Sample Category Title

Dollar Stays Soft after Job and Inflation Data, Yen Paring Gains

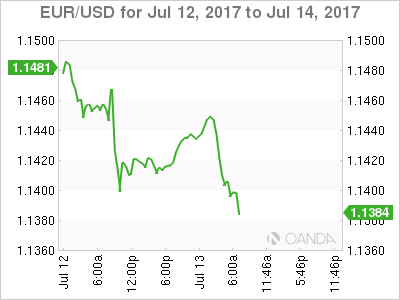

Dollar trades generally weaker today except versus Yen and Canadian Dollar, where it's consolidating in oversold conditions. The greenback, nonetheless, continues to feel the weight added by dovish testimony of Fed Chair Janet Yellen. Yellen will have the second round of her testimony today but that will likely bring little news. Meanwhile, overwhelming strength is seen in Aussie and Kiwi today, as lifted by rebound in commodity prices and solid Chinese trade data. Euro, on the hand, is also struggling as traders start to turn cautious on ECB policy bets. Sterling is believed to be saved by comments from BoE hawk Ian McCafferty and rebounds against most others.

US: Solid jobs, slower inflation

US initial jobless claims dropped 3k to 247k in the week ended July 8, slightly above expectation of 245k. That's the 123 straight weeks of sub 300k reading. Four week moving average rose 2.25k to 245.75k. Continuing claims stood at 1.95m in the week ended July 1, staying below 2m for 14 straight week. Also from US, headline PPI slowed to 2.0% yoy in June but beat expectation of 1.9% yoy. Core PPI also slowed, to 1.9% yoy, below expectation of 1.9% yoy. Released from Canada, new housing price index rose 0.7% mom in May.

ECB Draghi might signal policy shift at Jackson Hole

There are talks surfacing today that ECB President Mario Draghi could make use of the Fed's Jackson Hole conference in August to address the future of ECB's monetary stimulus. That will be the first appearance in the annual conference in three years. It's generally believed that ECB will formally announce what to do after the current EUR 60b per month asset purchase ends by the year end. And Jackson Hole could be a perfect occasion for Draghi to signal the policy shift.

ECB Governing Council member Ilmars Rimsevics said on Latvian radio today that the quantitative easing problem could continue fro at least " a couple of years" He pointed out that back in June, inflation forecasts were cut to 1.5% this year and 1.3% next. He noted that "shows that the medium-term inflation target of 2 percent is not met, which means that this programme could continue for at least a couple of years."

Released from Germany, CPI was finalized at 0.2% mom, 1.6% yoy in June. From Swiss, PPI dropped -0.1% mom, -0.1% yoy in June.

BoE hawk McCafferty pushed for balance sheet unwinding

BoE hawk Ian McCafferty said in an interview that the central bank should start considering to unwind its GBP 435b assets from the quantitative easing program. While there has been talks about rate hikes, this is so far the first voice regarding unwinding. Meanwhile, McCafferty maintained his views that interest rates should be raised and would continue to vote for a hike in August meeting. He cited the solid job data released earlier this week as the support for his view. Regarding inflation, he expects it to peak at around 3% while consumer growth will slow.

BoJ to revise down inflation forecasts, up growth projections

In Japan, there are continuous speculations on BoJ's forecasts revision in July. Unnamed sources were quoted by newspaper saying the BoJ will lower fiscal 2017 inflation projection from 1.4% to somewhere between 1% and 1.4%. That would be a sensible decision as core inflation stood at 0.4% in May, well off the 2% target. On the other hand, to be in line with recent upgrade in economic assessment, BoJ could also raise growth projections.

China trade data suggests solid external demand and resilient domestic economy

China posted a trade surplus of USD 42.8b in June, widened from prior month's USD 40.8b but missed expectation of USD 43.2b. Exports jumped 11.3% yoy while imports grew 17.2% yoy. The data showed that the economy in China is holding well, with solid global demand for its exports. The domestic economy also showed much resilience. In Yuan terms, trade surplus widened to CNY 294b, up from CNY 282b and beat expectation of CNY 273b.

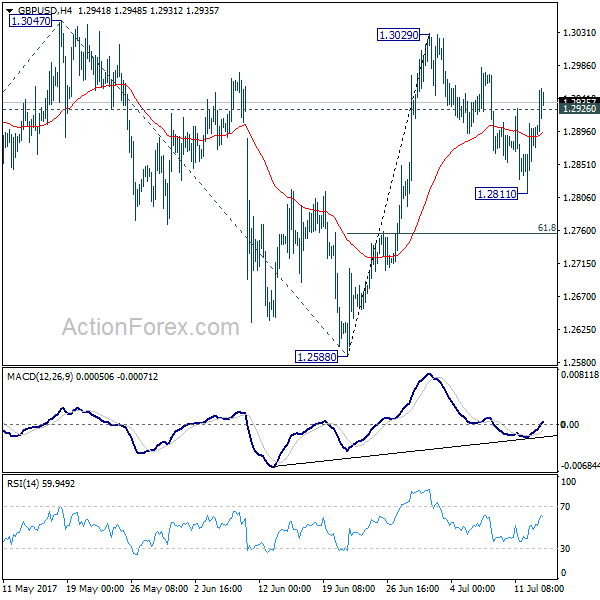

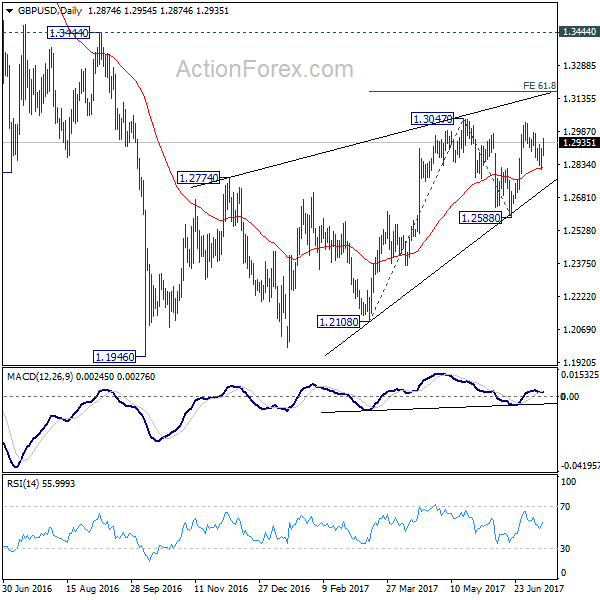

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2827; (P) 1.2867; (R1) 1.2922; More...

GBP/USD's rebound and break of 1.2926 minor resistance suggests that pull back from 1.3029 has completed at 1.2811 already. Intraday bias is turned back to the upside for 1.3029/47 resistance zone. Decisive break there will extend the larger rally to 61.8% projection of 1.2108 to 1.3047 from 1.2588 at 1.3168 next. On the downside, sustained break of 1.2811 and 55 day EMA will dampen our bullish view and turn bias back to the downside for 1.2588 support instead.

In the bigger picture, overall, price actions from 1.1946 medium term low are seen as a corrective pattern that is still in progress. While further upside is now in favor, overall outlook remains bearish as long as 1.3444 key resistance holds. Larger down trend from 1.7190 is expected to resume later after the correction completes. And break of 1.2588 will indicate that such down trend is resuming.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | RICS House Price Balance Jun | 7% | 15% | 17% | |

| 01:00 | AUD | Consumer Inflation Expectation Jul | 4.40% | 3.60% | ||

| 03:22 | CNY | Trade Balance (USD) Jun | 42.8B | 43.2B | 40.8B | |

| 03:22 | CNY | Trade Balance (CNY) Jun | 294B | 273B | 282B | |

| 06:00 | EUR | German CPI M/M Jun F | 0.20% | 0.20% | 0.20% | |

| 06:00 | EUR | German CPI Y/Y Jun F | 1.60% | 1.60% | 1.60% | |

| 07:15 | CHF | Producer & Import Prices M/M Jun | -0.10% | 0.00% | -0.30% | |

| 07:15 | CHF | Producer & Import Prices Y/Y Jun | -0.10% | 0.00% | 0.10% | |

| 12:30 | CAD | New Housing Price Index M/M May | 0.70% | 0.20% | 0.80% | |

| 12:30 | USD | PPI M/M Jun | 0.10% | 0.00% | 0.00% | |

| 12:30 | USD | PPI Y/Y Jun | 2.00% | 1.90% | 2.40% | |

| 12:30 | USD | PPI Core M/M Jun | 0.10% | 0.20% | 0.30% | |

| 12:30 | USD | PPI Core Y/Y Jun | 1.90% | 2.00% | 2.10% | |

| 12:30 | USD | Initial Jobless Claims (JUL 08) | 247K | 245k | 248k | 250K |

| 14:00 | USD | Fed Chair Yellen Testifies Before Senate Banking Panel | ||||

| 14:30 | USD | Natural Gas Storage | 72 | |||

| 18:00 | USD | Monthly Budget Statement Jun | -16.2B | -88.4B |

USD/CHF Breakout Attempt, USD/CAD Undecided ahead US Numbers, EUR/JPY Challenging Crucial Support Area

USD/CHF Breakout Attempt

The currency pair is trading in the green ahead the US figures, we'll see how will react after the numbers will be released. We'll have a high volatility later, after the US data, that's why you should be careful not to suffer a heavy loss.

We have a rebound on the USD/CHF, but a further increase will come only if will have enough energy to take out an important dynamic resistance. The greenback needs support from the US economy today so we can take the lead on the short term. USDX moves sideways on the short term, right above the 95.45 previous low, an accumulation movement will bring another leg higher, but right now is premature to say what will happen because the fundamental factors could ruin everything.

Price bounced back from the outside sliding line (sl) and now is pressuring the inside sliding parallel line (sl), only a valid breakout above this level will attract more buyers on the short term. Remains under selling pressure on the Daily chart as long as is trading within the descending pitchfork's body.

Is somehow expected to decrease further after the breakdown below the ascending sliding line (SL), major support could be found at the 0.9498 and lower at the 0.9440 level. USD/CHF moves sideways on the long term, is trapped within an extended range, the corrective phase could end soon if the behavior will change (if will make higher lows).

Is better to stay away from this pair because we don't have trading opportunity, the perspective remains bearish, personally I'll wait for a reversal sign, hoping to catch an upside movement right from the bottom.

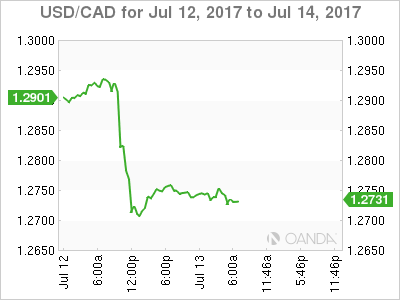

USD/CAD Undecided ahead US Numbers

The Loonie appreciated versus the USD in the morning, but now has lost some ground versus its major rival, we'll see what the US data will bring. We may have some volatility in the upcoming hours, you should keep an eye on the economic calendar later to see what will move the price.

Price dropped more than 230 pips in the yesterday's session after the BOC decision to hike the interest rate with 0.25% for the first time in the last 7 years. USD/CAD plunged much below the lower median line (LML) of the major descending pitchfork and found support only at the 1.2678 static obstacle.

The pair squeezed and closed much above the 1.2678 level and above the third warning line (wl3) of the former ascending pitchfork, a rebound could come only after the breakout above the median line (ml) of the minor descending pitchfork.

EUR/JPY Challenging Crucial Support Area

EUR/JPY is into a corrective phase and is pressuring an important support level, maintains a bullish perspective as long as is located somewhere above the 128.50 psychological level.

We had a breakdown below the upper median line (UML) of the major ascending pitchfork today, but this could be a false one and the rate will increase again. Has retested also the 38.2% retracement level and the median line (ml) of the ascending pitchfork. The outlook is bullish as long as is trading above these levels, because a breakdown below this confluence wil accelerate the sell-off.

USDJPY: Remains Bearish With Eyes On More Downside Pressure

USDJPY: The pair continues to retain its downside pressure on correction. On the downside, support comes in at the 113.00 level where a break if seen will aim at the 112.50 level. A cut through here will turn focus to the 112.00 level and possibly lower towards the 111.50 level. Its daily RSI bearish and pointing lower supporting this view. On the upside, resistance resides at the 113.50 level. Further out, we envisage a possible move towards the 114.00 level. Further out, resistance resides at the 114.50 level with a turn above here aiming at the 115.00 level. On the whole, USDJPY looks to pullback on price rejection.

Markets Bracing for Second Round of Yellen’s Testimony

Equity bulls received a shot in the arm while the Dollar was under pressure after Janet Yellen caught markets unaware by striking a dovish tone in her congressional testimony on Wednesday. Although Yellen reiterated the Federal Reserve's game plan to continue gradually tightening monetary policy, the lack of commitment to a hiking timeline and tone of caution, prompted investors to offload the Greenback. A key take away from the first round of the testimony was concerns raised over softening inflation, which may encourage market participants to re-evaluate the pace of monetary tightening this year.

With no fresh clues offered on the timings and magnitude of the balance sheet reduction on Wednesday, markets will closely scrutinize Yellen's second appearance today for clarity. If doves make an appearance once again and nothing new is brought to the table, the Dollar is likely to find itself under renewed selling pressure, as traders reduce their bets on an additional interest rate hike this year.

Sterling rescued by a BoE hawk

Sterling bulls were offered a helping hand during Thursday's trading session, as hawkish comments from BoE policy maker Ian McCafferty supported bets for higher UK interest rates. McCafferty was one of the hawks who voted for an interest rate increase last month and suggested that the central bank should consider unwinding its £435billion Quantitative Easing programme earlier than planned. Although the weak Dollar played a part in the GBPUSD's impressive appreciation on Thursday, price action suggests that Sterling is becoming increasingly sensitive to monetary policy expectations.

While speculations of the Bank of England tightening monetary policy may support prices in the short term, the fundamentals pressuring Sterling still remain intact. With Brexit uncertainty deteriorating economic fundamentals and political risk all weighing heavily on the British Pound, further downside may be on the cards. From a technical standpoint, the GBPUSD remains in a wide range on the daily charts. Bears still have some level of control below the tough 1.3000 resistance.

Commodity spotlight - Gold

Gold prices edged higher on Wednesday after Fed Chair Janet Yellen adopted a dovish stance in testimony before Congress. A vulnerable Dollar complimented the metals upside with prices hovering around $1220 at the time of writing. With Yellen's tone of caution prompting investors to trim their bets on another US rate increase this year, Gold, which is zero-yielding, was offered a lifeline. Although the metal remains heavily pressured on the daily charts, bulls could be given an opportunity to shine if Yellen doubles down on Wednesday's dovish remarks when she appears before Congress this afternoon. From a technical standpoint, repeated weakness below the $1240 resistance is likely to encourage a further decline back towards $1200.

CAC Slightly Higher, French Inflation Remains Listless

The CAC index has posted small gains in the Thursday session. Currently, the index is currently trading at 5247.30 and is up 0.49% on the day. In economic news, it's a quiet day. French Final CPI came in at a flat 0.0%, unchanged from the previous reading. Federal Reserve Chair Janet Yellen will testify before the Senate Banking Committee. On Friday, the eurozone releases Trade Balance, which is expected to show a surplus of EUR 20.3 billion. The US will publish CPI and retail sales reports.

Donald Trump is back in Europe, this time to visit France and take in Bastille Day with French President Emmanuel Macron. The new French President has started off his relationship with the unpredictable Trump on a solid footing, and Macron is eager to make France an important player on the global stage. The French government is also eager to take advantage of Britain's departure from the European Union. With large companies such as Deutsche Bank relocating their operations from London, France is making efforts to lure lucrative financial sector jobs which are leaving London. Earlier in the week, Prime Minister Edouard Philippe told a banking conference in Paris that he wants the city to become Europe's main financial hub after Brexit. This will be a tall order, as Frankfurt will likely be the most attractive choice for many large companies. Still, Philippe's comments underscore that France is looking for a bigger role on the international scene, and Brexit represents a unique political and economic opportunity for the French.

The Trump show is again on center stage in Washington, with more revelations about alleged secret ties between Russia and the Trump administration during the US election. This week's breaking news is that Donald Trump Jr. admitted that a Russian official contacted him and offered to provide him with evidence incriminating Hillary Clinton. Trump and the White House are trying to lower the flames and put a positive spin on the meeting, but the media and lawmakers (including Republicans) aren't about to let Trump off the hook. This crisis is just the latest miscue for the Trump administration, which hasn't been able to pass any significant laws through Congress, even though Republicans control both the House of Representatives and the Senate. The latest dark cloud over the White House has dampened investor confidence in the US economy, and European stock markets could take advantage of the latest political scandal in the US.

DAX Ticks Upwards As German CPI Matches Forecast

The DAX index has posted small gains in the Thursday session, as the index is up 0.26% on the day. Currently, the DAX is at 12,654.00. On the release front, German Final CPI improved to 0.2%, matching the estimate. In the US, it's a second day of testimony from Fed Chair Janet Yellen, who will speak before the Senate Banking Committee. On Friday, the eurozone releases Trade Balance, which is expected to show a surplus of EUR 20.3 billion. The US will publish CPI and retail sales reports.

The eurozone continues to struggle with low inflation, and although Germany's economy is in good shape, it has not been immune to chronically weak inflation levels. German Final CPI, a key gauge of consumer spending, improved to 0.2% in June, compared to -0.2% in May. CPI has managed just one reading above 0.2% in 2017, and earlier in the week, WPI came in at 0.0%, rebounding from a decline of 0.7% a month earlier. The ECB has set an inflation target of 2%, but German and eurozone inflation numbers remain well below that threshold. Although the eurozone economy has shown some improvement, there is no indication that inflation levels will move higher anytime soon, so we're unlikely to see the cautious ECB taper its aggressive stimulus package in the coming months.

Janet Yellen's testimony in front of a congressional committee was largely a non-event, as Yellen opted to repeat what we've been hearing from other Fed policy makers. Yellen reiterated that the Fed planned to raise rates “gradually”, and added that the Fed would begin trimming its balance sheet before the end of the year. The Fed chair was careful not to provide any timelines, but many analysts are circling September for a balance sheet reduction, with a rate hike to follow in December. However, despite Yellen's assurances, the markets remain lukewarm about a rate hike before the end of the year. Investors are concerned that the US economy has slowed down in 2017 and that inflation levels have not improved, despite the Fed arguing that the factors weighing on inflation are temporary. The CME Group has pegged a December rate increase at just 47%, while other forecasts are pointing to odds as low as 40%. Hints from the Fed will not suffice to bring investors on board – unless growth and inflation numbers move higher, the markets are likely to remain lukewarm about the likelihood of a third rate hike in 2017.

As if the markets don't have enough to worry about, the Trump administration's alleged ties with Russia are once again front-page news. This week, Washington is abuzz that Donald Trump Jr. admitted that a Russian official contacted him and offered to provide him with evidence incriminating Hillary Clinton. Predictably, the White House has attacked the media and is trying to distance itself from Trump Jr.'s meeting, but the miscue is one more example of the White House having to shift to damage control mode, rather than focus on its agenda. Trump hasn't been able to pass health care or other legislation through Congress, even though Republicans control both the House of Representatives and the Senate. The latest dark cloud over the White House has dampened investor confidence, and it's a safe bet that this latest crisis is not the last.

Rate Differentials Pack A High Yielding Punch

Thursday July 13: Five things the markets are talking about

As expected, Central Bank action and rhetoric is keeping capital markets on their toes.

In her testimony to Congress yesterday, Fed chair Yellen said that there is no rush to tighten monetary policy as inflation remains consistently 'below' target.

The Fed expects the U.S economy to continue to develop in the current direction, which will grant policy makers' room for 'gradual' rate hikes and that reduction in the balance sheet is likely to begin this year.

The market interpreted her comments as ‘less hawkish' - this has allowed U.S Treasuries to rally, the dollar to underperform vs. G10, and U.S equities to print fresh record highs.

Her counterpart at the Bank of Canada (BoC), Governor Poloz raised interest rates by +0.25% to +0.75% as widely expected, the loonie, however, gained +1.5% outright to record a new yearly high (C$1.2695) as his statement and comments were perceived as being more ‘hawkish.'

The Governor cited 'robust' economic activity that's led to a 'significant amount' of economic slack disappearing. It now expects the output gap to fully close before the end of 2017, versus a previous forecast of during H1 2018.

As for future rate moves, BoC said adjustments to be guided by data-which has been strong of late-although adding it will keep in mind continued uncertainty posed by the Trump administration's trade policy, and issues related to record levels of household debt and frothy real estate.

1. Stocks get a boost from dovish comments

U.S stocks took heart from Ms. Yellen's speech indicating a slower rate of hikes, as stocks across the board rallied with the Dow reaching a new all-time high and close.

In Japan, equities ended flat overnight, as gains in tech shares offset weakness in financial stocks after U.S yields slipped. The Nikkei closed +0.01% higher, while the broader Topix ended down -0.01%.

In Hong Kong, the Hang Seng Index climbed +1.1% to its highest level in two-years.

In China, stocks also firmed, with the blue-chip index closing at an 18-month high, supported by solid trade data. The blue-chip CSI300 index rose +0.8%, while the Shanghai Composite Index gained +0.6%.

Note: China exports rose +11.3% in June y/y, while imports expanded +17.2%, which suggests their economy is holding up, supported by global demand.

Elsewhere, Australia's S&P/ASX 200 Index strengthened +1.1% on the back of China's data, while in South Korea the Kospi rallied +0.7% when the Bank of Korea (BoK) held steady its benchmark rate, as expected.

In Europe, indices opened flat, but have moved higher ahead of the U.S open. Ms. Yellen is to continue speaking today and attention is also turning to the first reports of earning season.

U.S stocks are set to open in the black (+0.2%).

Indices: Stoxx50 +0.5% at 3,539, FTSE +0.1% at 7,424, DAX +0.4% at 12,678, CAC-40 +0.7% at 5,259, IBEX-35 +1.0% at 10,671, FTSE MIB +0.4% at 21,524, SMI +0.4% at 9,049, S&P futures +0.2%

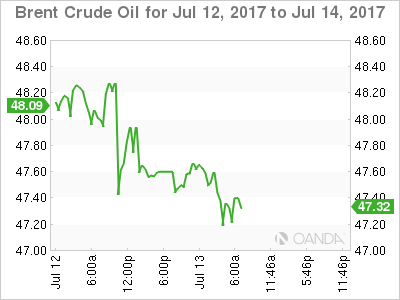

2. OPEC compliance with oil cuts falls to 6-month low, gold stable

Oil prices are again under pressure on worries about oversupply as the IEA this morning warned that a long-awaited market rebalancing could be delayed due to weak compliance with production cuts among OPEC members.

In its monthly report the IEA has issued a stronger outlook for global oil demand, however, with consumption in Germany and the United States increasing in recent months.

The report also noted a dramatic recovery in oil production from Libya and Nigeria and a lower rate of compliance by OPEC with its own output agreement.

Brent crude fell -34c to +$47.40 a barrel, while U.S light crude (WTI) is down -32c at +$45.17.

Note: Oil prices have dropped recently to levels not seen in 18-months as the market loses faith in a deal between OPEC and non-OPEC producers to reduce output, while U.S. shale oil production rises.

Gold prices (+0.2% to +$1,222.99 an ounce, a fourth day of gains) are holding steady ahead of the U.S open, as the Fed seems set to only gradually tighten monetary policy, curbing speculation that interest rates would rise more than once this year.

3. Yields fall on Yellen's comments

Similar to equities, bond prices have got a lift as the Fed's Yellen sounded caution on inflation.

Prior to Yellen's comments yesterday, global yields had been backing up, spooked by what seemed a collusion effort by top central banks about tightening monetary policy.

Fed fund futures are now only pricing a 50-50 chance of a rise by December.

U.S Treasuries have rallied in reaction, clawing back a third of their selloff with yields on two-year notes falling to three-week lows, while U.S 10's is down another -1 bps overnight at +2.32%.

Germany's benchmark 10-year Bund yield is flat, trading atop of its psychological +0.5% and has now given back a quarter of the rise triggered by last month's hint from ECB's Draghi that it was readying to scale back stimulus.

Elsewhere, the yield on Aussie 10-year notes has dropped -3 bps to +2.69%.

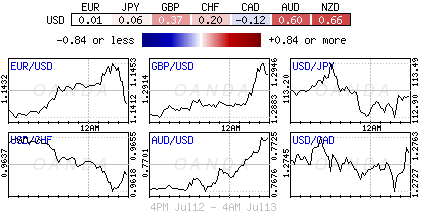

4. Dollar underperforms across the board

The ‘mighty' dollar has fallen broadly after Ms. Yellen's comments were perceived as 'dovish' and potentially dampening the outlook for future interest rate rises.

Currently, the EUR trades up +0.2% at €1.1423, while sterling is up +0.3% at £1.2928 and the loonie is holding steady at C$1.2732 after gaining +1.5% intraday yesterday. There was a lot of interest from Europe to own CAD on the crosses, especially against EUR (€1.4516) and GBP (£1.6446).

Higher-yielding currencies have been the strongest performers, as carry traders return to take advantage of the rate differential however, with the AUD rising +0.6% to a 16-week peak of A$0.7728 and the NZD up +0.75% at NZ$0.7340. Also supporting the antipodeans is the stronger than expected Chinese trade data showing strong imports.

5. Germany's June inflation numbers

Data this morning from Germany's statistics office confirmed last month's inflation figures - prices grew by +0.2% m/m and +1.6% on the year.

Note: In harmonized European terms, the price gain was +0.2% and +1.5% respectively.

Digging deeper, the data showed that energy prices were stable year-to-date in national terms, while food prices were up +2.8%. Ex-food and energy, prices grew by +1.6% on the year.

Among key categories, package holidays saw the sharpest annual gain, growing by +5.6%, while on the flip side, gas and vegetables both declined by -3.2% on the year.

Yields And USD Fall Ahead Of Yellen’s Second Testimony

- Yellen's dovish admission on rates weighs on USD and yields;

- Fed speakers and US data also on the agenda today.

US equity markets are expected to open higher again on Thursday as we await Federal Reserve Chair Janet Yellen's second day of testimony, this time in front of the Senate Banking Committee.

As is often the case with these hearings, the vast majority of what was said had very little impact on the broader markets, with lawmakers drifting repeatedly onto more political topics and Yellen giving very little away on the Fed's monetary policy position that isn't already known. Yellen's admission that rate increases will be gradual though – not a new revelation in itself – while highlighting persistent subdued inflation and low neutral rate, suggested that the pace of tightening next year and beyond may well be slower, with focus likely shifting to balance sheet reduction.

While many may have expected this to be the case prior to this, Yellen's acknowledgement of this potentially signals a slight shift in the Fed's rate outlook later this year, once the central bank unveils its plans to begin the process of reducing its bond purchases. In this moderate growth and low inflation environment, this comes as a relief to investors and therefore provided a temporary boost for equities. The question now is whether Yellen reiterates the point in today's testimony, adds further colour to it or possibly backtracks on it.

Following Yellen's slightly dovish testimony, the dollar has come off a little to trade near nine month lows as bond yields have also ticked a little lower. With central banks elsewhere only likely to pick up the pace, the US dollar may remain under some pressure for the foreseeable future. The Bank of Canada this week raised interest rates and the ECB could signal its intentions to continue to reduce its bond buying next week while the Bank of England may not be far behind on tightening.

Fed policy makers Charles Evans and Lael Brainard will also be appearing on Thursday, which could also grab some attention, with both being voters on the FOMC this year. We'll also get some economic data from the US, including jobless claims and PPI inflation figures, although tomorrow's retail sales and CPI inflation data is what traders will be primarily focus on, on that fro

Market Update – European Session: European Indices Extend Gains As Bond Yields Drop, Daimler Drops On Excess Emissions Report

Notes/Observations

European Equities continuing to rise following strong gains yesterday, as European Bond Yields retreat

OPEC compliance with oil cuts falls to 6 month low

Daimler shares fall after on report it cheated on Diesel emissions tests

Overnight

Asia:

Korea';s Kospi rose nearly 1% after BOK left rates on hold but did raise its outlook for 2017 GDP

China H1 trade balance in yuan terms fall 17.7% y/y to CNY1.28T; in dollar terms June trade was $42.8B, in line with expectations. Trade with the US in dollar terms was at its highest level since October 2015 at $25.4B

(JP) Bank of Japan (BOJ) reportedly intends to raise growth outlook for FY17-18 by 0.1-0.2% at policy meeting next week

Europe:

BOE's McCafferty (hawkish dissenter): BOE should consider unwinding £435B QE program earlier than planned, plans to vote for a 25bp hike again in August

UK to publish the Repeal Bill a key Brexit law, which is central to the government's plan to exit the EU in 2019

Germany, France and Spain confirm final CPI readings, whilst Sweden reported slightly stronger CPI for June

BOE Credit conditions survey saw availability of mortgage lending falling this Quarter

Americas

Fed's George (hawk, non-voter): favors starting balance sheet reduction in the near future, current asset valuations, low volatility may signal financial market complacency

Oil

IEA Monthly report: Expects 2017 Global demand to grow 1.5% to 98M b/d

Global oil supply increased by 720K b/d in June to 97.46M b/d

OPEC Compliance with cuts slips from 95% in May to 78% in June, lowest in 6 months

Economic Data

(SE) SWEDEN JUN CPI M/M: 0.1% V 0.0%E; Y/Y: 1.7% V 1.6%E

(DE) GERMANY JUN FINAL CPI M/M: 0.2% V 0.2%E; Y/Y: 1.6% V 1.6%E

(FR) FRANCE JUN FINAL CPI M/M: 0.0% V 0.0%E; Y/Y: 0.7% V 0.7%E

(ES) SPAIN JUN FINAL CPI M/M: 0.0% V 0.0%E; Y/Y: 1.5% V 1.5%E

(TR) Turkey May Current Account: -$5.2B v -$5.0Be

Fixed Income Issuance:

(IT) ITALY DEBT AGENCY (TESORO) SELLS TOTAL €2.0B VS. €1.5-2.0B INDICATED RANGE IN 2033 AND 2037 BTP BONDS

(IE) IRELAND DEBT AGENCY (NTMA) SELLS TOTAL €0.75B VS. €0.75B INDICATED IN 2022 AND 2045 IGB BONDS

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx50 +0.5% at 3,539, FTSE +0.1% at 7,424, DAX +0.4% at 12,678, CAC-40 +0.7% at 5,259, IBEX-35 +1.0% at 10,671, FTSE MIB +0.4% at 21,524, SMI +0.4% at 9,049, S&P futures +0.2%]

Market Focal Points/Key Themes: European indices opened flat or slightly down, but moved higher as the session progressed; trend following comments from Fed Chair Yellen seen not in a rush to raise rates; oil helped performance among energy stocks Metro's spinoffs debuted in trading; French press revived speculation that Alstrom was considering buying Siemens' train business; Yellen to continue speaking today; attention now turning to the first reports of earning season; upcoming US earnings include Delta Airlines and Emmis Communications

Equities

Consumer discretionary [Casino CO.FR +3.9% (earnings), Asos ASC.UK -2.4% (earnings), Game Digital GMD.UK +9.3% (SD takes stake), N Brown BWNG.UK -8.1% (cost evaluation)]

Consumer staples [Koninklijke Wessanen KWZ2.DE -3.1% (analyst action)]

Energy [Premier Oil PMO.UK -2.4% (production update)]

Financials [Partners Group PGHN.CH +3.4% (results)]

Healthcare [Astrazeneca AZN.UK -4.5% (CEO approached by Teva), Oxford Biomedica OXB.UK +6.9% (receives approval)]

Industrials [Alstom ALO.FR +2.7% (earnings), Daimler DAI.DE -0.5% (under investigation), Kvaerner KVAR.NO +3.7% (results)]

Speakers

(UK) Trade Sec Fox: UK will look at bridging mechanism if needed for Brexit

(RU) Russia Central Bank (CBR) Gov Nabiullina: Russia must stick to free-floating rouble policy

Currencies

GBPUSD continues to grind higher bouncing off yesterday morning lows, dealers note resistance stands at 1.2980. The bounce in Sterling has also helped EURGBP ease, dropping below yesterday low, with next support seen at 0.8815.

EURSEK trades sharply lower after strong Swedish inflation readings with the cross dropping below 9.55 from ~9.61 prior to the release. The pair trades at a 10 week low with near term support seen at 9.505

Fixed Income

Bund futures trade at 161.62 up 22 ticks as volume rises and stops are taken out. Resistance lies near the 162.10 level followed by 162.75. A break of the 160.00 support level could see lows target 159.25 followed by 157.50.

Gilt futures trade at 125.87 higher by 23 ticks and back towards the July 4th highs. Price finds key support at the 124.42 support level. An acceleration lower could test the 122.88 region. Resistance remains the noted 126.00 region, followed by 126.72.

Thursday';s liquidity report showed Wednesday';s excess liquidity fell to €1.667T a drop of €3B from €1.670T prior. Use of the marginal lending facility fell to €214M from €258M prior.

Corporate issuance saw $2B come to market via 3 issuers headlines by Cencosud $1B unsecured senior offering and PTT Exploration and Production $0.5B notes offering

Looking Ahead

05:30 (ZA) South Africa May Total Mining Production M/M: 1.0%e v -1.6% prior; Y/Y: 2.2%e v 1.7% prior

08:00 (BR) Brazil May IBGE Services Sector Volume Y/Y: -1.8%e v -5.6% prior

08:15 (UK) Baltic Dry Index

08:30 (US) Jun Final Demand PPI M/M: 0.0%e v 0.0% prior; Y/Y: 1.9%e v 2.4% prior

08:30 (US) Initial Jobless Claims: 245Ke v 248K prior; Continuing Claims: 1.950 v 1.956M prior

08:30 (US) Weekly USDA Net Export Sales

08:30 (CA) Canada May New Housing Price Index M/M: 0.3%e v 0.8% prior; Y/Y: 3.5%e v 3.8% prior

09:00 (RU) Russia Gold and Forex Reserve w/e July 7th : No est v $412.2B prior

10:30 (US) Weekly EIA Natural Gas Inventories

14:00 (US) Jun Monthly Budget Statement: -$35.0Be v -$88.4B prior

XAU/USD Analysis: Touches 1,226 Level

As Janet Yellen began giving her testimony on Wednesday, the yellow metal’s price jumped. During the move the commodity price broke out of the ascending channel pattern. However, as the chairwoman ended the speech, the metal had retreated back to the 1,220 level. Moreover, something unordinary was happening on Thursday morning. Although theoretically the pattern is broken, the upper trend line of the ascending channel was still providing resistance to the commodity. Meanwhile, the 200-hour SMA and the monthly S1 were providing support to the metal. Due to that reason it can be expected that additional gains will be scored by the end of the week.