Sample Category Title

US: The Job Market Hits Just Keep on Coming

Hiring picked up the pace in June, as non-farm payrolls increased by a healthy 222k, up from an upwardly revised 152K in May. On top of the solid headline gain, revisions to the previous two months' of payrolls added 47k positions.

Private payrolls rose by 187k, led by broad based gains across the services sector (+162k). Hiring continues to be strong in health care & education (+45k), leisure & hospitality (+36k), and business services (+35K). Goods hiring picked up (+25k), on gains in construction (+16k) and mining & logging (+8k). That marks eight straight months of job growth for the mining sector off its October 2016 low. Manufacturing continues to be relatively flat (+1k).

Government hiring also picked up (+35k), driven by gains at the state and local level. Federal hiring was more modest (+4k).

The unemployment rate ticked up slightly to 4.4% as 361k workers entered the labor force, reversing much of May's exodus. The labor participation rate rose 0.1 percentage points to 62.8% - in line with its average over the past 12 months. The growth in the labor force reversed May's improvement is broader underemployment measures, with the broadest measure (U-6) up 0.2pp to 8.6%.

One soft spot in the report was a middling 0.2% gain in average hourly earnings. Year-on-year, wages were up 2.5% in June, an slight improvement from 2.4% in May. Offsetting that disappointment somewhat was an uptick in hours worked to 34.5 in June.

Key Implications

Well, so much for job gains moderating. A strong June and upward revision to prior months has seen hiring average 180k jobs per month so far in 2017, roughly in line with 2016's 187k average. The slight uptick in the unemployment rate is not overly surprising given the large drop in the labor force in May, and the unemployment rate is still below what the Fed would consider the "neutral" rate.

We continue to expect monthly job gains to moderate in the coming months, as tight labor markets make new hires tougher to find (see our recent quarterly forecast). But, as long as monthly hiring remains above the 80-120k level required to absorb new entrants to the labor force, labor market slack will continue to diminish.

As far as its full-employment mandate is concerned, the Fed is well justified in gradually removing monetary stimulus. It is the recent softness in inflation that has caused some consternation by FOMC members (see FOMC minutes). The move up in year-on-year wage growth in June is encouraging, although the relationship between labor market tightness and inflation does seem weaker than in the past. We expect the Fed to next focus on shrinking its balance sheet, likely in the fall, before taking rates another quarter point higher at the end of the year.

Non-Farm Payrolls (NFP) and CAD Job Numbers

Non-farm payroll (NFP):

The most important number to track on the jobs report this morning is not the top number, or the unemployment rate, it's wages and it has disappointed again.

- U.S Employers add +222k Jobs in June

- Jun Unemployment Rate 4.4%; Consensus 4.3%

- Jun Average Hourly Earnings +0.15%, or +$0.04 to $26.25; Over Year +2.5%

- May Unemployment Unrevised at 4.3%

- May Payrolls Revised to +152K; Apr Revised to +207K

- Jun Labor-Force Participation Rate 62.8%

- Private Sector Payrolls +187K and Government Payrolls +35K

- Jun Average Workweek +0.1 Hour to 34.5 Hours

The revisions showed job growth was better in April and May than previously thought. The U.S economy has created an average of +194k jobs over the past three months.

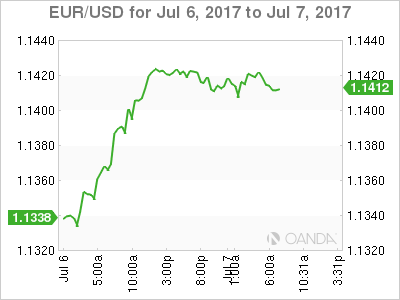

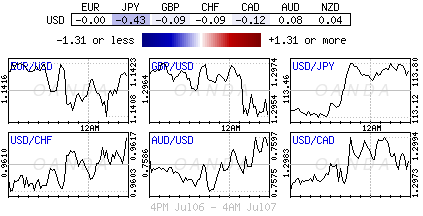

USD has pared some of its overnight gains (€1.1419, £1.2907, ¥113.76).

Selling pressure in the bond market is stalling as the payrolls release shows once again that bond investors place more importance on the wage inflation reading than the jobs growth figure.

The market is pricing in +62% chance on the Fed lifting rates one more time before the end of the year.

The yield on the U.S 10-year Treasury note has fallen -3 bops to +2.365%

Canada jobs report:

- Job Creation Keeps Chugging Along in Canada

- Canada Adds 45,300 jobs in June

- Unemployment rate falls to +6.5%

- Jun Avg. hourly wages +1.3% y/y

- Jun Full-Time Jobs +8,100; Part-Time +37,100

- Canada Jun Participation Rate At 65.9% Vs 65.8% In May

- C$1.2903 +0.65%

Today's numbers eliminate the last possible obstacle for the Bank of Canada should it choose to raise its policy rate next week (July 12) as widely expected.

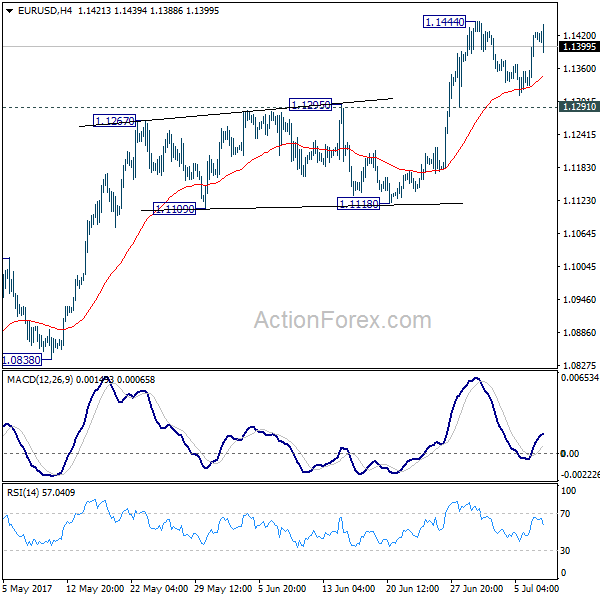

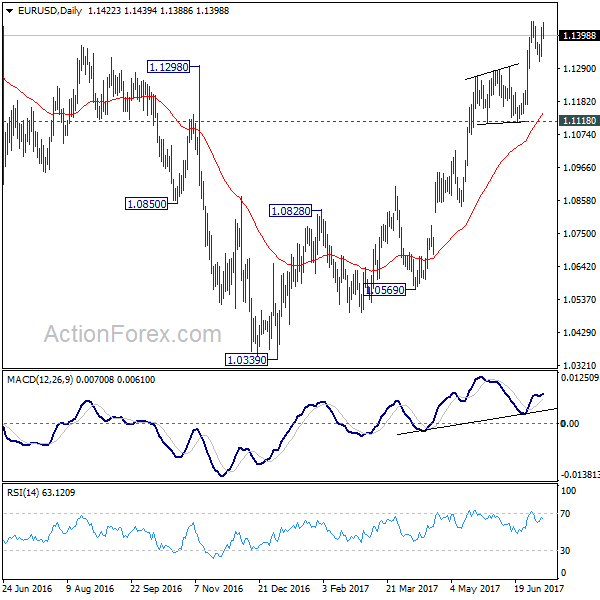

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1359; (P) 1.1392 (R1) 1.1454; More.....

Intraday bias in EUR/USD remains neutral for the moment with focus on 1.1444 resistance. Break there will resume whole rise from 1.0339 low and target 1.1615 resistance next. In case consolidation from 1.1444 extends with another fall, downside should be contained by 1.1291 resistance turned support to bring rally resumption. Meanwhile, break of 1.1291 will turn focus back to 1.1118 support instead.

In the bigger picture, the firm break of 1.1298 resistance further affirm medium term reversal. That is an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1776). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.

Dollar Unfancied by 222k Growth in Non-Farm Payroll, Canadian Dollar Jumps

Dollar is quite unfancied by the stronger than expected headline non-farm payroll number. NFP showed 222k growth in June versus expectation of 173k. Prior month's figure was also revised up from 138k to 152k. However, unemployment rate rose 0.1% to 4.4%. And more importantly, average hourly earnings rose 0.2% mom versus expectation of 0.3% mom. Prior months wage growth was also revised down from 0.2% mom to 0.1% mom. EUR/USD spikes lower to 1.1388 but is quickly back at 1.1420. Nonetheless, USD/JPY is firm at around 113.70, but as supported by Yen's weakness.

On the other hand, Canadian Dollar is gaining some momentum after its own job data. The employment market in Canada rose 45.3k in June, above expectation of 11.4k, not far from prior month's 54.5k. Unemployment rate also dropped 0.1% to 6.5%. The job data is supportive to a rate hike by BoC next week.

UK data disappointed again

Meanwhile, Sterling tumbles sharply as production data from UK released today completed a string of weaker than expected data that raised doubts on the strength of the economy. Industrial production dropped -0.1% mom, -0.2% yoy in May versus expectation of 0.4% mom, 0.2% yoy. Manufacturing production dropped -0.2% mom, rose 0.4% yoy versus expectation of 0.4% mom, 0.9% yoy.

Construction output dropped -1.2% mom in May versus expectation of 0.6% rise. Trade deficit also widened to GBP -11.9b in May versus expectation of GBP -10.9B. BoE Governor Mark Carney said before that the committee will discuss on raising rate in the coming months. But if the outlook worsen, it's believed the central bank will stay cautious, until at least when the picture for Brexit becomes clearer.

Also released from Europe today, German industrial production rose 1.2% mom in May versus expectation of 0.2% mom. Swiss unemployment rate rose 3.2% was unchanged at 3.2% in June. Swiss foreign currency reserves was relatively unchanged at CHF 639.5b in June.

BoJ announced emergency bond operation

In response to the this week's surge in global bond yields, BoJ announced to carry out an emergency fixed-rate bond buying operation to curb long term yields under the so called "Yield Curve Control" framework. The central bank said it will buy unlimited amount of JGB with maturities of 5 to 10 years. This is the third time BoJ carries out such operations since the announcement of YCC last year. The first offer in November drew no bids. Under the second operation in February, JPY 723.9b in bonds were purchased.

Released from Japan, labor cash earnings rose 0.7% yoy in May, while real cash earnings rose 0.1% yoy. Leading index rose to 104.7 in May.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1359; (P) 1.1392 (R1) 1.1454; More.....

Intraday bias in EUR/USD remains neutral for the moment with focus on 1.1444 resistance. Break there will resume whole rise from 1.0339 low and target 1.1615 resistance next. In case consolidation from 1.1444 extends with another fall, downside should be contained by 1.1291 resistance turned support to bring rally resumption. Meanwhile, break of 1.1291 will turn focus back to 1.1118 support instead.

In the bigger picture, the firm break of 1.1298 resistance further affirm medium term reversal. That is an important bottom was formed at 1.0339 on bullish convergence condition in weekly MACD. Further rise would be seen to 55 month EMA (now at 1.1776). Sustained break there will pave the way to 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 next. This will now remain the favored case as long as 1.1118 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | JPY | Labor Cash Earnings Y/Y May | 0.70% | 0.40% | 0.50% | |

| 00:00 | JPY | Real Cash Earnings Y/Y May | 0.10% | -0.10% | 0.00% | |

| 05:00 | JPY | Leading Index May P | 104.7 | 104.6 | 104.2 | |

| 05:45 | CHF | Unemployment Rate Jun | 3.20% | 3.20% | 3.20% | |

| 06:00 | EUR | German Industrial Production M/M May | 1.20% | 0.20% | 0.80% | 0.70% |

| 07:00 | CHF | Foreign Currency Reserves Jun | 693.5B | 695.0B | 693.7B | |

| 08:30 | GBP | Industrial Production M/M May | -0.10% | 0.40% | 0.20% | |

| 08:30 | GBP | Industrial Production Y/Y May | -0.20% | 0.20% | -0.80% | |

| 08:30 | GBP | Manufacturing Production M/M May | -0.20% | 0.40% | 0.20% | |

| 08:30 | GBP | Manufacturing Production Y/Y May | 0.40% | 0.90% | 0.00% | |

| 08:30 | GBP | Construction Output M/M May | -1.20% | 0.60% | -1.60% | -1.10% |

| 08:30 | GBP | Visible Trade Balance (GBP) May | -11.9B | -10.9B | -10.4B | -10.6B |

| 12:00 | GBP | NIESR GDP Estimate Jun | 0.20% | |||

| 12:30 | CAD | Net Change in Employment Jun | 45.3K | 11.4K | 54.5k | |

| 12:30 | CAD | Unemployment Rate Jun | 6.50% | 6.60% | 6.60% | |

| 12:30 | USD | Change in Non-farm Payrolls Jun | 222K | 173K | 138K | 152K |

| 12:30 | USD | Unemployment Rate Jun | 4.40% | 4.30% | 4.30% | |

| 12:30 | USD | Average Hourly Earnings M/M Jun | 0.20% | 0.30% | 0.20% | 0.10% |

| 14:00 | CAD | Ivey PMI Jun | 53.8 | |||

| 14:30 | USD | Natural Gas Storage | 46B |

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD had a bullish momentum yesterday topped at 1.1424. As you can see on my H4 chart below price is still moving convincingly above the trend line support and EMA 200 suggests a strong and valid bullish trend. The bias is bullish in nearest term testing 1.1500 – 1.1530 area. Immediate support is seen around 1.1350. A clear break below that area could lead price to neutral zone in nearest term testing 1.1285 support area but overall I remain bullish and any downside pullback should be seen as a good opportunity to buy. Fundamental focus today will be on the US NFP number.

GBPUSD

The GBPUSD had a bullish momentum yesterday topped at 1.2982. The bias is bullish in nearest term retesting 1.3050 key resistance which remains a good place to sell with a tight stop loss as a clear break and daily/weekly close above that area would activate my bullish mode targeting 1.3350 area next week. Immediate support is seen around 1.2925 area. A clear break below that area could lead price to neutral zone in nearest term testing 1.2875 region. Fundamental focus today will be on the US NFP number.

USDJPY

The USDJPY had another indecisive movement yesterday but traded higher earlier today in Asian session hit 113.83. The bias remains bullish in nearest term testing 114.30. Immediate support is seen around 113.20. A clear break below that area could lead price to neutral zone in nearest term testing 112.75 support area which is a good place to buy. On the upside, a clear break and daily/weekly close above 114.30 would expose 115.50 region or higher next week. Fundamental focus today will be on the US NFP number.

USDCHF

The USDCHF had a bearish momentum yesterday bottomed at 0.9601 and hit 0.9595 earlier today in Asian session. The bearish pin bar I showed you yesterday gave us a valid bearish signal. The bias is bearish in nearest term testing 0.9550 – 0.9450 key support area which remains a good place to buy with a tight stop loss below 0.9450 as a clear break and daily/weekly close below that area would expose 0.9250 region next week. Fundamental focus today will be on the US NFP number.

Euro In Holding Pattern Ahead Of US Nonfarm Payrolls

The euro is showing little movement in the Friday session. Currently, the pair is trading slightly above the 1.14 level. On the release front, German Industrial Production gained 1.2%, crushing the estimate of 0.2%. In the US, the week wraps up with key employment events. Average Hourly Earnings is expected to edge up to 0.3%, and Nonfarm Payrolls is forecast to jump to 175 thousand. As well, the Federal Reserve will release its semi-annual Monetary Policy Report.

The ECB released the minutes of its June meeting on Thursday, and the euro responded with gains, as the ECB mulled policy adjustments. Policymakers discussed removing its 'easing bias' at the June meeting, but ultimately decided not to make a move, since stronger economic conditions had not resulted in higher inflation. At the same time, minutes were cautious in tone, noting that 'it was necessary to avoid signals that could trigger a premature tightening of financial conditions'. The minutes come after comments from ECB President Mario Draghi last week, who said that the eurozone growth was broadly distributed and that factors keeping inflation down were temporary. The markets jumped on his remarks, as speculation rose that the ECB was preparing to taper its stimulus program. Draghi's message did not seem to veer away from ECB policy, but the markets clearly thought otherwise. As well, ECB chief economist Peter Praet reiterated the bank's stance at a conference in Paris. Praet noted that eurozone economic growth is accelerating, but said that the ECB still needs to provide a 'steady hand' in order to spur stubbornly low inflation levels. Next stop for the ECB is the July policy meeting. In June, the bank removed an easing bias towards lowering interest rates. However, policymakers may now be wary about sending more signals of tightening policy, so as to avoid another run on the euro. The ECB doesn't want the rate statement to shake up markets, so we could see a bland statement, to the effect that the economy is headed in the right direction, but QE will remain in place until inflation levels move higher.

The dollar shrugged off the release of the Fed's June policy meeting, which didn't provide any clarity about the Fed's plans. The minutes pointed to a divided Fed over the key issues of inflation and the Fed's bloated balance sheet. Some members expressed unease at the Fed's current forecast of rate hikes, given the persistently low levels of inflation. According to the current 'dot plot', the Fed expects to raise rates in December, and three times in 2018. There was also division over the timing of reducing the $4.2 trillion balance sheet – some policymakers were in favor of starting in September, while others preferred later in the year. At the June meeting, the Fed stated that it would begin reducing the balance sheet this year, but provided no details. Analysts expect the Fed to start winding down the balance sheet in September, prior to a rate hike in December. The markets are lukewarm about a rate hike in December, with the odds at just 50%, according to the CME Group.

Non-Farm Payrolls: A Boon Or Bust For The Dollar?

Friday July 7: Five things the markets are talking about

Global bond yields remain elevated as investors wait for this week's main event, non-farm payrolls (NFP).

It seems that the market is becoming more anxious that central banks are moving towards reducing stimulus efforts that have supported debt markets. The eurozone remains at the center of the selling as the yield on 10-year German Bunds rallies to its highest level in 18-months.

The U.S Labor Department reports its official jobs figures for June at 08:30 am EDT. American employers are expected to have added around +175k jobs last month along with wage growth.

Average hourly earnings are expected to improve in today's employment report, but not very much, the market is looking for a +0.3% monthly gain versus June's very subdued +0.2% increase. Year-on-year, consensus is looking for earnings to rise to a +2.6%.

Note: +3% is considered the minimum necessary to boost the Fed's most closely watched inflation measure, the PCE core.

If average hourly earnings prove a surprise in June, either improving more than expected or slowing more than expected, other headline prints (NFP and unemployment rate) may actually take a back seat for intraday moves.

Also, the G-19 + 1 summit begins in Hamburg this morning – U.S President Trump is expected to hold his first meeting with Russia's Vladimir Putin as well as meet his Chinese counterpart Xi Jinping.

1. Global stocks under pressure from rising yields

Rising global interest rates continue to weigh on equity sentiment.

Overnight, benchmarks in Japan, Korea and Hong Kong all fell for the third session in four, while Australia's S&P/ASX 200 has dropped three straight in recording a regional-worst -1% decline – the index has seen red for a third-consecutive week.

The outlier has been China to a certain extent; the Shanghai Composite has now risen for the ninth session in eleven with its overnight +0.2% climb.

In Europe, stocks remain under pressure following a barrage of macro data. Oil price continue to drag on energy stocks, while tightening concerns from central banks is providing added pressure.

U.S equities are set to open in the red (-0.1%).

Indices: Stoxx50 -0.2% at 3,455, FTSE -0.2% at 7,324, DAX -0.2% at 12,360, CAC-40 -0.4% at 5,133, IBEX-35 -0.4% at 10,463, FTSE MIB -0.6% at 20,967, SMI -0.3% at 8,860, S&P futures +0.1%

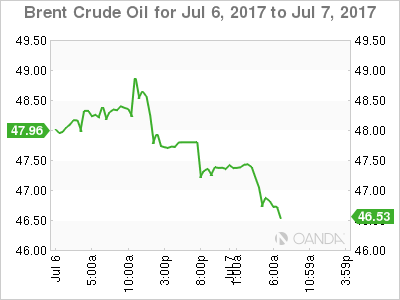

2. Oil prices fall on signs market still oversupplied, gold little changed

Ahead of the U.S open, oil prices are down more than -2% after data showed U.S production rose last week just as OPEC exports hit a 2017 high, basically casting doubt on efforts by producers to curb oversupply.

Brent futures are down -$1.07, or -2.2%, at +$47.04 a barrel, its weakest level in more than a week. U.S West Texas Intermediate (WTI) crude futures are trading at +$44.40 a barrel, down -$1.12 or -2.5%.

Weekly U.S government data showed yesterday that U.S. oil production rose +1% to +9.34m bpd, correcting a drop in the previous week that was down to one-off maintenance issues.

Note: The market has ignored news from the EIA that U.S crude inventories fell by -6.3m barrels in the week to June 30 to +502.9m barrels, the lowest since January.

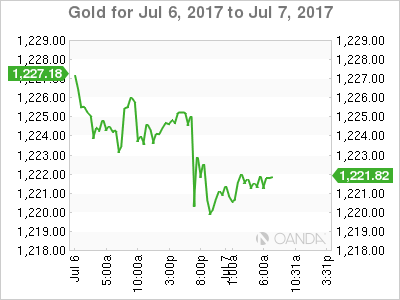

For now, rising geopolitical risks is providing some support for gold. The precious metal is little changed (-0.2% to +$1,220.97 an ounce) overnight as tensions on the Korean peninsula stoked safe-haven demand for the metal. Nevertheless, the dollars strength is expected to provide weight for some metal prices.

3. Global yields rally on monetary policy fear

Global government bonds continue their sell off as anxiety toward less monetary policy support from central banks continue to drive investors to cut bond holdings.

The center of the selling remains in the eurozone where government bond yields have jumped broadly. The yield on the 10-year German Bund has moved back above the psychological +50 bps to +0.56%, a level not seen since early 2016. The selling pressure has spread to the U.K, the U.S, Canada, Denmark and Sweden.

Yesterday, the yield on U.S 10's touched +2.38%, the highest level since May 11.

Elsewhere, down-under, Australia's benchmark yield has gained +2 bps to +2.66%. Earlier this week, the Reserve Bank of Australia's (RBA) Harper said that Aussie policy makers are “comfortable holding interest rates for now and see no reason to scare the horses at the moment” by signalling coming interest rate increases.

4. Dollar range bound until NFP

Major currency pairs sit atop some key levels ahead of NFP.

The EUR (€1.1412) remains at the high end of yesterday's rise as recent 'hawkish' commentary from ECB officials continue to keep the 'single' unit supported. Through €1.1427 the bulls are targeting June's high of €1.1447.

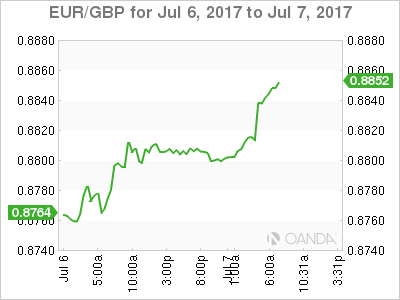

Sterling (£1.2907) is under pressure from weaker UK IP/MP data (see below), techies note support around £1.2890 area, which corresponds to the weekly lows. EUR/GBP has spiked to €0.8838, with resistance seen at €0.8845 initially.

Yen (¥113.65) is weaker in the overnight session as the Bank of Japan (BoJ) acts to slow JGB yield rise – officials announced that they would increase purchases of 5-10 year JGB's to +¥500B from +¥450B at its upcoming QE operation.

5. British Industrial Output Falls Unexpectedly

Data this morning showed that U.K. industrial production shrank unexpectedly in May, falling -0.1% vs. +0.3% gain expected, while factory output fell by -0.2%, against expectations of +0.3% growth.

Note: Industrial output was dragged lower by a fall in manufacturing output and lower energy production.

It's further proof that U.K economic growth has failed to pick up in Q2 after a sluggish start to the year.

Similar to other Central Bank rhetoric of late, the Bank of England (BoE) is considering raising interest rates given high inflation, however, disappointing economic data like this should surely give sterling 'bulls' pause for thought?

Dollar Holds Ground Ahead Of NFP

The Greenback held steady against its major counterparts during Friday's trading session, as investors awaited the heavily anticipated US employment report this afternoon for further insight on the health of the US job market. With the disappointing ADP data showing that US private employers added 158k jobs in June vs the 188k estimates, markets will be closely observing whetherthe pending NFP headline figure follows a similar pattern. June's jobs report is a big deal and has the potential to impact rate hike expectations this year, especially when considering how policy makers remain split on the outlook for inflation. Much attention will be directed towards average hourly wages, as a decline in wage growth may raise concerns over inflation picking up, consequently weighing on the prospect of higher rates this year. From a technical standpoint, although the Dollar is flexing against other major currencies today, this could be deflated if June's jobs report disappoints.

Sterling tumbles after industrial production falls

Sterling was vulnerable to heavy losses on Friday after industrial output data unexpectedly contracted in May, consequently fueling the Brexit fears. With the string of economic data from the UK this week proving nothing to celebrate about, investors may be forced to re-evaluate the possibility of a UK rate hike this year. With uncertainty still the name of the game when dealing with Sterling and Brexit woes weighing on sentiment, Sterling may be instore for further punishment. The GBPUSD is coming under increasing pressure on the daily charts. A breakdown below 1.2850 could encourage a further decline towards 1.2750.

WTI Crude under pressure again

WTI Crude dipped below $45 on Friday after reports of a rise in US production overshadowed data that showed US Crude oil and gasoline inventories declined sharply last week. Earlier reports of Russia being opposed to any further supply cuts and OPEC's output in June rising to its highest levels so far this year have also complimented oil's downside. With the unshakeable oversupply dynamics weighing heavily on investor sentiment and the increasingly clear fact that OPEC may be losing its grip over the industry, oversupply woes may remain a dominant theme. From a technical standpoint, WTI Crude is coming under increasing pressure on the daily charts. Weakness below $44.50 could encourage a further decline back towards $42.

Commodity spotlight – Gold

Gold prices depreciated during early trading on Friday, as investors adopted a cautious approach ahead of the heavily anticipated NFP report that is being released later today. A slightly stronger US Dollar complimented Gold's decline, with the metal edging towards $1220 at the time of writing. It is becoming quite clear that the rising prospect of tighter global monetary policies has punished the zero-yielding metal with the short-term outlook tilted to the downside. Although the heightening geopolitical tensions surrounding North Korea, Brexit developments and on-going political risk in Washington may stimulate the flight to safety and offer some support down the line, Gold currently remains pressured. From a technical standpoint, weakness below $1220 may open a path towards $1214.

Market Update – European Session: European Indices Drift Lower Ahead Of US Jobs Data

EU Mid-Market Update: UK data continues to underwhelm; European Indices drift lower ahead of US Jobs data

Notes/Observations

UK economic data continues to disappoint, pushing Sterling towards week lows

2 day G20 summit begins today in Hamburg

European Bond futures stabilize ahead of the US Jobs data, following sharp falls yesterday

Overnight

Asia:

Bank of Japan (BOJ) announced that it would increase purchases of 5-10 year JGBs to ¥500B from ¥450B at its upcoming QE operation.

JAPAN MAY LABOR CASH EARNINGS Y/Y: 0.7% V 0.4%E; REAL +0.1% V 0.1%E; Government said the May, regular pay (base wages) had the largest annual gain since March 2000.

China Foreign reserves rises for fifth straight month

Europe:

UK Industrial and Manufacturing production falls short of expectations, continuing the recent run of weaker data

Continued hawkish commentary overnight from ECB's Weidmann noting economic recovery now raises prospect of monetary policy normalization, followed by comments by ECB's Coeure reiterating that if needed Governing council can adjust its instruments both qualitatively and quantitatively, although he noted underlying inflationary pressures remain weak.

French and German Industrial production record strong beats of estimates and of prior months reading

BoE McCafferty acknowledges a modest loss of momentum in the UK economy into H1, noting however that pick up inflation is not something that can be ignored

UK house prices fall for the third quarter running according to the Halifax survey

2 day G20 Summit begins today

America:

Fed’s Mester (hawkish, non-voter) said Fed should launch portfolio runoff sooner rather than later; Expects inflation to resume climb toward 2%, but recent slowdown requires attention.

June NonFarm Payroll report due 8:30ET, Change in Payrolls expected at +178K.

Economic Data

(UK) MAY INDUSTRIAL PRODUCTION M/M: -0.1% V 0.4%E; Y/Y: -0.2% V 0.2%E

Manufacturing Production M/M: -0.2% v 0.5%e; Y/Y: 0.4% v 1.0%e

(DE) GERMANY MAY INDUSTRIAL PRODUCTION M/M: 1.2% V 0.2%E; Y/Y: 5.0% V 4.0%E

(FR) FRANCE MAY INDUSTRIAL PRODUCTION M/M: 1.9% V 0.6%E; Y/Y: 3.2% V 1.4%E

(UK) JUN HALIFAX HOUSE PRICE M/M: -1.0% V +0.2%E; 3M/Y: 2.6% V 3.1%E

(CN) CHINA JUN FOREIGN RESERVES: $3.0568T V $3.061TE (5th straight increase)

(UK) MAY VISIBLE TRADE BALANCE: -£11.9B V -£10.9BE

(CH) SWISS JUN UNEMPLOYMENT RATE: 3.0% V 3.0%E

(FR) FRANCE MAY TRADE BALANCE: €-4.9B V -€5.1BE

(NO) Norway May Industrial Production M/M: -0.7% v 0.7% prior; Y/Y: 0.5% v 0.9% prior

(IT) Italy May Retail Sales M/M: -0.1% v 0.3%e; Y/Y: 1.0% v 1.2% prior

Fixed Income Issuance:

Non seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx50 -0.2% at 3,455, FTSE -0.2% at 7,324, DAX -0.2% at 12,360, CAC-40 -0.4% at 5,133, IBEX-35 -0.4% at 10,463, FTSE MIB -0.6% at 20,967, SMI -0.3% at 8,860, S&P futures +0.1%]

Market Focal Points/Key Themes: European stocks open slightly lower and remained under pressure following a barrage of macro data; oil price dragging on energy stocks; risk sentiment remains muted following poor performance in Asia and risk events over coming weekend; materials stocks continue downward trend; equities in general under pressure following several days of concern over potential tightening from central banks; attention on comments from G-20 meeting, and upcoming NFP in the US

Equities

Consumer discretionary [Carrefour CA.FR -4.2% (Q2 sales), Dunelm DNLM.UK 4.8% (trading update), Aurelius AR4.DE +0.1% (raised guidance)]

Energy [Centrica CNA.UK +4.9% (takeover speculation)]

Financials [Protector Forsikring PROTCT.NO +2.4% (outlook)]

Healthcare [Cellnovo CLNV.FR 10.9% (placement)]

Industrials [Cape CIU.UK 45.8% (to be acquired), Fenner FENR.UK +7.7% (trading update), Deutz DEZ.DE 2.0% (Volvo sells stake)]

Technology [Future FUTR.UK +6.4% (acquisition)]

Telecom [Com Hem COMH.SE +4.0% (analyst action)]

Speakers

(EU) ECB's Coeure: Reiterates that if needed Governing council can adjust its instruments both qualitatively and quantitatively; Underlying inflationary pressures are still weak

EU's Juncker: Will respond adequately if US take punitive trade measures.on steel - comments before G20

Currencies

GBPUSD drops on weaker UK IP/MP data falling almost 40 pips to 1.2916, dealers note support around 1.2890 area which corresponds to the weekly lows. EURGBP spikes to 0.8838, with resistance seen at 0.8845 initially.

EURUSD consolidates above 1.14 following the strong rise seen yesterday, with a move above 1.1427 paving the way to target June highs. Recent hawkish commentary from ECB officials continue to keep the Euro supported.

USD/RUB drops to the lowest since January on the back of continued weakness in OIl.

Fixed Income

Bund futures trade at 160.55 down 5 ticks continuing its move after yesterday’s dramatic breaking of the 10-year yield 0.50% level. All eyes are on today’s US nonfarm payroll number. Resistance lies near the 160.75 level followed by 161.50. A break of the 160.00 support level could see lows target 159.25 followed by 157.50.

Gilt futures trade at 124.74 higher by 2 ticks as core European government bond yields have edged lower after yesterday's sharp rise but the market is unlikely to do much ahead of today's US non-farm payroll release. Gilts are near 5-month lows. Price finds key support at the 124.42 support level. An acceleration lower could test the 122.88 region. Resistance remains the noted 126.00 region, followed by 126.72.

Friday’s liquidity report showed Thursday’s deposits dropped rose to €612.9B from €611.0B prior. Use of the marginal lending facility fell to €187M from €136M prior.

Corporate issuance saw $5.75B come to market via 2 issues headlined by Sumitomo Mitsui Financial Group $4.25B 3-part offering. This week’s issuance is at $5.75B. For the week ending July 5th Lipper US fund flows reported IG funds net inflows $2.5B bringing YTD inflows to $69.1B, High yield funds reported outflows of $1.1B bringing YTD outflows to $7.7B.

Looking Ahead

06:00 (PT) Portugal May Retail Sales M/M: No est v 1.5% prior; Y/Y: No est v 4.9% prior

07:00 (BR) Brazil Jun FGV Inflation IGP-DI M/M: -0.7%e v -0.5% prior; Y/Y: -1.2%e v +1.1% prior

07:30 (IN) India Weekly Forex Reserves

08:00 (PL) Poland Jun Official Reserves: No est v $109.7B prior

08:00 (UK) Jun NIESR GDP Estimate: No est v 0.2% prior

08:00 (BR) Brazil Jun IBGE Inflation IPCA M/M: -0.2%e v 0.3% prior; Y/Y: 3.1%e v 3.6% prior

08:00 (CL) Chile Jun CPI M/M: 0.0%e v 0.1% prior; Y/Y: 2.1%e v 2.6% prior

08:00 (CL) Chile Jun CPI Ex Food and Energy M/M: 0.1%e v 0.3% prior; Y/Y: No est v 2.5% prior

08:15 (UK) Baltic Dry Bulk Index

08:30 (US) Jun Change in Nonfarm Payrolls: +178Ke v +138K prior, Change in Private Payrolls: +170Ke v +147K prior, Change in Manufacturing Payrolls: +5Ke v -1K prior

08:30 (US) Jun Unemployment Rate: 4.3%e v 4.3% prior, Underemployment Rate: No est v 8.4% prior, Change in Household Employment (civilian labor force): No est v 159.8K prior, Civilian Labor Participation Rate: 62.7%e v 62.7% prior

08:30 (US) Jun Average Hourly Earnings M/M: 0.3%e v 0.2% prior; Y/Y: 2.6%e v 2.5% prior; Average Weekly Hours: 34.4e v 34.4 prior

08:30 (CA) Canada Jun Net Change in Employment: +10.0Ke v +54.5K prior; Unemployment Rate: 6.6%e v 6.6% prior; Full Time Employment Change: No est v 77.0K; Part Time Employment Change: No est v -22.3K prior; Participation Rate: No est v 65.8% prior

08:30 (US) Weekly USDA Net Export Sales

08:30 (CL) Chile Jun Trade Balance: $0.1Be v $0.7B prior

08:30 (CL) Chile Jun International Reserves: No est v $38.9B prior

09:00 (MX) Mexico Jun CPI M/M: +0.3%e v -0.1% prior; Y/Y: 6.3%e v 6.2% prior; Core CPI Y/Y: 0.3%e v 0.3% prior

09:00 (RU) Russia Jun Official Reserve Assets: $407.3Be v $405.7B prior

10:00 (CA) Canada Jun Ivey Purchasing Managers Index (Seasonally Adj): 58.0e v 53.8 prior

10:30 (US) Weekly EIA Natural Gas Inventories

13:00 (US) Weekly Baker Hughes Rig Count data

GOLD Monitoring Support At 1214, SILVER Monitoring Support At 1214. Sharp Decline, CRUDE OIL Profit-Taking After The Strong Increase.

GOLD Monitoring support at 1214.

Gold's is trading lower towards strong support given at 1214 (09/05/2017 low). Hourly resistance can be found at 1258 (23/06/2017 high). Expected to show further weakness.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

SILVER Monitoring support at 1214. Sharp decline.

Silver's short-term decline should continue until support at 15.63 (27/12/2016 low). Key resistance is given at a distance at 17.75 (06/06/2017 high). The road seems wide open for further decline.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

CRUDE OIL Profit-taking after the strong increase.

Crude Oilis back to bearish again. Support is given at 42.05 (21/06/2017 low). Expected to show renewed weakness.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).