Sample Category Title

USDJPY – Weakens Further With Eyes On 111.00 Zone

USDJPY - The pair continues to hold on to its downside pressure closing lower on Wednesday and opening the door for more declines. On the downside, support comes in at the 111.50 level where a break if seen will aim at the 111.00 level. A cut through here will turn focus to the 110.50 level and possibly lower towards the 110.00 level. On the upside, resistance resides at the 112.50 level. Further out, we envisage a possible move towards the 112.00 level. Further out, resistance resides at the 111.50 level with a turn above here aiming at the 111.00 level. On the whole, USDJPY looks to pullback further in the days ahead.

Event Risk Overload

Event risk overload

There hasn't been much progress in the currency markets overnight as both US yield, and the US dollar continues to struggle. And for the time being, equity markets continue to be cheered by improving earnings.

Dealers remain in cautionary wait and see mode ahead today's high-risk events that lay in waiting.The focus today should be on the ECB, BoJ and Australian Employment data.It's been somewhat directionless trading as both USDJPY and EURUSD moderated on the back of profit-taking while AUDUSD carries on higher into the local jobs data.

But President Trump's Administration is worth keeping an eye on as the political quagmire thickens

Australian Dollar

Still waiting for the dust to settle on this trade as the Aussie is holding firm above 0.7950 after breaching the top of the two-year range earlier in the week There been very little retracement as dealers position to continued improvements in the domestic labour market.

AS we approach the A$ 80 level, it suggests we're beyond the fear of missing out on a policy shift trade. And while we can argue till blue in the face this move is overdone the reality is the Aussie is in demand.

Equity markets are getting cheered on from every level, and the steady beat of the Chinese economy has seen Iron ore prices rising.Also, the rally in WTI spurred on by a larger than expected drop in crude oil inventories is helping sentiment across the commodity block this morning and with implied volatility dropping there definitely some yield appeal for Aussie assets.

Australian Jobs Data

The Australian Jobs data just missed estimates, but this is robust enough to push the Aussie dollar higher with the full-time employment change greater than expected. On cue, Australia 3-year yield is trading at the highest since Dec 2015, following full-time employment change

The Aussie is stalling after the initial move suggesting some initial profit taking setting. Regardless the A$ continues with its gravity defying act, and push through A$80 is likely in the cards.

Euro

Despite the mild pullback on profit taking t, which was expected ahead of today's ECB, the trend remains intact. And while there probably a greater chance the ECB will disappoint as opposed to affirm the markets hawkish conviction, but even then, the Euro should continue to be a buy on dip given the US dollar weakness, and the market is looking to September for the key policy shift.The one concern into the ECB is market positioning which needless to say is long so if there is very dovish surprise the short term longs will run for the exits, and it could get messy for a while.

Japanese Yen

The BoJ is unlikely to move markets much on Thursday although it is expected to upgrade the economic assessment more or less. Sources on Tuesday discussed the possibility of CPI estimates being reduced and while unlikely it's still a risk

The USDJPY is more about the crowded EURJPY positioning, so a move lower in EUR on the ECB could see a sudden unwind of EURJPY and drive the USDJPY lower.

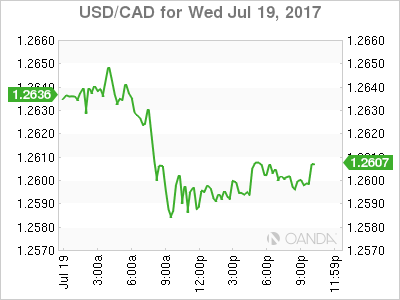

USD/CAD Canadian Dollar Rises After Oil Price Bounce

The Canadian dollar appreciated on Wednesday versus the US dollar. The Canadian currency got a boost from strong manufacturing sales, oil prices gaining on larger than expected drawdowns in the US and the cloud of uncertainty surrounding the healthcare Act in Washington.

US Trade Representative Robert Lighthizer has announced the NAFTA renegotiation talks will begin on August 16 to 20 in Washington. Both Canada and Mexico issued positive statements on the plans and look forward to modernizing the agreement. Presidential elections in Mexico and the US midterm elections in 2018 are incentives for the negotiations to take place as soon as possible and with a speedy outcome.

The USD/CAD lost 0.207 in the last 24 hours. The loonie rose against the US dollar as oil prices rose with a bigger than expected drawdown in the US and the continuing saga of political uncertainty surrounding healthcare reform in Washington. The currency pair is trading at 1.2594 breaking below the 1.26 with the help of oil prices.

Canadian manufacturing sales rose 1.1 percent in May. Auto sales drove the record high sales beating expectations of 0.8 percent increase. The Canadian economy is keeping pace with growth expectations that lead the Bank of Canada (BoC) to raise its benchmark interest rate for the first time in 7 years. The benchmark was hiked 25 basis points to 0.75 percent with another rate raise expected for later this year if growth marches on. Canadian retail sales and inflation data due this Friday will add more arguments for monetary policy.

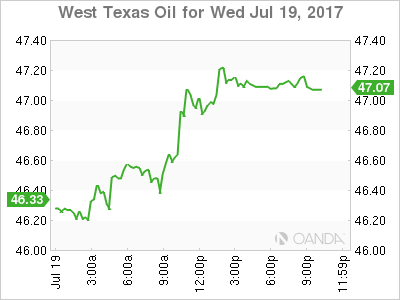

Energy prices surged 2.146 percent on Wednesday. The price of West Texas Intermediate is trading at $47.22 after the release of the Energy Information Administration (EIA) weekly US crude inventories showed a larger drawdown than he market expected. Crude stocks fell by 4.7 million barrels last week, the third time in as many weeks that drops in inventory are higher than forecasted. Gasoline and distillate inventories also had losses bigger than anticipated pushing the price of energy higher.

US production has increased which makes the shrinking inventories more puzzling without signs of demand growth. The Organization of the Petroleum Exporting Countries (OPEC) and other major exporters agreement to cut production has stabilized prices, but American shale producers have taken advantage and ramped up their operations.

The meeting between OPEC and Russia to discuss compliance later this month will open the door for the next steps for energy producers. A bigger cut in production after the agreed extension is in the cards, but there are some voice of dissent as current levels are causing distress for countries who depend on oil sales to balance their budget.

Ecuador is the latest OPEC member to disclose a smaller than agreed to levels of production. Oil minister Carlos Perez said that there is an unwritten agreement within the OPEC to allow “flexibility” to smaller producers. Nigeria and Libya were excluded from the agreement after suffering disruptions to their productions but are now close to normal levels so there is talk that they could be brought into the fold, which could prove difficult if other nations are not holding up their production quotas.

Market events to watch this week:

Wednesday, July 19

9:30 pm AUD Employment Change

Tentative JPY Monetary Policy Statement

Thursday, July 20

Tentative JPY BOJ Outlook Report

Tentative JPY BOJ Policy Rate

2:30 am JPY BOJ Press Conference

4:30 am GBP Retail Sales m/m

7:45 am EUR Minimum Bid Rate

8:30 am EUR ECB Press Conference

8:30 am USD Unemployment Claims

Friday, July 21

8:30 am CAD CPI m/m

8:30 am CAD Core Retail Sales m/m

Will the ECB and BoJ Have Any Surprises in Store?

The last month has seen G7 central banks re-emerge as the dominant driver of financial market volatility with policy makers becoming increasingly uncomfortable with the direction of travel, at least in most cases.

All of a sudden the Federal Reserve appears to be questioning the need to raise interest rates so quickly, the Bank of England is considering tightening as it's more worried about inflation than the economy and the Bank of Canada has already raised interest rates despite falling well short of its inflation target.

Two central banks that have so far continued to operate with some predictability are the ECB and the Bank of Japan, both of which are due to announce their latest monetary policy decisions on Thursday. Can we still rely on them not to have the sudden change of heart that their peers have had?

BoJ Refusing to Fall in Line With Other Central Banks

Given the shift that we've seen in recent weeks, it's difficult to say with any degree of certainty but of all the above, I think the BoJ and ECB may be the two that will follow a more predictable path (famous last words).

The BoJ has shown no desire to deviate from its ultra-accommodative stance, in fact it recently increased its bond purchases because the yield on 10-year JGBs was ticking higher, driven by similar moves elsewhere. With the central bank vowing to keep the 10-year yield around 0%, the move was a signal to markets that it is not in the same camp as a number of its peers. With that in mind and considering inflation remains far from target, I don't expect any sudden shifts on Thursday.

Source - Thomson Reuters Eikon

The ECB could be more interesting though, with the asset purchase program in its current form - €60 billion per month - due to expire at the end of the year. While the central bank will likely wait until September to announce how the program will be extended, it may use this month's press conference - being the last before September - to lay the groundwork for such an announcement.

We may therefore get some insight into what the central bank is considering doing next. For example, will it lay out plans to phase out asset purchases over a certain period of time? Or will it simply announce another short extension while reducing the size of the program, as it did in December, while insisting it is not tapering? We may get some insight into this on Thursday.

Of course, there is always the possibility that it simply extends the program as it is, although this appears the least likely option, which it may allude to.

Will Dovish Draghi Throw a Spanner in the Works?

Whatever the central bank does, these events often stir up some volatility in the markets, particularly in the euro and eurozone bonds. And in the current environment, these may be particularly vulnerable to any unexpected suggestions, intentional or otherwise.

With the euro trading near the highs of the last two and a half years against the dollar, it's potentially looking a little overstretched which could leave it vulnerable to a dovish surprise from ECB President Mario Draghi.

The flip side of this of this, of course, is that a more hawkish message could trigger a move through this major resistance which in turn could be very bullish for the pair. Clearly we're in for a very interesting end to the year for markets and the ECB could well be at the centre of it all.

Gold Pauses After Gaining on Trump Troubles

Gold is showing little movement in the Wednesday session. In the North American session, spot gold is trading at $1241.66. On the release front, Building Permits climbed to 1.25 million, beating the estimate of 1.20 million. Housing Starts improved to 1.22 million, above the forecast of 1.16 million.

US housing numbers have been mixed in recent months, but Tuesday's releases pointed to a strengthening housing sector. Building Permits improved to 1.25 million in June, up from 1.17 million a month earlier. Housing Starts jumped to 1.22 million, up sharply from 1.09 in the May report. The solid numbers will give a boost to second quarter numbers. US Advance GDP will be released next week, and the markets don't want to see a repeat of the first quarter reading, which missed expectations with a gain of just 0.7%.

Gold has been moving higher, gaining 2.1% since Friday. The metal moved higher after CPI and retail sales disappointed, and the rally has continued this week. The dollar lost ground after President Trump suffered a major defeat on Capitol Hill on Tuesday, and gold responded with gains of 0.08%. Political risk in the US has reduced investor appetite for risk and boosted gold prices.

President Trump hasn't done very well at learning how to tango with Congress, and this week's debacle on Capitol Hill could make the gap between Trump and Republican lawmakers even harder to bridge. Trump had vowed to replace Obamacare, but his health care bill has stalled in the Senate before lawmakers even had a chance to vote on the proposal. With some conservative Republicans coming out against the bill, it's questionable if the Republicans can pass another version before Congress takes a recess in August. Trump had promised to pass a health care before the summer break, so his credibility will take another hit if he's unable to do so. Trump has been in office for six months, but has been unable to get Congress to pass any significant bills, even though the Republicans enjoy a majority in both houses of Congress. With this latest setback, there is growing skepticism as to whether Trump will be able to convince Congress to pass other key parts of his agenda – tax reform and fiscal spending. This paralysis on Capitol Hill has deepened investor pessimism about Trump's legislative agenda and is weighing on the US dollar.

Lack of Data Leaves Pound Unchanged, UK Retail Sales Next

GBP/USD is subdued on Wednesday, and is unchanged on the day. In the North American session, the pair is trading at 1.3040. In economic news, there are no British events on the schedule. In the US, housing numbers were sharp, as Building Permits and Housing Starts improved in June and beat expectations. On Thursday, the UK will release retail sales, and the US will publish unemployment claims and the Philly Fed Manufacturing Index.

British CPI has been gaining strength, but the indicator slowed to 2.6% in June, down from 2.9% in May. This was considerably lower than the estimate of 2.9% and the first time in 2017 that inflation levels have not increased from the previous reading. The soft data eases the pressure on the BoE to raise rates in order to curb high inflation levels. Policymakers at the BoE have been at odds over raising rates – even though inflation is high, the economy has been showing signs of weakness, raising concerns that the economy does not need higher interest rates. On Tuesday, BoE Governor Mark Carney said that the main factor behind high inflation was the fall in the pound, which has dropped sharply since the Brexit vote in June 2016. The BoE hold its next policy meeting on August 4, and analysts expect the policymakers to hold the benchmark rate at 0.25%, where it has been pegged since August 2016.

Britain and European Union negotiators met in Brussels on Monday, marking the start of substantive negotiations on Britain's exit from the EU. After weeks of "discussions about what to discuss", the UK agreed to the European demand that the negotiations would focus on the rights of EU citizens in the UK and Britain's bill for leaving the EU, before entering talks on a new trade agreement. Britain has presented its position on guaranteed rights for EU citizens living in the UK, but EU negotiators have said that this offer doesn't go far enough. The EU has handed Britain an exit bill of EUR 69 billion, and although the May government has agreed that it owes funds to Brussels, it certainly will counter with a much lower figure. With significant gaps between the parties on both of these issues, the negotiations promise to be difficult. Another complication is internal dissent within the May government, with senior officials at odds over a 'transition period' for Britain after leaving Brexit. Finance Minister Philip Hammond has suggested a transition period of two years, but Brexit Secretary David Davis has said he wants the UK completely out of the single market when Brexit negotiations terminate in March 2019.

Yen Hits 3-Week High, BOJ Meeting Looms

The US dollar remains under pressure, as USD/JPY has posted gains for a second straight day. In Wednesday's North American session, USD/JPY is trading at 111.70, down 0.31% on the day. On the release front, there are no Japanese data releases, but the markets will be paying close attention to the BoJ rate statement. In the US, there was positive news from the housing sector. Building Permits climbed to 1.25 million, beating the estimate of 1.20 million. Housing Starts improved to 1.22 million, above the forecast of 1.16 million.

US housing numbers have been mixed in recent months, but Tuesday's releases pointed to a strengthening housing sector. Building Permits improved to 1.25 million in June, up from 1.17 million a month earlier. Housing Starts jumped to 1.22 million, up sharply from 1.09 in the May report. The solid numbers will give a boost to second quarter numbers. US Advance GDP will be released next week, and the markets don't want to see a repeat of the first quarter reading, which missed expectations with a gain of just 0.7%.

The Bank of Japan is in the spotlight, as policymakers gather for a policy meeting later on Wednesday. Unlike other central banks, such as the ECB and the Federal Reserve, there are no expectations of a tightening of monetary policy in the near future. However, investors will be looking for any tweaks to current monetary policy, which could trigger some movement from the yen. Inflation continues to hover below 1.0%, well below the BoJ's target of 2%. Most analysts expect the bank to push back the timeline for the 2% target, which is currently "around fiscal 2018", but do not anticipate the bank lowering the target. The BoJ has consistently said that it will not reduce its radical stimulus program until inflation levels move higher. Given current economic conditions, this is unlikely before 2018 at the earliest.

President Trump hasn't done very well at learning how to tango with Congress, and this week's debacle on Capitol Hill could make the gap between Trump and Republican lawmakers even harder to bridge. Trump had vowed to replace Obamacare, but his health care bill has stalled in the Senate before lawmakers even had a chance to vote on the proposal. With some conservative Republicans coming out against the bill, it's questionable if the Republicans can pass another version before Congress takes a recess in August. Trump had promised to pass a health care before the summer break, so his credibility will take another hit if he's unable to do so. Trump has been in office for six months, but has been unable to get Congress to pass any significant bills, even though the Republicans enjoy a majority in both houses of Congress. With this latest setback, there is growing skepticism as to whether Trump will be able to convince Congress to pass other key parts of his agenda – tax reform and fiscal spending. This paralysis on Capitol Hill has deepened investor pessimism about Trump's legislative agenda and is weighing on the US dollar.

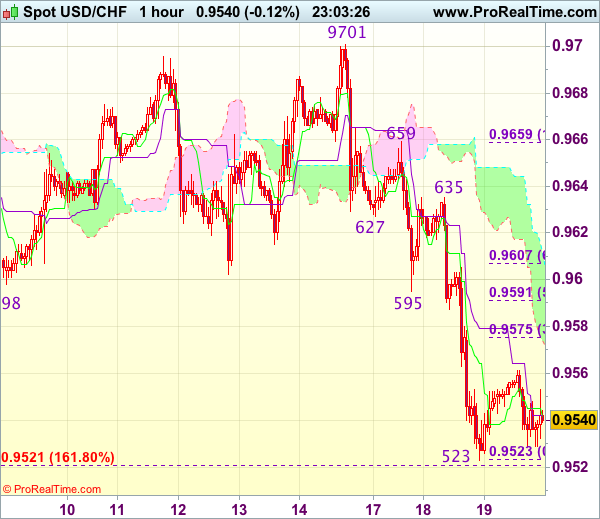

Trade Idea Wrap-up: USD/CHF – Stand aside

USD/CHF - 0.9640

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9542

Kijun-Sen level : 0.9542

Ichimoku cloud top : 0.9612

Ichimoku cloud bottom : 0.9574

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As the greenback has remained under pressure after dropping sharply from 0.9701, suggesting near term downside risk remains and below support at 0.9523 would extend recent selloff to 0.9500 and possibly towards 0.9475-80, however, loss of near term downward momentum should prevent sharp fall below latter level and reckon 0.9440-50 would hold from here, risk from there is seen for another rebound later.

In view of this, would be prudent to stand aside for now. Above 0.9575 (38.2% Fibonacci retracement of 0.9659-0.9523) would bring a stronger recovery to previous support at 0.9595 but reckon upside would be limited to 0.9605-10 (61.8% Fibonacci retracement) and resistance at 0.9635 should remain intact, bring another decline later.

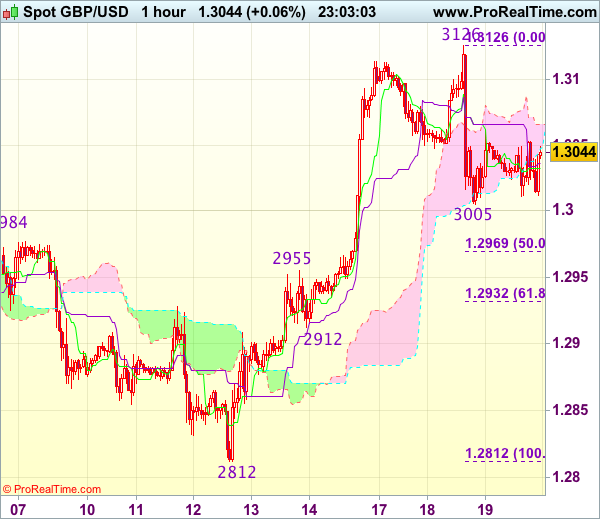

Trade Idea Wrap-up: GBP/USD – Sell at 1.3090

GBP/USD - 1.3043

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3037

Kijun-Sen level : 1.3066

Ichimoku cloud top : 1.3076

Ichimoku cloud bottom : 1.3029

Original strategy :

Sell at 1.3090, Target: 1.2990, Stop: 1.3125

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.3090, Target: 1.2990, Stop: 1.3125

Position : -

Target : -

Stop : -

Although the British pound rose briefly to 1.3126, the subsequent retreat suggests temporary top is possibly formed and consolidation below this level would be seen with mild downside bias, below support at 1.3005 would add credence to this view, bring retracement of recent upmove to 1.2965-70 (50% Fibonacci retracement of 1.2812-1.3126), then test of previous resistance at 1.2955 but reckon 1.2930-35 (61.8% Fibonacci retracement) would limit downside and support at 1.2912 should remain intact.

In view of this, we are looking to sell cable on recovery as 1.3090-00 should limit upside. Only break of said yesterday’s high at 1.3126 would signal recent upmove has resumed and extend gain to 1.3150-60 but upside should be limited to 1.3190-00, bring retreat later.

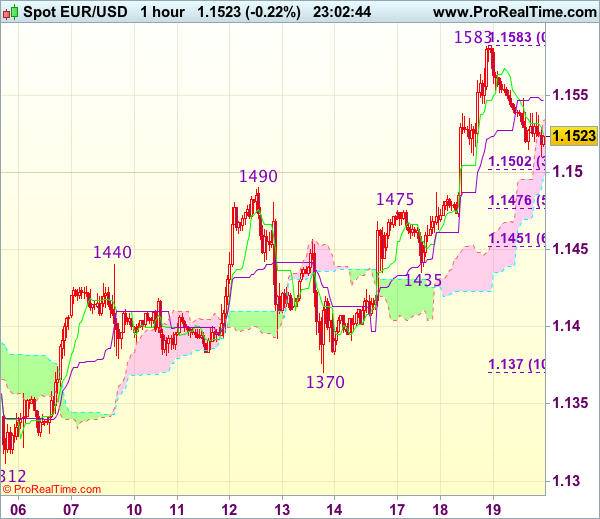

Trade Idea Wrap-up: EUR/USD – Buy at 1.1495

EUR/USD - 1.1529

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1525

Kijun-Sen level : 1.1547

Ichimoku cloud top : 1.1534

Ichimoku cloud bottom : 1.1497

Original strategy :

Buy at 1.1495, Target: 1.1595, Stop: 1.1460

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1495, Target: 1.1595, Stop: 1.1460

Position : -

Target : -

Stop : -

As the single currency has retreated after surging to 1.1583 yesterday, suggesting consolidation below this level would be seen and pullback to 1.1500-05 (38.2% Fibonacci retracement of 1.1370-1.1583) cannot be ruled out, however, reckon previous resistance at 1.1490 would contain downside and bring another upmove later, above said resistance at 1.1583 would extend recent upmove to 1.1600-10 and then 1.1630 but loss of upward momentum should prevent sharp move beyond 1.1650-60.

In view of this, we are looking to buy euro on further pullback as previous resistance at 1.1490 should turn into support and contain downside, bring another rise. Below 1.1475-76 (another previous resistance and 50% Fibonacci retracement of 1.1370-1.1583) would defer and signal top is formed, risk correction to 1.1450-55 (61.8% Fibonacci retracement) and then test of support at 1.1435 which is likely to hold from here.