Sample Category Title

USD/CAD Downside Paused, Gold Buying Opportunity, AUD/USD Dropped as Expected

USD/CAD downside paused

Price changed little today and awaits the Canadian data to bring life again, we may have some action in the upcoming hours as the fundamental factors will take the lead again. Maintains a bearish perspective on the Daily Chart, will drop much below the 1.2540 previous low if the Canadian data will come in better than expected.

You should be careful in the afternoon because we may have a high volatility if we'll economic data will produce a big surprise, will be better to keep an eye on the economic calendar to see what will move price till the end of the day.

Canada is to release the inflation and the retail sales reports, the CPI could decrease by 0.1% in June, could drop in the negative territory after 6-months, the Core CPI will be released as well by Statistics Canada. The Retail Sales could increase by 0.3% in May, less versus the 0.8% growth in the previous reporting period, while the Core Retail Sales could increase only by 0.0% in May, less versus the 1.5% in the former reading period.

Price stays above the 1.2540 yesterday's low, could drop much below this level if the Canadian data will come in better, only a huge disappointment will send the rate higher. The sentiment is bearish as long as is trading within the descending pitchfork's body.

The next major downside target will be at the 1.2460 swing low, could rebound from there if the USDX will found strong support as well. Could found support also at the fourth warning line (wl4) of the former minor ascending pitchfork. Will start another leg higher only after a minor accumulation, needs to recapture more directional energy before will jump much higher. A failure to reach the 1.2460 and the lower median line (lml) will signal an oversold and a potential rebound.

Gold buying opportunity

The yellow metal resumes the minor rebound, has managed to climb above two significant resistance level and is trying to take out another in the upcoming hours. Will climb much above the 1250 psychological level if the USDX will drop much deeper.

Continues to move sideways on the Daily chart, has broken above the upper median line (UML) of the major descending pitchfork and above the upper median line (uml) of the minor descending pitchfork and now is pressuring the 38.2% retracement level. A valid breakout above the UML and above the upper median line (uml) will favor an increase towards the major 38.2% retracement level.

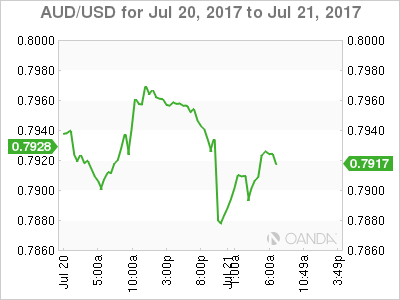

AUD/USD dropped as expected

AUD/USD decreased today, this was natural after the impressive rally, but the correction could be only temporary because the USDX could slide further. Has dropped after the fasle breakout above the warning line (wl1) of the minor ascending pitchfork, now has support again at the upper median line (uml), the perspective remains bullish as long as stays above this level.

Technical Outlook: WTI Crude oil – Risk Of Pullback Increases

WTI Oil is holding within narrow range around $47.00 handle on Friday, following previous day's spike to $47.72, the highest since 07 June.

Oil price failed to clearly break above key barrier at $47.30 (04 July former high) and ended Wednesday's trading in red candle with long upper wick which could be seen as initial signal of stall of recovery rally from $43.63 (10 July low).

Thickening and descending daily cloud continues to weighs on near-term action, along with bearish divergence on daily slow stochastic.

Initial support at $46.66 is provided by 55SMA, with break here needed to generate bearish signal for deeper pullback. Pivotal support lies at $45.80 (18 July trough, reinforced by rising 20SMA) break of which will be bearish.

On the other side, inverted H&S pattern that was completed on 4-hr chart, continues to underpin for renewed attempts through daily cloud base ($47.20) for retest of Wednesday's high at $47.72 and possible extension towards $48.18 (Fibo 61.8% of $51.98/$42.04) in extension.

Scenario will be valid while the price holds above $46.66 support.

Res: 47.19, 17.30, 47.72, 48.18

Sup: 46.66, 46.13, 45.80, 44.97

RBA Clears Up Misunderstanding

Friday July 21: Five things the markets are talking about

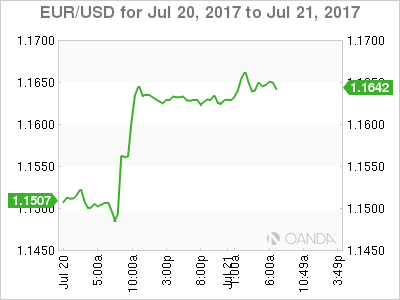

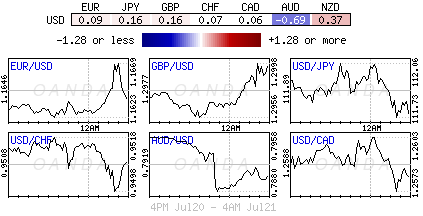

The EUR's has surged to a new two-year high outright earlier this morning (€1.1679) while most major stock exchanges consolidated as the markets assess an investigation into the U.S. president that may stall his economic agenda – special counsel Mueller is reportedly expanding his Russia probe into Trump's business transactions, as well as the financial dealings of his associates.

Yesterday's meeting of the ECB did just enough to show that regional policymakers seem to be on course to rein in their two-year old emergency program of QA without upsetting the ‘apple cart.' As expected, the ECB left rates unchanged and their lack of concern on a stronger EUR was enough to give the green light to investors to own even more.

President Draghi is now expected to use the Jackson Hole Federal Reserve conference in August (24-26) to prepare the ground for a bond-buying program tapering announcement in September.

This morning, Canada is expected to report a soft +1.1% rise in y-o-y inflation at 08:30 am EDT, while retail sales should come in at a +0.3% monthly gain.

1. Stocks finish on a flattish note

Following the flattish session in the U.S yesterday, most of the equity markets in Asia and Europe are slightly weaker overnight.

Global equities have continued hitting new fresh highs week amid corporate results that have reinforced faith in earnings and the economy. Asian shares are up more than +4% in the past fortnight, with markets in Japan and Hong Kong near two-year highs.

In Japan, the Nikkei share average retreated overnight as investors took profits on steelmakers and a firmer yen (¥111.68) also soured investors' mood. For the week, the benchmark index dipped -0.1%. The broader Topix dropped -0.2%.

In Hong Kong, shares ended their nine-day winning streak, pulling back from their two-year highs. The Hang Seng index shed -0.1%, ending its longest streak of gains since April 2015. However, it rose +1.3% this week, its second week in the black. The Hang Seng China Enterprises Index was -0.6% lower.

In China, stocks slipped, but ended the week higher, led by strong gains in blue chips. The CSI300 index fell -0.3%, retreating from its 18-month high, while the Shanghai Composite Index lost -0.2%.

In Europe, equities trade are mixed in a lackluster session. The FTSE 100 is a tad higher with help from the telecommunications sector's higher Q1 results.

U.S stocks are set to open in the black (+0.1%).

Indices: Stoxx600 +0.1% at 384, FTSE 0.3% at 7511, DAX +0.1% at 12457, CAC-40 +0.2% at 5208, IBEX-35 -0.1% at 10556, FTSE MIB flat at 21441, SMI +0.2% at 9046, S&P 500 Futures +0.1%

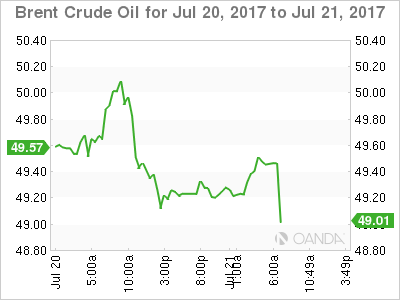

2. Oil nudges higher ahead of OPEC meeting, gold shine's

Ahead of the U.S open, oil prices have pushed higher ahead of a key meeting of major oil producing nations next week.

However, Brent crude is holding below the psychological +$50 per barrel level that was briefly breached yesterday for the first time in six-weeks.

Brent crude futures are up +10c, or +0.2%, at +$49.40 per barrel, while U.S West Texas Intermediate (WTI) crude futures are up +7c, or +0.2% at +$46.99 per barrel.

Note: Both benchmarks hit their highest levels yesterday, having been pushed higher by data showing U.S crude and fuel inventories fell sharply last week.

A global glut is putting pressure on oil prices and key members of OPEC are scheduled to meet non-members in St. Petersburg, Russia, on Monday (July 24) to discuss market conditions and whether more action is needed to support prices.

The ‘bears' don't believe there will be any action from Monday's OPEC/non-OPEC working committee meeting – It's OPEC itself that needs to take further steps to being inventories back to quasi-normal levels.

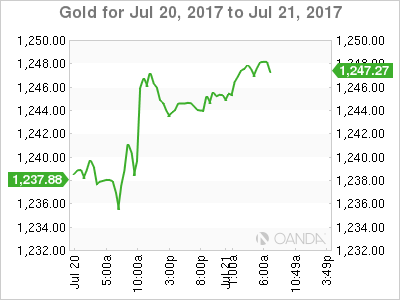

Gold hit a three-week high this morning and is on track for a second consecutive weekly gain as the dollar tumbled to a 13-month low. Spot gold is up +0.2% at +$1,247.17 per ounce, after hitting its highest since June 29 at +$1,248.30. It has gained about +1.5% so far this week.

3. Yields fall on ECB's dovish comments

The ECB continues to struggle to push up inflation to its desired target, making it difficult for policy makers to dial back monetary stimulus even as the global economy has been showing broad improvement. Draghi's ‘dovish' remarks yesterday gave the green light to own more sovereign debt.

Fixed income buying sent the yield on the benchmark 10-year Treasury note to as low as +2.239% intraday, before settling at +2.25%, its lowest level since June 28. German Bunds fell -3 bps to +0.52%, while U.K Gilts eased -1 bps to+1.19%.

Down-under, comments from Reserve Bank of Australia (RBA) Deputy Governor Debelle stating that the central bank was far from tightening its policy (differs from recent minutes) had yields under pressure. Aussie 10-year yield fell -4 bps to +2.70%, while the three-year yield fell -7 bps to +2.02%.

In Canada, bonds are likely to be more reactive to today's release of CPI and retail sales figures given the Bank of Canada (BoC) recent emphasis on economic data.

4. Dollar under pressure from all sides

The EUR (€1.1645) continues where it left off yesterday, trading atop its two-year high outright and eight-month high against sterling (€0.8973). In yesterday's ECB's press conference, Draghi failed to communicate any unwanted deflationary implications of EUR strength. Also providing support is the markets fixation that the ECB will announce its plan to taper or recalibrate its stimulus at the September 7 meet.

The ‘big' dollar is broadly weaker versus G20 pairs on concerns about the U.S Trump administration, while the pound (£1.2995) is struggling on worries about lack of progress in Brexit talks.

Elsewhere, the AUD at one point tumbled -0.7% overnight to A$0.7880 after RBA commented on 'neutral' interest rate (see below).

5. Comments from the Reserve Bank of Australia (RBA) Deputy Governor

Overnight, RBA Deputy Governor Debelle has cleared up any confusion around the central bank's communication this week.

The AUD had surged after the release of the July minutes on Tuesday – the publication of the RBA's thinking on the 'neutral' cash rate suggested, to some, that Aussie policy makers thought that the current level of official interest rates were too low, and needed to rise soon.

Debelle insisted that that there was 'no' significance to the discussion contained in the RBA's minutes. The discussion was merely procedural. He also said there is nothing compelling the RBA to follow other central banks in hiking interest rates. The RBA makes policy based on domestic fundamentals.

Net result, the RBA seemingly regrets making that discussion public and is a strong sign that it was unhappy with the tightening in financial conditions.

Note: Governor Philip Lowe is due to speak next week.

GOLD Bullish Momentum Continues, SILVER Bullish, CRUDE OIL Strong Upside Pressures.

GOLD Bullish momentum continues.

Gold's is trading higher after the precious metal reached the support given at 1204 10/07/2017 high). Hourly resistance lies at 1258 (23/06/2017 high). Expected to show further strengthening.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low)

SILVER Bullish.

Silver is pushing higher after the bounce still bouncing from hourly support given at 15.18 (10/07/2017 low). Key resistance is given at a distance at 17.75 (06/06/2017 high). The commodity has broken the 16-mark. Expected to inch higher.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

CRUDE OIL Strong upside pressures.

Crude Oil is trading higher. Hourly support is given at 43.65 (10/07/2017 low). Expected to monitor resistance given at 48.42 (05/06/2017).

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

DAX Steady As Investors Look For Cues

The DAX index has posted small gains in the Friday session. Currently, the DAX is trading at 12,454.20, up 0.22% on the day. It's a quiet end to the week, with no German or eurozone releases. On Thursday, the ECB made no changes to interest rates or its quantitative easing (QE) program.

It's been smooth sailing for the German economy in 2017, and the locomotive of Europe has led the way for a stronger eurozone economy, as growth has improved and unemployment has dropped. The German export sector has been boosted by stronger global demand, and domestic spending remains solid. Fears of an economic slowdown due to Britain's departure from the EU and US President Trump's protectionist stance have not materialized. The German Finance Ministry was positively upbeat on Thursday, saying that “the current picture of economic indicators suggests that the economic upswing continued vigorously in the second quarter”. GDP expanded at a strong clip of 0.6% in the first quarter, and Q2 is expected to post another gain of 0.6%. The economy received a thumbs-up from the IMF, which has raised its growth projections to 1.8% in 2017 and 1.6% in 2018. If the ECB tapers its asset purchase program in September, as many analysts expect, German economic growth could be even higher in the second half of the year. The fly in the ointment has been inflation, as both Germany and the eurozone continue to struggle with inflation levels well below the ECB's inflation target of 2%. German policymakers have long argued that the German economy needs higher interest rates. However, the ECB has to look after eurozone members who are not doing as well as Germany, and has insisted that it will not withdraw stimulus until inflation in the eurozone moves closer to the bank's inflation target.

The ECB didn't make any moves at its policy meeting, but that didn't stop the euro from posting strong gains on Thursday. EUR/USD has gained 1.6% this week, and earlier on Friday, the pair hit its highest level since August 2015. As expected, the ECB opted to hold steady with its monetary policy, keeping interest rates at 0.00% and the QE scheme at EUR 60 billion/month. The QE program is scheduled to end in December, and any change to that date could have a significant impact on the euro. At his press conference, ECB President Mario Draghi sounded upbeat about the eurozone economy, noting there were signs of “unquestionable improvement” in the eurozone economy. As for monetary policy, Draghi said the bank had not set an exact time for revisiting any changes to the current accommodative policy, but added that policymakers would review policy in September. These comments did not seem to break any new ground, but were perceived as hawkish by the markets and triggered a euro rally.

With Mario Draghi saying that the ECB will revisit its ultra-loose monetary policy in September (and the euro jumping higher as a result), what moves can we expect from the bank in September? As OANDA Senior Currency Analyst Craig Erlam explains, the markets should be prepared for some significant moves at the September policy meeting:

The most likely decision, despite the central bank still falling well short of its inflation target, will be to cut its purchases by another €20 billion as it did in April and extend by another six months. There has been a lot of speculation about a more explicit phasing out but I think the ECB want to be more careful given the fragile nature of the recovery. The result will likely be the same though with the central bank ending its quantitative easing program either at the end of 2018 or early 2019.

EUR/GBP Surging, EUR/CHF Pushing Higher, BITCOIN Surging.

EUR/GBP Surging.

EUR/GBP is very volatile. The pair has surged toward 0.9000. Hourly resistance is given at a distance at 0.8742 (16/07/2017 low). Downside risks are important.

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.

EUR/CHF Pushing higher.

EUR/CHF is still trading above psychological level at 1.1000 and the pair is approaching 1.1100. Selling pressures are growing at the moment. Hourly support is located at a distance at 1.0922 (30/06/2017 low). Expected to inch higher.

In the longer term, the technical structure is mixed. Resistance can be found at 1.1200 (04/02/2015 high). Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

BITCOIN Surging.

Bitcoin has well recovered after the sell-off this weekend. Hourly resistance can be found at 2417 (13/07/2017 high) has been exploded and hourly support looks very far at 1852 (14/07/2017 low). Expected to show some further retracement. Still good to enter buying orders below 2000.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will consolidate above $1500. Long-term support is given at $1464 (04/05/2017 low).

Market Update – European Session: EUR/USD Near 2-Year Highs Aided By Broad USD Weakness

Notes/Observations

EUR/USD near 2-year highs aided by broad USD weakness

Overnight

Asia:

RBA Dep Gov Debelle: Discussion of neutral rates had no implications for policy. Reiterated RBA view that a rising A$ was not welcomed and complicated the economy's adjustment

New Zealand Fin Min Joyce: 'Unperturbed' by NZD strength, kiwi dollar strength reflects strong economy

Europe:

ECB tapering decision reportedly may not be made until Oct

UK govt reportedly to offer EU citizens free movement for up to 2 years under plans devised by Chancellor Hammond

IMF confirmed approval of $1.8B conditional loan for Greece (as expected) but would not disburse any bailout until Europe details their debt relief plan

Americas:

Special counsel Mueller reportedly expanding Russia probe into Trump business transactions, as well as financial dealings of Trump associates

President Trump said to have made changes to legal team

Economic Data

(JP) Japan Jun Nationwide Dept Sales Y/Y: 1.4% v 0.0% prior; Tokyo Dept Store Sales Y/Y: +1.1% v -1.1% prior

(NL) Netherlands Jun House Price Index M/M: 0.7 v 0.8% prior; Y/Y: 8.0 v 7.8% prior

(UK) Jun Public Finances (PSNCR): £18.3B v £13.4B prior; Public Sector Net Borrowing: £6.3B v £4.2Be , Central Government NCR: 17.8B v £9.8B prior, PSNB ex Banking Groups: £6.9B v £4.9Be

Fixed Income Issuance:

(IN) India sold total INR150B in 2022, 2029, 2033 and 2051 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.1% at 384, FTSE 0.3% at 7511, DAX +0.1% at 12457, CAC-40 +0.2% at 5208, IBEX-35 -0.1% at 10556, FTSE MIB flat at 21441, SMI +0.2% at 9046, S&P 500 Futures +0.1%]

Market Focal Points/Key Themes: European Equities trade slightly higher across the board in a releatively lackluster session. The FTSE 100 outperforms with help from Vodafone which trades higher after Q1 results. Elsewhere Philips lighting, Accel Holdings and Sartorius Stedim trade sharply lower following results. In the M&A space Paysafe trade higher after confirming a bid

Equities

Consumer discretionary [Accel [ACCEL.NL] -7.5% (Earnings)]

Industrials: [Valeo [FR.FR] -4.0% (Earnings), Philips Lighting [LIGHT.NL] -7.5% (Earnings)]

Financials: [Paysafe [PAYS.UK] +7.5% (Receives take over approach)]

Technology: [Landis & Gyr [LAND.CH] +1.0% (IPO), Fingerprint Cards [FINGB.SE] +10% (Earnings)]

Telecom: [Vodafone [VOD.UK] +1.6% (Q1 Earnings)]

Healthcare: [Sartorius Stedim [DIM.FR] -7.6% (Earnings), Ypsomed [YPSN.CH] -23% (Ends distribution agreement with Insulet Corp)]

Speakers

ECB Survey of Professional Forecasters (SPF) cut its inflation outlook for the 2017-19 period and bumped up its growth forecasts (**Note: moves in-line with the most recent Staff Projections).

Turkey Econ Min Zeybekci reiterated govt view that interest rates were higher than they should be

South Korea govt said to discuss issues on possible tax hike in 2018

Currencies

EUR/USD probed near 2-year highs early in the session. EUR/USD tested 1.1677 for its highest level since August 2015. Dealers noted that the spike up in the Euro during the press conference was likely related to Draghi ducking the question about the recent EUR currency strength. Draghi failed to communicate any unwanted deflationary implications of EUR strength. Also providing a catalyst was expectations that the ECB announcement on plan to taper its stimulus will occur in September.

AUD currency was weaker after RBA Dep Gov Debelle noted that the central bank far from tightening its policy (differs from recent minutes)

Fixed Income

Bund futures trade at 162.38 up 41 ticks after dovish ECB survey. Resistance lies near the 162.10 level followed by 162.75. A break of the 160.00 support level could see lows target 159.25 followed by 157.50.

Gilt futures trade at 126.29 higher by 1 tick after being capped by key resistance from the 126.51 level. Price finds key support at the 125.42 support level. An acceleration lower could test the 122.88 region. Resistance remains the noted 126.51 region, followed by 127.50.

Friday's liquidity report showed Thursday's excess liquidity fell to €1.640T a drop of €7B from €1.647T prior. Use of the marginal lending facility rose to €280M from €272M prior.

Corporate issuance saw $3.2B come to market via 2 issuers headlined by Canadian Imperial Bank $1.75B covered bond offering and Church & Dwight $1.425B 4-part senior unsecured note offering. This week's issuance is at $46.9B. For the week ending July 19th Lipper US fund flows reported IG funds net inflows $3.8B bringing YTD inflows to $75.2B, High yield funds reported outflows of $2.2B bringing YTD outflows to $6.6B.

Looking Ahead

(UR) Ukraine Jun Industrial Production M/M: No est v 3.4% prior; Y/Y: No est v 1.2% prior

06:00 (IE) Ireland Jun PPI M/M: No est v -0.8% prior; Y/Y: No est v 1.1% prior

06:00 (UK) DMO to sell combined £3.5B in 1-month, 3-month and 6-month bills (£0.5B, £1.0B and £2.0B respectively)

06:45 (US) Daily Libor Fixing

07:30 (IN) India Weekly Forex Reserves

08:00 (PL) Poland Jun M3 Money Supply M/M: 0.6%e v 0.5% prior; Y/Y: 5.9%e v 6.2% prior

08:15 (UK) Baltic Dry Bulk Index

08:30 (CA) Canada Jun CPI M/M: -0.1%e v +0.1% prior; Y/Y: 1.1%e v 1.3% prior

08:30 (CA) Canada Jun CPI Core- Common Y/Y: 1.3%e v 1.3% prior, CPI Core- Trim Y/Y: No est v 1.2% prior, CPI Core- Median Y/Y: No est v 1.5% prior, Consumer Price Index: No est v 130.5 prior

08:30 (CA) Canada May Retail Sales M/M: 0.3%e v 0.8% prior; Retail Sales Ex Auto M/M: 0.0%e v 1.5% prior

09:00 (MX) Mexico Jun Unemployment Rate (Seasonally Adj): 3.5%e v 3.5% prior; Unemployment Rate (Unadj): 3.5%e v 3.6% prior

09:30 (BR) Brazil Jun Current Account: $1.4Be v $2.9B prior; Foreign Direct Investment (FDI): $2.5Be v $2.9B prior

11:00 (EU) Potential sovereign ratings after European close

13:00 (US) Weekly Baker Hughes Rig Count Data

15:00 (CO) Colombia May Economic Activity Index (Monthly GDP) Y/Y: 1.4%e v 1.4% prior

USD/CHF Weakening Again, USD/CAD Strong Weakness, AUD/USD Profit-Taking.

USD/CHF Weakening again.

USD/CHF is pushing lower. Hourly resistance can be found at 0.9696 (09/06/2017 high). Strong resistance is given at 1.0107 (10/04/2017 high). Expected to to show further weakness.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/CAD Strong weakness.

USD/CAD is going lower and the pair remains in a strong bearish momentum. Hourly support is given at 1.2541 (20/07/2017 low). Hourly resistance is given at 1.2701 (17/07/2017). Expected to show continued bearish pressures.

In the longer term, the pair lies in a bullish channel since a year. Strong resistance is given at 1.4690 (22/01/2016 high). Long-term support can be found at 1.2461 (16/03/2015 low)

AUD/USD Profit-taking.

AUD/USD's technical structure is bullish since early May despite some profit-taking. Hourly resistance is given at 0.7989 (19/07/2017 high). Hourly support is given at 0.7875 (21/07/2017 low).

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.

XAU/USD Analysis: Near 1,250 Mark

The yellow metal continues to surprise the bulls. The commodity price was reaching for the 1,250 mark on Friday morning. It was initially expected on Thursday that the metal will decline down to the lower trend line of a medium ascending channel pattern. However, as the metal fluctuated between the 100 and 55-hour SMAs, a fundamental event took place, which influenced the price of gold. As the ECB press conference took place, the massive buying of the Euro and simultaneous selling of the US Dollar caused a spill over. That resulted into the metal breaking the resistance of the 55-hour SMA. Due to that it can be observed on Friday morning that the bullion is most likely going to reach above the 1,250 levels on Friday, as there are no notable strong resistance levels, which might stop it.

USD/JPY Analysis: Fails To Bypass 100-Hour SMA

Contrary to expectations, an impulse given by an exit from a rising wedge pattern was not strong enough to push the currency pair to a closest combined resistance level formed by the 200-hour SMA and the weekly PP at 113.09. Namely, the currency pair soared to the 100-hour SMA near 112.30 but then rapidly fell back to the weekly S1 at 111.70. The new attempt to recover the lost ground failed as well, as the pair encountered a combination of the 20- and 55-hour SMA near 111.97. An early Friday morning shows that the above weekly S1 still does not let the rate to fall further and pushes it to make another attempt to climb upstairs. But in case of a third failure, the freefall of the rate should be stopped by the monthly PP 111.38.