Sample Category Title

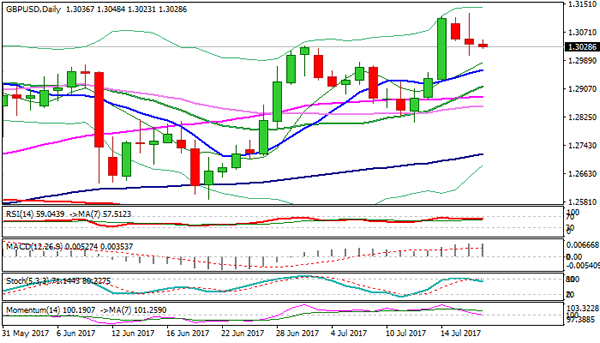

Technical Outlook: GBPUSD – Hourly Cloud Base Holds For Now But Near-Term Risk Is Skewed Lower

Cable stays at the back foot on Wednesday and consolidating within narrow range at 1.3040 zone, after Tuesday's sharp fall on weak UK CPI data found footstep at 1.3000 zone.

Near-term action is so far holding above hourly cloud base (1.3026) which marks key support along with psychological 1.3000 level.

While cloud base is holding, the price is expected to range within hourly cloud (1.3026/1.3074), with lift above cloud to signal an end of corrective phase and shift focus higher.

Eventual close above 1.3109 (Fibo 38.2% of 1.5016/1.1930 descend) is needed to signal bullish continuation. Otherwise, increased downside risk could be expected on sustained break below hourly cloud and 1.3000 handle. The notion is supported by reversal of slow stochastic from o/b territory on daily chart.

Close below 1.3010 (Fibo 38.2% of 1.2824/1.3125 upleg) is needed to generate stronger bearish signal for deeper pullback from fresh high at 1.3125. With no data from UK today, technicals are expected to be the main driver of GBPUSD pair.

Res: 1.3048, 1.3076, 1.3109, 1.3125

Sup: 1.3023, 1.3000, 1.2968, 1.2939

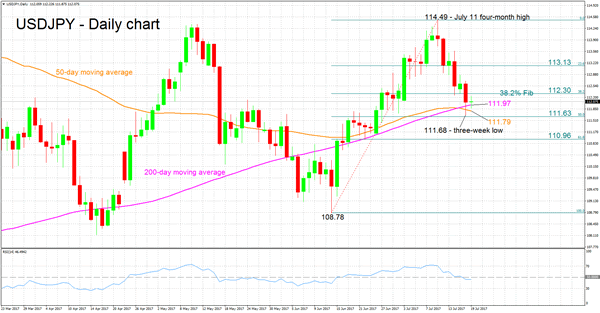

USDJPY Intra-Day Neutral, Records Bearish Cross

USDJPY hit a three-week low of 111.68 during yesterday's trading. The pair experienced significant declines since reaching a four-month high of 114.49 on July 11.

The RSI is currently at 46, close to the 50 neutral-perceived level. In addition, the indicator has flatlined, projecting neither a positive, nor a negative intra-day direction.

On the upside, the area around the 38.2% Fibonacci retracement level (June 14 – July 11 upleg) at 112.30 could provide resistance. Further up, the 113 handle, combined with the 23.6% Fibonacci mark at 113.13, might form an additional resistance area.

On the downside, the 200-day moving average (MA) and 50% Fibonacci level, ranging from 111.97 to 111.63, could offer support. Notice that this range also encapsulates the current level of the 50-day MA as well as yesterday's three-week low. Moreover, bear in mind that the 200-day MA was briefly violated today. Should the price continue declining, the 61.8% Fibonacci mark at 110.96 would be eyed next.

In the wider picture, the pair has recorded a bearish cross this week when the 50-day MA moved above the 200-day one. This is generally perceived as a positive medium-term signal. However, it is too early to judge the strength of this signal – a move below both MAs would reinforce it. For the time being, the pair remains predominantly neutral in the medium-term given the significant sideways movement since the start of the year.

Markets Calm Ahead Of ECB, BoJ Meetings, Oil Pressured On US Inventories

It has been a quiet overnight session ahead of what could be a stormy Thursday with the European Central Bank and the Bank of Japan holding their policy meetings. Most majors traded in a narrow range, while oil prices recorded the biggest move of the day.

The Australian and New Zealand dollars continued gaining against their US counterpart during the Asian session. Aussie/dollar was up to last trade at 0.7932, supported by comments perceived to be hawkish from the Reserve Bank of Australia’s policy meeting minutes and higher commodity prices.

The greenback was steady against the yen ahead of the Asian markets close, having traded in a relatively narrow range of 111.87-112.23. The US currency has been impacted negatively from both political and economic developments. The latest news on the failure to repeal and replace Obamacare, after two more Republican Senators opposed the latest bill proposal, sent the dollar tumbling against all major currencies. The news came after Friday’s disappointing inflation and retail sales figures. The markets are skeptical about future interest rate hikes considering the lack of inflation pressures and fear of the Trump administration failing to pass any legislation which could spur growth. The yield on 10-year US Treasuries is up one basis point to 2.27%, though down seven basis points this week after dropping five basis points last week.

The euro has been pressured during Asian trading as some profit taking might have taken place ahead of the ECB policy meeting tomorrow. It will be ECB President Mario Draghi’s first public appearance following his relatively hawkish comments in Sintra, Portugal, which sent the euro to new highs against the dollar. News broke out overnight about the ECB examining its options concerning its stimulus package, in order to make a decision in the autumn. Traders will be closely monitoring the meeting tomorrowas it could significantly move the euro against its peers. Euro/dollar was last trading at 1.1534.

Sterling was flat against the US dollar during the Asian session. Pound/dollar was last trading at 1.3037.

Crude oil prices were the biggest movers during session, with both WTI and Brent falling about half-a-percent. Oil prices pulled back, as investors awaited fresh data on US crude inventories, which are seen to have increased last week. WTI was last trading at $46.15 a barrel while Brent was at $48.61.

Gold has been under slight pressure today, following a strong rally for three days. The precious metal was last trading at $1,240.00 an ounce.

While the Asian session was quiet due to a lack of economic releases, the US session could get busier amid the release of building permits issued in June as well as housing starts. Oil traders will likely be busy with the release of US crude oil inventories in the early US session.

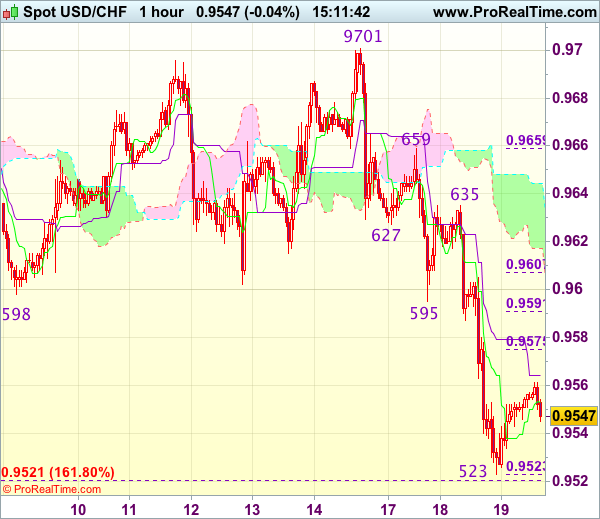

Trade Idea : USD/CHF – Exit long entered at 0.9555

USD/CHF - 0.9647

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9549

Kijun-Sen level : 0.9564

Ichimoku cloud top : 0.9644

Ichimoku cloud bottom : 0.9617

Original strategy :

Bought at 0.9555, Target: 0.9655, Stop: 0.9520

Position : - Long at 0.9555

Target : - 0.9655

Stop : - 0.9520

New strategy :

Exit long entered at 0.9555,

Position : - Long at 0.9555

Target : -

Stop : -

Although the greenback recovered after falling to 0.9523 yesterday, near term downside risk remains and below said support would extend recent selloff to 0.9500 and possibly towards 0.9475-80, however, loss of near term downward momentum should prevent sharp fall below latter level and reckon 0.9440-50 would hold from here, risk from there is seen for another rebound later.

In view of this, would be prudent to exit long entered at 0.9555 and stand aside for now. Above 0.9575 (38.2% Fibonacci retracement of 0.9659-0.9523) would bring a stronger recovery to previous support at 0.9595 but reckon upside would be limited to 0.9605-10 (61.8% Fibonacci retracement) and resistance at 0.9635 should remain intact, bring another decline later.

Dollar Bears

UK Consumer Price Index (CPI) data was released on Tuesday showing inflation easing for the first time in nearly 10 months, retreating from the near 4-year high touched in May, as fuel prices fell substantially in the UK in June. The consumer price index increased by an annual rate of 2.6% in June, falling below the consensus forecast of 2.9%, and below the 2.9% rise recorded in May. UK inflation is above the BoE’s 2.0% target for the 5th straight month, but the slowdown in the rate of inflation is likely to dull calls from some of the UK Monetary Policy Committee members for a near-term hike in UK interest rates.

USD fell back to an 11-month low against many of its G-10 counterparts as President Trump’s economic revitalization agenda stumbled with his health care reform bill “dead in the water”, as 2 more of his own party’s Senators announced their opposition to the plan.

EUR gained nearly 1% on the day versus USD as EURUSD reached a high of 1.15828, levels not seen for over 1 year. The market is cautious of pushing EURUSD too high for fear that the European Central Bank policy meeting on Thursday proves less hawkish than the bulls are hoping for. Currently, EURUSD is trading around 1.1535.

GBP fared poorly against overall USD weakness as CPI data showed UK inflation falling in June. GBPUSD traded down as the data was released, moving from the day’s high of 1.31251 to trade as low as 1.30044 on the day. Currently, GBPUSD is trading around 1.3040.

The USD bears were seen in USDJPY as the USD sell-off saw the pair back off from early highs of 112.618, to give up 0.7% on the day to trade as low as 111.681. The Bank of Japan is expected to keep economic policy unchanged at its scheduled meeting on Thursday. Currently, USDJPY is trading around 112.15.

AUDUSD improved over 1.8% on the day as a resolute Reserve Bank of Australia stated it isn’t ready to join global Central Banks in reducing policy stimulus. AUDUSD traded off early lows of 0.77859 to trade up to a new 2 year high of 0.79424 on the day. Currently, AUDUSD is trading around 0.7930.

Ahead of today’s EIA report on US Oil Inventories WTI has also benefitted from USD weakness, trading from $46.02pb to a high on the day of $47.12pb. The US EIA Inventories data releasing today will likely cause significant volatility in Oil. WTI is currently trading around $46.50pb.

Gold gained 0.7% on the day to trade as high as $1,243.30, a level not seen since the start of July. Currently, Gold is trading around $1,241.

At 13:30 BST US Housing Starts (MoM) (Jun) will be released. The consensus is for an improvement to 1.150 Million from the previous reading of 1.092 Million. An improved number will be seen as vindication that the US economy is growing, amid recent mixed economic data releases.

At 15:30 BST the United States Energy Information Administration (EIA) will release the EIA Crude Oil Stocks change (Jul 14). The previous drawdown of -7.5645 Million is expected to improve to a drawdown of -3.740 Million.

Technical Outlook: EURUSD Eases On Profit-Taking But Quiet Trading Expected Ahead Of ECB

The Euro eases in early Wednesday's trading after posting new 2 1/2 month high at 1.1583 on strong acceleration on Tuesday. Profit-taking on past three-day rally could drag the price further down, as overbought slow stochastic and RSI are turning lower on daily chart. Psychological support at 1.1500 and rising Tenkan-sen (1.1476) should ideally contain dips and keep bulls in play, as bulls eye targets at 1.1614 and 1.1716/35 in extension. However, today's trading is likely to be within limited range as markets are focusing on tomorrow's ECB policy meeting which is expected to provide stronger signals.

Res: 1.1565, 1.1614, 1.1643, 1.1716

Sup: 1.1500, 1.1476, 1.1452, 1.1400

Trade Idea : GBP/USD – Sell at 1.3090

GBP/USD - 1.3039

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3037

Kijun-Sen level : 1.3066

Ichimoku cloud top : 1.3076

Ichimoku cloud bottom : 1.3029

New strategy :

Sell at 1.3090, Target: 1.2990, Stop: 1.3125

Position : -

Target : -

Stop : -

Although the British pound rose briefly to 1.3126, the subsequent retreat suggests temporary top is possibly formed and consolidation below this level would be seen with mild downside bias, below support at 1.3005 would add credence to this view, bring retracement of recent upmove to 1.2965-70 (50% Fibonacci retracement of 1.2812-1.3126), then test of previous resistance at 1.2955 but reckon 1.2930-35 (61.8% Fibonacci retracement) would limit downside and support at 1.2912 should remain intact.

In view of this, we are looking to sell cable on recovery as 1.3090-00 should limit upside. Only break of said yesterday’s high at 1.3126 would signal recent upmove has resumed and extend gain to 1.3150-60 but upside should be limited to 1.3190-00, bring retreat later.

Trade Idea : EUR/USD – Buy at 1.1495

EUR/USD - 1.1538

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1540

Kijun-Sen level : 1.1547

Ichimoku cloud top : 1.1496

Ichimoku cloud bottom : 1.1470

Original strategy :

Buy at 1.1335, Target: 1.1440, Stop: 1.1300

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1495, Target: 1.1595, Stop: 1.1460

Position : -

Target : -

Stop : -

As the single currency has retreated after surging to 1.1583 yesterday, suggesting consolidation below this level would be seen and pullback to 1.1500-05 (38.2% Fibonacci retracement of 1.1370-1.1583) cannot be ruled out, however, reckon previous resistance at 1.1490 would contain downside and bring another upmove later, above said resistance at 1.1583 would extend recent upmove to 1.1600-10 and then 1.1630 but loss of upward momentum should prevent sharp move beyond 1.1650-60.

In view of this, we are looking to buy euro on further pullback as previous resistance at 1.1490 should turn into support and contain downside, bring another rise. Below 1.1475-76 (another previous resistance and 50% Fibonacci retracement of 1.1370-1.1583) would defer and signal top is formed, risk correction to 1.1450-55 (61.8% Fibonacci retracement) and then test of support at 1.1435 which is likely to hold from here.

Currencies: Dollar Decline Slows, At Least For Now

Sunrise Market Commentary

- Rates: Summer trading set to continue

Today's eco calendar remains razor thin with only US housing starts and building permits. Normally they are no market mover, but a downward surprise won't go unnoticed and could benefit US Treasuries further. Overall, we expect trading to remain confined to tight ranges ahead of the ECB. If any, core bonds could trade with a small upward bias. - Currencies: Dollar decline slows, at least for now

Yesterday, the USD was aggressively sold in Asia and in Europe, but tensions eased in US trading. US housing data probably won't be a game-changer for USD trading. The dollar desperately needs high profile good news, but that isn't available right now. Some consolidation might be on the cards today, but a sustained USD rebound isn't around the corner yet.

The Sunrise Headlines

- After an initial decline due to the failure of Republican efforts to end Obamacare, American equity markets rebounded. The tech-heavy Nasdaq closed at a record high. The good mood transferred to Asian markets.

- The Australian Prudential Authority announced that the country's four major banks would need to have tier 1 capital ratios of at least 10.5%. The announcement was less onerous than expected.

- China's holdings of US Treasuries climbed to the highest level since the country ceded its status as America's largest creditor nation to Japan last year. China's total holding of US paper rose by $10B from a month prior to $1.1T in May.

- Greece's return to bond markets is held off partly due to a ceiling set by the IMF on the amount of debt the country can hold, according to unnamed officials. The IMF is expected to discuss a new credit line to Greece tomorrow.

- US President Trump said he was disappointed about the collapse of Republicans' efforts to replace or repeal Obamacare and added that his plan was now to “let Obamacare fail”.

- Not much on the eco calendar today apart from the US housing starts and building permits data and a German bond auction

Currencies: Dollar Decline Slows, At Least For Now

Dollar decline takes a breather

On Tuesday, the dollar nosedived after Conservative lawmakers in the US admitted that a repeal/replacement of Obamacare won't occur anytime soon. Dollar selling was aggressive in Asia and in Europe, but eased later in US dealings. EUR/USD settled north of the 1.1489/1.15 resistance and finished the session at 1.1554. LT interest rate differentials between the US and Germany narrowed further. USD/JPY dropped temporary below the 112 handle but finished the day at 112.07.

Overnight, Asian equities mostly show modest gains as the tension due to the Obamacare stalemate are ebbing. USD/JPY stabilizes near the 112 pivot. EUR/USD trades in the 1.1535 area, off yesterday's correction top (1.1583 area). There is no high profile story to guide trading. Investors are looking forward to tomorrow's BOJ and ECB policy meetings. The Aussie dollar takes a breather after its recent impressive run. AUD/USD is changing hands in the 0.7920/25 area.

Today, the eco calendar is thin with only US housing starts and permits able to move markets. They will get more attention than usually. Starts disappointed over the previous three months, permits during three of the last four months. A rebound is expected as special (weather) factors were probably in play during spring. If the rebound fails to materialize, it might weigh push US yields and the dollar lower. In a day-to-day perspective, we expect some USD calm to return as investors are looking forward to tomorrow's BOJ and ECB decision. We don't expect a meaningful rebound of the dollar. Investors will be cautious to be euro short going into the ECB meeting. We expect the ECB to maintain a balanced approach, but hints on a gradual policy normalisation may trigger more euro gains.

In a broader perspective, the dollar was in the defensive of late. Mediocre US wage growth, Yellen's focus on the recent setback in inflation and soft eco data made markets questioning the pace of future Fed normalisation and weighed on the USD. Initially, EUR/USD didn't retest the 1.1489/1.15 resistance, but this area was broken yesterday on the failure to replace Obamacare. In a longer term perspective, the market discounts very little Fed policy normalisation. At some point this might lend the dollar support. However, in a day-to-day perspective there is no reason to try to catch the falling USD. The dollar needs high profile good news and that isn't available at this stage.

USD: technical picture worsens further

End June, EUR/USD rebounded above the 1.1300/66 resistance. The payrolls and other recent data were not good enough to trigger a sustained USD rebound. Yesterday EUR/USD broke beyond the 1.1489/1.15 resistance. This break opens the door to the LT-correction tops at 1.1616/1.1714. A break would end the long consolidation that followed the sharp decline of EUR/USD in 2014/early 2015. Such a key area is not easy to break. We don't preposition for a break, but the pressure is mounting. Return action below 1.13 would be a first indication of a loss in upside momentum. EUR/USD 1.1119/10 is the next support.

The USD/JPY rally ran into resistance in May and the pair returned lower in the 108.13/114.37 range. The post-Fed USD rebound pushed the pair above the 112.13 correction top, but follow-through gains remain modest. USD/JPY 114.37 resistance was tested, but for now the test is rejected. This suggests a pause in the recent USD/JPY uptrend. We stay cautious on USD/JPY long positions despite the recent decent performance.

EUR/USD nears top of LT consolidation pattern as dollar tumbles on failure to repeal Obamacare act

EUR/GBP

EUR/GBP holding near recent top

Sterling was mostly driven by technical considerations of late. Eco data again came in play yesterday. UK CPI unexpectedly declined from 2.9% Y/Y to 2.6% Y/Y (2.9% was expected).The report eased market expectation/speculation that the BoE would raise its policy rate in the near future. EUR/GBP jumped from the 0.88 area to levels just shy of 0.89 and closed the session at 0.8860. EUR/USD strength reinforced the move. Cable initially lost a full big figure despite broad-based US weakness but rebounded slightly later as USD-selling eased. The pair finished the session at 1.3040.

Today, there are no important eco-data in the UK. Given the thin calendar in the US and Europe, trading in the euro and to dollar will probably also provide little guidance. Brexit remains a wildcard, but it is probably too early to expect big news from the negotiations. So, sterling might also shift into consolidation mode today.

From a technical point of view, EUR/GBP recently broke above the 0.8854/66 resistance (2017 top) to set a new correction top north of 0.89, but the move finally fell prey to profit taking (sterling short squeeze). A break below 0.8720 would suggest that upside momentum is easing. For now, we see all sterling rebounds as technical in nature and don't expect them to last very long. We still look to buy EUR/GBP on more pronounced dips. For that the happen, EUR/GBP probably needs some help from a correction in EUR/USD. This isn't the case yet

EUR/GBP correction short-lived as sterling declines again after soft inflation data

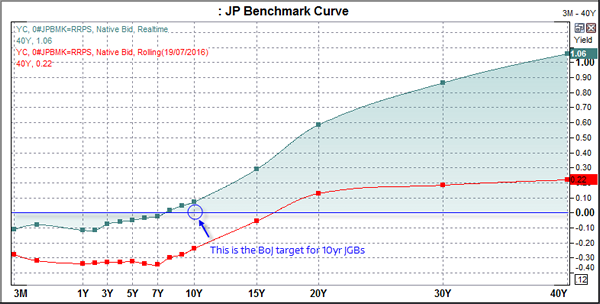

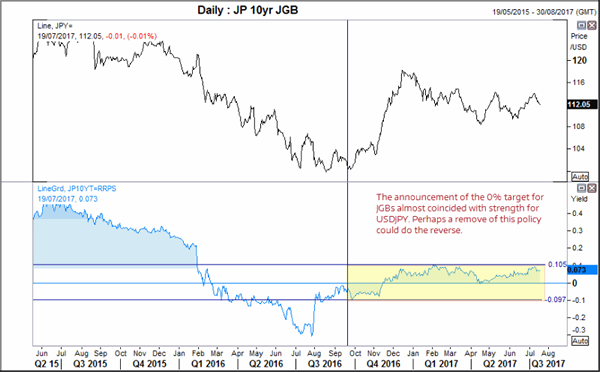

No Change From BoJ Expected, At Least Not Tomorrow

Market consensus of for now change of policy tomorrow, yet with bond markets continuing to give BoJ a headache then a change of some sort cannot be fully discounted at some point.

The Bank of Japan hold their monetary policy meeting tomorrow, which is already having a suppressive effect on price action as we near it. Alongside the usual press conference, statement and decision, the quarterly outlook report will also be released. As we expect no changes to policy tomorrow, it may be the outlook report that is more telling about their confidence of the recovery to be sustained. Yet we cannot rule out a surprise from BoJ regarding their 0% target on JGB's.

Since their last meeting the game has changed somewhat; ECB have turned slightly more hawkish (which prompted BoE ad BoC to follow suit) whilst the FED turned slightly dovish. BoC have since raised rates and there is potential for another hike to follow this year. To add to the list, the RBA crawled slightly out of the neutral zone by speaking of a neutral interest rate being as high as 3.5%. So, from a global policy standpoint is has been a busy period since the previous quarterly outlook. This seemingly combined coordination to tighten is only going to add to the BoJ's job harder regarding policy.

Since September '16 the BoJ have been battling markets to keep the 10yr JGB's ‘around' 0%. This has proven a tough match at times, especially when global stock markets sell off amid expectation of central bank tightening which sends yields higher. As we continue to suspect that ECB are behind the curve and will later be forced to ‘talk taper', this leaves bonds yields susceptible to further upside. In turn, this places extra pressure on the BoJ to keep their rising yields ‘around' 0% as the bond market sell-off rags the 10yrs higher.

Additionally, there have been a couple of BoJ members which have constantly doubted the expansive pace of their QQE program and remain concerned at the financial stability or long-term impact of these actions. Additionally, a recent report, or leak, suggested liquidity concerns are only growing as the BoJ continue their purchase of assets. So, the question now becomes whether the BoJ may announce a change to their policy and of so, how will it be changed?

We do not think such a change will be announced tomorrow but we will look out for subtle clues with the outlook report. There is potential for the inflation forecast to be lowered (again) although markets are likely expecting this due to the lack of inflation in general. With household spending, low wage growth and weak producer prices it is hard to justify their forecasts, let alone a 2% target. A more telling sign may be if they slightly lower their growth outlook, as it is this part which was revised higher on three occasions since 2016. Whilst potential for growth remains, there are just as many headwinds with capex and machinery tool orders printing heavy declines.

We doubt BoJ will announce an end to the 10yr target tomorrow, but it is something that will eventually make sense if yields continue to rise. We note that USDJPY printed an important lower high just days after BoJ announced their new policy with Trump's (now defunct) reflationary policies, sending it into hyperbole. Perhaps the reverse may occur if they are to throw in the towel on the 10yr target. This is something to seriously consider in the light of a hawkish Fed (weaker USD) and headwinds the BoJ face with this particular policy. We doubt it will completely reverse the moves seen since September, but it may have a decent move lower none the less.