Sample Category Title

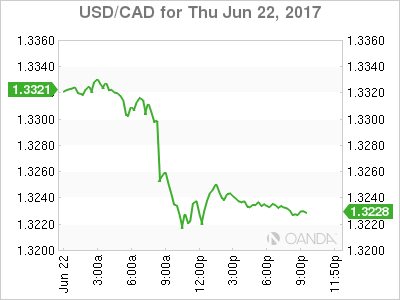

USD/CAD Canadian Dollar Higher After Retail Sales And Oil Gains

The Canadian dollar rose on Thursday after the release of retail sales data showed a gain of 0.8 percent and an even bigger jump when excluding auto sales. Core retail sales surged 1.5 percent validating the view of the Bank of Canada (BoC) on economic growth. Second quarter growth appears solid and is well within what is needed for a rate hike before the end of the year. Inflation data out on Friday, June 23 at 8:30 am EDT will give freighter insight into the state of the Canadian economy.

Canadian policy makers have been worried about the rise of household debt and the retail sales gain is mixed news for that reason. Housing and auto expenditures have risen with Canadian personal debt up to 166 percent of income. Core inflation will be an important data point for the central bank governor to decide when to pull the trigger on what appears is an impending interest rate move upwards. The loonie also benefited from gains in oil prices and the news that Berkshire Hathaway will provide a C$2 billion loan to Home Trust Capital and take a 38 percent stake in the troubled mortgage lender.

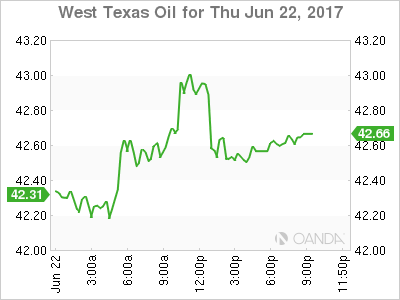

Oil prices bounced back slightly on Thursday after hitting 10 month lows. Energy prices are facing a losing battle with oversupply. The Organization of the Petroleum Exporting Countries (OPEC) and other major producers production cut has only stabilized prices, but as the US and others not part of the deal ramp up production prices have begun to slide down. Rifts between OPEC members are anticipated to escalate which could end up ending not only the agreement but the cooperation of the group as a whole.

Canadian Prime Minister Justin Trudeau commented on steel exports to the US. The Trump administration is researching the probability of steel exports posing a risk to the security of the US. Trudeau said it was “silly” for Canada to be on that list. Trade topics will begin to heat up as NAFTA renegotiations talks are expected to begin in mid August.

The USD/CAD lost 0.624 percent in the last 24 hours. The pair is trading at 1.3236 after the release of the Canadian retail sales and a bounce in oil prices boosted the loonie. The USD was held back by Fed member Bullard, a known policy dove, who called the projected rate path unnecessarily aggressive. He did say that the central bank should be reducing its balance sheet soon.

Retail sales painted a solid picture of the Canadian economy and it is now up to the inflation release on Friday to corroborate the optimistic view of the Bank of Canada (BoC) top policymakers.

Oil gained 0.299 percent on Thursday. The price of West Texas Intermediate is trading at $42.53 after touching lows of $42.05 earlier in the session. The price of oil continues to be caught between the OPEC oil production cut and the ramp up in production from other producers. Demand is proving to be a tie breaker as it remains subdued creating a glut even as some of the world’s largest producers are reducing their output. Compliance to the OPEC deal was 106 percent in May. Saudi Arabia has been the main driving force of the deal and has done the heavy lifting by over cutting when needed. The change in leadership in the kingdom could also signal a shift away from that role, or vice versa become even more vocal on the role of the OPEC and oil prices.

Market events to watch this week:

Friday, June 23

8:30 am CAD CPI m/m

Gold Edges Higher As May Heads To EU Summit

Gold has posted slight gains in the Thursday session. In North American trade, spot gold trading at $1248.63 per ounce. In economic news, US unemployment claims rose to 241 thousand, matching the forecast. On Friday, the US publishes New Home Sales.

The Federal Reserve has surprised the markets with its hawkish stance, as underscored by last week’s rate statement. The statement mentioned that the Fed plans to reduce its balance sheet later in 2017, although it did not provide further specifics. The balance sheet has ballooned to $4.5 trillion, which accumulated after the 2008 financial crisis, when the Fed went on a bond-buying spree to stimulate the economy. The reduction will be gradual, but still marks an important change in direction for the central bank. On Wednesday, FOMC member Patrick Harker said that he was in favor of the reduction commencing in September. The Fed has hinted at one more rate hike in the second half of 2017, and the markets have circled December as the most likely date for a rate move. The CME Group has pegged the odds of a September hike at just 13%, compared to 18% a week ago. However, the odds for a December increase are at 49%, and this could increase if Fed policymakers continue to wax positive about the economy.

Although gold prices have struggled recently, the growing uncertainty over Brexit has prevented gold from falling even lower. It’s been a rough few weeks for British Prime Minister Theresa May, who gambled by calling an election earlier this month and squandered her majority in parliament. May is trying to cobble together so her political situation remains precarious. May will attend an EU summit in Brussels on Thursday, and will brief the Europeans on how Britain plans to treat EU citizens living in the UK after Brexit. It will be interesting to see the reception she receives from the European leaders. There is plenty of bad blood between the parties, and the players on both sides will need to control their egos and tempers in order to keep the divorce process amicable. Formal negotiations between the UK and the EU began this week, and both sides agreed that the first round of talks was held in a constructive atmosphere. However, if the negotiations fall apart, the repercussions could send shock waves in the markets, and gold could be the big winner.

Canadian Confusion

The Canadian dollar surged again Thursday after a strong retail sales report but the real question is when the Bank of Canada will hike. The AUD and EUR were laggards in the otherwise low-key day. The June Japan manufacturing PMI is up next.

Canadian retail sales rose 0.8% compared to 0.3% expected. Excluding autos, sales were up 1.5% compared to 0.7% expected. The strong numbers have been ongoing for months and household consumption is now forecast to rise 5% this year.

In a surprise turn, the Bank of Canada shifted gears last week and shifted to a hawkish stance after remaining stubbornly neutral for months. USD/CAD is down 3 cents since including more than a cent on Thursday.

In that same timeframe, the chance of a BOC hike on July 12 has risen to 50/50 from 5%. Poloz has a reputation as someone who doesn't mind surprising the market.

But let's recap. All that Wilkins said is that the BOC “will assess whether all the stimulus in place as economic growth continues and, ideally, broadens further.” There is no urgency in that statement and a good retail sales report isn't enough to add any. Meanwhile, oil is down nearly 20% in a month.

The BOC will also have noted the recent decline in Toronto home prices. According to a preliminary realtor report released Wednesday, prices have tumbled 12% since April. By hiking, the BOC would be risking popping a bubble that's already deflating.

So come July 12, the trade will likely be to sell CAD ahead of the headlines but until then, it's tough to bet against an economy that's cranking out good numbers.

Another economy that's done well this year is Japan. The calendar is generally quiet in Asia-Pacific trading Friday but the Nikkei Japan PMI due at 0030 GMT could get some attention. The prior reading was 53.1.

Loonie Boosted by Strong Canadian Retail Sales; Oil Makes Some Recovery

Major currencies were mostly range-bound in a relatively quiet session due to a light news flow and few data releases.

The UK published the CBI industrial orders expectations data for June, which rose to +16 versus an expectation for a fall to +7 from a reading of +9. This was the highest number in 30 years, reflecting strength across most sectors of the economy. A weaker pound since the Brexit vote has helped. Meanwhile, UK Prime Minister Theresa May went to Brussels today for the EU Summit, where she will talk about the rights of EU citizens after the UK leaves the EU. However, any detailed Brexit-related discussion with EU leaders is discouraged during the Summit.

Sterling was barely impacted by today's data and was trading slightly below $1.2700, consolidating gains made after rising on hawkish comments by Bank of England policymaker Andrew Haldane on Thursday.

From the US, weekly unemployment claims figures and April's housing price index (HPI) data were out. Initial jobless claims rose by 3000, to 241,000 for the week ending June 17, versus a rise of 2,000 to 240,000 that was expected. The prior week's claims were revised higher to 238,000. HPI rose 0.7% versus a 0.5% rise expected. The dollar was trading above the 111-yen level in the later half of the European session.

Canada reported April retail sales data which boosted the loonie, helping offset some of the weakness from the drop in crude oil prices recently. Retail sales beat on both the headline and core numbers, which would be good news for the Bank of Canada. Headline sales in April rose by 0.8% month-on-month versus 0.3% expected. However, the prior month was revised down to show a 0.5% gain from a prior 0.7%. The core figure was strong and was up +1.5% month-on-month, more than twice that of the 0.7% forecast. Focus shifts to Friday's CPI data which will be more important for the BoC's outlook. USD/CAD fell after the data from C$1.3300 to $1.32166.

The kiwi extended gains following the RBNZ's positive outlook on the economy at its policy meeting today. NZDUSD rose to as high as $0.7272 during the European session.

In commodities, spot gold bounced higher to $1254 an ounce, while oil prices made some recovery today, halting a 3-day decline that took WTI crude to $42.05 a barrel on Wednesday as investors were concerned about a supply glut.

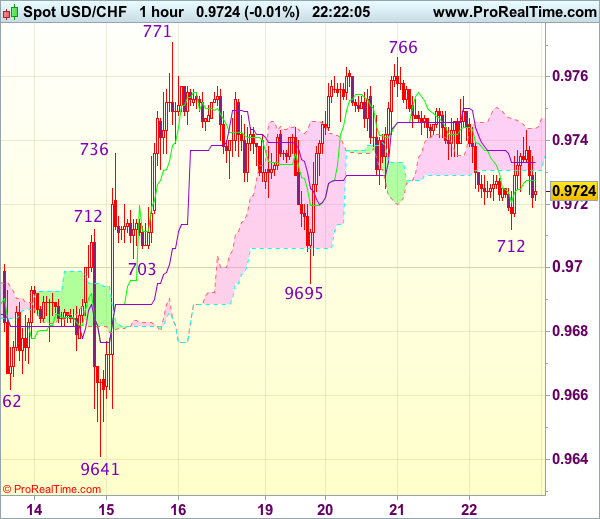

Trade Idea Wrap-up: USD/CHF – Hold long entered at 0.9705

USD/CHF - 0.9721

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9728

Kijun-Sen level : 0.9733

Ichimoku cloud top : 0.9744

Ichimoku cloud bottom : 0.9731

Original strategy :

Bought at 0.9705, Target: 0.9805, Stop: 0.9690

Position : - Long at 0.9705

Target : - 0.9805

Stop : - 0.9690

New strategy :

Hold long entered at 0.9705, Target: 0.9805, Stop: 0.9690

Position : - Long at 0.9705

Target : - 0.9805

Stop : - 0.9690

As the greenback has slipped again after meeting resistance at 0.9766, suggesting further consolidation below said last week’s high at 0.9771 would be seen, however, as long as support at 0.9695 holds, bullishness remains for recent upmove to resume after initial sideways trading, break of said resistance at 0.9771 would confirm recent rise from 0.9613 low has resumed for test of resistance at 0.9808 but reckon previous resistance at 0.9825 would hold from here due to near term overbought condition.

In view of this, we are holding on to our long position entered at 0.9705. Below said support at 0.9695 would defer and risk weakness towards said support at 0.9641 but only break there would abort and revive bearishness, this would also suggest the rebound from 0.9613 has ended instead, bring retest of this level later.

Yen Ticks Higher Ahead of Japanese Mfg. PMI

It continues to be an uneventful week for USD/JPY. In Thursday's North American session, the pair is down 0.9% and is trading at 111.30. On the release front, US unemployment claims rose to 241 thousand, matching the forecast. Later in the day, Japan releases Flash Manufacturing PMI, which is expected to improve to 53.4 points. On Friday, the US publishes New Home Sales.

Recent statements from the Bank of Japan indicate that when it comes to monetary policy, markets can expect more of the same. BoJ Governor Haruhiko Kuroda has insisted that the bank's ultra-loose policy would continue until inflation has reached the 2% target. Although the bank shows no signs of exiting its quantitative easing scheme, the BoJ has reduced its purchase of bonds. If this continues, bond purchases could slow to JPY 60 billion/year, down from the current 80 billion/year. In the April rate statement, the BoJ was more upbeat in its economic appraisal. This was an acknowledgement of a stronger Japanese economy, which grew at annualized rate of 1.0% in the first quarter, as exports and consumer spending strengthened. On Wednesday, the BoJ released the minutes of the April meeting. Policymakers noted that under the bank's asset-purchase program, the amount of government debt purchases would fluctuate, but that this did not pose a problem. The minutes also noted that members were optimistic about exports and industrial production.

The Federal Reserve has surprised the markets with its hawkish stance, as underscored by its rate statement. The statement mentioned that the Fed plans to reduce its balance sheet later in 2017, although it did not provide further specifics. The balance sheet has ballooned to $4.5 trillion, which accumulated after the 2008 financial crisis, when the Fed went on a bond-buying spree to stimulate the economy. The reduction will be gradual, but still marks an important change in direction for the central bank. On Wednesday, FOMC member Patrick Harker said that he was in favor of the reduction commencing in September. The Fed has hinted at one more rate hike in the second half of 2017, and the markets have circled December as the most likely date for a rate move. The CME Group has pegged the odds of a September hike at just 13%, compared to 18% a week ago. However, the odds for a December increase are at 49%, and this could increase if Fed policymakers continue to wax positive about the economy.

USD Desperately Waiting for ‘Real News’

- Brent oil price rose slightly and rebounded north of $45 after multiple daily losses since the end of May. Despite this small rise, European stocks are heading for a third daily decline. US stocks opened mixed, while gold and silver advance. Treasury yields are little changed.

- Britain's manufacturers are enjoying their healthiest pipeline of orders in nearly thirty years, the CBI survey for June showed. Export orders, supported by the weak pound, and overall demand are at their highest level since 1995 and 1988. This means a UK growth recovery in Q2 after the slowdown in Q1 is becomes more likely.

- Norway's central bank kept the policy rate unchanged but removed the easing bias in its meeting statement. It eliminated the prospect of a future cut and pencilled in a first increase in the beginning of 2019. As a result, the krone jumped 0.6% compared to the euro and settled a little lower at EUR/NOK 9.48 later in the day.

- The US weekly jobless claims figure of 241k was only slightly above the consensus of 240k. This followed a slightly upwardly revised 238k in the previous week, which was initially reported at 237k.

- EMU consumer confidence in June came in higher than consensus at -1.3. After close today in the US, the Fed will release the results of part one of its annual bank stress test.

Rates

German 2-yr yield near key levels

The Bund and US Note future traded uneventful today. Recovering commodity/oil markets, small losses on equity markets and close to consensus US weekly jobless claims didn't impact trading. The underperformance at the front end of the German yield curve continued during European dealings. Comments by ECB chief economist Praet partly explain the move. He said that prices will rise sooner or later and that this will bring about a change in monetary policy. "There is a light at the end of the tunnel". Moreover, his comments fit in the globally changing monetary policy stance. It's becoming clearer that the peak in dovish central bank talk is behind us. The Fed is the most obvious example, but other central banks are also gradually turning the corner. The ECB's change to its forward guidance, last week's dissent in the Bank of England, the co-ordinated comments by the chair and vice-chair of the Bank of Canada, upbeat comments on economic growth by the RBA, the slightly more optimistic view on inflation by the RBNZ overnight and the Norges Bank dropping its easing bias this morning… The correction at the front end of the German curve, the most extremely positioned market, suggests that markets started picking up the signals. The German 2-yr yield moved above -0.63% resistance, painting an inverse head and shoulders formation on the charts. A break above -0.6% would have important technical implications. The 2-yr yield is at its highest level since November 2016. During US dealings, bonds found new vigour, partly undoing European moves.

At the time of writing, changes on the German yield curve range between +0.8 bps (2-yr) and -1.9 bps (30-yr). The US yield curve shifts -0.8 bps (30-yr) to -2.2 bps (5-yr) lower. On intra-EMU bond markets, 10-yr yield spread changes versus Germany narrowed up to 3 bps (Spain/Ireland) with Greece and Portugal slightly underperforming.

Currencies

USD desperately waiting for 'real news'

There is still no big story to tell on the dollar. The decline of the oil price and the potentially negative impact on interest rates weighed slightly on the dollar this morning. However, the decline of oil halted, at least temporary, and so did the dollar. The data were no able to case any intraday dynamics. EUR/USD trades in the 1.1155/60 area. USD/JPY hovers around 111.25.

Overnight, Asian markets opened with a positive bias as the tech sector rebound continued. The positive momentum dwindled as the session proceeded though. Brent oil held below the $45/barrel level. The decline in oil prices and ongoing low core yields kept USD/JPY in the defensive. USD/JPY traded in the low 111 area. The dollar also traded marginally softer against the euro (EUR/USD 1.1170 area).

European equities failed to join the tech rally from the US and Asia and opened with modest losses. However, there was again little fallout from this poor start of equities on bonds or on the dollar. The correction also eased quite soon. USD/JPY dropped again to the 111 area, but the 110.65 correction low stayed well out of reach. EUR/USD still didn't show a clear trend and held stable in the 1.1175 area. Changes in interest rate differentials were negligible.

US jobless claims printed bang in line with expectations (241 000), offering no guidance for USD trading. USD/JPY trades currently in the 111.15 area. EUR/USD is changing hands in the 1.1160/65 area.

The Norges bank kept its policy rate unchanged at 0.5%, but left its easing bias. The Norwegian Crown strengthened from EUR/NOK 9.52 to EUR/NOK 9.46 (currently 9.48) even as the oil price struggles to prevent further losses.

EUR/GBP holds near the 0.88 pivot

After yesterday's Haldane inspired swings, sterling shifted in wait-and see modus. The political crisis isn't solved, but there was no additional negative news. A similar story can be told on Brexit. EUR/GBP settled in a tight range close to, mostly slightly above the 0.88 barrier. The CBI trends orders were again stronger than expected, but with no noticeable impact on sterling trading. EUR/GBP trades currently in the 0.8810/15 area. Cable holds an extremely tight range in the 1.2675 area.

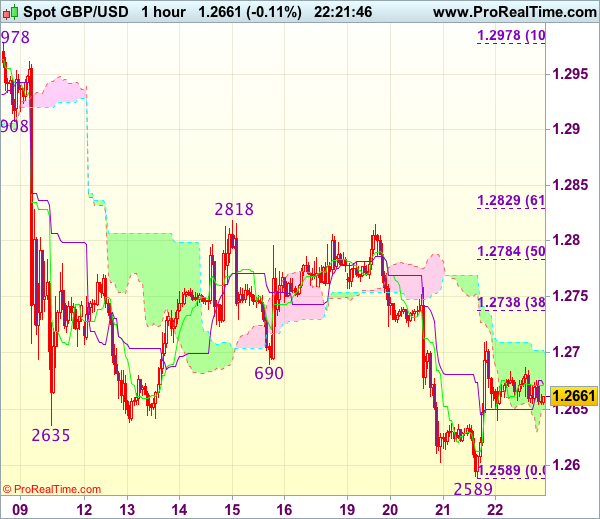

Trade Idea Wrap-up: GBP/USD – Hold short entered at 1.2695

GBP/USD - 1.2672

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2671

Kijun-Sen level : 1.2672

Ichimoku cloud top : 1.2702

Ichimoku cloud bottom : 1.2650

Original strategy :

Sold at 1.2695, Target: 1.2595, Stop: 1.2710

Position : - Short at 1.2695

Target : - 1.2595

Stop : - 1.2710

New strategy :

Hold short entered at 1.2695, Target: 1.2595, Stop: 1.2710

Position : - Short at 1.2695

Target : - 1.2595

Stop : - 1.2710

Although cable staged a strong rebound after yesterday’s brief fall to 1.2589, as long as 1.2710 holds, mild downside bias remains for another decline, below 1.2635-40 would bring another fall towards said support but break there is needed to retain bearishness and signal recent decline has resumed for weakness towards 1.2550, however, oversold condition should limit downside to 1.2520-25.

In view of this, we are holding on to our short position entered at 1.2695. Only above 1.2720-25 would abort and suggest low has been formed instead, bring a stronger rebound to 1.2755-60 and possibly 1.2780 but price should falter below indicated strong resistance at 1.2818.

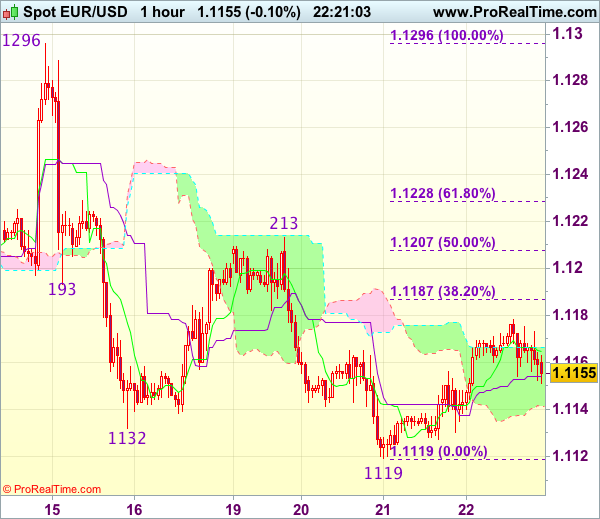

Trade Idea Wrap-up: EUR/USD – Sell at 1.1200

EUR/USD - 1.1162

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.1165

Kijun-Sen level : 1.1154

Ichimoku cloud top : 1.1166

Ichimoku cloud bottom : 1.1141

Original strategy :

Sell at 1.1190, Target: 1.1090, Stop: 1.1225

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1200, Target: 1.1100, Stop: 1.1235

Position : -

Target : -

Stop : -

The single currency has rebounded again after holding above this week’s low at 1.1119, suggesting further consolidation would be seen and near term upside risk remains for retracement to 1.1185-90 (38.2% Fibonacci retracement of 1.1296-1.1119), however, upside should be limited and price should falter below 1.1207-13 (50% Fibonacci retracement and previous resistance), bring another decline later, below 1.1135-40 would suggest the rebound from 1.1119 has ended, brig retest of this level, below there would confirm recent decline has resumed for further weakness to previous support at 1.1109, then towards 1.1075-80 but loss of near term downward momentum should prevent sharp fall below 1.1050.

In view of this, we are looking to sell euro on recovery as 1.1195-00 should limit upside. Only above 1.1213 resistance would defer and risk a stronger rebound to 1.1230-35 but upside should be limited to 1.1260-70, bring another decline later.

Trade Idea Wrap-up: USD/JPY – Buy at 110.65

USD/JPY - 111.25

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 111.17

Kijun-Sen level : 111.35

Ichimoku cloud top : 111.37

Ichimoku cloud bottom : 111.35

Original strategy :

Buy at 110.65, Target: 111.65, Stop: 110.30

Position : -

Target : -

Stop : -

New strategy :

Buy at 110.65, Target: 111.65, Stop: 110.30

Position : -

Target : -

Stop : -

As the greenback slipped again after faltering below recent high at 111.79, retaining our view that further consolidation below this level would be seen and pullback to 110.80 is likely, however, reckon previous support at 110.65 would limit downside and bring another rise later, above 111.45-50 would bring retest of 111.79 but break there is needed to confirm the rise from 108.82 low has resumed and extend headway to 111.90-95 (50% projection of 108.82-111.42-110.65), however, upside should be limited to resistance at 112.13 and 112.25 (61.8% Fibonacci retracement of 114.37-108.82 and 61.8% projection) should hold.

In view of this, would not chase this rise here and we are looking to buy dollar on pullback as 110.65 support should limit downside. Below 110.30-35 (50% Fibonacci retracement of 108.82-111.79 and previous resistance turned support) would abort and signal a temporary top has been formed instead, risk weakness towards 109.95-00 (61.8% Fibonacci retracement).