Builders/ Wells Fargo Housing Market Index write up released yesterday, we noted that single-family starts have not advanced as much as the stillelevated level of builder sentiment likely reflecting the shortage of lots and overall construction costs including labor. That said, the producer price index shows that inputs to residential construction rose 2.5 percent yearover- year in July, outpacing inflation. The shortage of labor is also putting upward pressure on construction costs and can be seen in average hourly earnings in the residential component.

Looking Ahead: The Residential Story Is Unchanged

For starters, residential lending standards are still supportive of the sector. On net, senior loan officers reported that standards for all residential real estate lending categories eased or were unchanged in Q2, while demand for most segments remained strong. Consistent with lending standards, loan growth for single-family residential (1-4 units) grew more than 11 percent in Q1 relative to a year earlier, which is more or less consistent with the pace of construction and land development loan growth. Lending for multifamily loans remained largely unchanged during the quarter.

Multifamily housing units (5+ units) completed, which reflect deliveries, were up almost 7 percent year-over-year in July. Much of the supply is still in luxury units. We continue to expect multifamily completions to peak this year, which should level off the recent moderation in asking rent growth.

The residential component of architecture billings, which is mostly apartments, jumped to its highest level in almost a year in June, intimating there is some upside.

Pound Yawns Despite Solid British Job Numbers

The British pound is showing limited movement in the Wednesday session. In North American trade, the pair is trading at 1.2864, down 0.05% on the day. On the release front, British employment numbers looked sharp. Average Earnings Index accelerated to 2.1%, above the estimate of 1.8%. Claimant Change declined 4.2 thousand, compared to an estimate of a gain of 3.2 thousand. Finally, the unemployment rate dropped to 4.4%, edging below the forecast of 4.5%. Over in the US, housing numbers were softer than expected. Building Permits dipped to 1.22 million shy of the forecast of 1.25 million. Housing Starts slowed to 1.16 million, missing the estimate of 1.22 million. Later in the day, the FOMC will release the minutes of its July policy meeting. On Thursday, the UK releases Retail Sales. There are two major events in the US – unemployment claims and the Philly Fed Manufacturing Index.

The pound lost ground on Wednesday, as British CPI remained unchanged at 2.6% in July. Inflation has dropped considerably since May, when CPI came in at 2.9%. With inflation levels weakening, the pressure has eased on the BoE to raise interest rates. BoE policymakers have been divided over monetary policy, with recent policy meetings showing a sizable majority in favor raising rates. However, BoE Governor Mark Carney has come out against raising hikes in the near future, citing continuing uncertainty on how Brexit will affect the UK economy. The BoE still sees high inflation levels ahead, saying that CPI could hit around 3% in October. This means that policymakers will have to make some tough decisions regarding interest rate policy in the next few months.

With the reality of Brexit coming ever closer, there are growing concerns in the British business sector, notably what happens on the "day after". There has been discussion about a transition period, before the actual departure date from the European Union. This would minimize the destabilizing effect of Brexit on the British economy. On Tuesday, the government said that it will seek an "interim customs agreement" with the continent, which would last up to two years. Under the proposal, Britain would enjoy tariff-free trade with the EU, while being able to negotiate free trade agreements at the same time. However, it's questionable whether the EU, which has already taken a hard negotiating stance with Britain, will agree with such an arrangement. The two sides will meet next on August 28 for another round of what promise to be arduous talks.

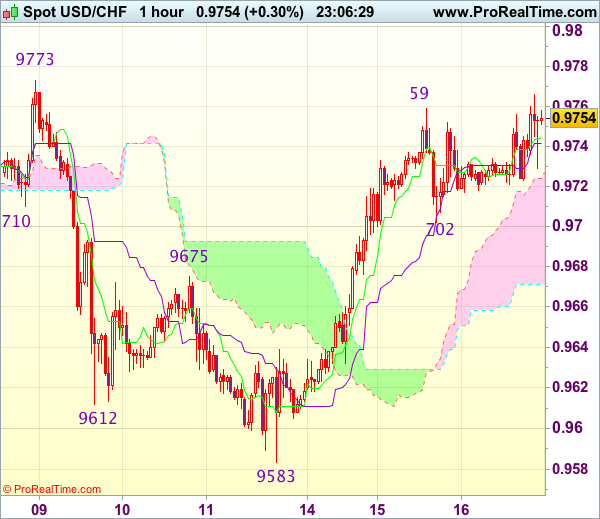

Trade Idea Wrap-up: USD/CHF – Buy at 0.9680

USD/CHF - 0.9749

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9745

Kijun-Sen level : 0.9642

Ichimoku cloud top : 0.9724

Ichimoku cloud bottom : 0.9671

Original strategy :

Buy at 0.9690, Target: 0.9790, Stop: 0.9655

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9680, Target: 0.9780, Stop: 0.9645

Position : -

Target : -

Stop : -

As the greenback has maintained a firm undertone after staging a strong rebound from 0.9583 (last week’s low), adding credence to our view that the retreat from 0.9773 has ended there, hence consolidation with upside bias remains for another test of said resistance, however, break there is needed to confirm early rise from 0.9438 low has resumed and extend gain to 0.9808 and possibly 0.9825 resistance, having said that, near term overbought condition should limit upside and price should falter below previous support at 0.9859.

In view of this, we are looking to reinstate long on pullback as 0.9690-95 should limit downside and bring another rise later. Below previous resistance at 0.9675 would defer and risk weakness towards 0.9640 but downside should be limited to 0.9615-20 and bring another rise later.

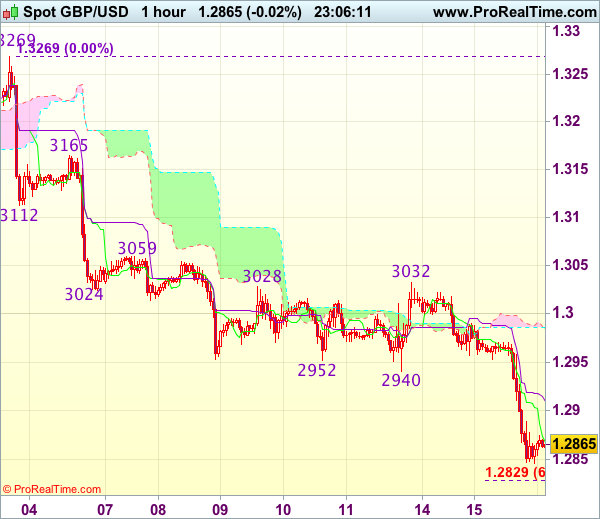

Trade Idea Wrap-up: GBP/USD – Sell at 1.2920

GBP/USD - 1.2863

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2868

Kijun-Sen level : 1.2910

Ichimoku cloud top : 1.2986

Ichimoku cloud bottom : 1.2984

Original strategy :

Sell at 1.2920, Target: 1.2820, Stop: 1.2955

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.2920, Target: 1.2820, Stop: 1.2955

Position : -

Target : -

Stop : -

As cable has remained under pressure after breaking below support at 1.2933-40, adding credence to our bearish view that the decline from 1.3269 top is still in progress for retracement of early upmove, hence downside bias remains for further weakness to 1.2825-30 (61.8% projection of 1.3269-1.2940 measuring from 1.3032), having said that, near term oversold condition should limit downside to 1.2800 and reckon 1.2770 would hold from here, bring rebound later.

In view of this, would not chase this fall here and would be prudent to sell sterling on recovery as said previous support at 1.2933 should turn into resistance and cap cable’s upside, bring another decline. Above 1.2950 would defer and risk a stronger rebound to 1.2990-00 before another decline.

Ahead of Fed & ECB Minutes

Commodity currencies dominate a quiet Wednesday summer session as traders await this evening's release of the minutes from the Jul 26-27 FOMC meeting. Recall the dollar fell sharply on that day, partly due to escalating adversity between the White House and Washington as well as the Fed statement itself.

So what did the Fes say on Jul 27? The Committee made two minor changes: i) saying inflation was 'below' target rather than 'somewhat below'; and; ii) that the balance sheet runoff will start 'relatively soon' which could mean later than September. Also note that 3 weeks after the Fed decision, July CPI was a miss. Today's minutes may further enlighten us whether the inflation tweek was a mark-to-market reflection or a possible sign of the Fed's plan.

Let's also not forget tomorrow's release of the ECB minutes from the Jul 20 meeting/press conference, which triggered broad EUR strength and sharp DAX selling after the ECB was perceived to be largely on course towards curtailing QE. Today's rally in the DAX and retreat in the euro were spurred by Reuters reports that Draghi will not make any policy-related remarks at next week's scheduled speech at the Jackson Hole symposium, thus, allaying (or delaying) worries about any references to a curtailing QE. Yet, this remains a matter of "when" rather than "if".

Mixed UK Data and Brexit Uncertainty Cloud Outlook for Sterling

After being criticised by EU officials for turning up at the negotiating table unprepared, the UK has this week published its most comprehensive vision yet of a post-Brexit relationship with the bloc. The British government published yesterday its first policy paper on a future customs agreement with the European Union, and is due to soon release a paper on Northern Ireland and its border arrangements with the Irish Republic.

The paper calls for a new customs partnership with the EU with the aim of achieving "as frictionless as possible" trade between the UK and the EU. Aside from the desire to maintain a barrier-free trade with the EU, the British government wants to avoid a return to a hard-border between Northern Ireland and the Republic of Ireland as this could jeopardise the Peace Process in the province. Also outlined in the paper are proposals for an interim arrangement for a "time-limited period" to allow UK businesses to adjust to the new customs agreement once Britain is out of the EU.

The proposal for an interim customs system is a welcome relief for the UK business community who feared a cliff-edge scenario when the prime minister, Theresa May, raised the prospect of a 'hard Brexit' in her first major speech on the UK's exit plans back in January. Signs that the government is now shifting towards the idea of having a transitional agreement in place once the UK leaves the EU in March 2019 have helped the pound move towards 10-month highs against the US dollar, rising above $1.32 earlier this month.

The turnaround came after the Prime Minister lost her parliamentary majority in June's snap election, which had the opposite intention of strengthening her negotiating hand in what proved to be a major political misjudgement. Many blamed the Conservatives' poor performance in the election on the government's hard line on Brexit, with the shock vote outcome giving an unexpected boost to the Remainers within May's cabinet, notably, the finance minister, Philip Hammond.

Amid all the political headlines, a more hawkish Bank of England has also lifted the pound, as surging import costs, brought on by sterling's post-Brexit depreciation, pushed UK inflation to near 4-year highs in May. However, CPI has eased back to 2.6% in June and July, alleviating some of the pressure on the Bank to act sooner rather than later.

The pound slipped back below the $1.29 level after this week's July inflation data, but more crucial will be Thursday's retail sales figures. Annual retail sales have moderated significantly in 2017 compared to last year. Household consumption comprises around 65% of UK GDP and a slowdown in spending would have a significant impact on growth, especially as so far, the weaker pound has not provided much of a boost to exporters. Rising exports and a subsequent increase in business investment has the potential to offset any decline in consumer spending.

A persistent weakness in consumption would mean the UK economy will likely continue growing at around the sluggish rate of 0.2-0.3% seen during the first two quarters of the year. This would make it more difficult for the BoE to raise rates when growth is so low and the economy vulnerable to Brexit developments. Without a rebound in consumer spending in sight, sterling could further reverse some of its impressive gains made since April.

Not all data has been feeble however, with the UK labour market remaining robust. Figures released today showed the jobless rate fell to a 42-year low of 4.4% in the three months to June. Wage growth also came in above expectations, picking up to 2.1% during the same period (though this is still below the rate of inflation). Further gains in earnings growth would be viewed as being positive for higher consumer spending and would ease concerns of a prolonged downturn in consumption.

It would also give more weight to the hawkish voices within the BoE's Monetary Policy Committee. With more MPC members becoming uncomfortable with inflation running above their target, the Bank may feel confident enough to overlook the current soft patch in the economy and raise rates on the expectation that higher wage growth will keep CPI running above 2%.

The constantly altering outlook for UK rates has become a bigger factor driving the pound in recent weeks, with the UK currency becoming less sensitive to the Brexit negotiations. However, it is too early to rule out further big political shocks causing disruption in the forex markets as no conclusive agreement has yet to emerge from the Brexit talks, while Theresa May's future in Number 10 looks highly uncertain and another fresh election plausible.

In the meantime, the broader dollar weakness and the resurgent euro have also influenced the outlook for the pound, particularly the single currency, which has risen to 10-month highs of above 0.91 pounds this week. Morgan Stanley projected last week the euro would hit parity with the pound in 2018, though other forecasts are a bit more bullish for sterling. Some analysts see the euro rally as overdone as the excessive rise in euro/dollar is not supported by a corresponding increase in either the short- or long-term yield differentials between US and German government bonds, suggesting the moves are mostly speculative.

According to the latest Reuters poll, forecasts for pound/dollar during Q3 2017 and Q2 2018 range between $1.15 and $1.44, while for euro/pound they stand between 0.77 and 1.03 pounds. For now though, the pound remains well supported above $1.26, but may struggle to climb past $1.33 without a fresh breakthrough in the Brexit negotiations or signs that the UK economy is gaining traction.

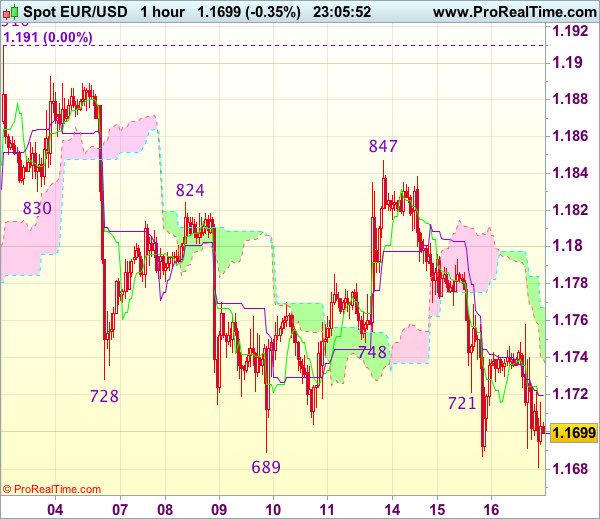

Trade Idea Wrap-up: EUR/USD – Hold short entered at 1.1755

EUR/USD - 1.1705

Most recent candlesticks pattern : N/A

Trend : Sideways

Tenkan-Sen level : 1.1720

Kijun-Sen level : 1.1720

Ichimoku cloud top : 1.1767

Ichimoku cloud bottom : 1.1739

Original strategy :

Sold at 1.1755, Target: 1.1655, Stop: 1.1755

Position : - Short at 1.1755

Target : - 1.1655

Stop : - 1.1755

New strategy :

Hold short entered at 1.1755, Target: 1.1655, Stop: 1.1755

Position : - Short at 1.1755

Target : - 1.1655

Stop : - 1.1755

Euro’s selloff after meeting renewed selling interest at 1.1847 signals the erratic fall from 1.1910 top is still in progress and mild downside bias remains for further weakness to 1.1640-50 (50% Fibonacci retracement of 1.1370-1.1910 and previous support), below there would encourage for subsequent decline towards 1.1600-10 which is likely to hold from here due to near term oversold condition.

In view of this, we are holding on to our short position entered at 1.1755. Above 1.1755-60 would defer and risk a stronger rebound to 1.1790-95, break there would abort and signal a temporary low is possibly formed, bring subsequent gain to 1.1820 but price should falter below said resistance at 1.1847.

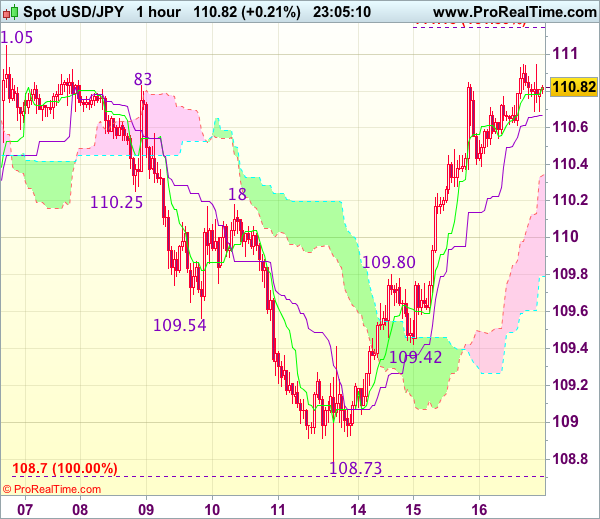

Trade Idea Wrap-up: USD/JPY – Buy at 110.00 or sell at 111.45

USD/JPY - 110.80

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 110.82

Kijun-Sen level : 110.67

Ichimoku cloud top : 110.34

Ichimoku cloud bottom : 109.79

Original strategy :

Buy at 110.20, Target: 111.20, Stop: 109.85

Position : -

Target : -

Stop : -

New strategy :

Buy at 110.00, Target: 111.00, Stop: 109.65

O.C.O.

Sell at 111.45, Target: 110.45, Stop: 111.80

Position : -

Target : -

Stop : -

As the greenback has risen again after brief pullback, adding credence to our bullish view that the rebound from 108.73 low is still in progress, hence gain to previous resistance at 111.05 cannot be ruled out, break there would extend this rise for a stronger correction of early decline to 111.45-50, having said that, loss of upward momentum should prevent sharp move beyond there and price should falter below previous resistance at 111.71, bring a strong retreat later.

In view of this, whilst we are still looking to buy dollar on pullback, we are inclined to sell dollar on subsequent rally. Below previous resistance at 109.80 would signal top is formed instead, bring weakness towards support at 109.42.