Sample Category Title

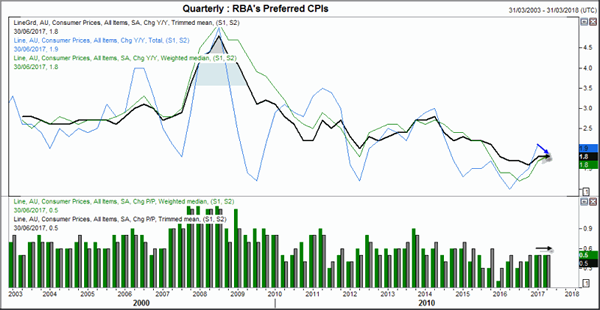

AU CPI Softens But It’s Not Necessarily A Game-Changer

Weak inflation is not an ideal scenario for a central bank which is looking to improve it. Yet as trimmed and median hit consensus and RBA expect inflation to be variable then it may not be as bad as first feared.

Broad CPI read let the team down by missing expectations and softening on a quarterly and annual basis. Broad weakness for AUD ensued where AUDNZD felt the biggest squeeze just moments after the release. Trimmed mean, the RBA's preferred inflationary gauge softened form 1.9% YoY to 1.8%, yet this was the consensus figure, so this may not come as too much of a surprise.

Debelle may be feeling a touch of 'I told you so' and now Lowe may get to rub it in a little, but overall the downside for AUD is limited. Today's CPI data doesn't really change the underlying issues of a higher AUD; the US Dollar remain on the back ropes and AU sensitive commodities remain elevated. Until this scenario changes then verbal interventions will only provide limited pullbacks but, for now at least, 80c appears to be safe from bulls.

As quarterly CPI for weighted and trimmed have moved sideways for two quarters (three quarters for trimmed) then we expect a basing effect to take hold on these measures and support them. Although headline CPI has moved lower, this is partly to do with lower petrol prices and, whilst still followed by the RBA, is not their favoured measure as it is more volatile.

When you break down the CPI data into sectors, it has predominantly been led higher by health, with furnishings, alcohol & tobacco and housing. The biggest drags on the headline figure are recreation & culture, transport, communication, clothing 7 footwear and food & non-alcoholic beverages.

AUD has respected the weekly pivot (0.7894) to provide interim support ahead of the Fed meeting. We may find the 0.7873 level also tested upon any spikes lower but in all the time we remain above the 2016 high, we expect traders to buy the dip and take advantage of the weaker Greenback.

The downside on AUDJPY has also been limited as market sentiment overnight was a classic risk-on. Stocks broke to new highs and dragged yields higher whilst VIX moseyed on down to a record low. This environment favours carry trades such as AUDJPY, so we continue to think AUDJPY may eventually move its way to Y90 over the coming weeks unless risk-off rears its ugly head.

GBPAUD could be setting up for a swing trade short. 1.65 resistance is close to monthly S1 which allows for a little noise around this bearish zone. If we are to see Sterling move lower then this should help GBPAUD towards an inverted hammer or bearish signal of some sorts. If you were confident resistance may hold then a market order or sell-limit may be used to capture an anticipated move. Or for extra confirmation, await for NY close to assess the daily candle or simply use a sell-limit beneath today's low as part of a set and forget entry.

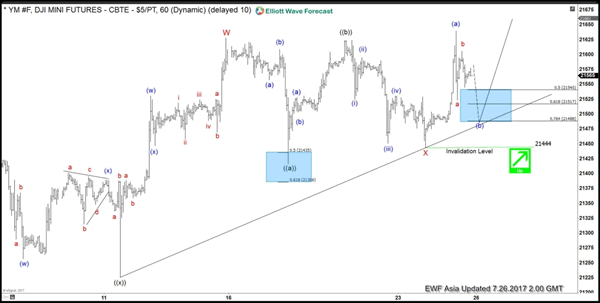

Elliott Wave View: Dow Future Resuming Higher

Short term YM_F (Dow E-Mini Future) Elliott Wave view suggests the rally from 6/29 low is unfolding as a double three Elliott wave structure and ended with Minor wave W at 21628. Down from there, Minor wave X pullback unfolded as a running Elliott Wave flat. Minute wave ((a)) ended at 21457, Minute wave ((b)) ended at 21624, and Minute wave ((c)) of X ended at 21444. Index has since made a new high suggesting the next leg higher has started. Up from 21444 low, Minutte wave (a) ended at 21640. While Minutte wave (b) pullback stays above 21444, expect Index to extend higher again.

Alternatively, the new high at 21640 could still be Minute ((b)) and part of a flat from 21628 high. In this case, we could still see Minute wave ((c)) lower in 5 waves before Index resumes the rally. We don't like selling the Index and expect more upside against 21444 low in the first degree.

Dow E-Mini Future 1 Hour Elliott Wave Chart

Market Morning Briefing: The FOMC Policy Statement Tonight May Dictate The Near Term Path For The Majors

STOCKS

Dow (21613.43, +0.47%) could be ranged within 21700-21500 for the next couple of sessions. There is some chance of testing 21800 on the upside while immediate support near 21500 holds.

Dax (12264.31, +0.45%) is trying to recover from levels near 12140, and could rise towards 12400 once again in the coming sessions. There is some support visible near 12000 on the 3-day charts coming up from June’16 and while that holds, Dax is likely to recover in the near term with some chances of a dip towards 12000-11870.

Shanghai (3240.27, -0.11%) is almost stable and could either come off or remain sideways from levels near 3260/70. There is room on the downside towards 3200 which is possible before again moving up to current levels.

Nikkei (20048.62, +0.47%) has moved up a bit as Dollar Yen and the US-Japan yield spread has bounced up a bit. Decent support is visible near 19600 and while that holds, the index could move up towards 20500 in the coming weeks.

Nifty (9964.55, -0.02%) opened at 10011 yesterday before coming off sharply to close near 9964. As we have been mentioning, 10000-10050 levels could act as an immediate resistance and while that holds, we may expect some correction in Nifty in the near term.

COMMODITIES

Gold (1247) is trading within the range of 1245-58. It has a crucial Support at 1245. If that holds, we can see a rise towards 1258 and 1270. But, in case the Support at 1245 breaks, there will be a further dip to 1230 and 1210. Silver (16.40) is also within the range of 16.20-16.50.Only a close below 16.20 could open up 15.90 and 15.50 respectively.

Copper (2.83) looks on a firm footing as it sustain the higher levels. We were bullish on copper since 22nd of June 17 and the intraday highes of 2.85-89 were at par to our initial targets. Our next target of 2.95 and 3.00 may be achieved in the rest of the week. Midterm resistance comes at 3.08-12 regions from where we may see some correction due to short term profit taking.

Oil Price rose higher in line with our expectation. Both Brent (50.56) and WTI (46.34) September contacts are trading within the ranges of 49.60-51.30 and 47.60-49.50 respectively. We are bullish on oil since 10th of July 17 onward and there is no reason to change our bullish stance in near term while Brent and WTI are trading above 47.70 and 45.50 on a weekly closing basis. We have U.S weekly crude oil inventory data today at 8:00 p.m IST. If the anticipation of -3.3 M Barrel of shortage will match the actual outcome, we might see further rally toward 51.50 (Brent) and 49.70 (WTI). A weekly close above those levels might confirm the end of the midterm bearish trend too.

FOREX

The FOMC policy statement tonight may dictate the near term path for the majors, especially if there is any specific hints regarding normalization of the Fed balance sheet.

A rise in German business confidence at 116.00 against the expectations of a drop to 114.90 had pushed Euro (1.1650) above 1.17 but it was rejected exactly at the resistance of 1.1712 we have been following. Unless we see a weekly closing above 1.1712, this latest phase of the rise remains a bit suspect as it remains in the most overbought state since 2008.

Dollar Index (94.06) remains almost unchanged with the trend firmly down. Only a bounce above 94.65 can give initial hints about a recovery but till then, the downside target of 93.00 remains a strong possibility.

Dollar Yen (111.89) has bounced back sharply as expected and now if it manages a break above 112.10, the bounce may extend higher to 112.55 and 113.00. Immediate support comes at 111.50-15.

Aussie (0.7914) continues its consolidation with the larger trend up. With Copper (2.88) surging to a fresh 26-month high (Check Commodities section), the probability of further rise towards 0.80+ levels in the coming sessions strengthens considerably.

It was a day for mute price action for Dollar-Rupee (64.38) as expected but the range boundaries of 64.28-60 may be tested in the next couple of sessions . Bias neutral at this point.

INTEREST RATES

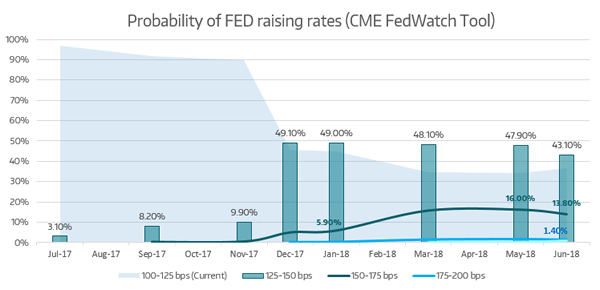

Market awaits the FOMC meeting tonight. Although the rates are likely to remain unchanged the market would look for firmer statements on the timings to start the effort on reducing the balance sheet. The probability of a rate hike in September has risen to 91.6%.

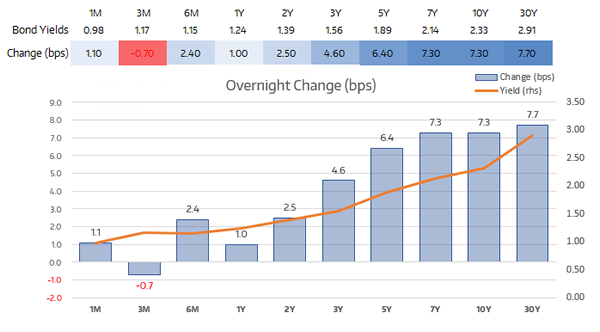

The US yields have risen sharply ahead of the FED meet tonight and could re-test the medium term resistance in the coming sessions. The 30Yr (2.91%) is trading close to the medium term resistance of 3% and while that holds, not much room is available on the upside just now. Unless the 30YR breaks above 3%, medium to long term looks bearish for the US yields.

The US 10YR (2.33%) has risen as expected breaking above our expected 2.28% mentioned yesterday. It could possibly move up faster as compared to the 5Yr (1.89%) as indicated by a rising 10-5Yr differential (0.44%) which could now move up towards 0.45-0.46%.

The US-Japan 10YR (2.25%) has bounced from support levels as expected and while it continues to move up, it could pull up both Dollar Yen and Nikkei in the coming sessions. The yield spread could test 2.3% in the near term.

The German-US 10Yr (-1.76%) and the German-Us 2Yr (-2.06%) have come off sharply and are testing decent supports near current levels. If the supports hold, we could see a bounce back else we could see a fall in the next few sessions before the yield spreads pause. Euro could come off a bit, if the yield spreads continue to fall.

Sentiment Improves Ahead Of Fed Meeting

US stocks hit record highs on the back of improved earnings, which pushed the VIX down to a fresh record low yields higher upon improved risk sentiment.

The expectations of a dovish meeting also played a part as it is deemed good for stocks and bonds, sending yields higher in the process.

After extending its 13-month decline, the US Dollar Index stabilized and recouped all of Monday's losses ahead of tonight's Fed meeting. The single bullish outside day looks a little lonely right now, but perhaps if the Fed aren't as dovish as feared there is potential for a bounce. Yet even under this scenario a move higher is more likely to be down to profit taking or technical traders betting the downside is temporarily over-extended. If the Republicans pull of the seemingly impossible with health-care we can revisit the upside potential, as this paves the way for other inflationary policies. Until then, the trend points lower.

Yesterday closed with a bullish pinbar and now trades above the monthly S2, making 93.64-93.92 a viable support zone. As the monthly S1 is at 94.78 and coincides with the 10-day MA, this is the lower bound of a resistance zone which takes us the 95.16 high. As sentiment and trend point lower, we suspect any rally up towards this zone may be tempting for bears to fade into for a run down to 93. As momentum from the monthly pivot has been increasingly bearish we expect a shallow pullback from here, unless the Fed manage to surprise markets (unlikely) or Whitehouse tremors subside.

December remains the most probable window for the next hike, according to CME's FedWatch tool. Yet at a 49.1% probability, traders remain unconvinced of this likelihood, and even then they're spreading their bets by pricing in a 47.9% to 49.1%. from the December through to the May 2018 meeting. Between now and November, traders see rates on hold as being a 89.8% probability which is as good as saying no chance at all until December.

Traders are keeping a keen eye on Australia's inflation data and speech by the RBA governor later today. Given that inflation is showing signs of picking up and AUD is moving higher against RBA's wishes, we could see another verbal intervention by Philip Lowe. Currently in a holding pattern below 80c, the weaker USD is propping AUD up despite Debelle's best efforts to lower the currency on Friday. Although in all the time the US Dollar Index points lower and AU economic data outperforms the US, verbal interventions may have limited impact and a break above 80c is imminent.

EUR/CHF Another Breakout Attempt

Price rallied aggressively and erased the last day’s losses, looks motivated to take out some important resistance level, signaling that the rate will increase further in the upcoming period.

Is pressuring the median line (ml) of the minor ascending pitchfork after the impressive breakout above the upper median line (UML) of the major ascending pitchfork. Right now is trying to take out the 1.1087 resistance (previous high). Sould increase further if will stabilize above the UML, even if will stay below the median line (ml) of the minor ascending pitchfork, another drop will come only if will fail once again to stay above the UML.

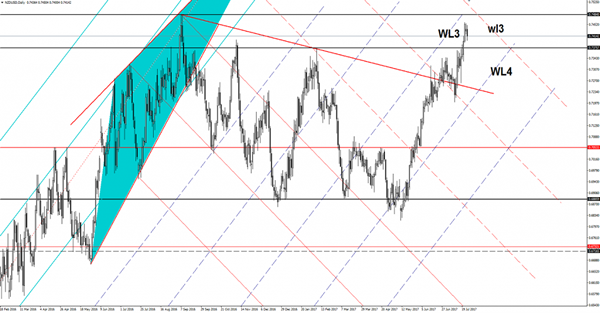

NZD/USD Is The Upside Movement Completed?

Price dropped significantly today and touched the 0.7400 psychological level, the retreat is natural after the impressive rally, could come down to test and retest a static support in the upcoming days.

Could approach and reach the 0.7375 static support (resistance turned into support) after the failure to reach the third warning line (wl3) and the WL3 of the former ascending pitchfork. We may have a buying opportunity if the rate will consolidate above the mentioned static obstacle, but only if will take out the wl3 resistance.

A breakdown below the 0.7375 level will confirm a drop towards the fourth warning line (WL4), which represents a critical support.

AUD/USD Accumulation Or Distribution?

Price moves in range on the short term and awaits for the Australian economic figures to bring some action. Technically, has shown some exhaustion signs, but is premature to say that we'll have another leg lower in the upcoming period.

Is trading near the 0.7937 level, below the 0.7940 yesterday's low, remains to see how will react after the Australian data will come out. A disappointment will send the rate tumbling on the short term, but we have to wait for a confirmation.

The Australian CPI could increase by 0.4% in Q2, less versus the 0.5% growth in the former reading period, while the Trimmed Mean CPI could increase by 0.5%.

AUD/USD moves sideways on the short term, but maintains a bullish perspective as long as is trading above the upper median line (uml) of the minor ascending pitchfork. Remains to see what will happen in the morning because the fundamental factors are expected to take the lead again and to drive the rate, remains to see the direction.

Is trapped between the 0.7989 and the 0.7874 levels, only a breakout from this range will bring a clear direction.

Looks a little exhausted after the failure to reach and retest the warning line (wl1) and the 0.7989 major static resistance, but a selling opportunity could occur only if we'll have a valid breakdown below the median line (ml).

EUR/USD Touches To The Pip And Immediately Rejects Off Resistance From 2015

Back today with a follow up to Monday's EUR/USD already reaches top of daily range blog.

Take this little extract:

…to now sit just 30 pips away from the daily range top.

Well, it looks like those 30 pips made all the difference in the end:

EUR/USD Hourly:

As you can see on the EUR/USD hourly chart above, price couldn't help itself and ripped that extra 30 pips to touch daily resistance TO THE PIP.

Yes, this is a daily resistance level drawn from the exact point that price rejected off two years ago.

Come on, tell me that's not pretty cool!

If you now believe that this touch and rejection is confirmation of sellers, you can really start to look for short term strength to possibly sell into.

The Global Petrie Dish

The rising tide of global growth is lifting all boats but there are lessons in how some are recovering better than others. The Aussie is the strongest, while the JPY is the weakest as equity indices enter an obligatory corrective rally ahead of the Fed. Month-to-date, all currencies are up against the dollar, with the loonie on top and GBP at the bottom. The Premium Insights will issue a trade tomorrow ahead of the Fed decision

In the pre-crisis era there was an economic orthodoxy that virtually every country followed. That order has broken down in the past decade and led to a series of economic experiments and now we're beginning to see the results.

The big surprise of 2017 has been Canada...as it was the surprising outperformer of 2016. The IMF said on Monday Canada will lead G7 countries in growth and that's with commodity prices halved from two years ago. Economists still don't quite believe in how strongly it's grown.

A pessimist would say that unsustainable asset price rises – housing in this case – have juiced consumer spending. A more favourable judgement would be that stimulative government policies boosted growth.

The UK could have been in the same position as Canada but fiscal tightening and Brexit uncertainty undercut some of the growth potential. It's a similar story in Europe where fiscal discipline and pockets of tight bank lending have held back the recovery.

In the US, Washington is incapable of consensus and the gridlock continues but there is always the belief that politicians there will do the right thing…once all the other options have been exhausted.

The two biggest losers in Monday's IMF update were the US and UK. The commonality there is political uncertainty.

The lesson so far this year is that it's tough to pick the winners and losers because it's such a fine line. In generations past, one country would be growing 4% and another 1%. Now, the difference in forecasts between the top G7 country (Canada 2.5%) and laggard (Japan 1.3%) is small but still has big implications in FX.

We could see just how big those implications are if Japan ever turns the corner. The minutes of the June BOJ meeting showed the board has no plans of exiting policy any time soon as long as CPI does not reach 2% despite tightening labour markets.

Something In The Air

Something in the Air

A risk on session overnight ahead of tonight s FOMC meeting as WTI bounced higher sparked by Saudi Arabia pledging to cut oil exports further while an array of encouraging earnings reports and better-than-expected economic data has lifted equity markets and bond yields overnight

And indeed headlines that the Republican Senate had enough votes to open the health care vote has rekindled some optimism for the greenback

But the waves of bond selling across fixed income which saw the US 10 Year touch 2.34% suggesting the market, or at least some, are having a look see at the reflation trade again has tongues wagging this morning

On currency markets, all eyes are on the FOMC meeting, but dealers will be occupied with the month end rebalancing act. As for the FOMC, while we can never really tell what they have up their sleeve. Latest chatter suggests the may tip their hat to September the starting date for reducing the balance sheet. However, on the inflation front, the real question is how to spin doctor four consecutive misses on CPI. The September date has been communicated already so the Greenback should not get much of a rise from that but it will be the inflation language where a possible dovish skew will emerge

While it has not set off any alarm bells yet, Yellen has voiced concerns over “ somewhat rich” asset prices. Given that overarching asset prices could harbinger a degree of financial instability into the calculus, it could also strengthen the argument to keep tightening policy. If the FOMC drives this home tonight, we could see some interesting price action.

EURO

Some unusual price action over night saw the EURO initially rallied to 1.1712 but fell after the USD sprang back to life after US bond yields took off. Some interesting battle lines getting drawn on both fixed income and USD currencies markets and we may see the eventual winner play out in the EURUSD trade.

Japanese Yen

Buoyant risk appetite and rising ten-year bond yields have us within shooting distance of the physiological 112 level. Not much to say here as the 10 Year US bond yield correlation to USDJPY holds true once again

Australian Dollar

Commodity currencies continue to trade buoyant in a weak dollar/low vol market, but some dents in the armour forming as the USD was showing some vitality overnight. With the domestic CPI and Governor Lowe taking to the airwaves via a speech at the Anika Foundation Luncheon later this morning, the market will remain on hold.But given the surging Aussie dollar complicates the post mining boom economic rebalancing act, one could only expect Governor Lowe to lean against the current market view