Sample Category Title

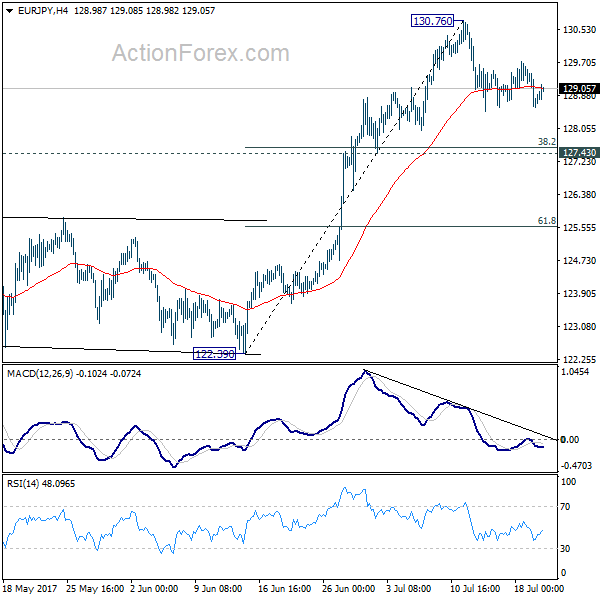

EUR/JPY Daily Outlook

Daily Pivots: (S1) 128.46; (P) 128.99; (R1) 129.41; More...

EUR/JPY is staying in the consolidation pattern from 130.76 and intraday bias remains neutral. Deeper fall might be seen. But downside should be contained by 127.43 cluster support (38.2% retracement of 122.39 to 130.76 at 127.56) and bring rebound. Above 130.76 will extend the larger rally to next key fibonacci level at 134.20.

In the bigger picture, the down trend from 149.76 (2014 high) is completed at 109.03 (2016 low). Current rally from 109.03 should be at the same degree as the fall from 149.76 to 109.03. Further rise is expected to 61.8% retracement of 149.76 to 109.03 at 134.20. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. Medium term outlook will remain bullish as long as 124.08 resistance turned support holds.

Swiss Franc Trading A Tad Lower In The Morning Session

For the 24 hours to 23:00 GMT, the USD marginally declined against the CHF and closed at 0.9548.

In the Asian session, at GMT0300, the pair is trading at 0.9549, with the USD trading slightly higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9532, and a fall through could take it to the next support level of 0.9514. The pair is expected to find its first resistance at 0.9564, and a rise through could take it to the next resistance level of 0.9578.

Ahead in the day, traders will look forward to Switzerland’s trade balance figures for June.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

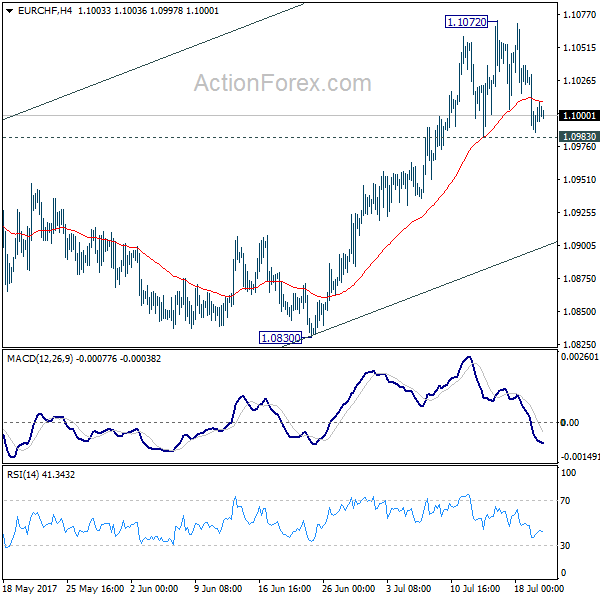

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0983; (P) 1.1008; (R1) 1.1030; More...

Intraday bias in EUR/CHF remains neutral for the moment. As long as 1.0983 support holds, further rally is expected in the cross. Current rise from 1.0629 should target 1.1127/98 resistance zone. However, break of 1.0983 will indicate short term topping and turn bias back to the downside for 55 day EMA (now at 1.0908).

In the bigger picture, the price actions from 1.1198 are seen as a corrective move. Such correction could have completed after defending 38.2% retracement of 0.9771 to 1.1198 at 1.0653. Decisive break of 1.1198 will resume the long term rise from SNB spike low back in 2015. In such case, EUR/CHF could eventually head back to prior SNB imposed floor at 1.2000. However, rejection from 1.1198 will extend the multi-year range trading with another fall.

Loonie Reverses Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.25% against the CAD and closed at 1.2600.

On the data front, Canada's manufacturing shipments climbed 1.1% MoM in May, topping market consensus for a rise of 0.8%. Manufacturing shipments had advanced by a revised 0.4% in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.2614, with the USD trading 0.11% higher against the CAD from yesterday's close.

The pair is expected to find support at 1.2577, and a fall through could take it to the next support level of 1.2540. The pair is expected to find its first resistance at 1.2652, and a rise through could take it to the next resistance level of 1.2690.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

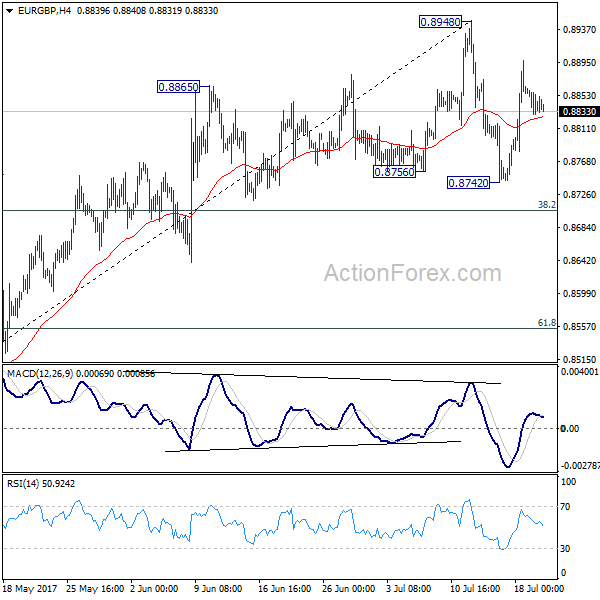

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8825; (P) 0.8844; (R1) 0.8859; More

Intraday bias in EUR/GBP remains neutral for the moment as it's staying in range of 0.8742/8948. On the downside, below 0.8742 will target 38.2% retracement of 0.8312 to 0.8948 at 0.8705 first. Break will target 61.8% retracement at 0.8555 next. However, break of 0.8948 will extend the rebound from 0.8312 towards 0.9304 resistance.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. It's uncertain whether it is finished yet. But in case of another fall, we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside and bring rebound. Whole up trend from 0.6935 is expected to resume after consolidation from 0.9304 completes.

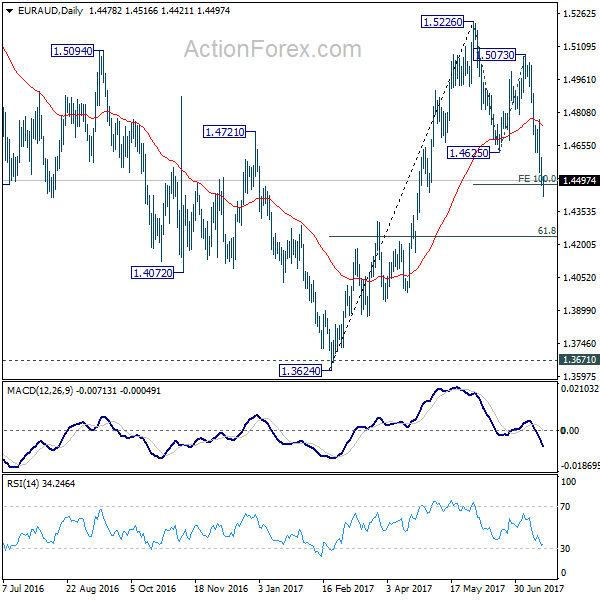

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4432; (P) 1.4518; (R1) 1.4563; More...

EUR/AUD drops to as low as 1.4421 so far today and met 100% projection of 1.5226 to 1.4625 from 1.4472. The cross quickly recovered. But for the moment, with 1.4617 minor resistance intact, intraday bias remains on the downside. Firm break of 1.4472 will pave the way to larger fibonacci level at 61.8% retracement of 1.3624 to 1.5226 at 1.4236. Meanwhile, above 1.4617 will indicate short term bottoming and turn bias back to the upside for 55 day EMA (now at 1.4744).

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term has completed at 1.3624. But we will monitor the structure of the decline from 1.5226 to adjust our view. Above 1.5226 will target a test on 1.6587 key resistance. However, further downside acceleration will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

Euro Treading Water as ECB Draghi Awaited, Yen Steady after BoJ

Dollar recovers in general today as markets turned into consolidation mode. Euro is treading water while markets await ECB rate decision and press conference. Traders would be eager to hear how ECB President Mario Draghi would clarify his comments in the past few weeks. Or Draghi will just let markets' perceived ECB hawkishness be an assumed base case. Meanwhile, Yen is steady as BoJ delivered what are expected, keeping policies unchanged, raising growth forecast and lowering inflation forecast. Aussie was lifted briefly by solid job data but quickly retreated.

BoJ left policies unchanged, raised growth forecast, cut inflation projections

BoJ left monetary policies unchanged as widely expected. Short term policy interest rate was held at -0.1%. The central bank also maintained the annual pace of asset purchase at JPY 80T to keep 10 year JGB yield at around 0%. Meanwhile, BoJ noted in the quarterly report that "recent price developments have been relatively weak, as companies remained cautious in raising wages and prices." And, "risks to the economy and price outlook are skewed to the downside." Also as widely expected, BoJ lowered inflation projections and raised growth projections. The timing for meeting 2% inflation target is pushed back for the sixth time. BoJ now expects inflation to hit target in the fiscal year ending March 2020. Here is a summary of the revisions.

For fiscal 2017:

- Core inflation is projected at 1.1%, down from prior forecast of 1.4%

- GDP growth is projected at 1.8%; up from prior forecast of 1.6%

For fiscal 2018:

- Core inflation is projected at 1.5%, down from prior forecast of 1.7%

- GDP growth is projected at 1.4%; up from prior forecast of 1.3%

For fiscal 2019:

- Core inflation is projected at 1.8%, down from prior forecast of 1.9%

- GDP growth is projected at 0.7%; unchanged from prior forecast of 0.7%

Also from Japan, trade surplus narrowed to JPY 0.08T in June. All industry activity index dropped -0.9% mom in May.

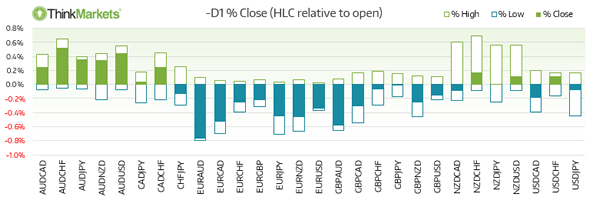

Aussie enjoyed brief lift by solid job data

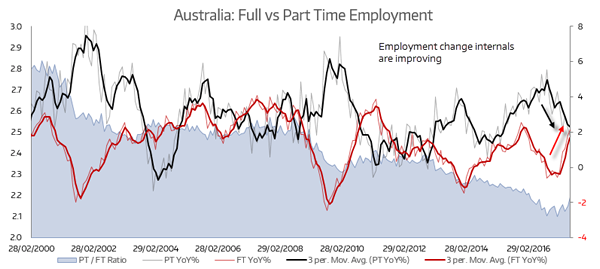

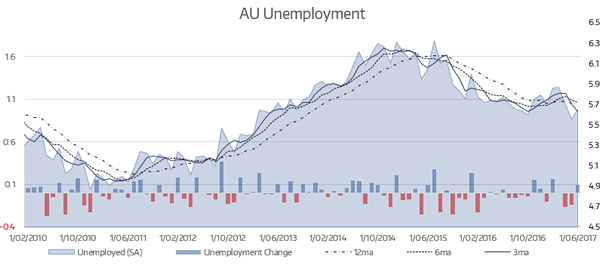

Aussie is lifted earlier today by solid job data but is seen losing momentum. Headline job data showed 14k growth in June, slightly below expectation of 15k. Prior month's figure was revised down from 42k to 38k. Unemployment rate was unchanged at 5.6%. Looking at the details, full-time jobs rose 62k while partly offset by -48k fall in part-time jobs. Australia NAB business confidence was unchanged at 7 in Q2.

Aussie jumped sharply this week as RBA noted that the neutral nominal rate is now at 3.5%. But with reduction in risk aversion and/or increase in trend growth rate, the neutral real interest rate could rise back from current 1.0% to 1.5%. And that indirectly implies that the neutral nominal rate could also follow and rise. Australia Prime Minister Malcolm Turnbull tried to calm the market and said that RBA is only "sending a signal, which is probably prudent, which is to say ... rates are more likely to go up than go down."

Euro cautious ahead of ECB

Euro is trading mixed as markets are awaiting ECB rate decision and press conference. The central bank is widely expected to keep policies unchanged today. The common currency was shot up in late June after ECB President Mario Draghi's upbeat comments on the economy and receding political risks. Draghi further noted that renewed reflationary forces could now give room for "adjustment of parameters" of the current stimulus program. There are speculations that ECB could announce tapering of some sort in the September meeting, or by latest in October. But in any case, today's press conference will give Draghi a chance to clarify if the markets have misjudged him. Without any clarifications, market will take the assumption of tapering in 2018 as a assumption and that could provide additional lift to the Euro.

Elsewhere

UK retail sales will be a focus in European session today. Germany will release PPI. Swiss will release trade balance. from US, jobless claims, Philly Fed survey and leading indicators will be featured.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.4432; (P) 1.4518; (R1) 1.4563; More...

EUR/AUD drops to as low as 1.4421 so far today and met 100% projection of 1.5226 to 1.4625 from 1.4472. The cross quickly recovered. But for the moment, with 1.4617 minor resistance intact, intraday bias remains on the downside. Firm break of 1.4472 will pave the way to larger fibonacci level at 61.8% retracement of 1.3624 to 1.5226 at 1.4236. Meanwhile, above 1.4617 will indicate short term bottoming and turn bias back to the upside for 55 day EMA (now at 1.4744).

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term has completed at 1.3624. But we will monitor the structure of the decline from 1.5226 to adjust our view. Above 1.5226 will target a test on 1.6587 key resistance. However, further downside acceleration will dampen our view and would drag EUR/AUD lower to retest key support zone around 1.3624.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| JPY | BOJ Monetary Policy Statement | |||||

| 23:50 | JPY | Trade Balance (JPY) Jun | 0.08T | 0.12T | 0.13T | 0.12T |

| 1:30 | AUD | NAB Business Confidence Q2 | 7 | 6 | 7 | |

| 1:30 | AUD | Employment Change Jun | 14.0k | 15.0k | 42.0k | 38.0k |

| 1:30 | AUD | Unemployment Rate Jun | 5.60% | 5.60% | 5.50% | 5.60% |

| 4:30 | JPY | All Industry Activity Index M/M May | -0.90% | -0.80% | 2.10% | 2.30% |

| 6:00 | CHF | Trade Balance (CHF) Jun | 2.89B | 3.40B | ||

| 6:00 | EUR | German PPI M/M Jun | -0.10% | -0.20% | ||

| 6:00 | EUR | German PPI Y/Y Jun | 2.30% | 2.80% | ||

| 8:00 | EUR | Eurozone Current Account (EUR) May | 23.3B | 22.2B | ||

| 8:30 | GBP | Retail Sales M/M Jun | 0.30% | -1.20% | ||

| 11:45 | EUR | ECB Rate Decision | 0.00% | 0.00% | ||

| 12:30 | EUR | ECB Press Conference | ||||

| 12:30 | USD | Initial Jobless Claims (JUL 15) | 245K | 247K | ||

| 12:30 | USD | Philly Fed Manufacturing Jul | 23.7 | 27.6 | ||

| 14:00 | EUR | Eurozone Consumer Confidence Jul A | -1.1 | -1.3 | ||

| 14:00 | USD | Leading Indicators Jun | 0.40% | 0.30% | ||

| 14:30 | USD | Natural Gas Storage | 57B |

Euro Weakens Ahead Of ECB Meeting, BoJ And AU Employment In Focus

BoJ meeting, trade data and AU employment make the bulk of Asia data where attention will then shift to tonight's ECB meeting.

The Euro weakened overnight as traders booked profits ahead of today's ECB meeting. The confusion following Draghi's seemingly hawkish speech last month the ECB may use today's meeting to tweak their message to calm the markets. Draghi sent the Euro above 113 at the end of June and ECB officials attempt to tame the run came to little avail as the Euro stopped just shy of 116 overnight. So they may use today's meeting to tweak the message again and take the fun ot of the rally.

EURAUD remains out preferred Euro short as sentiment on AUD remains strong, it is the strongest G10 performer this year whilst Euro faces further profit taking over the near-term. AU employment is expected to soften slightly but unless it throws a curve-ball then AU should remain supported. If there is any concern to the AUD rally it may come from Guy Debelle's speech tomorrow as the temptation to jawbone AUD may now be on his agenda.

The positive sentiment surrounding AUD is likely to help AUDJPY on its way to Y90 following today's BoJ meeting. No major changes are expected on the policy front but a downgraded inflation outlook is viable. With household spending, wage growth CPI all disappointing, it is hard to justify their inflation forecast let alone a 2% target. Large speculators have also piled into Yen shorts in recent weeks whilst bulls remain on the sideline, making Yen the preferred short over the coming weeks.

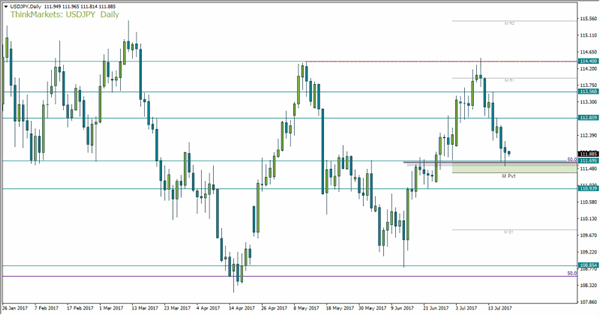

US data bucked the trend by beating forecasts overnight, seeing an improvement in building permits and housing starts. It helped slow the bleeding on the US Dollar index, although the weaker Euro probably provided the bulk of support. USDJPY found support at 111.55 and focus now switches to the BoJ meeting where a corrective rally is expected. The healthcare plan disappointment is largely priced in and Yen outflows are likely to persist as traders are currently net short the Yen by US$12.3bn (as of last week's CFTC report).

The monthly pivot and 50% retracement provide a broad zone up support between 111.37 – 111.68, with yesterday's bullish hammer respecting the upper part of the zone. If we are to see a break of yesterdays low, as long as we remain above the monthly pivot then we do see potential for an eventual upside move so. Bearish momentum on the lower timeframes is waning and the downside appears stretched.

AU Employment Sends AU Close To 80

Close to 80 but no cigar, yet. Markets perceived the employment set to be a net positive to promptly bid AUD higher, only to book profit just shy of the milestone

AUD extended gains as employment was seen as a net positive. As there was an expectation for employment to soften slightly, the realisation of the fact came as no surprise. Unemployment ticked higher to 5.6% as expected and employment change increased by +14k verses +15k expected (down from 38k prior). The higher participation rate took the edge off of the slightly higher unemployment rate, which we expect to soften over the coming months as capacity utilisation continues to increase.

Part-time employment weighed heavily on total jobs number yet full-time employment increased by 62k, allowing markets to see the a healthier underlying employment change other than the 14k presented.

AUDUSD stopped just shy of 80c although we'd be surprised if this key, psychological level broke upon first attempt as temptation to book a quick profit may be high. But unless we hear a verbal intervention of some sorts, we should be above 80c soon enough. Volatility is something to also note as the past two weeks are already bordering on an outlier. Last week's close was its most bullish week since Feb and if you look across the percentage changes, you'll see that volatile weeks are not exceeded and, often, the subsequent week's range is sanguine. As this occurs below the 80c level and the risk of verbal intervention is potentially rising, this may pour water on volatility for the bulls. However, a break above 80c is a milestone worthy of seeking bullish setups on lower timeframes (intraday) if you remember the volatility potential theoretically goes down the higher we trade.

RBA Assistant Governor Guy Debelle speaks tomorrow and traders are on guard for a potential jawbone. With sentiment and technicals on AUD remaining very much bullish we have moved beyond levels which have previously warranted a verbal intervention of some sort. Throughout 2016 the statement included “An appreciating exchange rate could complicate' the economic adjustment when AUD traded between 0.732-0.77. In 2017 this was switched from 'could complicate' to 'would complicate' for the same range, yet AUD now trades just shy of 0.80. The last time AUD traded at these levels was in 2015 when the language used within the statement was quite bluntly 'further depreciation is likely / necessary'.

Focus now shifts to the BoJ meeting where we think AUDJPY is headed for Y90. Yen outflows are likely to persist over the coming weeks and a lower inflation outlook from BoJ should help support carry trades.

In some ways is it not fair to directly compare the levels over time as the economic background has changed over this period. Yet it has not improved to the point where AUD will be comfortable with a higher AUD. In the backdrop of a weaker USD whilst the Fed find data hard to truly justify another hike, it may also be the RBA's perception of this extra hike as to whether they try to publicly talk AUD down between meetings. If they were banking on the Fed to hike and effectively remove the 25bps positive carry AUDUSD currently has, then there is good reason to expect verbal intervention at some point. Tomorrow may just be that day.

Market Morning Briefing: All Eyes Are Fixed On The BOJ Policy Meet In The Morning

STOCKS

Stocks have resumed their uptrend and could possibly face some interim dips within an overall uptrend. Some clarity is needed in Dax which is trading at crucial levels just now.

Dow (21640.75, +0.31%) has bounced back from levels near 21470 and is trading above 21600 just now. Upward momentum looks strong and we could possibly see arise towards 21800 in the coming sessions. Near term trend is firmly up.

Dax (12452.05, +0.17%) is almost stable and is holding above the immediate support near 12400. If the support holds, the price index could further towards 12500-12600. Failure to sustain above 12400 would shift our focus to levels near 12300 or lower. Need to wait and watch.

Shanghai (3237.48, +0.20%) has risen sharply in the last 3-sessions and is heading towards immediate channel resistance near 3250-3260. From there a short correction is possible before resumption of the uptrend. Near term looks firmly bullish.

Nikkei (20092.14, +0.36%) has started to rise from levels near 19950. It could continue to move up towards 20200-20300 in the coming sessions. This could possibly pull up Dollar-Yen also to higher levels in the next few sessions.

Nifty (9899.60, +0.74%) could limit its near term dip at 9800 and could be headed towards 10000 in the coming sessions. Near term looks strongly bullish.

COMMODITIES

Gold (1238) and Silver (16.21) are still trading above their crucial support at 1231 and 16.20 respectively. A break above 1245 is necessary for gold to remain bullish towards 1260 for the near term else a fall below 1230 could take it lower towards 1220. Silver is trading within the range of 16.20-16.50 and only a close above 16.50 could negate our midterm bearish view. As dollar index is highly oversold, it will be difficult for Bullion to maintain this short term bullish momentum. At the same time market is waiting for today’s ECB press conference, at 6:00 pm IST.

Muted price action had been seen in Copper (2.71) for last couple of trading sessions. It is trading within a range of 2.66-78. Only above 2.78, higher resistances of 2.80 can come into consideration. In the medium term 2.55-57 are going to be a strong support and we will remain bullish while it is trading above those levels.

Both Brent (49.66) and WTI (47.28) moved upward as U.S weekly crude inventory data (actual -4.7M B) was highly supportive for the entire energy pack. This is the 4th consecutive week of shortage in weekly U.S crude inventory. We will remain bullish while Brent and WTI are trading above 48.80 and 46.70 on a weekly closing basis. Immediate trading range for Brent and WTI could be 48-52 and 46-50 respectively.

FOREX

All eyes are fixed on the BOJ policy meet in the morning and the ECB meet in the afternoon. Till then, no activity in the markets is expected.

Dollar-Yen (111.97) is being watched for the reaction after the BOJ policy decision due in a few minutes today. We expect the support of 111.00 to be tested before any major short covering emerges.

Then comes the ECB policy decision which may affect Euro (1.1525) which has been trading quietly for the last 2 sessions. Repeat - The trend remains firmly up but it must be noted that the net position in Euro is the largest since 2011 and any surprise from the central bank or any other corner may trigger a very sharp correction. Similarly, the Dollar Index (94.84) may have attracted too many shorts. These two crowded trades may invite nasty surprises eventually as the previous historical instances show. Therefore high caution warranted at the current levels this week.

Aussie (0.7940) has almost tested 0.80 levels with a high of 0.7990. While a couple of days of rest after the sharp rally can’t be ruled out, the larger target of 0.8150-75 remains unchanged and a break above 0.80 may provide more impetus.

Pound (1.3024) remains in a shallow corrective mode which is expected to be followed by another leg up towards 1.3125 and then 1.32-1.34 later.

Regarding Dollar-Rupee (64.29), the trend remains firmly down and but some short covering and fresh buying of Dollars can be expected near 64.20.

INTEREST RATES

The US yields have been coming off from channel resistances and could head to lower levels in the near term. The 30Yr (2.85%) could test 2.80% in the near term while the 10?Yr (2.27%) could come off towards 2.20/23%. Medium to long term looks bearish.

The German-US 2Yr (-2.00%) and the German-US 10YR (-1.73%) have dipped a bit but could rise back soon to rise towards -1.95% and -1.70% respectively. We wait for the ECB meeting today to see if that impacts the Euro and the yields.

The Japan yields could start moving higher in the coming sessions and looks bullish just now. This could possibly indicate that the Dollar-Yen may start moving up too in the coming sessions.