Sample Category Title

Trade Idea Wrap-up: EUR/USD – Buy at 1.1335

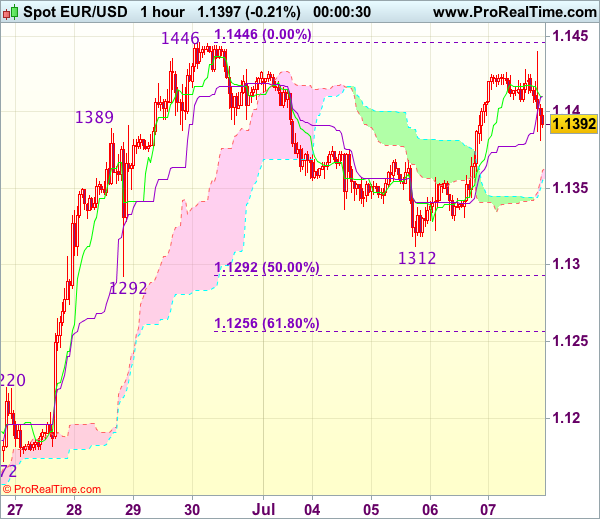

EUR/USD - 1.1401

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.1410

Kijun-Sen level : 1.1410

Ichimoku cloud top : 1.1365

Ichimoku cloud bottom : 1.1359

Original strategy :

Buy at 1.1335, Target: 1.1440, Stop: 1.1300

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.1335, Target: 1.1440, Stop: 1.1300

Position : -

Target : -

Stop : -

Remark: Due to holidays, update will resume on 19 July 2017.

As the single currency has retreated after faltering below resistance at 1.1446, suggesting consolidation below this level would be seen and pullback to 1.1355-60 cannot be ruled out, however, reckon support at 1.1312 would limit downside and bring another rise later, above said last week’s high at 1.1446 would confirm recent upmove has resumed for headway to 1.1475-80 but price should falter below 1.1500.

In view of this, we are looking to buy euro on dips but one should exit on subsequent rally. Below said support at 1.1312 would abort and signal top has been formed at 1.1446, bring retracement of recent rise to 1.1292 (previous support as well as 50% Fibonacci retracement of 1.1139-1.1446), then towards 1.1270.

Trade Idea Wrap-up: USD/JPY – Stand aside

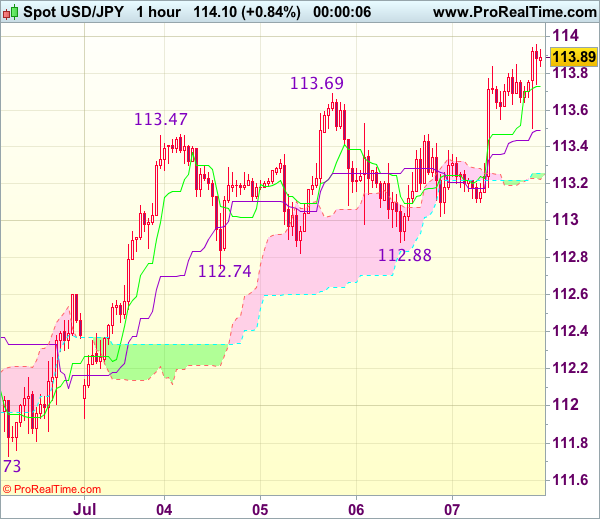

USD/JPY - 113.89

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 113.73

Kijun-Sen level : 113.49

Ichimoku cloud top : 113.26

Ichimoku cloud bottom : 113.23

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Remark: Due to holidays, update will resume on 19 July 2017.

Although the greenback has risen again and broke above resistance at 113.69 and initial upside risk remains for recent upmove to extend gain to 114.00, loss of momentum should prevent sharp move beyond 114.25-30 and reckon 114.50-55 would hold from here, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to stand aside in the meantime. Below the Kijun-Sen (now at 113.49) would bring pullback to 113.10-15 but only break of support at 112.74-88 would signal top is formed, bring correction of recent rise to 112.60, then 112.40.

Yellen’s Testimony, BoC Rate Decision, Key Data in Focus

Next week's market movers

- In the US, we have Fed Chair Yellen's semi-annual testimony before Congress. Market participants may look for hints with regards to B/S normalization and the timing of the next rate increase.

- We expect the BoC to remain on hold, despite the latest hawkish remarks that a hike may come sooner than previously anticipated.

- We also get key economic data from China, Norway, Sweden, the UK, and the US.

On Monday, during the Asian morning, China's CPI and PPI for June are due to be released. The forecast is for both rates to have remained unchanged. Our own view is that there is the possibility for upside surprises in both prints. We base this on the nation's official manufacturing PMI for the month, the price components of which both increased for the first time since December.

During the European day, we get Norway's CPI data for June, though no forecast is available yet. Despite the steep slowdown in inflation, at its latest meeting the Norges Bank removed its easing bias and noted that it now expects the key policy rate to remain at the current level, while it revised slightly higher its expected rate path for 2017 and 2018. What's more, the Bank noted that inflation is lower than expected and may continue to drift lower in the months ahead, but increased activity and receding unemployment suggest that inflation will pick up. Therefore, even if inflation slows again, it may not be particularly worrisome for policymakers, as it would still be in line with the Bank's outlook.

On Tuesday, we don't have any major events or indicators on the agenda.

On Wednesday, the market will turn its attention to the Bank of Canada rate decision. At its latest meeting, the Bank kept its policy unchanged, while the tone of the meeting was neutral overall, indicating that although uncertainties continue to cloud the Canadian outlook, the economy's adjustment to lower oil prices is almost complete and recent economic data such as business investment have been encouraging. A few weeks after that gathering, BoC Deputy Governor Wilkins indicated that the Bank will start assessing whether all of the monetary stimulus currently in place is still required, while at last week's ECB forum on Central Banking, Governor Poloz said that low interest rates have "done their job".

Although the Governor did not comment on future policy plans, the market has started recalibrating its expectations with regards to the Bank's next move. Before we get any comments from these two key officials, the implied probability for a hike at the July meeting was resting near 0%. However, at the time of writing, - according to Canada's Overnight Index Swaps - more than half of market participants expect the Bank to lift interest rates for the first time in 7 years next week.

Indeed, recent economic data have been encouraging. Economic growth was impressive in Q1, while April's mom data showed that the economy entered Q2 on a decent footing. The stellar retail sales for April and the strong employment reports for April, May and June enhance that view. Having said that though, we don't share the view of those who expect a rate increase next week. Yes, we have strong signals that a hike may come sooner than previously anticipated, but given how fast the core CPI rate has been falling in recent months, we doubt that this will happen next week. Conditional upon further improvement in economic data and a rebound in underlying inflationary pressures, we believe that policymakers may choose the last quarter of the year for raising borrowing costs.

In the US, the main event will be Fed Chair Yellen's semi-annual testimony on monetary policy before the House of Representatives Financial Services Committee of Congress. She will address the same testimony before the Senate Banking Committee on Thursday. Usually the Fed's semi-annual monetary policy report is released on the day Yellen testifies, but this time around the report will be published a few days earlier, specifically later today. As such, we don't expect any major market reaction as she presents the report. Nevertheless, market participants may pay extra attention to the Q&A session. In particular, they may be on the lookout for any fresh signals with regards to balance sheet normalization and the timing of the next rate increase. Having said that though, we believe that what will play the biggest role in market expectations with regards to the Fed's future plans are the nation's CPIs due out on Friday.

As for the indicators, we get UK employment data for May, though no forecast is available yet. Our own view is that the unemployment rate likely remained unchanged, while average weekly earnings may have risen at the same pace as previously, with risks skewed towards an acceleration. The nation's services PMI for May indicated that the rate of employment growth across the sector was little changed since April, and that the reported rise in input prices was partly attributed to higher staff salaries. Considering that the service-sector accounts for roughly 80% of the nation's GDP, we consider it a decent gauge of the overall economy. However, we see it very unlikely for the wage growth rate to overcome May's inflation rate of 2.9%, so the UK is likely to experience negative real wages for the 4th consecutive month. In fact, real wages are accelerating to the downside, something that raises concerns over household spending.

On Thursday, during the Asian morning, China's trade balance for June is due to be released and expectations are for the nation's trade surplus to have increased. Exports are forecast to have risen at the same pace as the previous month, while imports are expected to have slowed. Our own view is that the risks surrounding both figures are tilted to the upside. The official manufacturing PMI suggested stronger foreign demand during the month, with new export orders increasing by a larger margin than overall new orders, while the import index rose to a four-month high.

During the European session, we have Sweden's CPIs for June, but no forecast is available yet. At its latest policy meeting, the Bank noted that inflation has recently been slightly higher than expected and that the risks of setbacks abroad are thought to have decreased, which makes it less likely than before for the repo rate to be cut in the near term. Nevertheless, officials clearly pointed out that this does not rule out any further cuts in the period ahead. The Executive Board remains prepared to implement further monetary policy easing if necessary to stabilize inflation and safeguard its target. Having all these in mind, we believe that CPI data could be of major importance for investors as an increase in underlying inflation pressures may revive speculation that the Riksbank is likely to remove its interest rate easing bias soon, following in the footsteps of the Norges Bank and the ECB.

Finally on Friday, we get US CPI and retail sales data, both for June. Getting the ball rolling with the CPIs, the headline rate is expected to have slid for the 4th consecutive month, while the core rate is anticipated to have held steady after falling for four months in a row as well. Given the latest tumble in the yearly change of oil prices, we do not expect the decline in the headline rate to be particularly worrisome. We believe that investors will have their gaze locked on the core rate. The price sub-index of the ISM manufacturing PMI showed that prices continued to increase, but at a slower pace than the previous month, while the respective sub-index of the non-manufacturing PMI showed a rebound in prices after recording a decline in May. These mixed signals support somewhat the case of an unchanged core CPI rate, which is unlikely to clear the picture with regards to the Fed's future plans. A decent rebound is needed to increase the probability for another rate increase by the end of this year.

As for the US retail sales, the forecast is for both the headline and core rates to have rebounded from the previous month. The consensus for a rebound is supported by both the Conference Board and U of M consumer sentiment indices for the month, both of which rose. A rebound in sales combined with the better-than-expected ISM PMIs and the decent employment report, all for June, may be early signals that the US economy ended the second quarter on a solid footing. This may confirm those who viewed the latest softness in US data as transitory.

Fed Minutes Leave Markets Hopeless

- Global bond rally threatens EM - Peter Rosenstreich

- Fed Minutes Leave Markets Hopeless - Arnaud Masset

- Switzerland Retail Sales Declined Less Than Expected - Yann Quelenn

- "Vice" Stocks

Economics - Global Bond Rally Threatens EM

Developed markets bond yields continue to rally, slowing investors rush into EM assets. Banks and data from ETFs are reporting the slowest EM inflows since the start of 2017. With rates driving currencies, last week saw steady depreciation in most EM currencies against G10. High beta currencies like TRY, RUB and ZAR lost over 2% as yields differentials widened. The root cause is the growing expectations of policy regime shift in central banks. Led by the Fed, ECB and BoE investors can finally see a light, abet distant, at the end of the ultra-accommodating monetary policy tunnel which dominated the last 10 years. In the FOMC meeting minutes members continued to highlight that a combination of interest rate hikes and reduction of balance sheet will utilized to prevent the economy from overheating. At the ECB Draghi attempted to back track from his hawkish comments, yet optimistic economic outlook suggests that the days of emergency measures in Europe are numbered. So far, the shift out of EM has been orderly yet as we have seen with the taper tantrum, sentiment can change in a moment.

Lower oil prices and protectionisms Trump behaviors towards China has once again put the spotlight on Mexico. Banxico meeting minutes signaled a cautious stance towards policy setting. Inflation outlook remains skewed to the upside, which is problematic for the central bank that would like to pause hiking cycle with overnight rate at 7.00%. With the Mexican economy mired down in weak oil prices, soft consumer demand and stalled industrial production, higher funding cost would not help. Annual consumer price inflations has gone ballistic now standing at 6.15% from 2% in December. Markets are already expecting a reversal and have two cuts priced in for the end of 2018. Yet in the short term this feel optimistic. Baring orderly rise in US yields, break down in Pena Nieto & Trump communication or a panic exodus from EM, MXN should continue to rally.

USDMXN bearish monument should continue with a test of near term support at 17.80.

Economics - Fed Minutes Leave Markets Hopeless

Beside the start of the G20 meeting in Hamburg, the release of the June FOMC meeting minutes was the highlight of last week. Investors were impatiently waiting for clues about the Fed's thinking and expectations were quite high. There was considerable disappointment when they realised that the minutes showed a highly-divided committee, increasing the overall uncertainty about the timing of the next interest rate hike and the beginning of balance sheet unwinding programme.

The committee noticed that the labour market continued to strengthen together with the economic activity, the latter improving at a moderate pace though. FOMC members acknowledged both headline and core inflation measures came in below their anticipation but "viewed the recent softness in these price data as largely reflecting idiosyncratic factors" and added that it will have little bearing effect on the mediumterm. However, some participants appeared quite concerned about the downside risk in inflation and raised doubts about reaching the 2% target, suggesting that dissent started to appear within Fed presidents.

Regarding the asset-reduction plan, the minutes did provide clarity regarding the game plan and the timing of the announcement, revealing that several participants prefer to announce the start of the process within a couple of months, which puts the September meeting right in target. Indeed, we do not believe the Fed will do this at its July meeting.

We reiterate our view that the weakness in inflationary pressures that has emerged at the beginning of the year will force the Fed to slow down the pace of monetary tightening. Therefore, we expect only one other rate hike this year, most likely in December. We also anticipate that the Fed will wait until at least until September to announce the timing of the balance sheet reduction, which will most likely start at the earliest in the second half of 2018. However, given the disappointing reading in average hourly earnings last Friday (2.5%y/y versus 2.6% exp. and a downwardly revised figure of 2.4% in the previous month), we won't be surprise should the Fed delay further the announcement.

Given the lack of new information provided by the minutes, the USD extended losses starting on Thursday. On Friday, EUR/USD was on its way to test the 1.1445 resistance.

Economics - Switzerland Retail Sales Declined Less Than Expected

The CHF is still trading below 1.10 against the single currency despite short-term bullish pressures on the pair. We believe that there are at the moment two major reasons that are pushing the euro against the Helvetic currency.

The French Presidential election and the start of the "Brexit" negotiations have removed - at least reduced - the political and geopolitical uncertainties, markets are clearly shifting towards risk-on and which is why we see the EURCHF pair moving up.

In addition, Mario Draghi's recent comments pushed the euro higher by stating that the Eurozone recovery is progressing and that the ECB monetary policy stance must accompany this recovery. Markets interpreted those declarations from the ECB as hawkish.

Overall, we may judge that the economic fundamentals of Switzerland are now better than what could have been expected after January 2015 despite the constant overvaluation of the CHF pushed by the extreme monetary policy of the European Central Bank. It has been now two years and a half since the removal from the floor and upside pressures on the Swiss franc are still strong.

For the time being, the situation looks under control. The trade balance remains largely positive, unemployment rate is still very low (3%) and the GDP growth, even though low is decent (Q1 at 0.3% q/q). The one major issue is inflation which is not picking up and this should, at some point, have a negative impact on growth. Hence, we may assess that the Swiss economy still has some room to resist, in case larger weaknesses of the single currency drive the CHF higher.

It is worth noting the CHF is valued under its political and economic stability rather than on its economic data. By the way markets barely reacted on the release of retail sales growth which came in negative for the 2nd month in a row at -0.3% y/y. Swiss safe haven status is what makes the country attractive and we see the EURCHF pair showing a short-term continued bullish move towards 1.1000.

The SNB must still hold tight to defend the Swiss franc but we are concerned about the level of FX reserves which continues their massive increase. This has enabled the Swiss central bank to become the eighth most important investor in the world with $80 billion dollar invested In the US market.

Themes Trading - "Vice" Stocks

Investing in vice (or "sin") companies isn't for everyone. But it has been shown to significantly outperform more conventional stocks. The economic rationale for investing in socially irresponsible companies is clear. "Politically incorrect" industries --such as alcohol, tobacco, gambling and military (heck, we'll even throw in fast food and big oil for good measure) --generally outperform in bull markets and are more resilient in bear markets. That's because earnings growth and dividend yields tend to remain stable, no matter what the state of the economy.

Many vice stocks even exhibit countercyclical behaviour, performing better as the economy worsens. Some people find this type of investment questionable for moral reasons. But make no mistake: this is big business with big opportunities. The US alcoholic-beverage market was worth a whopping $211.6 billion in 2016, with a growth rate of 7% between 2000 and 2016. This Theme will focus on companies that generate most of their revenue from alcohol, tobacco, guns, fast food, adult entertainment and gambling.

Dollar Makes Comeback on NFP Gain; Sterling Slips on Weak UK Manufacturing

There was a great amount of important economic data releases today. In the US, the key focus was on the non-farm payrolls jobs report, while the unemployment rate and average earnings growth were also of significant interest. Disappointing UK industrial and manufacturing production for May have been dictating sterling movements during the European trading session.

The much-anticipated jobs report today showed a gain of 222,000 jobs in the US economy for June, which followed a revised 152,000 expansion in May and beat forecasts for a gain of around 179,000 jobs. However, the wage growth came in below the expectations. Average hourly earnings increased by 0.2% month-on-month, following a downwardly revised 0.1% rise in May, but below the expected 0.3%. On a yearly basis, wages grew 2.5% in June. Meanwhile, the unemployment rate inched up to 4.4% from 4.3% in May.

The dollar market gave a mixed reaction against the yen, falling at first, but later gained ground and was testing the 114 handle. Markets might have gotten worried by the slower wage growth, which isn't generating substantial wage pressure and this could translate to lower inflation growth. However, a pickup in job additions seems to have instilled confidence into investors that the Fed will continue with its plan of another rate hike this year and for balance sheet reduction.

Sterling was one of the worst performing currencies against the greenback as it tumbled on a disappointing manufacturing production figure for May. UK manufacturing production fell 0.2% in May, month-on-month, coming in below the expected 0.5% and the prior month's 0.2% gain. Similarly, at a 0.1% decline, industrial output also disappointed, coming below the forecasted 0.4% gain. Pound/dollar fell a quarter of a percent following the release, last trading at $1.2875 as European markets were coming to a close. The figures were the latest in a string of weak numbers this week including a number of disappointing PMI numbers, pointing to a cooling economy and adding downward pressure on the pound.

The loonie leaped against the dollar on the figures pointing to a strong labor market in Canada. The upbeat data also adds to the speculation that the Bank of Canada could start tightening monetary policy as soon as next week during its planned policy meeting. At 45,300 there were far more job additions than expected (10K) in June, causing unemployment to dip. The unemployment rate was 6.5% in June, below the expected and the prior month's 6.6%. Dollar/loonie fell 0.66%, below the 1.29 level.

Looking at commodities, a stronger US currency deterred demand for gold that has fallen to a two-month low, reaching an intra-day low of $1,213.15 an ounce.

Pressure on oil prices unfolded for the third consecutive day, with WTI trading at $44.23 a barrel and Brent at $46.76. Investors remain doubtful that OPEC-led production cuts will clear a global supply glut.

Sterling Ceding Ground on Poor UK Data

- European equities traded modestly lower for most of the day, but the losses narrowed after the US payrolls. US equities are regaining ground after yesterday's setback. The Dow and the S&P show gains of about 0.3%. The Nasdaq outperforms (+ 0.7%)

- May UK data disappointed across the board today with industrial production (-0.1% M/M and -0.2Y/Y) and manufacturing production (-0.2% M/M and 0.4% Y/Y) both lower than the April numbers and the consensus. The UK trade deficit was also wider than expected.

- The US June payrolls report was strong with non-farm payrolls increasing strongly by 222K instead of the expected 178K rise. The May figures was revised upward from 138K to 152K. Average hourly earnings on the other hand disappointed with a rise of 0.2% M/M and 2.5% Y/Y (consensus 0.3% and 2.6% Y/Y).

- German industrial production rose more than anticipated, underpinning a strong and broad-based upswing in Europe's largest economy. Output, adjusted for seasonal swings and inflation, jumped 1.2% M/M in May (5.0% Y/Y) after rising a revised 0.7% M/M in April (2.8% Y/Y). Consensus forecasts were lower at 0.2% M/M and 4.0% Y/Y.

- Chinese President Xi Jinping took a swipe at the US for retreating from globalization at the G20, exposing the tensions before a meeting of world leaders divided over everything from trade and climate change to handling North Korea's provocations.

- ECB policy makers might be open to terminating the institution's purchases of asset-backed securities when they set the course for stimulus in 2018, according to three euro-area officials familiar with the matter. They added that the Governing Council members generally agree that the program missed the aim of reviving the ABS market.

Rates

Payrolls indecisive for core bonds

Market were eagerly awaiting the June US payrolls, but the report was mixed and didn't decisively affect the core bond markets. The payrolls and the average workweek were strong and higher than expected, suggesting buoyant activity, but the wage component (Average Hourly Earnings) disappointed once more and suggests there is no noticeable upward wage trend despite a tightening labour market. This means that core inflation will remain subdued for longer and that will lead to pressure on the Fed to tighten policy even slower. In this context, the T-Note future couldn't really choose a direction. After some minor volatility the T-Note settled near 125, the opening level. The picture is similar for the Bund which held its sideway range and trades modestly above opening levels too. The US equity future and EUR/USD didn't go far either.

At the time of writing, German yields decreased about 2 bps in the 2-to-5-year sector and were flat to up 1.1 bps in the 10-to-30-yr sector. The break of the key 0.50% yield resistance yesterday was confirmed. The US yield curve bear steepened slightly with yields up between flat (2-yr) and 2.3 bps (30-yr).

The labour market report showed the headcount was very strong with net job growth of 222K and an upward revision of the previous two reports by 47K. The lengthening of the average workweek to 34.5h (from 34.4) is also a positive sign on the health of the economy. Unemployment rose slightly to 3.4% from 3.3% due to a strong entrance of new jobseekers (361K) that surpassed the 245K new (household) jobs (the participation rate increased 0.1%-point to 62.8%). This is in fact also a positive factor. The only really negative element was the small 0.2% M/M (and 2.5% Y/Y) gain in average hourly earnings, which fell short of the 0.3% M/M and 2.6% Y/Y consensus expectation, while the May figure was revised lower to 0.1% M/M from 0.2% M/M previously.

Currencies

Dollar gains modestly on solid US payrolls

This morning, interest markets and the dollar shifted temporary in wait-and-see modus after yesterday's moves. The US payrolls were expected to decide on the next directional move. However, this wasn't the case. The global payrolls report was strong, but wages disappointed again. The dollar initially didn't know which way to go, but finally gained ground slightly. EUR/USD trades again near the 1.14 pivot. USD/JPY is nearing the 114 big figure.

Overnight, Asian equities joined the correction from WS yesterday, but the losses remained modest. The yen weakened further even as equities declined. Interest rate differentials widened further against the yen as core currencies (EMU/USD) rose. At the same time, the BOJ bought JGB's to prevent Japanese LT yields from following the rise in the US and Europe. USD/JPY set a new correction top and settled in the 113.55/85 area. EUR/JPY touched the 130 barrier early in Europe. EUR/USD also remained well bid (1.1420 area).

This morning, German May production data were very strong. They were however not able to extend yesterday's rise in European yields or in EUR/USD. Investors were reluctant to add positions ahead of the key US payrolls report. (European) yields settled near the ST top. EUR/USD held an extremely tight sideways range in the low 1.14 area.

The US June payrolls grew a strong and higher than expected 222K and the previous two months were revised higher by a total of 47K. The unemployment rate rose from 4.3% to 4.4%, but this was due to a rise in the labour force (higher participation rate). However, wage growth disappointed again at 0.2% M/M and 2.5% Y/Y (2.6% was expected). Despite the slight miss in wage growth, the report should be considered as strong, confirming the recovery in the US labour market. Even so, the reaction on the interest rate markets and of the dollar was hesitant, with no clear directional trend. After some nervous swings, the dollar finally gained ground slightly. EUR/USD came close to the 1.1445 reaction top, but a break didn't occur. The pair currently trades in the 1.1400 area. USD/JPY is setting a minor new top near the 114 barrier.

Sterling ceding ground on poor UK data

Earlier this week, sterling didn't react much to (slightly) weaker than expected data. Trade was mostly driven by technical considerations and by the price moves in the dollar or the euro. Today, there was a series of (not so important) UK eco data with the May production data, construction output, trade balance and Halifax House prices. All were weaker than expected but especially the miss in the production data was quite substantial. The data are raising new questions whether a BoE rate hike is appropriate in the near future. Sterling came under pressure after the data releases. EUR/GBP rebounded to the mid 0.8850 area. Cable dropped to the 1.29 area. The US payrolls had only a marginal impact on sterling trading. EUR/GBP now trades in the 0.8845 area while cable lost a few more tics on the USD rebound (1.2880 area).

Job Growth Signals Continued Growth and Fed Action

June job gains of 222,000 and a rise in wages indicate continued economic growth ahead and a basis for the Fed to continue its current policy path. Beyond the cycle, structural unemployment issues remain.

Jobs Up 222,000 in June: Consistent with Economic Growth

Nonfarm payrolls rose a strong 222,000 in June, with the three month average at 194,000 jobs. Monthly average job gains this year continue the moderating trend started in 2014 and are consistent with a tighter labor market and rising wages/salaries.

Hiring in the services sector remained solid, with gains in business services, education & health, finance and leisure & hospitality (top graph). The local government sector showed a strong gain in June - summer schools?

In the goods sector, manufacturing employment posted a small gain, while hiring in construction was up a solid 16,000 jobs, likely reflecting some seasonal improvement. Our outlook remains for a rebound in real GDP growth in Q2 and gains of roughly 2.5 percent to 3.0 percent for the second half of this year.

Wages: Not an Isolated Number but Part of the Economic System

Job gains, on average, continue to outpace the growth in the labor force, thereby putting downward pressure on the unemployment rate and modest upward pressure on wages.

Average hourly earnings rose 0.2 percent in June, putting the year-ago pace of wage growth at 2.5 percent. Despite continued steady job growth in 2017, earnings have yet to break out of this mid-two percent pace. The softer inflation readings and weak productivity numbers have limited the gains in nominal wage growth. On balance, average hourly and weekly earnings continue to improve and, along with more jobs, support the case for household income gains.

Over the longer run, wages reflect the economic fundamentals of the labor market, and those fundamentals include productivity and inflation (middle chart). During the current cycle, analysts have repeatedly commented on low productivity, while inflation has been persistently below the FOMC's target of two percent. With both productivity growth and inflation continuing to prove sluggish, it is not altogether surprising that wage growth has disappointed given the performance of the fundamentals.

Structural Problems Persist: Limits Growth

Long-term unemployment (bottom graph) remains higher than levels of the past 30 plus years, signaling a structural shift in the labor market. Recent articles on the opioid epidemic and the shift in behavior of young men towards playing videos games at home rather than work suggest a more structural problem of worker displacement than can be dealt with by monetary policy alone. The net result is a continued lower than expected labor force participation rate, slower than expected economic growth and a gradual rise in wages as employers chase increasingly rare skilled workers.

Trade Idea: EUR/GBP – Hold short entered at 0.8845

EUR/GBP - 0.8844

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term up

Original strategy :

Sold at 0.8845, Target: 0.8745, Stop: 0.8885

Position : - Short at 0.8845

Target : - 0.8745

Stop : - 0.8885

New strategy :

Hold short entered at 0.8845, Target: 0.8745, Stop: 0.8885

Position : - Short at 0.8845

Target : - 0.8745

Stop : - 0.8885

Remark: Due to holidays, next Trade Ideas update will be made on 19 July 2017.

Although the single currency has rebounded after finding support at 0.8756 and initial upside risk remains, as long as indicated resistance at 0.8882 (last week’s high) holds, further consolidation would be seen and prospect of another retreat remains, below said support at 0.8756 would add credence to our view that a temporary top is possibly formed at 0.8882, bring retracement of recent upmove to 0.8730-35, however, still reckon downside would be limited to 0.8719 support.

In view of this, we are holding on to our short position entered at 0.8845. Above 0.8882 would revive bullishness and extend recent upmove from 0.8304 low to 0.8900-10, having said that, as broad outlook remains consolidative, reckon current c leg of larger degree wave b should be limited to 0.8950 and price should falter well below 0.9000 psychological level.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

U.S. Labour Markets Still Solid in June

Highlights:

- Employment jumped 222k in June following upwardly revised increases in both May and April.

- Private employment rose 187k following a 159k increase in May. Public jobs jumped 35k led by higher employment at local governments — including a sizeable 14k jump in the education sector.

- The unemployment rate ticked up to 4.4% from the 4.3% cycle-low in May as labour force participation edged higher.

- Average hourly earnings rose 0.2% on a month-over-month basis and 2.5% from a year ago.

Our Take:

The 222k increase in employment in June was stronger than the ~180k expected ahead of the report, even more so including 47k worth of upward revisions to the prior two months. The unemployment rate ticked higher but only because of a 361k jump in the labour force that partially retraced a large decline in May. The 4.4% unemployment rate is still below the 4.6% the Federal Reserve views as consistent with full employment in the long-run. Unemployment is down half a percent from a year ago and double that when including sources of 'hidden unemployment' like discouraged workers. Wage growth has moderated somewhat year-to-date but ticked higher in June with an increasingly tight labour market arguing more gains are on the way. On balance, the labour force data continues to suggest that the economy is having little difficulty absorbing Federal Reserve rate hikes to-date and should provide additional confidence that more are warranted.

Canada Posted Another Whopping Job Gain in June

Highlights:

- Employment rose by a much-stronger-than-expected 45k in June following May's 55k increase. Market expectations were for a 10k gain.

- Much of the increase was in part-time employment though the average increase over the last two months is still skewed toward full-time work.

- Both goods producing and services industries posted solid gains in June. The goods sector has been punching above its weight in 2017, accounting for 30% of year-to-date job growth.

- Job growth was concentrated in Quebec and BC, and to a lesser extent Alberta. Relative to a year ago, gains are more widespread with employment up in 8 of 10 provinces.

- The unemployment rate fell back to a cycle low of 6.5% despite an increase in labour force participation.

- Wage growth remained a weak point with average hourly earnings for permanent employees up just 1%.

Our Take:

Canada's impressive pace of job growth continued in June with 100k jobs having been added in the last two months alone. The economy appears to be making full use of its labour resources with the unemployment rate at a cycle low and the participation rate for 15-64 year-olds at a record high. That still isn't translating into wage pressure according to this report, though other measures are showing a healthier pace of pay growth. And the Bank of Canada might not be overly concerned about today's wage number. Their recent comments on inflation lagging the cycle indicate a willingness to tighten policy based on limited slack that should eventually put more upward pressure on prices. Their latest Business Outlook Survey should also give the bank confidence that tighter labour market conditions will eventually stoke wage growth. Plans to increase employment are more widespread than at any time in the survey's history and firms are reporting that filling jobs has become more difficult. Judging by today's report and last week's survey, we think the labour market is giving a green light for the Bank of Canada to raise rates next Wednesday.