Sample Category Title

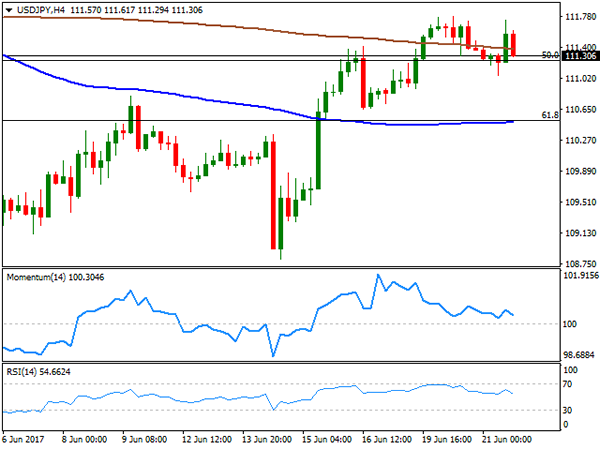

Technical Outlook: USDJPY – Mixed Outlook Between 110.65 And 111.80 Pivots

The pair remains at the back foot on Thursday and probed below 111.00 handle (55SMA) on extension of pullback from 111.80 zone after repeated rejection at daily cloud base.

Thin cloud which twists next week may attract for fresh attack. Plethora of daily MA's continues to underpin and supports scenario.

Strong supports at 110.85 (200SMA) and 110.65 (10/20SMA bull-cross/Fibo 38.2% of 108.80/111.78) are expected to hold for fresh upside attempts.

On the other side, slow stochastic is reversing from overbought territory on daily chart and warns of deeper pullback.

Firm break below 110.65 will neutralize expectations of fresh bullish action and expose supports at 110.29/109.94 (Fibo 50% and 61.8% retracement of 108.80/111.78 rally respectively).

Res: 111.42, 111.78, 112.24, 112.05

Sup: 111.00, 110.85, 110.65, 110.29

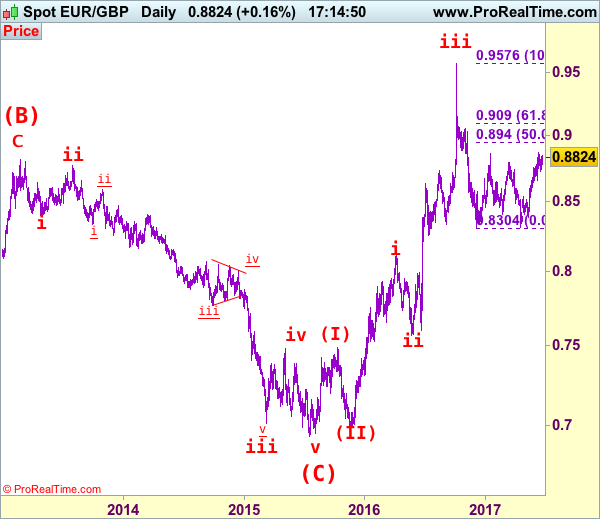

EUR/GBP Elliott Wave Analysis

EUR/GBP – 0.8823

EUR/GBP – The major (A)(B)(C)-(X)-(A)(B)(C) correction from 0.9805 is unfolding and 2nd (A) has possibly ended at 0.6936.

As the single currency has maintained a firm undertone after recent upmove, suggesting the erratic rise from 0.8304 low is still in progress and above resistance at 0.8866 would extend gain to 0.8900, then towards 0.8940-50 (50% Fibonacci retracement of 0.9576-0.8304), however, loss of upward momentum should prevent sharp move beyond 0.9000 psychological level and price should falter below 0.9090-00 (61.8% Fibonacci retracement) and bring retreat later.

Our latest preferred count is that the wave V of a 5-wave series from 0.5682 ended at 0.9805 earlier and major from there has possibly ended at 0.8067 as A-B-C-X-A-B-C. We are keeping our view that the entire correction from 0.9805 has possibly ended at 0.7756 and as labeled as the attached daily chart and impulsive move from 0.9084 has ended at 0.7756 as a 5-waver which marked either the (C) wave or the A leg of (C), a daily close above resistance at 0.8831 would suggest (C) leg has ended and headway towards 0.9084.

On the downside, whilst initial pullback to 0.8735-40 cannot be rule out, reckon 0.8680-90 would limit downside and bring another rise later. A daily close below support at 0.8652 would suggest top is possibly formed and risk weakness towards 0.8600-05 but reckon downside would be limited to 0.8550 and previous support at 0.8524 should hold from here, bring rebound later.

Recommendation: Buy at 0.8680 for 0.8880 with stop below 0.8580

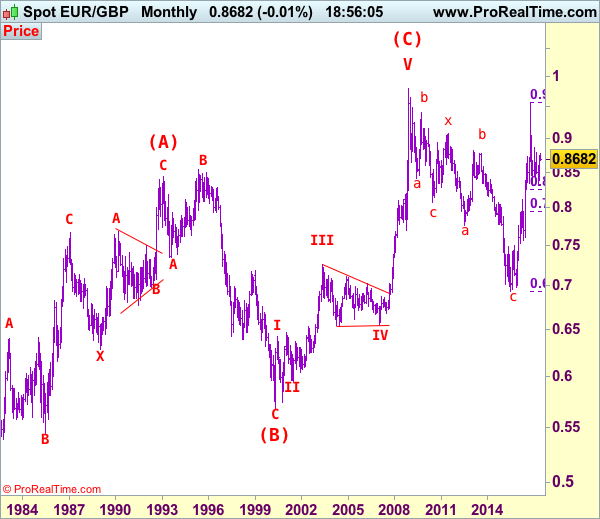

Euro's long term uptrend started in Feb 1981 at 0.5039 and is unfolding as a (A)-(B)-(C) move with (A): 0.8433 (Feb 1993), (B): 0.5682 (May 2000) and impulsive wave (C) should have ended at 0.9805 with wave III ended at 0.7254 (May 2003), triangle wave IV at 0.6536 (23 Jan 2007) and wave V as well as wave (C) has ended at 0.9805.

We are keeping an alternate count that only wave III ended at 0.9805 and the correction from there is the wave IV and may extend weakness to 0.7700, however, it is necessary to see a daily close above resistance at 0.9143 would change this to be the preferred count.

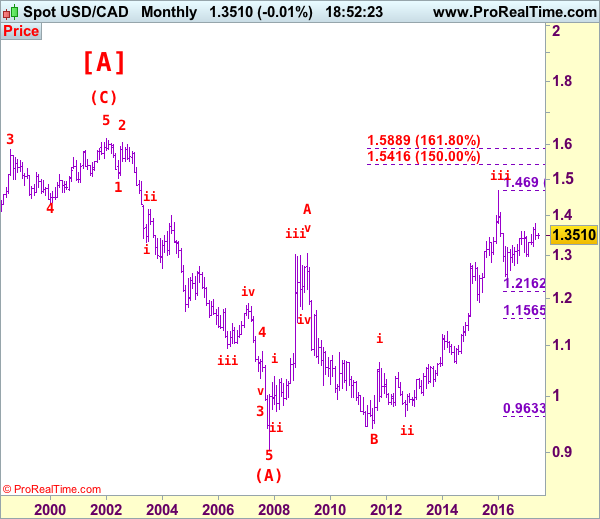

USD/CAD Elliott Wave Analysis

USD/CAD – 1.3317

USD/CAD – Wave v ended at 0.9407 and a-b-c correction may extend gain to 1.4700

Despite last week’s anticipated decline to 1.3165, the subsequent rebound suggests 1-2 weeks of consolidation above this level would be seen and recovery to 1.3387 (previous support) cannot be ruled out, however, reckon upside would be limited to 1.3470-75 and price should falter below resistance at 1.3547, bring another decline later. Below 1.3260-65 would bring test of 1.3190-95 but break there is needed to signal the rebound from 1.3165 has ended, bring retest of this level. A drop below there would add credence to our view that top has been formed at 1.3794, bring further weakness to 1.3150 and then 1.3100, however, oversold condition should limit downside and reckon previous support at 1.3056 would hold, price should stay above psychological support at 1.3000.

We are keeping our view that the wave b from 1.0657 (a leg top) has possibly ended at 0.9633 with (a): 0.9800, wave (b): 1.0447 and wave c at 0.9633, the subsequent rise from there is now treated as wave c exceeded indicated upside target at 1.3770-80 and 1.4000 and wave (3) has possibly ended at 1.4690 and wave (4) correction has commenced for retracement back to 1.2832 support, then 1.2410-20.

On the daily chart, our latest preferred count remains that the A of (B) rally from 0.9059 low (7 Nov 2007) unfolded into an impulsive wave with i: 0.9059-1.0380, ii ended at 0.9819, iii at 1.3019 followed by triangle wave iv at 1.2026 , then wave v formed a top at 1.3066 and also ended the wave A. The wave B is unfolding as an double three a-b-c-x-a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c at 1.0784, followed by wave x at 1.1725, another set of a-b-c unfolded with 2nd a at 0.9931, 2nd b at 1.0674. the 2nd c has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3900 had been met and gain to 1.4700 would follow.

On the upside, whilst initial recovery to 1.3350 cannot be ruled out, reckon upside would be limited to previous support at 1.3387 (now resistance) and bring another decline later. A daily close above 1.3387 would suggest low is possibly formed, bring a stronger rebound to 1.3425-30, break there would add credence to this view, then further gain to 1.3490-00 would follow but resistance at 1.3547 should remain intact.

Recommendation: Stand aside for this week.

Longer term - The selloff from 1.6194 (21 Jan 2002) to 0.9059 (07 Nov 2007) is viewed as (A) wave which is a 5-waver as labeled on the monthly chart as below, the subsequently rally is labeled as (B) with impulsive A leg of (B) ended at 1.3066, wave B of (B) is unfolding which has either ended at 0.9407 or would extend one more fall but downside should be limited to 0.9200 and 0.9000 should hold.

Swiss Trade Data Jumps, Oil Sell-Off Continues

Switzerland's trade activity picked up in May

After the usual March-April contraction, Switzerland's trade surplus bounced back in May amid a sharp recovery in exports. The trade surplus rose to CHF 3.4 billion in May from CHF 1.96 a month earlier. Exports - in real terms - increased 2.9% m/m while imports eased to 2% m/m.

Exports to China passed the CHF 1bn threshold to print at 1.16bn while imports reached 1.02bn, leaving a trade surplus of CHF 139 million. Trade activity with the European Union also accelerated substantially with exports and imports rising 1.47bn and 2.12bn respectively, adding evidence that the European economy is on the right track.

It was quite a pleasant surprise for the Swiss watch industry as exports rose 9% last month compared to a contraction of 5.7% in the previous month. The sharp recovery was mostly driven by a surge in exports to Hong Kong, China and Italy, while Gulf countries reduced sharply their imports amid falling oil revenue and geopolitical uncertainties.

All in all, the report showed that the Swiss economy is still right on track but continues to suffer from the strong CHF. The recovery pace is solid especially given the slower than expected recovery in Europe and the United States. Swiss companies already optimised their functioning and no more gains can be expected on this side. Investments have been reduced to the minimum, costs have been cut. Economic improvement of Switzerland's main trading partner is more necessary to see a substantial growth acceleration.

Load up on EM risk

Time to make hay while the sun is shining. We are highly constructive on EM FX risk given the current environment. The summer doldrums have hit but conditions are ideal for carry trading. EM economic outlook remains positive, spearheaded by improving trade data (US and EU economic momentum is more balanced). While in the G10 a soft inflation backdrop will keep monetary policy supportive, driving yields seekers in to EM, finally political noise such as President Trump's pro-growth agenda and rising protections threat has subsided.

Idiosyncratic domestic risks in Romania, Venezuela and Brazil to name a few have shown no hint of sparking broader contagion. We are focused on the growth differentials rather than just interest rates differential for FX carry selection. Depreciation of oil prices and negative price outlook has us avoiding crude-linked currencies like RUB, COP and MXN. In addition we have shifted away from USD as the primary funding currency due to the expectation of higher rates and political uncertainty driving rogue volatility, preferring JPY, CHF and even CAD due to bearish outlook for oil.

Looking forward there is scant scheduled events in July and August that could likely derail the EM carry trade. Political developments in UK-EU Brexit discussions are likely to slow while there are not enough US data points to decisively determine a recovery in 2H and firm repricing of the Fed interest rate path. Time to load up on EM carry risk.

Probability of November BoE hike increases

We continue to suspect that markets are underpricing the probability of a BoE policy adjustment. We suspect that as with the Fed, the threshold of removal of emergency measures is significantly lower than standard interest rate hikes. While interest rates in the UK never went negative, it's difficult for MPC members to justify ultra-easy policy given the economic momentum. BoE Governor Carney's Mansion House speech dented our expectations of a 2017 rate hike.

However, BoE chief economist Haldanes indicated that marginal data would suggest hikes in 2H (most likely November). This is not the first time Haldane's view diverged from the MPC, but it will put the markets on alert for shifts in doves Broadbent and Vlieghe and improving data. Markets are now pricing in 12bp of hikes by end of 2017. To materialise our constructive GBP view, we see long GBPCHF as the ideal position.

Oil prices continue to slide; back below $40 within a few weeks?

Since May 23, oil has been in short-term decline. Crude oil is now testing its 1-year low mark around $42. We believe that the decline is set to continue. Since the Qatar diplomatic issue, there are growing concerns that other OPEC members will not respect the production cut and therefore oversupply.

Will the decline continue? When looking specifically to Saudi Arabia, the largest oil exporter in the world, we may believe this bearish trend should continue. The Arabic country really needs to have higher oil prices. Fundamentally speaking, its FX reserves have declined 27% from its 2014 peak. Just in 2017, it has diminished by $36 billion.

Current oil prices seem way too low for Saudi Arabia, which is in return obliged to liquidate its FX reserves to assume its running costs. On top of that, Saudi Arabia is willing to let investors buy 5% of its oil reserves. Yet, at the current oil price, this seems like a deal for bullish buyers. In our view, that means Saudi Arabia is concerned about future oil prices. In addition, the US shale gas industry is booming back and is putting deeper downside pressures on oil. We believe that the oil price should go back below $40 within the next few weeks.

Crude Oil Inventories Drop For Second Straight Week

'US crude and gasoline stockpiles are significantly higher compared with their five-year averages, which will weigh on prices.' — Abhishek Kumar, Energy's Global Gas Analytics

US oil inventories fell for the second consecutive time last week, official data showed on Wednesday. As reported by the Energy Information Administration, the number of barrels of crude oil dropped 2.5M in the week ended June 16, compared to the preceding week's decline of 1.7M barrels, while analysts predicted a much lower drop of 1.2M barrels. US crude oil production climbed to 9.35M barrels per day, 20K higher than in the prior week, the EIA reported. Gasoline stockpiles plunged 578K, whereas analysts anticipated a gain of 444K barrels. In the meantime, distillate stocks advanced 1.1M barrels, surpassing expectations for a 465K-barrel increase. US refinery runs fell 104K bpd as the utilisation rate dropped 0.4% to 94%. The number of barrels of crude oil held in storage at the Cushing, Oklahoma, plunged 1.08M barrels during the reported week. Oil prices rose shortly after the report was published but failed to sustain those gains. Thus, soon after the release, West Texas Intermediate futures fell to $43.41 per barrel, whereas Brent futures declined to $45.79 per barrel.

Reserve Bank Of New Zealand Remains On Hold

'It appears that the bank isn't too perturbed by the rally in the currency given that export prices have also risen.' — Zoe Wallis, Kiwibank

The Reserve Bank of New Zealand held its policy and interest rates unchanged at its meeting on Thursday, stating it would unlikely change its stance in the near future. Policymakers voted to leave the benchmark rate at a record low of 1.75% and keep the Bank's monetary policy accommodative for 'a considerable period' amid high uncertainties. According to the RBNZ, interest rates are set to remain unchanged until late 2019 despite the fact that inflation returned to its 1-3% target range. Even though inflation hit 2.2% in the three-month period to March, policymakers said that the following inflation pickup was triggered by temporary factors. However, the Bank suggested that pay and non-tradables inflation would likely improve in the upcoming months. The RBNZ Governor Graeme Wheeler said that the Kiwi's recent gains were driven mainly by higher export prices. Nevertheless, the Governor noted that the weaker New Zealand Dollar would help to rebalance the growth outlook towards the tradable sector. Despite the weak March quarter performance, the Bank expressed optimism over the economic outlook for New Zealand.

Bear Territory For Oil?

Oil continued to trade lower on Thursday as traders look ready to test new lows for crude prices with worries persisting over a global glut.

Since peaking in late February, crude has dropped approximately 20%, with only brief rallies, completely erasing the gains it made at the end of the year following the initial OPEC-led production cut. OPEC and other major producers agreed to cut output by 1.8 million barrels per day from January for six months which was recently extended for an additional nine months. Whilst this was a major shift in policy for OPEC the hope it gave to markets was short lived. With increased production from the US, Nigeria, Libya and other producers the extra supply outstripped demand and forced prices lower. US Crude inventories fell 2.5 million barrels in the week to June 16, surpassing analyst expectations for a decrease of 2.1 million barrels. Even comments from Iran’s oil minister that OPEC members are considering further output cuts has made little impact to prices.

Brent crude was trading at $44.95 a barrel at 09:05 GMT, after spending much of the Asian trading day in positive territory. Brent had fallen 2.6% in the previous session to its lowest level since November of last year.

WTI was trading at $42.50 a barrel at 9:10 after spending much of the day trading higher this after touching its lowest intraday level since August 2016.

GBPUSD is trading around $1.2670 after making some gains on Wednesday after Bank of England’s chief economist, Andy Haldane, suggested that “he was likely to vote for an interest rate hike this year”. Haldane was largely supportive of keeping rates low, contrasting sharply with the tone set by the bank’s Governor Mark Carney just the day before.

NZD gained nearly 0.5% against USD following the expected RBNZ decision to keep interest rates unchanged at a record low 1.75%. RBNZ Governor Wheeler stated “Global economic growth has increased and become more broad-based. However, major challenges remain with on-going surplus capacity and extensive political uncertainty”. NZDUSD was trading at 0.7260 at 9:30 BST.

Markets will be looking at US Initial Jobless claims, that are released at 13:30 BST today and a scheduled speech from FOMC member Powell at 15:00 BST for further evidence of the US economy strengthening.

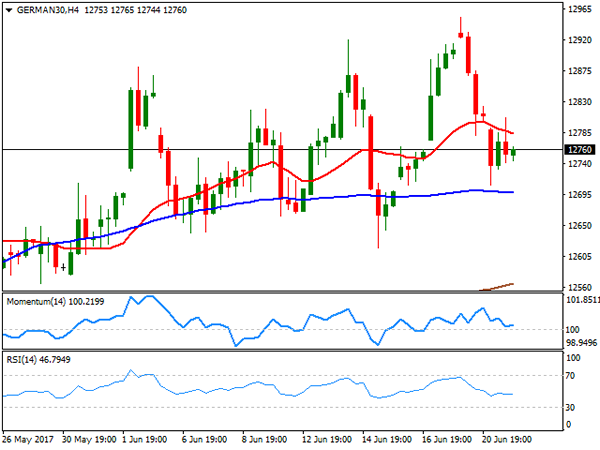

Elliott Wave Analysis: German DAX Trading In A Temporary Correction, More Weakness In View

German DAX is undergoing a three wave correction within black wave B. Upside for the final leg c of B can be found around the Fibonacci ratios of 38.2, 50.0 or 61.8 and as we can see on the chart around the previous levels of wave iv at 12822. Once wave B completes itself, a new reversal lower can come in play.

German DAX, 1H

Technical Outlook: GBPUSD – Recovery Remains Capped By Falling Tenkan-Sen

Cable stayed within 30-pips range in Asia and below fresh recovery high at 1.2709, following strong rally on Wednesday, sparked by hawkish comments from BoE's Haldane.

Failure to clearly break above 1.2700 pivot (50% of 1.2814/1.2588 downleg, reinforced by daily Tenkan-sen in steep fall and descending 10SMA), keeps risk at the downside, as daily studies are in bearish setup.

The pair may extend consolidation after repeated failure to close below cracked 100SMA, but limited upside is seen for now, as multiple bear-crosses of daily MA's maintain bearish pressure.

Lower pivots lay at 1.2631 (100SMA) and 1.2600 (correction low), loss of which would open way towards targets at 1.2578/50 (daily cloud base/200SMA).

Conversely, lift above 1.2700 pivot would expose key near-term barriers at 1.2800/20 zone (daily cloud top/recent multiple upside rejection).

Sterling will be closely watching the outcome of Queen's speech vote in the parliament for stronger signals. The vote will be basically vote of confidence in PM Theresa May and her government and approval of Queen's speech is expected to boost pound. Conversely, Sterling may come under strong pressure if Queen's speech will not be approved.

Res: 1.2686, 1.2700, 1.2728, 1.2757

Sup: 1.2656, 1.2631, 1.2600, 1.2578

Foreign Exchange Market Commentary: EUR/USD, USD/JPY, GBP/USD, GOLD, WTI CRUDE, DJIA, FTSE100, DAX

EUR/USD

The EUR/USD pair recovered some ground after this Thursday, but the pair remained confined to a tight intraday range and near the lower end of its last 5-week extend. The European macroeconomic calendar remained empty, while in the US, Fed's officers were once again in the wires talking about unwinding the balance sheet, despite latest weak inflation, although with less impressive headlines. Also, the country released its May Existing Home Sales figures, surprisingly better-than-expected, as home prices rose by 5.8% to a new record. Sales climbed 1.1% to a seasonally adjusted annual rate of 5.62 million in the month, from a downwardly revised 5.56 million in April. This Thursday, the US will release its usual weekly unemployment data, alongside with April housing price index and the Kansas manufacturing index.

From a technical point of view, the pair has found some support around 1.1125 the 23.6% retracement of its latest bullish between 1.0606, April 10th low, and the high set this June at 1.1295. The pair has also a relevant low at 1.1109 posted on May 30th, with the lowest for the last five weeks being 1.1075, reached on May 18th. A break below this last will likely open doors for a steeper downward move, moreover as the price keeps moving away from the critical 1.1300 mark. In the meantime, the short term picture remains neutral-to-bearish, with the price holding below a strongly bearish 20 SMA that already broke below the 100 SMA, whilst technical indicators hold directionless near oversold readings.

Support levels: 1.1110 1.1075 1.1030

Resistance levels: 1.1220 1.1260 1.1300

USD/JPY

The USD/JPY pair closed the day unchanged around 111.30, still stubbornly attached to yields' behavior and despite news coming from both major economies. The Bank of Japan released the Minutes of its latest meeting at the beginning of the day, cooling down speculation of tapering surged during the past few weeks. Policy makers officers acknowledged that the amount of government debt purchases will fluctuate under the current quantitative easing programme, but don't expect that to pose a problem, while also recognized that there's a long way ahead before inflation reaches the desirable target of 2%. In the US, existing home sales surprised to the upside, up in May by 1.1%, following a notable decline in April of 2.5% according to the official report. Technically, the 4 hours chart shows that the price struggles around a modestly bearish 200 SMA and the 50% retracement of its latest bullish run, while technical indicators eased within positive territory, lacking, however, directional strength, all of which limits chances of further gains ahead. A stronger decline is likely only on a break below 110.50, a strong Fibonacci support.

Support levels: 111.25 110.80 110.50

Resistance levels: 111.60 112.00 112.45

GBP/USD

It was a wild ride for the Pound this Wednesday, with the GBP/USD pair sinking to a fresh 2-month low of 1.2588 before bouncing to 1.2709, and then settled midway around 1.2640. The pair fell early London on news indicating that the Democratic Unionist Party (DUP) threatened to walk away from a deal with May's conservatives. The following bounce was triggered by hawkish comments coming from BOE's Haldane, who said he is ready to vote for a rate hike amid rising inflation. Haldane didn't vote for a hike in the latest monetary policy meeting, which pretty much anticipates already 4 hike votes out of 8 MPC members for the next Central Bank meeting. Also, Queen's speech at the Parliament opening, focusing on getting the best deal possible for the UK on the Brexit, something looking harder day after day, as PM May seems unable to form a government. Mid American afternoon, hundreds of protesters marched to Downing Street, asking for May's resignation, while another of her top advisors, John Godfrey, quit. The 4 hours chart shows that the intraday rally found sellers around a bearish 20 SMA, currently around 1.2710, while technical indicators have resumed their declines well-below their mid-lines, after correcting oversold readings earlier today. The risk remains towards the downside, with an immediate support now at 1.2635, the post-election low.

Support levels: 1.2635 1.2590 1.2560

Resistance levels: 1.2670 1.2710 1.2750

GOLD

Gold prices consolidate losses around the 1-month low reached this week, with spot adding a few cents daily basis and settling at $1,246.10 a troy ounce. The commodity was unable to attract buyers, despite falling equities, while the downside was limited by diminishing Fed's surprise headlines on rate hikes and shrinking the balance sheet. The daily chart for the commodity shows that the price peaked right below Tuesday's high, but still stands below its 20 and 100 DMAs, while technical indicators turned horizontal near well below their mid-lines, limiting chances of a steeper recovery. In the 4 hours chart, the recovery stalled right below a bearish 20 SMA, this last acting as an immediate resistance at 1,248.20 while technical indicators recovered within negative territory, not enough to confirm an upcoming advance. At this point, the commodity would need to advance beyond 1,260.00 to regain its bullish stance and attempt a retest of the 1,300 region.

Support levels: 1,241.95 1,230.90 1,222.80

Resistance levels: 1,248.10 1,257.20 1,265.90

WTI CRUDE OIL

Crude oil prices extended their declines to fresh 2017 lows, despite the EIA weekly stockpiles´ report showed a larger-than-expected draw-down. West Texas Intermediate crude oil prices traded at as low as $42.04 a barrel and settled at 42.66, while Brent fell below $45.00 a barrel. The US Energy Information Administration reported that crude inventories declined by 2.45 million barrels in the week ended June 16th, exceeding expectations for a 2.1 million-barrel drop, with the news triggering a short-lived spike in prices. West Texas Intermediate crude futures quickly turned south as the headline was not enough to revert concerns over a worldwide glut. From a technical point of view, the daily chart shows that technical indicators extended their declines, with the RSI still heading south, despite being at 23, and the price further below its moving averages, in line with further declines. Shorter term, and according to the 4 hours chart, the risk remains also towards the downside, as an early advance was rejected by a bearish 20 SMA, whilst technical indicators are currently consolidating within oversold levels, due to limited volumes at the time being.

Support levels: 42.10 41.65 41.10

Resistance levels: 43.00 43.75 44.50

DJIA

Wall Street closed mixed, with only the Nasdaq Composite managing to advance, up 45 points to 6,233.95. The Dow Jones Industrial Average lost 57 points, and closed at 21,410.03, while the S&P ended pretty much unchanged, down 0.06%, to 2,435.61. The sour sentiment that dominated equities at the beginning of the week was exacerbated by a sharp decline in oil prices to fresh 2017 lows. Within the Dow, Caterpillar led decliners, down 3,52%, followed by El du Pont and Chevron, down 2.65% and 1.82% respectively. Nike was the best performer adding 1.83%. Falling for a second day in a row, the daily chart for the DJIA shows that the movement remains corrective, as moving averages maintain their sharp bullish slopes below the current level, whilst the RSI indicator is barely beginning to correct overbought conditions, now heading lower around 66. In the 4 hours chart, the index is poised to extend its decline, having extended below its 20 SMA and with technical indicators heading south within bearish territory.

Support levels: 21,389 21,351 21,303

Resistance levels: 21,449 21,495 21,542

FTSE100

The Footsie edged lower, undermined by a stronger Pound and falling oil prices. The London benchmark settled at 7,447.79, down 24 points or 0.33%, as the Sterling got an unexpected boost from BOE's Haldane, pledging to vote for a rate hike in the next BOE's meeting should inflation remain high. Plummeting oil prices weighed on the energy sector, although financials also edged lower across the region. The worst performer was Provident Financial, down by 17.59% after warning a shake-up of its lending division would dent profits much more than previously forecast. Among losers was also Royal Dutch Shell, down 1.34%, and Standard Chartered that lost 1.33%. Whitbread was the best performer with a 3.40% gain. The daily chart for the FTSE 100 shows that the index remains below a directionless 20 DMA but above its 100 DMA, while technical indicator present modest downward slopes right below their mid-lines, maintaining the risk towards the downside. In the 4 hours chart, the technical outlook is neutral-to-bearish as indicators keep hovering around their mid-lines, but the index develops below its 20 and 100 SMA, with the shortest gaining bearish traction.

Support levels: 7,403 7,376 7,327

Resistance levels: 7,499 7,541 7,584

DAX

The German DAX closed the day at 12,774.26, down 40 points amid falling oil prices dragging energy-related equities lower. Banks and retailers also edged lower across the region, and within the DAX, Deutsche Boerse was the worst performer, down 1.84%, while Commerzbank shed 0.81% and Deutsche Bank lost 0.35%. Only 5 members closed up, led once again by ThyssenKrupp that added 2.23%. The index closed down for a second consecutive day, now flat weekly basis, and with the daily chart showing that the index met some buying interest on a test of its 20 DMA, now around 12,719, the immediate support, while technical indicators turned lower, still holding above their mid-lines. In the shorter term, and according to the 4 hours chart, the benchmark presents a neutral-to-bearish stance, trading a few points below its 20 SMA but above the larger ones, whilst technical indicators head nowhere around their mid-lines.

Support levels: 12,719 12,653 12,605

Resistance levels: 12,807 12,851 12,892