Sample Category Title

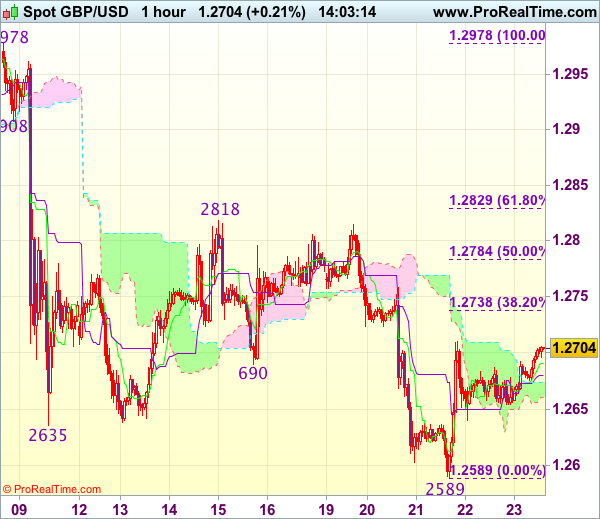

Trade Idea : GBP/USD – Hold short entered at 1.2695

GBP/USD - 1.2702

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2671

Kijun-Sen level : 1.2672

Ichimoku cloud top : 1.2702

Ichimoku cloud bottom : 1.2650

Original strategy :

Sold at 1.2695, Target: 1.2595, Stop: 1.2710

Position : - Short at 1.2695

Target : - 1.2595

Stop : - 1.2710

New strategy :

Hold short entered at 1.2695, Target: 1.2595, Stop: 1.2710

Position : - Short at 1.2695

Target : - 1.2595

Stop : - 1.2710

Although cable has rebounded again and upside risk remains, as long as 1.2710 holds, mild downside bias remains for another decline, below 1.2635-40 would bring another fall towards said support but break there is needed to retain bearishness and signal recent decline has resumed for weakness towards 1.2550, however, oversold condition should limit downside to 1.2520-25.

In view of this, we are holding on to our short position entered at 1.2695. Only above 1.2720-25 would abort and suggest low has been formed instead, bring a stronger rebound to 1.2755-60 and possibly 1.2780 but price should falter below indicated strong resistance at 1.2818.

Trade Idea : EUR/USD – Sell at 1.1200

EUR/USD - 1.1167

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.1158

Kijun-Sen level : 1.1159

Ichimoku cloud top : 1.1158

Ichimoku cloud bottom : 1.1146

Original strategy :

Sell at 1.1200, Target: 1.1100, Stop: 1.1235

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1200, Target: 1.1100, Stop: 1.1235

Position : -

Target : -

Stop : -

The single currency found support just below 1.1140 and has recovered, retaining our view that further consolidation above this week’s low at 1.1119 would be seen and near term upside risk remains for retracement to 1.1185-90 (38.2% Fibonacci retracement of 1.1296-1.1119), however, upside should be limited and price should falter below 1.1207-13 (50% Fibonacci retracement and previous resistance), bring another decline later, below 1.1135-40 would suggest the rebound from 1.1119 has ended, bring retest of this level, below there would confirm recent decline has resumed for further weakness to previous support at 1.1109, then towards 1.1075-80.

In view of this, we are looking to sell euro on recovery as 1.1195-00 should limit upside. Only above 1.1213 resistance would defer and risk a stronger rebound to 1.1230-35 but upside should be limited to 1.1260-70, bring another decline later.

Trade Idea : USD/JPY – Buy at 110.65

USD/JPY - 111.23

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 111.33

Kijun-Sen level : 111.21

Ichimoku cloud top : 111.37

Ichimoku cloud bottom : 111.27

Original strategy :

Buy at 110.65, Target: 111.65, Stop: 110.30

Position : -

Target : -

Stop : -

New strategy :

Buy at 110.65, Target: 111.65, Stop: 110.30

Position : -

Target : -

Stop : -

Although the greenback found support just below 111.00 level, near term downside risk remains for the erratic fall from this week’s high of 111.79 to bring retracement of recent rise and weakness to 110.90-95 cannot be ruled out, however, reckon previous support at 110.65 would limit downside and bring another rise later, above 111.45-50 would bring retest of 111.79 but break there is needed to confirm the rise from 108.82 low has resumed and extend headway to 111.90-95 (50% projection of 108.82-111.42-110.65), however, upside should be limited to resistance at 112.13 and 112.25 (61.8% Fibonacci retracement of 114.37-108.82 and 61.8% projection) should hold.

In view of this, would not chase this rise here and we are looking to buy dollar on pullback as 110.65 support should limit downside. Below 110.30-35 (50% Fibonacci retracement of 108.82-111.79 and previous resistance turned support) would abort and signal a temporary top has been formed instead, risk weakness towards 109.95-00 (61.8% Fibonacci retracement).

Market Update – Asian Session: Japan Prelim PMI Slides To 6-Month Low

Asia Mid-Session Market Update: Japan Prelim PMI slides to 6-month low; North Korea carries out another rocket engine test

US Session Highlights

(US) INITIAL JOBLESS CLAIMS: 241K V 240KE; CONTINUING CLAIMS: 1.944M V 1.93ME

(US) APR FHFA HOUSE PRICE INDEX M/M: 0.7% V 0.5%E

Stocks opened to the upside this morning, with the Dow gaining 50 points, before retracing late afternoon. Other major markets followed suit, with both the Dow and the S&P wiping out all their gains and closing slightly down on the day. The Nasdaq managed to post a small gain, and the Russell kept 0.4% of it gains for the day. In the S&P, the Health Care sector gained 1.1%, helping to pare losses from Consumer Staples and Financials, which lost 0.6% each.

US markets on close: Dow -0.1%, S&P500 -0.1%, Nasdaq flat

Best Sector in S&P500: Health Care

Worst Sector in S&P500: Consumer Staples

Biggest gainers: ORCL +8.6%; SPLS +6.2%; KMX +4.6%

Biggest losers: ACN -4.0%; DPS -3.6%; WLTW -2.4%

At the close: VIX 10.5 (-0.3pts); Treasuries: 2-yr 1.35% (flat), 10-yr 2.15% (-1bps), 30-yr 2.72% (flat)

US movers afterhours

SGH Reports Q3 $0.62 v $0.62e, Rev $207M v $205Me; Guides Q4 $0.62-0.66 v $0.61e, Rev $205-215M v $213Me, gross margin 21-23%; +2.1% afterhours

BBBY Reports Q1 $0.58 adj v $0.66e, Rev $2.74B v $2.80Be; Affirms FY17 EPS to decline low single digits to 10%, implies low end $4.12 v $4.29e; -7.4% afterhours

Politics

(NZ) Latest Roy Morgan survey shows ruling National Party support rise 3.5pts to 46.5% following FY17/18 budget - NZ press

(VE) Venezuela opposition to block streets nationwide on Friday

Key economic data

(JP) JAPAN JUNE PRELIMINARY PMI MANUFACTURING: 52.0 V 53.1 PRIOR; 9th straight month of expansion; 6-month low

Speakers and Press

China

(CN) PBoC: China banks are confident about June-end liquidity - Chinese press

(CN) China Banking Regulator (CBRC): China banks' NPL ratio fell 16bps y/y to 1.99% in May

(CN) China said to cut retail gasoline price by CNY250/ton starting June 24th - press

Australia/New Zealand

(NZ) Quotable Value (QV): Average cost of building a home in New Zealand rose 3.5% y/y in May - NZ press

Korea

(KR) US officials: North Korea has carried out another rocket engine test, likely for small stage of 3-stage ICBM type rocket engine - press

Asian Equity Indices/Futures (00:30ET)

Nikkei +0.2%, Hang Seng +0.1%, Shanghai Composite -0.7%, ASX200 +0.0%, Kospi +0.1%

Equity Futures: S&P500 +0.1%; Nasdaq +0.1%, Dax +0.1%, FTSE100 flat

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.1160-1.1170; JPY 110.95-111.45; AUD 0.7540-0.7560; NZD 0.7200-0.7270

Aug Gold +0.7% at 1,254/oz; Aug Crude Oil +0.1% at $42.55/brl; July Copper -0.1% at $2.59/lb

iShares Silver Trust ETF daily holdings rise to 10,571 tonnes from 10,504 tonnes prior

(CN) PBOC SETS YUAN MID POINT AT 6.8238 V 6.8197 PRIOR; Weakest Yuan fix since May 31st and 4th straight weaker setting

(CN) PBoC: To skip today's open market operation (OMO)

(CN) China Finance Ministry sells 3-month bonds at 3.376%

(AU) Australia Finance Ministry (AOFM) sells A$600M in 1.75% 2020 bonds; avg yield 1.843%; bid-to-cover 5.29x

Asia equities notable movers

Australia

CSR (CSR) +2.0%; Guides FY17/18 earnings to rise y/y; Chairman to stand down at the 2018 AGM

Infigen (IFN) -4.9%; Cuts FY17 EBITDA to A$136-138M from A$147M prior forecast

Japan

Takata (7312) +45.5%; Toyota, Honda and Nissan will continue to financially support Takata after it files for bankruptcy protection - Nikkei

Don Quixote (7532) +0.2%; FY16/17 Rev said to rise 10% to ~¥830B; Op profit seen around ¥46.5B, above ¥45.5B prior forecast - Nikkei

Toshiba (6502) -4.2%; Reportedly to request securities report filing deadline extension - Japan press

Hong Kong

Lonking Holdings Limited (3339) +3.0%; Issues positive H1 profit alert

China Electric (85) -2.4%; Guides H1 profit -90% to -80% y/y due to prior one off gain

Bauhaus International Holdings (483) +31.3%; Reports FY17 (HK$) Net 64.9M v 52.9M y/y; Rev 1.31B v 1.51B y/y; SSS -10%

Aussie Dollar Trading Higher In The Morning Session

For the 24 hours to 23:00 GMT, the AUD marginally declined against the USD and closed at 0.7541.

LME Copper prices rose 1.5% or $86.0/MT to $5736.0/MT. Aluminium prices rose 0.4% or $6.5/MT to $1872.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7546, with the AUD trading 0.07% higher against the USD from yesterday’s close.

The pair is expected to find support at 0.7534, and a fall through could take it to the next support level of 0.7521. The pair is expected to find its first resistance at 0.7560, and a rise through could take it to the next resistance level of 0.7573.

Next week, traders would focus on Australia’s HIA new home sales and private sector credit data.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Consumer Confidence Zoomed To A 16-Year High Level In June

For the 24 hours to 23:00 GMT, the EUR declined 0.15% against the USD and closed at 1.1165.

On the data front, the Euro-zone's flash consumer confidence index improved more-than-expected to a level of -1.3 in June, notching its highest level since April 2001, buoyed by improved economic outlook after recent data signalled that the region's economy has gathered pace. Markets were expecting the index to climb to a level of -3.0, compared to a reading of -3.3 in the prior month.

Meanwhile, the European Central Bank (ECB), in its latest economic bulletin report, noted that the common currency region remains on course for stronger growth this quarter. Further, the central bank added that underlying inflation continues to remain subdued and has yet to show a convincing upward trend.

Macroeconomic data indicated that the number of Americans filing for fresh jobless claims advanced to a level of 241.0K in the week ended 17 June, slightly more than market consensus for a rise to a level of 240.0K. In the prior week, initial jobless claims had registered a revised reading of 238.0K. On the contrary, the nation's housing price index climbed 0.7% on a monthly basis in April, compared to a revised similar rise in the prior month, while market participants had envisaged for a gain of 0.5%. Also, the nation's leading indicator increased 0.3% on a monthly basis in May, at par with market expectations. In the prior month, leading indicator had registered a revised rise of 0.2%.

In the Asian session, at GMT0300, the pair is trading at 1.1158, with the EUR trading 0.09% higher against the USD from yesterday's close.

The pair is expected to find support at 1.1139, and a fall through could take it to the next support level of 1.1119. The pair is expected to find its first resistance at 1.1178, and a rise through could take it to the next resistance level of 1.1197.

Ahead in the day, investors will keep a close watch on the flash Markit manufacturing and services PMIs data for June across the Euro-zone, to gauge strength in the region's economy. Moreover, in the US, the preliminary Markit manufacturing and services PMIs for June along with new home sales data for May, slated to release later in the day, will be on investors' radar.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Pound Trading Higher In The Asian Session

For the 24 hours to 23:00 GMT, the GBP rose 0.14% against the USD and closed at 1.2679.

In economic news, data revealed that UK’s CBI industrial trends total orders surprisingly advanced to a nearly 30-year high level of 16.0 in June, mainly driven by faster growth in export orders. Meanwhile, markets expected it to ease to a level of 7.0, from a reading of 9.0 reported in the preceding month.

In the Asian session, at GMT0300, the pair is trading at 1.2696, with the GBP trading 0.13% higher against the USD from yesterday’s close.

The pair is expected to find support at 1.2667, and a fall through could take it to the next support level of 1.2637. The pair is expected to find its first resistance at 1.2713, and a rise through could take it to the next resistance level of 1.2729.

With no major economic releases in the UK today, investors will look forward to Britain’s final GDP figures, BBA mortgage applications, GfK consumer confidence and net consumer credit data, all slated to release next week.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japan’s Manufacturing Sector Growth Slowest Since November 2016 In June

For the 24 hours to 23:00 GMT, the USD rose 0.16% against the JPY and closed at 111.30.

Yesterday, the Japanese Government raised its assessment of the economy for the first time in six months, noting that the economy is on a gradual recovery path aided by increased consumer spending and capital investment.

In the Asian session, at GMT0300, the pair is trading at 111.36, with the USD trading marginally higher against the JPY from yesterday's close.

Overnight data revealed that Japan's preliminary Nikkei manufacturing PMI dropped to a level of 52.0 in June, reducing the nation's manufacturing sector growth to its weakest level in seven months. In the prior month, the PMI had recorded a reading of 53.1.

The pair is expected to find support at 111.06, and a fall through could take it to the next support level of 110.75. The pair is expected to find its first resistance at 111.56, and a rise through could take it to the next resistance level of 111.75.

Going forward, Japan's jobless rate, consumer price index, industrial production and retail trade data, all slated to release next week, will attract market attention.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Swiss Trade Surplus Rose In May

For the 24 hours to 23:00 GMT, the USD declined 0.08% against the CHF and closed at 0.9719.

On the economic front, Switzerland trade surplus widened to a level of CHF3.40 billion in May, as exports grew faster than imports. The nation had reported a revised surplus of CHF1.96 billion in the prior month.

In the Asian session, at GMT0300, the pair is trading at 0.9711, with the USD trading 0.08% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9700, and a fall through could take it to the next support level of 0.9688. The pair is expected to find its first resistance at 0.9733, and a rise through could take it to the next resistance level of 0.9754.

Moving ahead, investors will eye Switzerland’s KOF institute summer economic forecast report, scheduled to release in a few hours.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Canadian Retail Sales Surged In April

For the 24 hours to 23:00 GMT, the USD declined 0.71% against the CAD and closed at 1.3233.

The Canadian Dollar gained ground, after Canada’s retail sales rose more-than-anticipated by 0.8% MoM in April, boosting optimism over the state of the economy and intensifying hopes that the Bank of Canada will raise interest rates at its July meeting. Retail sales had recorded a revised advance of 0.5% in the previous month, while markets were expecting for a gain of 0.3%.

In the Asian session, at GMT0300, the pair is trading at 1.3228, with the USD trading a tad lower against the CAD from yesterday’s close.

The pair is expected to find support at 1.3178, and a fall through could take it to the next support level of 1.3128. The pair is expected to find its first resistance at 1.3308, and a rise through could take it to the next resistance level of 1.3388.

This afternoon will bring a crucial Canadian release, namely the consumer price index for May.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.