Sample Category Title

GBP/USD Mid-Day Outlook

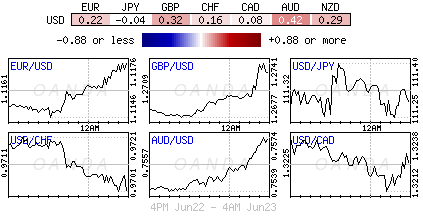

Daily Pivots: (S1) 1.2660; (P) 1.2675; (R1) 1.2697; More...

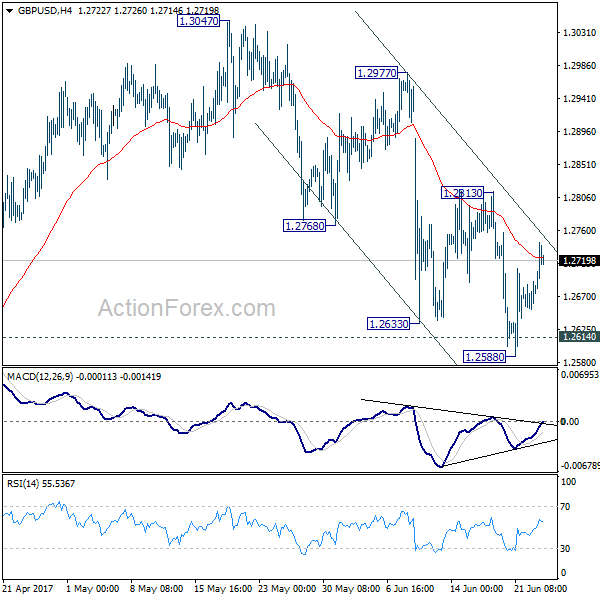

While GBP/USD rebounds today, it's staying below 1.2813 resistance. Intraday bias stays neutral first. At this point, we're still favoring the bearish case that consolidation pattern from 1.1946 has completed at 1.3047 already. Sustained break of 1.2614 resistance turned support should confirm our bearish view and target a test on 1.1946 low next. However, break of 1.2813 resistance will dampen our view and turn bias back to the upside for 1.3047 and above.

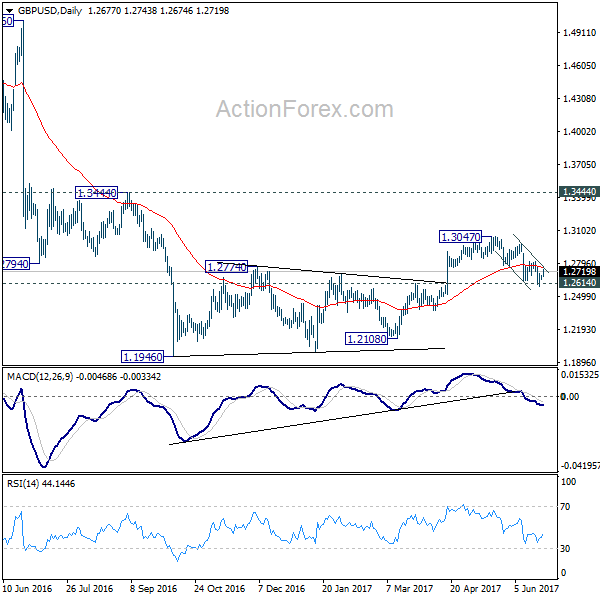

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. Price actions from 1.1946 medium term low are seen as a consolidation pattern, which could have completed after hitting 55 week EMA. Break of 1.1946 low will target 61.8% projection of 1.5016 to 1.1946 from 1.3047 at 1.1150 next. In case the consolidation from 1.1946 extends, outlook will stay remain bearish as long as 1.3444 resistance holds.

Trade Idea Update: USD/JPY – Buy at 110.65

USD/JPY - 111.30

Original strategy :

Buy at 110.65, Target: 111.65, Stop: 110.30

Position : -

Target : -

Stop : -

New strategy :

Buy at 110.65, Target: 111.65, Stop: 110.30

Position : -

Target : -

Stop : -

Although the greenback found support just below 111.00 level, near term downside risk remains for the erratic fall from this week’s high of 111.79 to bring retracement of recent rise and weakness to 110.90-95 cannot be ruled out, however, reckon previous support at 110.65 would limit downside and bring another rise later, above 111.45-50 would bring retest of 111.79 but break there is needed to confirm the rise from 108.82 low has resumed and extend headway to 111.90-95 (50% projection of 108.82-111.42-110.65), however, upside should be limited to resistance at 112.13 and 112.25 (61.8% Fibonacci retracement of 114.37-108.82 and 61.8% projection) should hold.

In view of this, would not chase this rise here and we are looking to buy dollar on pullback as 110.65 support should limit downside. Below 110.30-35 (50% Fibonacci retracement of 108.82-111.79 and previous resistance turned support) would abort and signal a temporary top has been formed instead, risk weakness towards 109.95-00 (61.8% Fibonacci retracement).

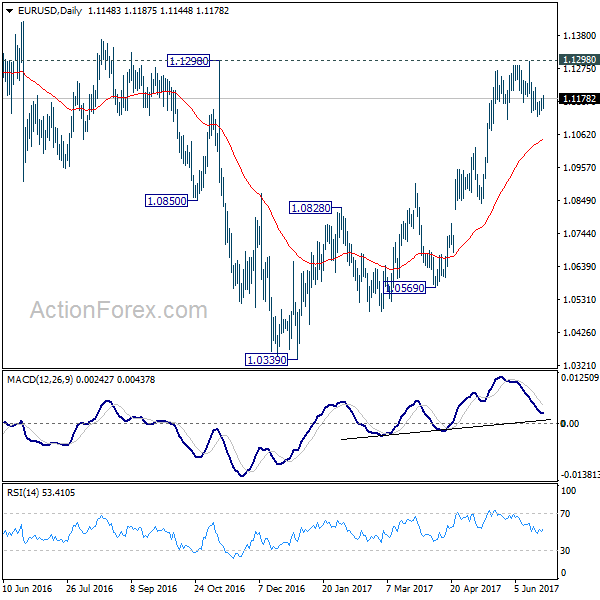

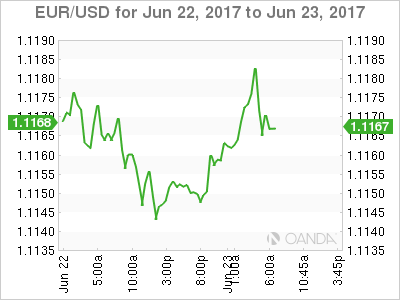

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1134; (P) 1.1156 (R1) 1.1172; More....

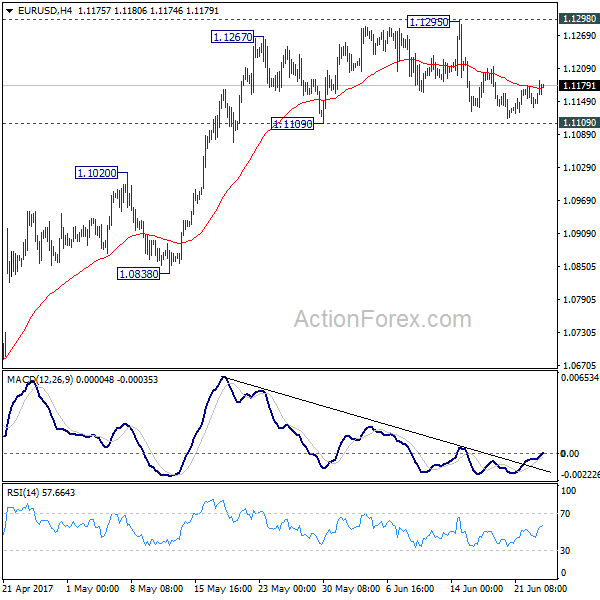

Intraday bias in EUR/USD remains neutral as it's staying in consolidation in range of 1.1109/1295. There is no confirmation of near term reversal yet. And focus remains on 1.1298 key resistance. Decisive break of 1.1298 key resistance will carry larger bullish implication and extend the whole rise from 1.0339 to 1.1615 resistance next. On the downside, firm break of 1.1109 support will indicate short term topping and rejection from 1.1298. In such case, intraday bias will be turned to the downside for 1.0838 support.

In the bigger picture, the case for medium term reversal continues to build up with EUR/USD staying far above 55 week EMA (now at 1.0932). Also, bullish convergence condition is seen in weekly MACD. Focus will now be on 1.1298 key resistance. Rejection from there will maintain medium term bearishness and would extend the whole down trend from 1.6039 (2008 high). However, firm break of 1.1298 will indicate reversal. In such case, further rally would be seen back to 1.2042 support turned resistance next.

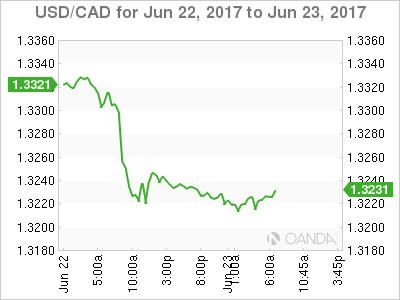

Disappointing Data Keeps Euro and Canadian Dollar in Range

Canadian Dollar weakens notably in early US session after inflation data missed expectation. Headline CPI slowed to 1.3% yoy in May, down from 1.6% yoy, below consensus of 1.5% yoy. CPI core - common was unchanged at 1.4% yoy, CPI core - median slowed to 1.5% yoy from 1.6% yoy. CPI core - trim slowed to 1.2% yoy from 1.3% yoy. The Loonie has been lifted recently by the hawkish turn of BoC Governor Stephen Poloz. And it tried to resume the rally yesterday after solid retail sales data. Today's tamer than expected inflation reading could now keep USD/CAD in range in near term. The real test will come when BoC announce rate decision again on July 12, when quarterly forecasts will also be released.

Euro recovers mildly against Dollar today but there is no follow through buying seen so far. Eurozone PMI manufacturing rose to 57.3 in June, up from 57.0 and beat expectation of 56.8. But Eurozone PMI services dropped to 54.7, down from 56.3 and missed expectation of 56.1. Germany PMI manufacturing dropped slightly to 59.3, down from 59.3, but beat expectation of 59.0. Germany PMI services dropped to 53.7, down from 55.4, below expectation of 55.4. France PMI manufacturing rose to 55.0, up from 53.8 and beat expectation of 54.0. But France PMI services dropped to 55.3, down from 57.2 and missed expectation of 57.0.

While the set of data is overall disappointing, Markit chief business economist Chris Williamson noted that "at the moment I'm not too worried about it." And "we may be reaching the stage where growth has been strong for quite a few months and we are hitting a few ceilings in terms of degrees to which firms can expand capacity." Also, he noted that there it's not clear what the drop in PMI services is about and he "inclined to treat it just as some payback for the sheer strength of growth in recent months,"

In Japan, PMI manufacturing dropped to 52.0 in June, down from 53.1 and missed expectation of 53.4. Looking at some details, new orders dropped to 51.3, down from 53.4, and hit the lowest level since November. New export orders also dropped to 52.5, down from 53.0. Markit noted that "slower growth was signaled in June, with both orders and output rising at the weakest rates since late last year amid reports of a slight softening in market conditions." Nonetheless, "demand is holding up well, and the sector continues to operate within a solid growth range."

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1134; (P) 1.1156 (R1) 1.1172; More....

Intraday bias in EUR/USD remains neutral as it's staying in consolidation in range of 1.1109/1295. There is no confirmation of near term reversal yet. And focus remains on 1.1298 key resistance. Decisive break of 1.1298 key resistance will carry larger bullish implication and extend the whole rise from 1.0339 to 1.1615 resistance next. On the downside, firm break of 1.1109 support will indicate short term topping and rejection from 1.1298. In such case, intraday bias will be turned to the downside for 1.0838 support.

In the bigger picture, the case for medium term reversal continues to build up with EUR/USD staying far above 55 week EMA (now at 1.0932). Also, bullish convergence condition is seen in weekly MACD. Focus will now be on 1.1298 key resistance. Rejection from there will maintain medium term bearishness and would extend the whole down trend from 1.6039 (2008 high). However, firm break of 1.1298 will indicate reversal. In such case, further rally would be seen back to 1.2042 support turned resistance next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Jun P | 52 | 53.4 | 53.1 | |

| 07:00 | EUR | France Manufacturing PMI Jun P | 55 | 54 | 53.8 | |

| 07:00 | EUR | France Services PMI Jun P | 55.3 | 57 | 57.2 | |

| 07:30 | EUR | Germany Manufacturing PMI Jun P | 59.3 | 59 | 59.5 | |

| 07:30 | EUR | Germany Services PMI Jun P | 53.7 | 55.4 | 55.4 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Jun P | 57.3 | 56.8 | 57 | |

| 08:00 | EUR | Eurozone Services PMI Jun P | 54.7 | 56.1 | 56.3 | |

| 12:30 | CAD | CPI M/M May | 0.10% | 0.20% | 0.40% | |

| 12:30 | CAD | CPI Y/Y May | 1.30% | 1.50% | 1.60% | |

| 12:30 | CAD | CPI Core - Common Y/Y May | 1.30% | 1.40% | 1.30% | |

| 12:30 | CAD | CPI Core - Median Y/Y May | 1.50% | 1.60% | ||

| 12:30 | CAD | CPI Core - Trim Y/Y May | 1.20% | 1.30% | ||

| 13:45 | USD | US Manufacturing PMI Jun P | 52.9 | 52.7 | ||

| 13:45 | USD | US Services PMI Jun P | 53.9 | 53.6 | ||

| 14:00 | USD | New Home Sales May | 593K | 569K |

GBPUSD – Recovers Higher Within Trading Range

GBPUSD - The pair continues to face upside pressure but within its established range. Support lies at the 1.2700 level where a break will turn attention to the 1.2650 level. Further down, support lies at the 1.2600 level. Below here will set the stage for more weakness towards the 1.2550 level. Conversely, resistance stands at the 1.2800 levels with a turn above here allowing more strength to build up towards the 1.2850 level. Further out, resistance resides at the 1.2900 level followed by the 1.2950 level. On the whole, GBPUSD continues to face upside threats.

DAX Slips As Oil Prices Remain Under Pressure

The DAX index has posted losses in the Friday session. Currently, the index is at 12,730.25 points, down 0.50%. There was positive news on the manufacturing front, as German and Eurozone Manufacturing PMIs beat their estimates. However, data from the services sector failed to keep pace, as German and Eurozone Services PMIs both missed expectations.

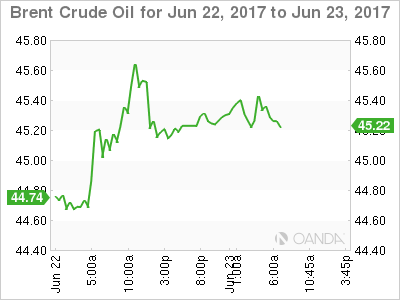

Global stock markets continued to contend with low oil prices, which are weighing on investor confidence. Brent crude has plunged 10.8% in June, as crude trades around $45 a barrel. As crude prices continue to fall, there are rising concerns of disinflation. The US, Japan and much of Europe are struggling with low inflation, and lower levels could hamper growth. OPEC members continue to discuss lowering production, but the markets do not seem impressed. OPEC is already bound by a production agreement and compliance is over 100%, yet this has failed to prevent the collapse in oil prices. Another headache for major producers is the increase in production from the US, Libya and Nigeria.

A stronger global economy has spurred demand for exports from the euro-area, and this has boosted the manufacturing sectors in Germany and the eurozone. German Manufacturing PMI ticked lower to 59.3 in May, above the forecast of 59.1 points. Germany's manufacturing sector continues to show strong growth, and the April reading of 59.4 was the highest since March 2011. The news was also positive in the eurozone, as Manufacturing PMI improved for a tenth straight month, climbing to 57.3 points. This beat the estimate of 56.9 points. On Thursday, the ECB's economic bulletin projected solid growth in the euro-area in the second quarter, buoyed by low inflation rates and stronger domestic demand.

The German economy remains robust, with a strong labor market and stronger consumer and state spending. As well, the manufacturing and export sectors are booming due to increased global demand for German products. There were cries of despair in political and business circles in Europe when Donald Trump was elected, as Trump campaigned on a protectionist, 'America first' agenda. However, these concerns have largely died down, as the eurozone economy has improved and Trump has been in damage control mode, as he focuses on domestic scandals. Earlier this week, the well-respected German BDI Federation of Industry added its voice to the chorus of accolades for the German economy. The BDI said that Germany's economic output would increase by 1.5% this year. At the same time, the BDI counseled caution, noting that the economy had been buoyed by a weaker euro, lower oil prices and the ECB's accommodative monetary policy. All three are ‘external factors', in the sense that Germany has limited influence on them, and a significant change in any one factor could weigh on economic growth.

US 30 Index Declines To Reach One-Week Low, Medium-Term Outlook Remains Bullish

The US 30 index is on its fourth day of declines after reaching an all-time high of 21,539.10 on Monday. Today's decline has led the index to record a one-week low of 21,340.70.

Technical indicators such as the RSI and stochastics are pointing to a change in short-term momentum for the index. The RSI is theoretically in bullish territory at 60, but it has steeply fallen from overbought territory to reach its current level. In addition, the indicator remains downward sloping. Meanwhile, the stochastics are projecting a similar picture with the %K line in bearish territory (after recording a steep fall) and below the slow %D line.

On the upside, Monday's all-time high of 21,539.10 is likely to act as a point of resistance. Further up, the 21,600.00 level might act as psychological barrier to upside movements as well.

On the downside, today's decline violated the Tenkan-sen line (red), which was providing intra-day support at 21,378.00. The 21,300.00 handle, a potential psychological level, could provide some support. Another likely important support area is the one formed by the Kijun-sen line (blue) at 21,089.10 and the 21,000.00 psychological mark. Notice that the 50-day moving average (MA) at 21,020.00 is also in between these two points.

As regards the medium-term outlook, it remains bullish given the significant advancing by the index since the start of the year. Further supporting this is the fact that the index level is comfortably above the 50- and 200-day MAs as well as the Ichimoku cloud top, while both MAs are currently upward sloping. A note of caution though as the considerable divergence from the 200-day MA might be indicative of an overextended rally.

Overall, the near-term momentum is currently looking negative and the medium-term is bullish.

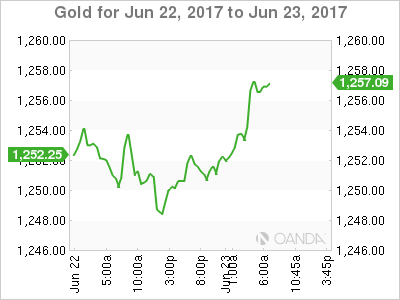

Technical Outlook: Spot Gold – Extended Recovery Eyes $1262/64 Barriers

Spot Gold extends recovery from week’s low at $1240 and took out initial barrier at $1254 (Fibo 23.6% of $1296/$1240 descend / 10SMA).

Correction may extend through $1259 (55SMA / daily Tenkan-sen) towards strong resistance at $1262/64 (Fibo 38.2% / 20SMA) as slow stochastic on daily chart is heading north after reversal from O/B territory and showing more room at the upside.

Close above $1264 is needed to generate strong signal for extended recovery.

Broken 10SMA now acts as initial support at $1255, followed by more significant broken 100SMA at $1248, loss of which would signal an end of corrective phase and shift focus towards $1240 and 200SMA at $1236.

Res: 1259, 1262, 1264, 1268

Sup: 1255, 1248, 1245, 1240

Technical Outlook: WTI Oil – Limited Upside Action Despite Strong Bullish Signals On RSI/Slow Stoch Reversal

WTI oil holds positive tone on Friday but upside attempts remain limited following Thursday's strong upside rejection after brief probe above $43.00 barrier.

Negative technicals and sentiment maintain strong bearish pressure for retest of temporary footstep at $42.04 (21 June low) and extension of bear-leg from $51.98 (25 May high) towards next target at $40.63 (weekly cloud base / 50% retracement of $26.04/$55.22 recovery).

On the other side, strong bullish signal is coming from daily RSI slow stochastic reversal from oversold territory, which may spark fresh recovery rally towards upper pivots at $43.82/$44.13 (Fibo 38.2% of $46.69/$42.04 / falling 10SMA).

Res: 43.14, 43.30, 43.82, 44.13

Sup: 42.67, 42.26, 42.04, 41.09

Fed Talk Provides Little Support For Dollar

Global equities are trading mixed now that this weeks Fed speakers have done little to alter market projections for the path of interest rate. Crude oil is poised for its fifth straight week of declines.

The 'mighty' USD peaked at a one-month high on Tuesday after the Fed did the expected, hiked interest rates last week and left the door ajar for further monetary tightening later in the year.

However, with fed fund futures odds of that happening straddling atop of +41%, the greenback has been stuck in a tight range ever since, pending fresh catalysts.

Nonetheless, the market is waiting on U.S data due next week – which include the June consumer confidence indicator, pending home sales, crude oil inventories, revised Q1 GDP and the PCE price index – for direction.

Yet, for a stronger conviction, what really matters for the dollar are wages and inflation-related data which occurs in a fortnight with non-farm payrolls (NFP).

This market snooze fest, aside from the commodity currency moves this week – CAD in particular – investors have to be patient and pick their moments now that central banks again have a stranglehold on currency markets.

Note: Today, the Fed's Bullard, Mester and Powell cap a busy week for speeches from U.S policy makers.

1. Global stocks keep their head above water

Global equities, helped by a rebound in tech shares in particular, remain resilient despite investor concerns about a policy misstep from the Fed – inflation is lagging – and a rout in the oil market that extended for a fifth-week.

In Japan, the Nikkei share average finished this week little changed as dollar-yen levels steadied (¥111.28). The broader Topix added less than +0.1%, while down-under, Australia's S&P/ASX 200 Index gained +0.2%.

In Hong Kong, the Hang Seng China Enterprises Index added +0.3%, while the Hang Seng Index rose less than +0.1%.

In China, blue chips stocks ended at an 18-month high, buoyed by MSCI inclusion of mainland shares in its key index. The blue-chip CSI300 index settled up +0.9%, while the Shanghai Composite Index added +0.3%.

In Europe, indices are trading modestly lower across the board with continued weaker oil prices weighing.

U.S stocks are set to open in the 'black' (+0.1%).

Indices: Stoxx600 -0.1% at 388, FTSE -0.3% at 7416, DAX -0.3% at 12757, CAC-40 -0.2% at 5271, IBEX-35 -0.5% at 10656, FTSE MIB -0.3% at 20862, SMI -0.2% at 9034, S&P 500 Futures +0.1%.

2. Oil edges up, but still set for biggest H1 fall in 20-years, gold shines

Overnight, oil prices have edged a tad higher, but remains on course for its worst first-half decline in almost two decades as production cuts have failed to sufficiently reduce oversupply.

Brent crude futures are up +28c at +$45.50 a barrel, while West Texas Intermediate (WTI) crude futures are trading at +$43.04 a barrel, up +30c from yesterday's close.

Since peaking in late February, crude has dropped around -20% in the wake of the initial OPEC-led production cut.

Note: OPEC and non-OPEC oil producers' compliance with the output deal reached 106 percent in May. However, a number of producers – notably Iraq, Saudi Arabia and Russia – aggressively ramped up output in the run-up to the deal, while U.S producers, Libya and Nigeria are exempt from the cuts.

Ahead of the U.S open, gold prices (+0.6% at +$1,257.1 an ounce) have climbed to a weekly high, supported by a lower dollar and economic and political uncertainty around the world. However, the prospect of further interest rate hikes by the Fed is expected to limit gains.

3. German Yield Spreads Poised to Reach Pre-Trump Levels

The Treasury/Bund 10-year gap currently stands at +191.3 bps, down from +233.38 bps in late December.

Some dealers believe that the risk that the Fed may be moving ahead of the curve in its interest rate-rise path, given declining inflation rates and a shift in political risk from Europe into the U.S, argues for a tighter yield spread between the two bonds (U.S 10's to outperform German debt product). For many, the technical target is around +165 bps, a level last seen before Trumps U.S presidential win.

Overnight, the yield on 10-year Treasuries has backed up +1 bps to +2.16%. In the U.K 10-year yields have added +3 bps to +1.05%, while French OAT's and German Bund yields are little changed.

Note: The Fed has raised interest rates four times since late 2015, and three times since the U.S election last November. U.S Treasury yields have fallen around -50 bps since the March rate hike.

4. The 'Big' dollar under pressure

Overnight, the U.S dollar has traded mostly on the back foot. The EUR (€1.1174) has found support following better-than-expected manufacturing data in the eurozone (see below).

Sterling (£1.2727) rises after outgoing BoE member Kristin Forbes said in a speech yesterday that there were “compelling” reasons why a U.K interest rate rise should not be delayed. Ms. Forbes leaves the MPC next week, but the comment carries weight, as she is not a lone voice, with three out of eight members voting to raise rates at this month's BoE meeting. The pound 'bear' expect gains to be limited due to political and Brexit uncertainty.

Note: It's exactly a year today since Britain voted to leave the E.U – in the past 12-months the pound has fallen more than -15% outright, and almost -13% versus the EUR.

Commodity-linked currencies continue to hold onto their significant gains made yesterday following a rebound in crude oil prices from 10-month lows – CAD in particular is trading flat (C$1.3232).

5. Eurozone economy slows, but

Data this morning showed that the eurozone's economy slowed slightly this month, but it still had its strongest quarter in more than six years, according to a survey of activity in the manufacturing and services sectors.

The composite PMI fell to 55.7 from 56.8 in May, a five-month low. The market was expecting it to fall to 56.6; however, it still leaves the eurozone economy growing at its fastest rate since the start of 2011.