Sample Category Title

Trade Idea Wrap-up: USD/CHF – Stand aside

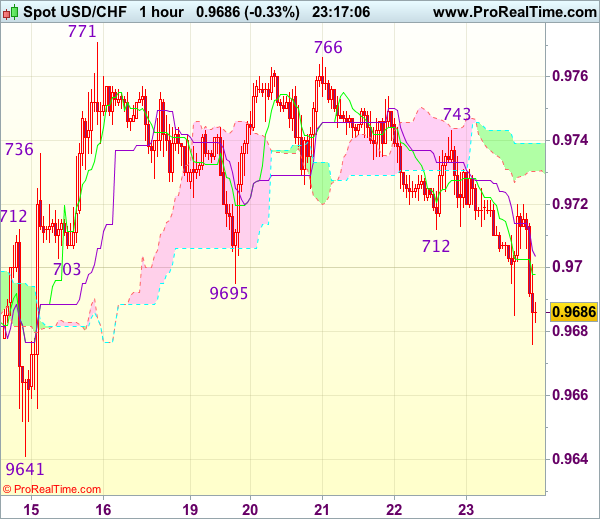

USD/CHF - 0.9692

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9699

Kijun-Sen level : 0.9704

Ichimoku cloud top : 0.9739

Ichimoku cloud bottom : 0.9730

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Dollar’s breach of previous support at 0.9695 dampened our bullishness and erratic fall from 0.9771 top may extend weakness to 0.9660, however, as broad outlook remains consolidative, still reckon downside would be limited to 0.9641 support, risk from there is seen for another rise to take place next week.

On the upside, expect recovery to be limited to the upper Kumo (now at 0.9739) and bring another decline. Only a firm break above resistance at 0.9743 would revive bullishness and signal an intra-day low is formed, bring test of 0.9766-71 resistance first. Once this resistance is penetrated, this would confirm recent rise from 0.9613 low has resumed for test of resistance at 0.9808, then towards another previous resistance at 0.9825.

Trade Idea Wrap-up: GBP/USD – Stand aside

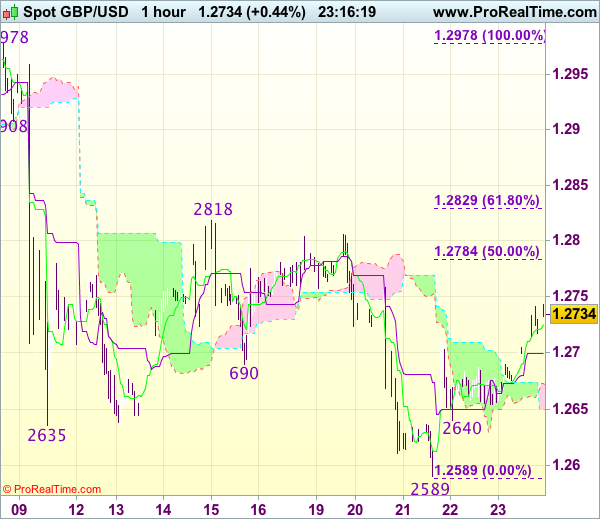

GBP/USD - 1.2726

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2726

Kijun-Sen level : 1.2700

Ichimoku cloud top : 1.2673

Ichimoku cloud bottom : 1.2649

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Cable’s intra-day rebound dampened our bearishness and suggests a temporary ow has been formed at 1.2589, hence upside risk remains for this move to bring retracement of recent decline to 1.2755-60, however, reckon upside would be limited to 1.2780-85 (50% Fibonacci retracement of 1.2978-1.2589) and price should falter well below resistance at 1.2818, bring another selloff next week.

In view of this, would not chase this move here and would be prudent to stand aside for now. Below 1.2690-95 would bring weakness towards 1.2640-50 but break of latter level is needed to signal the rebound from 1.2589 has ended, bring retest of this level later.

Week Ahead – GDP Out of US and UK in Focus; Eurozone and Japan Inflation Due

Growth data are due from two of the world's largest economies - the United States and the United Kingdom. Japan will also be releasing a flurry of data.

United States

A slew of data are expected from the US next week. The Personal Consumption Expenditure (PCE) price index is one of the most important indicator as well as personal income and spending. The May PCE figure is due on Friday and it is a closely monitored indicator as it is the Federal Reserve's most preferred gauge of inflation. The April PCE index rose 0.2% for April following a 0.2% decline the previous month. Any increase in the May number would add to expectations of the Fed hiking interest rates again later this year.

Final GDP for the first quarter is due on Thursday, which is also a very important piece of data. It is expected to show growth at 1.2%, the same as the previous estimate. Other data such as durable goods orders for May are expected to come in at -0.5% versus the prior month's -0.8%. The June final reading of the University of Michigan consumer sentiment index will also be looked at for indications of the US economy's health and is forecast at 94.5 as the previous reading.

May building permits are due on Monday, while the April number for the Case Shiller House Price Index will be released on Tuesday. The May report for pending home sales is out on Wednesday.

United States

Final GDP data for the first quarter are due on Friday. The figure is expected to be the same as previous at 0.2% growth quarter-on-quarter and 2% year-on-year.

It has been a year since the Brexit vote and overall, the UK economy has performed relatively well in terms of GDP growth during the second half of 2016 following the referendum. However, more recently there have been signs of a slowdown in economic activity. The fall in real average wages could have serious consequences on growth in the future.

Eurozone

The flash CPI reading is expected to show inflation falling. The June reading is due on Friday and is expected at 1.3% year-on-year. May's final CPI was confirmed at 1.4%, which was unchanged from the flash reading and also in line with consensus forecasts. A lower reading would support the ECB's view that underlying price pressures remain subdued.

At the ECB's June policy meeting, the inflation forecast for 2017 was cut to 1.5% from 1.7% previously.

On Thursday, the June economic sentiment report is expected to improve further and is expected at 109.5 versus 109.2 in the previous reading. The German Ifo business climate is due on Monday.

Japan

There will be flurry of data releases out of Japan next week, starting with retail sales on Thursday, then household spending, unemployment figures, CPI and industrial production due on Friday

Japan's CPI numbers are expected to show core inflation rising in May to 0.4% year-on-year versus 0.3% previously. The preliminary industrial production number is expected at -3.2% month-on-month versus the prior month's reading of 4%.

China

China PMI for manufacturing and non-manufacturing sectors are due on Friday.

Markets Overly Bearish GBP

- Markets overly bearish GBP - Peter Rosenstreich

- Switzerland's Trade Activity Picked Up - Arnaud Masset

- Oil prices continue to slide; below $40 within a few weeks?

- Biotech Revolution

Economics - Markets overly bearish GBP

We continue to suspect that markets are underpricing the probability of a BoE policy adjustment. We believe that as with the Fed, the threshold for removal of emergency measures is significantly lower than standard interest rate hikes. Central banks would like to get to "normal" conditions in order to have tool to defend and economic downturn or worse. While interest rates in the UK never went negative, it's difficult for MPC members to justify ultra-easy policy given the economic momentum. BoE Governor Carney's Mansion House speech dented our expectations of a 2017 rate hike. However, his argument that consumer cant handle higher rates due to large debt load feels akin to teasing a bull.

However, BoE chief economist Haldane indicated that solid economic data (although still below trend) and inflation risks would suggest hikes in 2H (most likely November). This was a surprising development since Haldane is a known dove. This is not the first time Haldane's view diverged from the MPC, but is especially interesting since Haldane is not part of the three MPC members which dissented last week. The wide majority advantage the MPC doves have enjoyed has quickly erod€ed. This change will put the markets on alert for shifts in doves Broadbent and Vlieghe and improving domestic data.

Last week UK manufacturing firms reported export and total order books has improved to multi decade highs. This CBI reports supports expectations for firmer 2H of economic growth. As with the rest of the G10 wage inflation remains subdued but at 1.7% wage grow is not terrible considering the Brexit induced threat of mass exodus. Outside Brexit negotiations, Friday release of 1Q final GDP read will the focus of sterling trader.

Markets are now pricing in 12bp of hikes by end of 2017. We would avoid EURGBP as Europe is enjoying an accelerating cyclical growth uptrend and ECB nearing reducing emergency measures which is likely to give Euro a boost. To materialize our constructive GBP view, we see long GBPCHF as the ideal position. Outside improving economic data and increase probably of near term rate hike, Brexit negotiating have taken a friendly turn with PM May decision to offer EU citizens right in UK. Switzerland is struggling with weak economic data driven by overvalued CHF. The SNB is unlikely to even entertain the notion of exiting from extreme monetary policy and stands ready to intervene should CHF appreciate further.

Economics - Switzerland's Trade Activity Picked Up

After the usual March-April contraction, Switzerland's trade surplus bounced back in May amid a sharp recovery in exports. The trade surplus rose to CHF 3.4 billion in May from CHF 1.96 a month earlier. Exports - in real terms - increased 2.9% m/m while imports eased to 2% m/m. On a year-over-year basis, exports rose 7.5% and imports 8.7% amid solid growth in chemical and pharmaceutical products.

Exports to China passed the CHF 1bn threshold to print at 1.16bn while imports reached 1.02bn, leaving a trade surplus of CHF 139 million. Trade activity with the European Union also accelerated substantially with exports and imports rising 1.47bn and 2.12bn respectively, adding evidence that the European economy is on the right track.

It was quite a pleasant surprise for the Swiss watch industry as exports rose 9% in May compared to a contraction of 5.7% in the previous month. The sharp recovery was mostly driven by a surge in exports to Hong Kong, China and Italy, while Gulf countries reduced sharply their imports amid falling oil revenue and geopolitical uncertainties.

All in all, the report showed that the Swiss economy is still right on track but continues to suffer from the strong CHF. The recovery pace is solid especially given the slower than expected recovery in Europe and the United States. Swiss companies already optimised their functioning and no more gains can be expected on this side. Investments have been reduced to the minimum, costs have been cut. Economic improvement of Switzerland's main trading partner is more necessary to see a substantial growth acceleration.

In the FX market, the Swiss franc continued to move higher against the single currency as investors sit on the sidelines assessing the potential effects of Macron's upcoming economic reform and the renewed positive dynamic between France and Germany. EUR/CHF held above the 1.08 threshold but short sellers will most likely try to push the pair lower, which force the SNB to give a warning shot.

Economics - Oil prices continue to slide; below $40 within a few weeks

Since May 23, bearish pressures on oil have been stronger. The black commodity is largely declining. Crude oil is approaching $40 a barrel. This represents lowest levels since August 2016. For now, we believe that the decline is set to continue. Indeed, since the Qatar diplomatic issue, there are growing concerns that other OPEC members will not respect the production cut and therefore oversupply.

Why the decline will continue? When looking specifically to Saudi Arabia, the largest oil exporter in the world, we may believe that there are supporting evidence to this. In our view, the Arabic country really needs to have higher oil prices. For us its FX reserves are declining too sharply, 27% from its 2014 peak. We recall that only for this year, it has diminished by $36 billion.

Current oil prices seem then way too low for Saudi Arabia, which is in return obliged to liquidate its FX reserves to assume its running costs. On top of that, Saudi Arabia is willing to let investors buy 5% of its oil reserves in a clear effort to get cash as soon as possible. By the way, at current oil prices, this seems like a deal for bullish buyers.

For the time being, Saudia Arabia looks unable to prevent the decline of its FX reserve at oil prices below $55 a barrel. Consequences will be catastrophic for the country and this is why see Saudia Arabia opening its reserves to investors despite their reserves are scarce and should last, according to most analysts, no more than 60 years.

Another solution appears nonetheless possible. That would be to convince other OPEC members to cut their production and prices would certainly go back up. Yet, geopolitical issues are important as Qatar is accused to finance terrorism.

The foreseeable future does not look so bright for Saudi Arabia. In addition, the US shale gas industry is booming back and is putting deeper downside pressures on oil. In the medium-term, we believe that oil prices should head below $40.

Themes Trading - Biotech Revolution

The pharmaceutical industry is going through a minor revolution. Biotechnology has a broad mandate, covering a wide range of processes for transforming living organisms for human purposes. However, this theme focuses on a new breed of companies that have joined the race to use modern technology to create healthcare products.

These companies harness cellular and bio-molecular processes to develop technologies and products to fight disease. Exploding R&D costs have forced traditional pharma companies to look to smaller, more agile, technology-driven firms as the primary pipeline for innovation. With public and private investors and big pharma all expecting the next big breakthrough to come from this dynamic sector, valuations are on the rise.

We built this theme by filtering on firms with a market capitalization of over $1 billion and positive sales growth over the past two years, ensuring that they have sufficient cash flow to fund the next blockbuster.

Weekly Focus: Inflation Pressure Still Missing

Market movers ahead

- Inflation readings for both the US and the euro area will be clearly below central bank targets, both on actual and core measures.

- European growth indicators have remained high while others have weakened, but we expect to start seeing a decline in IFO numbers this week.

- China's official PMI may start to show more weakness.

- We are optimistic on Swedish exports this year, and hopefully that will be reflected in the upcoming trade data.

- Lower unemployment and higher consumer spending could add to the increasing optimism in Norway.

Global macro and market themes

- Supply/demand dynamics suggest the oil price may fall further near term.

- Falling inflation expectations are driven by weaker demand and the lack of a monetary policy response.

- A hard Brexit is still the most likely outcome.

- Stay tactically long USD, slightly bearish equities.

- Expect core global yields to range trade, possibly with a slight upside bias in the US

Loonie Suffers on Inflation; Dollar Down; Sterling Maintains Positive Momentum

Among the highlights in today's European session were flash Markit PMI estimates out of the eurozone and the US, Canadian inflation figures and US new home sales data. Beyond economic releases, the pound maintained yesterday's momentum on rising expectations of a rate hike by the Bank of England.

Flash eurozone PMI numbers for the month of June showed the manufacturing sector performing strongly and the services sector surprising to the downside. Specifically, the manufacturing PMI number came in at the more than six-year high of 57.3, exceeding forecasts for a reading of 56.8 and May's 57.0. The respective figure for the services sector stood at 54.7, the lowest since February of this year and below the 56.2 projected by analysts as well as the 56.3 from the previous month. The composite PMI, which blends the two sectors, also fell to its lowest since February, reaching 55.7 and failing to meet expectations for a reading of 56.5 and May's 56.8.

Despite the not so strong composite and services readings, overall the numbers are suggesting that the euro area growth rate would reach 0.7% quarter-on-quarter during the second quarter of the year, its highest since 2015. The euro posted some gains relative to the dollar as the data hit the markets, rising to $1.1187, its highest for the day at the time. Those gains were short-lived though. Euro/dollar gained momentum later in the day, rising above the 1.12 handle. In afternoon European trading hours, the pair was up 0.5% compared to where it started the day.

Weaker inflation figures led the loonie to reverse gains it made versus the US dollar earlier in the day on the back of oil prices picking up. In particular, inflation rose by 0.1% month-on-month in May, below the 0.2% expected and April's 0.4%. On an annual basis, CPI rose by 1.3%, negatively comparing to the projected 1.5% and the 1.6% from the previous month. Annual core inflation, which strips out volatile items in its calculations and which is closely watched by the Bank of Canada, fell to 0.9%, its lowest in almost twenty years. April's respective figure stood at 1.1%. The BoC's target for inflation is 2% annually and today's numbers might pose a challenge to the Bank's recent rate-hike talk, which significantly boosted the loonie.

In terms of reaction in the forex markets to Canadian inflation numbers, dollar/loonie surged, rising to as high as 1.3296 within the first few minutes of data release. The pair was trading at 1.3219 before. As the European trading session is getting closer to its end for the day, dollar/loonie is up 0.3%.

Turning to data out of the US released later in the day, the June flash manufacturing PMI was released at the nine-month low of 52.1. Moreover, this was at a negative surprise compared to the 53.0 expected and below May's 52.7. The services flash PMI was also below expectations, standing at the three-month low of 53.0. Dollar/yen fell as the data hit the markets, though it quickly recovered.

Other data out of the US pertained to new home sales during May. Those rose by a more-than-expected 2.9% to reach 610,000 units from April's upwardly revised 593,000 (from 569,000 before). Dollar/yen experienced volatility upon data release, showing no clear direction. It last traded at 111.26, slightly down on the day. The dollar index looks set to finish the day lower and was last down 0.3% on the day.

Sterling continued gaining versus the dollar today after Kristin Forbes, the Bank of England Monetary Policy Committee (MPC) member who is to complete her term at the MPC by the end of the month, urged fellow MPC members to raise rates immediately. Pound/dollar was last up on the day, reaching a three-day high of 1.2744 at its highest.

A weaker US currency spurred demand for gold which is on track for its third straight day of gains. At its highest for the day, the precious metal hit a one-week high of $1258.73 an ounce. WTI and Brent crude were trading at $42.94 and $45.49 a barrel, up 0.47% and 0.60% on the day respectively.

FOMC voting member Jerome Powell will be giving a speech at a Federal Reserve Bank of Chicago Symposium at 18:15 GMT.

FX Markets Close the Week in Peace

- US stocks slipped somewhat in the opening, but European equities encountered more substantial losses today (between 0.3% and 1%). The dollar lost some minor ground against the euro and was more or less stable against the Yen. Oil failed to rebound and hovers near the sell-off lows around $45/barrel.

- The ECB is pushing for a change to the EU-law as it seeks "clear legal competence in the area of central clearing" of euro-denominated financial contracts, giving it more control over non-EU clearinghouses, also in the UK after brexit, that are deemed systemically important to the bloc's financial markets.

- EC president Tusk said that the UK's offer on citizen's rights was below expectations. "If we compare the current level of citizens' rights to what we have heard from the British prime minister, it's obvious that this is about reducing the citizens' rights --I mean the EU citizens in the U.K.".

- According to a poll, British households are not expecting a major upsurge in inflation over the next 12 months, despite growing rancour within the ranks of the Bank of England over rising prices.

- Unidentified sources close to the matter point out that the growing scarcity of German government bonds makes any major extension of the ECB's asset buying scheme difficult and this will be a key consideration when policymakers decide whether to extend the buys.

- During a joint summit press conference, Macron and Merkel said to be fully committed to a free market economy IF it respects multilateral rules. By September, the two will also present plans to expand their cooperation.

- Eurozone PMI data were mixed today with services surprising to the downside and manufacturing to the upside. General levels stay high however. Combined with the strong consumer confidence figures yesterday, Eurozone economic growth in the second quarter promises to be strong. Price components of the PMI's disappointed.

- French Q1 growth was upgraded again to 0.5% from 0.4% in the second reading and 0.3% in the first. Consumption remained flat over the quarter, but businesses ramped up their investments, with grossed fixed capital formation increasing by 1.2 %. Meanwhile, the PMI surveys indicated French job creation hit near decade highs in June.

Rates

PMI's can't influence bond trading

Global core bond markets ended the week in the same vein as the previous 4 trading sessions: with a range-bound, technically-inspired, neutral trading session. In contrast with previous days, the eco calendar was interesting with the release of EMU PMI's. The composite declined more than forecast in June, driven by a disappointing services PMI. The PMI remained at an elevated level from an absolute point of view though and suggests EMU growth to accelerate in Q2 to 0.7% Q/Q. Price components fell to the lowest level in 5 months and confirm the ECB's reluctance in normalising monetary policy. Markets didn't react on the release and seem to be counting down to the Summer holidays. Brent crude made a second miserable attempt to correct higher, but remains near the sell-off lows. European equity market got off in a swoon around European noon, but didn't trigger safe haven flows. Sources indicated that scarcity of German government bonds is a key consideration for the ECB when deciding on extending its QE-programme. This scarcity limits the possibility of a major extension. Markets didn't react today, but if this idea gains traction it could trigger repositioning higher especially in the German bond market.

At the time of writing, changes on the German yield curve range between +0.3 bps (5-yr) and +1.8 bps (30-yr). The US yield curve shifts up to 1.6 bps (30-yr) higher. On intra-EMU bond markets, 10-yr yield spreads versus Germany were close to unchanged with Portugal (-3 bps) and Greece (-9 bps) outperforming.

Currencies

FX markets close the week in peace

Dollar cross rates didn't show much spirit either today. Traders are already looking forward to next week's more interesting eco calendar with a Yellen speech (Tuesday) and crucial inflation data on both sides of the Atlantic on Friday (US PCE and EMU CPI). USD/JPY kept a perfect tight sideways trading range near 111.30 in the final session of the week, while EUR/USD moved slightly higher, from around 1.1150 to 1.1180. The short term (2y) rate differential moved slightly in favour of the euro this week, explaining the small gains in an uneventful week. The US/German 2-yr yield spread narrowed from 200 bps on Monday to 196 bps today. The above mentioned Reuters rumours could, if reinforced eventually underpin the single currency, but for now it's still a long shot.

Sterling initially profited from BoE Forbes' farewell speech last night. The resigning policy maker tried to boost the hawkish' wing in the central bank's momentum one final time. The recent sequence of events (BoE meeting – Carney comments – Haldane speech) triggered a significant rethinking in rate hike expectation. The probability of a 25 bps hike by the BoE this year rose from 6.5% on June 14 to 50% today. Sterling still has difficulties to gain decent ground though as official Brexit-talks started on a bad note. EU Tusk said that PM May's opening offer on EU nations is below expectations. He added that Brexit took up only very little time at today's EU Summit. Sterling's fortunes changed throughout the day with EUR/GBP returning to opening levels around 0.8790.

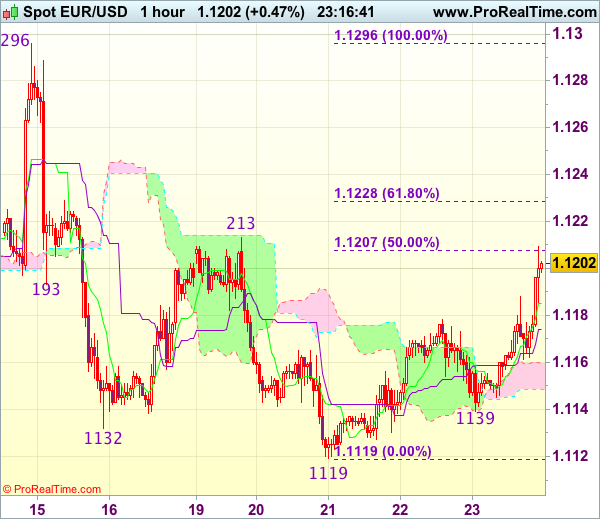

Trade Idea Wrap-up: EUR/USD – Stand aside

EUR/USD - 1.1202

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.1185

Kijun-Sen level : 1.1174

Ichimoku cloud top : 1.1160

Ichimoku cloud bottom : 1.1147

Original strategy :

Sell at 1.1210, Target: 1.1110, Stop: 1.1245

Position : -

Target : -

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

The single currency has surged again in NY morning, suggesting near term upside risk remains for the rebound from this week’s low of 1.1119 to extend gain to 1.1213 resistance, then towards 1.1228-30 ((61.8% Fibonacci retracement of 1.1296-1.1119), however, reckon upside would e limited to 1.1260-70 and price should falter well below resistance at 1.1296, bring retreat next week.

In view of this, would not chase this rise here and would be prudent to stand aside for now. Below the Kijun-Sen (now art 1.1174) would bring weakness towards 1.1139 support but break there is needed to revive bearishness and signal an intra-day top is formed, bring retest of 1.1119.

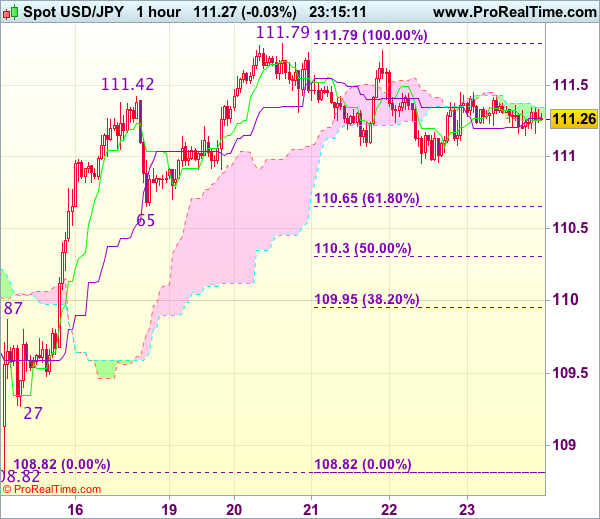

Trade Idea Wrap-up: USD/JPY – Buy at 110.65

USD/JPY - 111.25

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 111.26

Kijun-Sen level : 111.28

Ichimoku cloud top : 111.35

Ichimoku cloud bottom : 111.26

Original strategy :

Buy at 110.65, Target: 111.65, Stop: 110.30

Position : -

Target : -

Stop : -

New strategy :

Buy at 110.65, Target: 111.65, Stop: 110.30

Position : -

Target : -

Stop : -

Although the greenback found support just below 111.00 level, near term downside risk remains for the erratic fall from this week’s high of 111.79 to bring retracement of recent rise and weakness to 110.90-95 cannot be ruled out, however, reckon previous support at 110.65 would limit downside and bring another rise later, above 111.45-50 would bring retest of 111.79 but break there is needed to confirm the rise from 108.82 low has resumed and extend headway to 111.90-95 (50% projection of 108.82-111.42-110.65), however, upside should be limited to resistance at 112.13 and 112.25 (61.8% Fibonacci retracement of 114.37-108.82 and 61.8% projection) should hold.

In view of this, would not chase this rise here and we are looking to buy dollar on pullback as 110.65 support should limit downside. Below 110.30-35 (50% Fibonacci retracement of 108.82-111.79 and previous resistance turned support) would abort and signal a temporary top has been formed instead, risk weakness towards 109.95-00 (61.8% Fibonacci retracement).

Trade Idea: EUR/GBP – Buy at 0.8660

EUR/GBP - 0.8795

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term up

Original strategy :

Buy at 0.8660, Target: 0.8860, Stop: 0.8620

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.8660, Target: 0.8860, Stop: 0.8620

Position : -

Target : -

Stop : -

Euro’s retreat after meeting resistance at 0.8846 earlier this week has retained our view that further consolidation below recent high at 0.8866 would be seen and another corrective fall to 0.8740-50 cannot be ruled out, however, downside should be limited to support at 0.8652, bring another rise later. Above said resistance at 0.8846 would signal the retreat from 0.8866 has ended, bring retest of this last week’s high but break there is needed to confirm recent erratic upmove from 0.8304 low has resumed and extend further gain to 0.8880, then 0.8900, having said that, as broad outlook remains consolidative, reckon current c leg of larger degree wave b should be limited to 0.8950 and price should falter well below 0.9000 psychological level.

In view of this, we are looking to buy euro on subsequent pullback but one should exit on such rise. Below 0.8650 would defer and risk test of 0.8620, a break below there would signal top is formed instead, bring further fall to 0.8620, then 0.8600 which is likely to hold from here.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.