Sample Category Title

Sterling Propelled as BoE Chief Economist Haldane Turned Hawkish

Sharp volatility in Sterling continues today as hawkish comments from BoE chief economist Andy Haldane propels it higher. Haldane said today that partial removal of monetary stimulus would be "prudent relatively soon". And he noted that "risks associated with tightening too early, on the one hand, and too late, on the other, has swung materially towards the latter in the past six to nine months." He pointed out that "the risks of tightening too early have shrunk as growth and, to lesser extent, inflation have shown greater resilience than expected. And if policy tightened too late, this could result in a much steeper path of rate rises later on."

Haldane's comments was taken seriously by the markets as firstly, he's the chief economist. Secondly, he's perceived by many as the most dovish MPC member. Thirdly, while Kristin Forbes will be released by Silvana Tenreyro, there are potentially still three MPC member, including Haldane, Ian McCafferty and Michael Saunders, that could vote for rate hike ahead. Haldane's comments were in sharp contrast to BoE Governor Mark Carney's, showing a clear split between the board.

Separately, a report by BoE's regional agents noted moderate growth in the country overall. Export volume was helped by depreciation of the Pound and showed continuing growth. More importantly, rising intentions on investments were seen. The report noted that upward pressure on companies' costs due to currency effect "may have passed their peak". Meanwhile, it warned that highest costs are feeding into consumer inflation that could weight on consumptions and some investments.

Technically, nonetheless, GBP/USD is staying below 1.3813 resistance, GBP/JPY below 142.75 resistance, EUR/GBP above 0.8639 support. The pound is staying near term bearish in these pairs.

ECB noted US, China and Brexit as new sources of risks

ECB noted in its monthly economic bulletin that "careful communications by the Federal Reserve System, coupled with a very gradual course of monetary policy tightening, and the decline in vulnerabilities in major emerging markets, appears to have eased the risk of a disorderly tightening of global financial conditions." But the central bank also warned of "new sources of risk". In particular, ECB pointed to the "potentially protectionist direction of the new US administration" that could have a "significant negative effect on the global economy". In addition, "China's vulnerabilities over the medium term are also still elevated". And potential contentious negotiations over Britain's departure from the European Union remain a source of concern".

BoJ Kuroda: economy on firmer footing

BoJ Governor Haruhiko Kuroda said today that the economy is on "firmer footing" but Japan is still "distant from our 2 percent inflation target". He reiterated that "it is appropriate to keep monetary conditions easy with our current market operations framework." Also Kuroda noted that it's he is not thinking about stimulus exit yet. And the pace of JGB purchase could rise again easily. Regarding the economy, he offered an optimistic of assessment of capital expenditure and corporate profits. and Output gap is moving back into positive territory.

The minutes of BoJ's April meeting showed that policy makers were comfortable with the fluctuation in JGB purchases. The minutes noted that "members reaffirmed their view that debt purchases will fluctuate within a range depending on market conditions and agreed this poses no problems to the BOJ's guidance for market operations." This came into question as BoJ recently slowed down the bong purchases. And with the current pace, the total annual increase could be projected as JPY 60T, instead of JPY 80T as the central noted in its communications. Nonetheless, it's been clear that BoJ changed its approach last year to the so called Yield Curve Control framework. That is, the central bank is targeting to keep long term yield at zero, instead of a figure of asset purchase.

On the data front

UK public sector net borrowing dropped to GBP 6.0b in May. Australia Westpac leading index rose 0.0% mom in May. Japan all industry index rose 2.1% mom in April. RBNZ rate decision will be a focus in the upcoming Asian session. The central bank is widely expected to keep OCR unchanged at 1.75%.

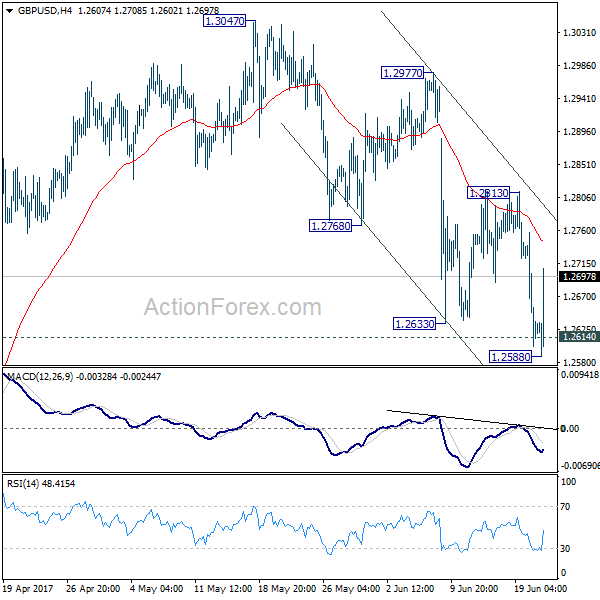

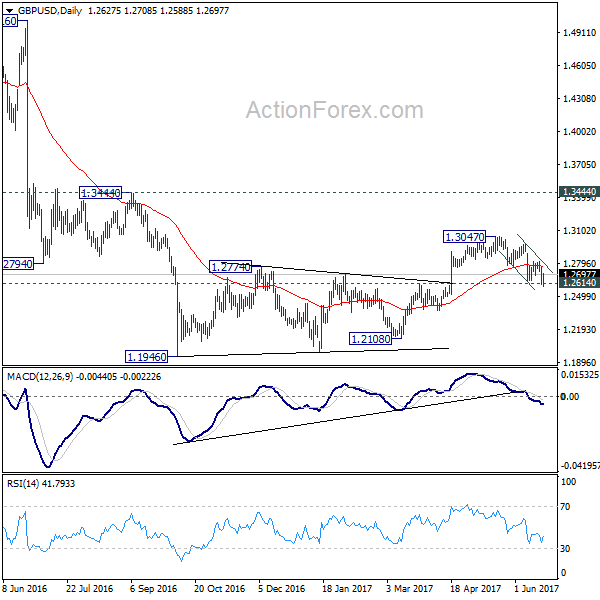

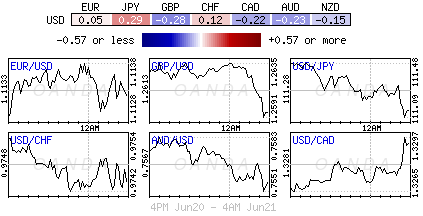

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2565; (P) 1.2661; (R1) 1.2721; More...

GBP/USD rebounds strongly after dipping to 1.2588 earlier today. As the pair is trying to draw support from 1.2614 key support level, intraday bias is turned neutral first. Deeper fall is still expected as long as 1.2813 resistance holds. As noted before, we're still favoring the bearish case that consolidation pattern from 1.1946 has completed at 1.3047 already. Sustained break of 1.2614 resistance turned support should confirm our bearish view and target a test on 1.1946 low next. However, break of 1.2813 resistance will dampen our view and turn bias back to the upside for 1.3047 and above.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. Price actions from 1.1946 medium term low are seen as a consolidation pattern, which could have completed after hitting 55 week EMA. Break of 1.1946 low will target 61.8% projection of 1.5016 to 1.1946 from 1.3047 at 1.1150 next. In case the consolidation from 1.1946 extends, outlook will stay remain bearish as long as 1.3444 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BOJ Minutes April Meeting | ||||

| 0:30 | AUD | Westpac Leading Index M/M May | 0.00% | -0.10% | ||

| 4:30 | JPY | All Industry Activity Index M/M Apr | 2.10% | 1.60% | -0.60% | -0.70% |

| 8:30 | GBP | Public Sector Net Borrowing (GBP) May | 6.0B | 7.3B | 9.6B | 8.7B |

| 14:00 | USD | Existing Home Sales May | 5.54M | 5.57M | ||

| 14:30 | USD | Crude Oil Inventories | -1.7M | |||

| 21:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% |

Mild Risk Aversion Seen In Early Trade

- Gold and yen gain in slightly risk averse start to trading on Wednesday;

- Oil stabilises but still looks vulnerable to further downside;

- Sterling finds temporary support after Tuesday's sell-off.

US indices are seen pulling a little further away from record high levels on Wednesday, as we appear to see a slight shift in risk appetite although there are no signs at this stage of a broader trend developing.

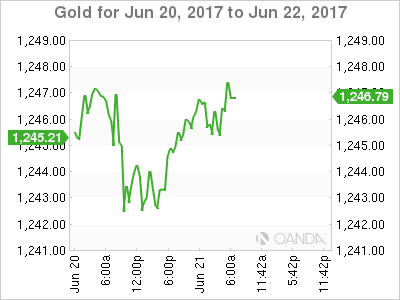

We're not in a particularly risk averse environment right now, by any extent, with numerous stock indices trading around record highs, but we do appear to be seeing some today. Gold is making small gains on the back of this today, having suffered over the last couple of weeks since falling just short of $1,300 for the second time in the last couple of months. Another move towards $1,300 again would be a very good sign for the bulls, with the dip having once again been bought at higher levels.

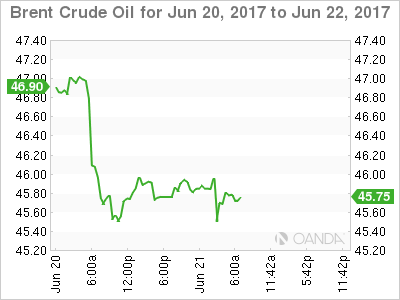

Oil has stabilised on Wednesday but may remain under pressure in the coming days, having fallen sharply on Tuesday despite there being no clear fundamental trigger for the move. Brent and WTI did find some support around $45.50 and $43, respectively, levels that have prompted similar reactions over the course of the last year. With bearish sentiment only appearing to grow though, you have to wonder whether these levels can hold on this occasion or whether $40 could be hit or even breached, in both cases.

For the latter to happen, we may need to see clear evidence that the production cut is either insufficient in clearing the excessive stocks or that compliance with the deal is in doubt. Inventory data from EIA will offer some insight into the success of the cut, with another small drawdown expected. API reported a similar number on Tuesday, claiming inventories fell by 2.72 million last week and while this has been a relatively good guide in the past, we did see last week that it isn't always reliable.

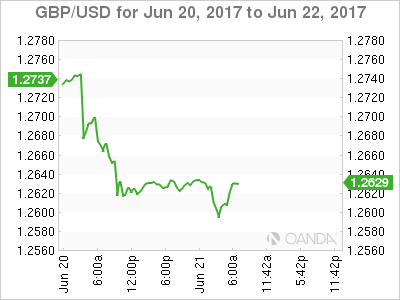

Sterling is trading a little lower once again on Wednesday, adding to losses made on the back of dovish comments from Bank of England Governor Mark Carney on Tuesday. The pound is trading a little lower against the dollar after finding some support around 1.26, a break of which could open up a move back towards April's lows just above 1.2350. Larger losses are being seen against the yen, which is seeing some safe haven flows today, along with Gold, although the key test here falls just above 138.50, a break of which could signal further downside ahead.

DAX Loses Ground, German Bonds Lower

The DAX index has dipped lower on Wednesday, giving up the slight gains from the Tuesday session. The index is down 0.51% and is currently at 12,743.50 points. On the release front, there are no major events in Germany or the eurozone. German 30-year bonds sold for 1.02% at auction, lower than the May release of 1.24%.

Germany's economy, the largest in the eurozone, continues to receive a thumbs-up from experts. On Tuesday, the German BDI Federation of Industry added its voice to the chorus, saying that Germany's economic output would increase by 1.5% in 2017. However, the BDI noted that the economy had been buoyed by a weaker euro, lower oil prices and the ECB's accommodative monetary policy. All three of these are ‘external factors', in the sense that Germany has limited influence on them, and a significant change in any one factor could hamper the country's economy. In the meantime, a growing global demand for German products has boosted the export sector and relieved concerns about President Trump's protectionist ‘America first' stance. There was another bullish forecast from the Ifo economic institute revised its prediction for Germany's GDP for 2017 from 1.8% to 2.0%, and economic growth from 1.5% to 1.8%. The report also forecast that inflation would jump to 1.7% in 2017, up from 0.6% in 2016. Stronger economic conditions in Germany have helped raise growth in the eurozone in 2017, although inflation levels in both Germany and the euro-area have been sluggish. This has prompted the ECB to reiterate that it has no plans to tighten monetary policy until inflation moves higher.

The Fed is done with rates hikes for now, but has hinted at one more rate hike in the second half of 2017. As for the markets, they have circled the December policy meeting as the most likely date for a rate move. The CME Group has pegged the odds of a September hike at just 13%, compared to 18% a week ago. However, the odds for a December increase are at 49%, and this could increase if Fed policymakers continue to wax positive about the economy. Earlier this week, Federal Reserve of New York President Charles Dudley continued the upbeat message, cautioning the Fed against halting its current tightening cycle. Dudley said that the tight labor market should lead to higher wages, which in turn would push inflation to the Fed's target of 2.0%. The markets like what they are hearing – not just the positive spin on the economy, but also that the Fed has signaled that it plans to reduce the bloated balance sheet of $4.2 trillion.

Oil Back In Bear Market After Latest Sell-Off, Commodity Currencies Fall Only Modestly

Crude oil prices fell by 2% on Tuesday as investors continued to fret about the lingering oversupply, which is showing no sign of easing despite 6 months of output restrictions by major producers. The recovery in prices from the 2014-15 downtrend stalled in January when they peaked at 1½-year highs.

WTI crude has since fallen by 22% from $55.24 on January 3 to a 7-month low of $42.75 a barrel yesterday. Brent crude is also down sharply, declining from $58.37 to $45.42 a barrel. Both benchmarks now stand significantly below their 200-day moving average, while the 50-day moving average has widened its bearish gap. This could be a sign of a new longer-term bear market, having emerged from its last one only a year ago.

In May, OPEC and some non-OPEC countries including Russia, agreed to extend last December's output deal to cap production by a further nine months until the end of March 2018. The initial agreement was for six months, starting in January 2017, but was extended after failing to have a major impact on reducing global inventories, which remain near record levels.

The main reason for the ineffectiveness of the output deal in reducing the supply glut is rising production elsewhere. US output has recovered sharply since the middle of 2016 as US shale producers have successfully managed to cut costs and consolidate following the downturn when many were forced out of the industry. The number of active oil rigs in the United States now stands at a two-year high of 747 according to data from Baker Hughes.

But the US isn't the only major producer that's seeing output rise. Libya and Nigeria, which although both are OPEC members, were exempted from the output deal due to the disruptions they experienced to their production from regional conflicts. However, as those disruptions have now ended, Libya looks set to ramp up its output to 1 million barrels a day in the coming weeks and Nigeria has resumed exports from its Forcados pipeline terminal.

While cheaper oil is good news for consumers, another big slump in oil prices has ramifications for both equity and currency markets. Energy stocks have already taken a knock from the latest plunge and an extended downslide could hurt the overall positive risk sentiment currently being enjoyed by equity markets around the world.

In forex markets, oil-linked currencies such as the Canadian dollar and Norwegian krone have come under pressure from yesterday's losses in oil prices, though so far the impact is limited. The US dollar is up 0.6% against its Canadian counterpart in the past two days and is eyeing the 1.33 level for the first time in a week. Against the Norwegian krone, the dollar has made more substantial gains, rising by 3% since the end of May.

However, a bigger concern for investors is the possible impact of a sustained fall in energy prices on monetary policy. Central banks around the world have just breathed a sigh of relief after eliminating the threat of deflation. A renewed risk of deflationary pressures could force major central banks such as the Federal Reserve to halt or even reverse its current cycle of gradual rate increases. Traders already responded to the possibility of lower inflation, and therefore lower interest rates as a result of the latest rout in oil prices, by buying US treasury notes. The yield on 10-year US treasuries slid back for a second day today towards last week's 7-month lows.

Oil Spill Sends Stocks And Yields Lower, Dollar Steady

With the lack of fundamentals on offer this week and central banks confiding FX moves to technical range trading, investors continue to feed off scraps looking for price vindication.

Global stocks remain on the back foot, pressured mostly by crude oil tumbling into a ‘bear’ market on concern a global supply glut will persist.

The yen has strengthened on haven demand while the pound weakens for a third day, trading atop of its April lows outright when PM Theresa May called a snap election.

The weakness in crude and other commodities is denting the Fed’s argument that weak inflation rates will be transitory, despite the domestic economy showing any signs of distress. Fixed income dealers are facing a ‘bull’ flattening treasury yield curve.

Note: Still to come on the Fed speaker list this week – Eric Rosengren, Robert Kaplan, Jerome Powell, James Bullard and Loretta Mester.

1. Stocks under pressure from commodities

A break lower in oil prices yesterday continues to weigh on global equity sentiment. Both Brent and WTI prices are testing 2016 September lows as technical pressure and continued skepticism regarding oil producers’ collective efforts to buoy the market.

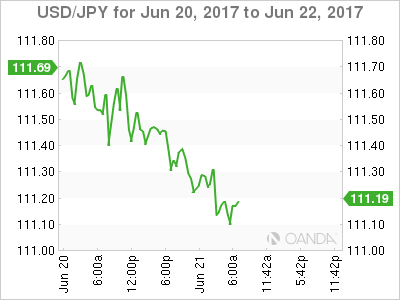

In Japan, the Nikkei share average fell -0.5% overnight as a stronger yen (¥111.20) sapped risk appetite, while mining stocks underperformed as oil prices tumbled. The broader Topix fell -0.4% after climbing for three days to the highest level since August 2015.

In China, Shanghai equities advanced after MSCI Inc. added China’s domestic stocks to its emerging-markets index – the Shanghai Composite rose +0.5%.

In Hong Kong, the Hang Seng and the Hang Seng China Enterprises Index each fell about -0.6% on fears that MSCI’s decision to include more mainland China stocks to its EM index will threaten the financial centre’s role as a key global investor gateway to China.

Down-under, Australia’s S&P/ASX 200 Index slumped -1.6% to the lowest in four months, with resource names sliding at least -3%.

In Europe, regional indices trade lower across the board following on from weakness in the U.S yesterday, with falling oil prices said to attribute to the negative sentiment.

U.S stocks are set to open in the ‘red’ (-0.4%).

Indices: Stoxx 600 -0.6% at 379, FTSE -0.2% at 7459, DAX -0.6% at 12738, CAC-40 -1.0% at 5243, IBEX-35 -0.8% at 10666, FTSE MIB -0.3% at 20745, SMI -0.8% at 8956, S&P 500 Futures -0.4%.

2. Oil falls as bulls discount OPEC cuts, gold shines

Oil prices have entered bear market territory, pressured mostly by a market concern that nonstop production from U.S shale fields is overwhelming OPEC’s efforts to ease a global supply glut.

Libya, exempt from the OPEC-led output cuts, is pumping the most in four-years while oil stored on tankers has reached a 2017 high this month.

August Brent crude futures are down -12c at +$45.85 a barrel – yesterday it fell nearly -2% yesterday to their lowest settlement since November. U.S crude futures (WTI) for August are down -7c at -$43.44, having hit its lowest price since September on Tuesday.

Note: So far this year, oil has lost -20% in value, its worst performance for the first six-months of the year in 20-years.

API data (American Petroleum Institute) yesterday showed U.S crude stockpiles last week had dropped more than forecast. Gasoline and distillate inventories rose.

The market will take its cue from today’s U.S government report (EIA) on inventories at 10:30 a.m. EDT.

Note: OPEC and non-OPEC oil producers’ compliance with the output deal reached 106 percent in May. However, a number of producers – notably Iraq, Saudi Arabia and Russia – aggressively ramped up output in the run-up to the deal.

Ahead of the U.S open, gold prices (+0.2% at +$1,245.82 per ounce) remain better bid after hitting its lowest price in five-weeks yesterday, buoyed as global equities fall and the ‘mighty’ dollar eases from its one-month highs following crudes tumble. However, the possibility of another interest rate hike by the Fed this year is underpinning the ‘bearish’ outlook for the yellow metal.

3. Energy slide supporting bull flatteners

Lower oil prices have sent market-based inflation expectation readings to the lowest in eight-months. The 10-year breakeven rate – the yield premium to hold US 10-year product relative to the 10-year TIPS (Treasury Inflation-Protected Securities) – is at +165.6 bps, down -2 bps this week.

Note: The breakeven rate rose above +200 bps in January, but now it is drifting below the Fed’s +2% target.

According to the latest JPMorgan weekly client survey last week, investors are the most bullish on Treasury prices in more than two-months. The share of investors expecting ‘lower’ yields, or longs, has risen to +18% for the week that ended this Monday – that doubles the share a week earlier.

The share of those expecting ‘higher’ yields, or shorts, falls to +25% from +27% and those that are neutral holds a +57% share vs. +64% a week earlier.

Treasuries are generally in favor as the stock markets sells off. The U.S 10-year yield has shed -3 bps overnight to reach +2.155% – the curve continues to flatten, as the 10/30-year spread falls further to below +58 bps.

4. Pound remains under pressure

The flight from oil and into long-dated government bonds is benefitting the safe-have yen (¥111.20), while the USD is holding its own elsewhere, despite lower yields.

The EUR stands at €1.1147 after hitting a three-week low, while sterling remains in the firing line sliding back under £1.2600. It took a spill after BoE Governor Carney hosed down speculation yesterday that he might soon back higher interest rates, saying he first wanted to see how the economy coped with Brexit talks.

Note: The last time the pound visited these levels was back on April 18, the day when PM Theresa May called a snap election.

Elsewhere, commodity currencies are feeling the pressure from lower oil price – CAD (C$1.3287), NOK ($8.5505) and MXN ($18.2582).

5. Bank of Japan (BoJ) monetary policy minutes

Bank of Japan (BoJ) Apr 27 Policy Meeting Minutes noted that most members saw momentum towards price goal was not firm enough. Policymakers agreed that the amount of government debt purchases will fluctuate under its QE program, but don’t expect such changes to pose problems for its guidance on market operations. They expressed more optimism about exports and industrial production, but remained cautious on inflation expectations.

In his press conference, BoJ Governor Kuroda reiterated that the BoJ still had long way to go before achieving the +2% price target; price momentum warranted close attention.

He also reiterated the view that it was appropriate to continue with strong easing. The JGB’s yield curve has been moving in line with BoJ’s market operation.

Elliott Wave Analysis: German DAX Trading Bearish

Stock markets are turning sharply down from the highs, with E-mini S&P500 loosing nearly 20 points in the last 24 hours, while Dax fell nearly 230 points so far. We see very strong reversal with impulsive price move on intraday charts so it's start of a bigger corrective drop that will be expected to continue after any three wave rally. On Dax that can be wave B which may find resistance near 12822 region. Ideally that wave B will start after the gap is filled from June 15.

German DAX, 30Min

Euro Calm As Investors Look For Cues

The euro continues to show little movement this week, and has inched higher in the Tuesday session. Currently, EUR/USD is trading at 1.1140. On the release front, there are no major events in the eurozone, so it could remain a quiet day for the pair. The US will release Existing Home Sales, which is expected to dip to 5.54 million. As well, the weekly Crude Oil Inventories will be published, with a forecast of -1.2 million barrels. On Thursday, the US releases unemployment claims.

The well-respected German BDI Federation of Industry added its voice to the chorus, saying that Germany's economic output would increase by 1.5%. At the same time, the BDI counseled caution, noting that the economy had been buoyed by a weaker euro, lower oil prices and the ECB's accommodative monetary policy. All three of these are ‘external factors', in the sense that Germany has limited influence on them, and a significant change in any one factor could hamper the country's economy.

The Federal Reserve has now raised twice this year, each time by 25 basis points. The Fed has hinted at one more rate in the second half of 2017, and the markets have circled December as the most likely date for a rate move. The CME Group has pegged the odds of a September hike at just 13%, compared to 18% a week ago. However, the odds for a December increase are at 49%, and this could increase if Fed policymakers continue to wax positive about the economy. Earlier this week, Federal Reserve of New York President Charles Dudley continued the upbeat message, cautioning the Fed against halting its current tightening cycle. Dudley said that the tight labor market should lead to higher wages, which in turn would push inflation to the Fed's target of 2.0%. The markets like what they are hearing – not just the positive spin on the economy, but also that the Fed has signaled that it plans to reduce the bloated balance sheet of $4.2 trillion.

Market Update – European Session: Focus Turns To Queen’s Speech For UK Approach On Brexit

Notes/Observations

Oil price weakness morphing into a broader-based risk-off move

PM May's decision to push ahead with the Queen's Speech without the agreement on working govt illustrates her commitment to lead the UK even with a minority government

MSCI will include China A shares in Emerging Markets Index; sees adding 222 China A large cap stocks

Overnight

Asia:

Bank of Japan (BOJ) Apr 27th Policy Meeting Minutes noted that most members saw momentum towards price goal not firm enough. No conflict between JGB purchases and market operation guidelines and agreed JGB purchases will fluctuate somewhat under YCC

MSCI to include China A-shares in its indices; opens Chinese mkt to more foreign investors; plans to add 222 China ‘A' large cap stocks to global emerging market benchmark

Europe:

German Fin Min Schaeuble reportedly urges CDU-CSU party lawmakers to support aid for Greece (**Note: Germany's Bundestag (lower house of parliament) to debate the latest compromise deal for Greece on Wed, Jun 21st)

France INSEE Stat Agency forecasts France 2017 GDP growth at 1.6% vs. 1.1% y/y (**Note: would be highest level of growth since 2011)

PM May: Need to deliver on Brexit in a way that commands maximum public support; will work with Parliament, Businesses and devolved Govts to ensure smooth and orderly EU exit

UK govt said to be considering a registry of EU citizens living in the UK; to gauge demand for residency applications post Brexit

Reports that PM May to remove unpopular policies from Queen's Speech; Govt might shelve energy bill price cap

Northern Ireland DUP sources: British govt must give greater focus to negotiations to form a voting bloc; our party cannot be taken for granted by Conservative Party.

Conservative Party source noted that talks with DUP were ongoing; continuing to work towards a confidence and supply arrangement with DUP. Additional press reports that Power share deal between DUP and Tories likely on Thurs, Jun 22nd

Americas:

Fed's Kaplan (moderate, voter): Wants to keep an open mind on amount of rate hikes this year. Inflation has been notably sluggish; would like to see evidence that weak inflation is transitory

House Speaker Ryan: we are going to fix this nation's tax code once and for all. will consolidate the existing seven brackets into three, double the standard deduction, and simplify things to the point that you can do your taxes on a form the size of a postcard

Republican Karen Handel beat Jon Ossoff in Georgia Congressional race (53-47%) (**Insight: Georgia was viewed as Democrats best shot at a win; most expensive House race in history)

Brazil federal police said to have found evidence that President Temer received bribes

Energy:

Saudi Arabia King Salman removed Crown Prince Mohammed bin Nayef and replaced him with Deputy Crown Prince Mohammed bin Salman

Weekly API Oil Inventories: Crude: -2.7M v +2.8M prior

Economic Data

(NL) Netherlands Jun Consumer Confidence: 23 v 23 prior

(SE) Sweden Jun Consumer Confidence: 102.5 v 105.0e; Manufacturing Confidence: 119.9 v 115.0e, Economic Tendency Survey: 112.1 v 110.4e

(ZA) South Africa May CPI M/M: 0.3% v 0.2%e; Y/Y: 5.4% v 5.4%e (2nd straight month annual CPI was within the target range of 3.0-6.0%)

(ZA) South Africa May CPI Core M/M:0.1% v 0.1%e; Y/Y: 4.8% v 4.8%e

(UK) May Public Finances (PSNCR): +£13.4B v -£15.2B prior; Public Sector Net Borrowing: £6.0B v £7.0Be

Fixed Income Issuance:

(IN) India sold total INR140B vs. INR140B indicated in 3-month and 12-month Bills (INR80B and INR60B respectively

(DK) Denmark sold total DKK2.25B in 2020 and 2027 bonds

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx 600 -0.6% at 379, FTSE -0.2% at 7459, DAX -0.6% at 12738, CAC-40 -1.0% at 5243, IBEX-35 -0.8% at 10666, FTSE MIB -0.3% at 20745, SMI -0.8% at 8956, S&P 500 Futures -0.4%]

Market Focal Points/Key Themes European Indices trade lower across the board following on from weakness in the US yesterday, with falling Oil prices said to attribute to the negative sentiment. On the corporate front UK based Whitbread trades higher by over 4% after strong LFL sales, whilst Berkeley Group trades higher after strong FY results. Scout 24 trades lower after Deutsche Telekom sold its entire stake in company, while Provident financial trades sharply lower after issuing a profit warning. Looking ahead to the US morning, scheduled earnings include Carmax, Actuant and Winnebago industries.

Equities

Consumer discretionary [Whitbread [WTB.UK] +4.5% (Trading update), Scout24 [G24.DE] -3.3% (Deutsche telekom places shares), Hornby [HRN.UK] +11.2% (Earnings), SAS [SAS.SE] -3% (Earnings)]

Real Estate: [Berkeley Group [BKG.UK] +2.8% (FY Results)]

Healthcare: [Shire Pharm [SHP.UK[ +1.5%(FDA approval for Mydayis)]

Energy: [Centrica [CNA.UK] +2.0 (Divestment)]

Financial [Provident Financial [PFG.UK] -16% (profit warnings)]

Speakers

ECB published details of corporate bond purchases and noted it had purchased 950 securities from around 200 groups. 12% of CSPP holdings were purchased at negative yields but above the Deposit Rate (**Note: currently at -0.40%) and 55% of corporate bonds had been either German or French paper

BOE agent Q2 survey noted that the moderate underlying growth in activity had continued overall. Direct impact of the fall in sterling on cost inflation for manufacturers' raw materials had eased, but increased costs continued to pass through supply chains into retail prices.

Italy PM Gentiloni - commented in Parliament ahead of EU Leader Summit that Italy sought clarity in Brexit negotiations and was neither for a hard or soft Brexit. Believed that UK is not in a strong position at the start of the negotiations

EU Commission paper said to note that Greece needs additional debt relief to regain trust of investors even though it will have €9B in cash buffer after it exits from bailout program

Finland Finance Ministry updated economic forecasts which raised both 2017 and 2018 growth outlook. Raised 2017 GDP growth from 1.2% to 2.4% and raised 2018 GDP growth from 1.0% to 1.6%

Czech Central Bank Gov Rusnok noted that the continuing strengthening of CZK currency (Koruna) could be reason for slower raising of rates. Rate hike in Q3 was not likely

BOJ Gov Kuroda reiterated BOJ still had long way to go before achieving the 2% price target; price momentum warranted close attention. Reiterated view that was appropriate to continue with strong easing. Yield curve has been moving in line with BOJ's market operation

China Foreign Ministry spokesperson Geng Shuang: Govt efforts on Korean Peninsula is unrelenting; not motivated by external pressure

Currencies

Major FX pairs were generally range-bound in quiet trading as traders noted that there was little important economic data. EUR/USD was steady at 1.1135 area

The GBP currency remained wobbly in the aftermath of dovish rhetoric by BOE Gov Carney on Tuesday. The GBP/USD hovered around the 1.26 level. Focus turns to the Queen's Speech which is delivered by the UK PM and outlines the legislative agenda for the parliamentary session

Commodity currency complex pressured by oil price. CAD, NOK and RUB were all softer in the session as oil prices maintained its soft footing. Oil prices held near multi-month lows on Wednesday as investors discounted evidence of strong compliance by OPEC and non-OPEC oil producers with a deal to cut global output.

Fixed Income

Bund futurestrade at 165.15 up 15 ticks, as European stocks slide as oil falls into bear market territory. Resistance lies near the 165.52 level, followed by 166.21. A break of the 163.89 support level could see lows target 162.05 followed by 160.30.

Gilt futures trade at 129.64 up 17 ticks with the focus on BOE's Haldane speech due at 12pm London and the Queen's speech, which provide insight on PM May's objectives at 11:30am London. Price is approaching the higher third portion of the June trading range. If price becomes bearish and drops below the noted 129.14 level, initial support lies at the 128.27 level, with key support at the 127.96 support level. An acceleration lower could test the 127.43 region. Resistance lies at the 129.80 level followed by 132.65.

Wednesday's liquidity report showed Tuesday's excess liquidity fell to €1.6096T a drop of €25.4B from €1.6350T prior. Use of the marginal lending facility rose to €380M from €338M prior.

Corporate issuance saw over $1.5B come to market via 2 issues headlined by Federal Realty Investment Trust $400M 2-part senior unsecured note offering and Jackson National Life Global Funding $1.1B 3-part FRN FA-backed notes

Looking Ahead

(DE) Germany's Bundestag (lower house of parliament) to debate the latest compromise deal for Greece

(FR) France govt announcement on composition of the new govt post-election

(BR) Brazil Jun CNI Industrial Confidence: No est v 53.7 prior

05:30 (SL) Sri Lanka National CPI Y/Y: No est v 8.4% prior

05:30 (DE) Germany to sell €1.0B in 2.5% 2044 Bunds

05:30 (PT) Portugal Debt Agency (IGCP) to sell €1.0-1.25B in 6-month and 12-month Bills

06:00 (IL) Israel Apr Manufacturing Production M/M: No est v 2.5% prior

06:00 (RU) Russia to sell combined RUB30B in 2022 and 2024 OFZ bonds

06:15 (UK) Queen's speech in Parliament

06:45 (US) Daily Libor Fixing

07:00 (US) MBA Mortgage Applications w/e Jun 16th: No est v 2.8% prior

07:00 BOE's Haldane (chief economist)

08:15 (UK) Baltic Dry Bulk Index

10:00 (US) May Existing Home Sales: 5.55Me v 5.57Me

10:00 (DE) German Chancellor Merkel with Finland PM Siplia in Berlin

10:30 (US) Weekly DOE Crude Oil Inventories

12:00 (CA) Canada to sell 10-Year Bonds

15:00 (AR) Argentina Q1 GDP Q/Q: No est v 0.5% prior; Y/Y: +0.1%e v -2.1% prior

17:00 (NZ) New Zealand Central Bank (RBNZ) Interest Rate Decision: Expected to leave Official Cash Rate (OCR) unchanged at 1.75%

GOLD Ready To Bounce Back, SILVER Selling Pressures Continues, CRUDE OIL Bearish Breakout.

GOLD Ready to bounce back.

Gold's medium-term momentum is positive. Hourly support is located at 1241 (intraday low). Stronger support is given at 1214 (09/05/2017 low). Expected to show renewed upside pressures.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

SILVER Selling pressures continues.

Silver declines. Closest support is given at 16.44 (18/05/2017 low). Strong support is given at 16.06 (09/05/2017 low). Key resistance is given at a distance at 19.00 (09/11/2017 high). The road seems wide open for further decline.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

CRUDE OIL Bearish breakout.

Crude Oilis finally continuing its decline since the recent collapse from $52. Support is given at a distance 43.76 (05/05/2017 low). Expected to show further decline.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 24.82 (13/11/2002) while resistance can now be found at 55.24 (03/01/2017 high).

EUR/JPY Short-Term Buying Pressures Are Fading, EUR/GBP Monitoring 6-Month High, EUR/CHF Pushing Lower.

EUR/JPY Short-term buying pressures are fading.

EUR/JPY has bounced back after breaking hourly support given at 122.56 (18/05/2017 low) has been broken. Hourly resistance can be found at 125.82 (16/05/2017 high). Major support is given at 114.90 (18/04/2017 low).

In the longer term, the technical structure validates a medium-term succession of lower highs and lower lows. As a result, the resistance at 149.78 (08/12/2014 high) has likely marked the end of the rise that started in July 2012. Strong support at 94.12 (24/07/2012 low) looks nonetheless far away.

EUR/GBP Monitoring 6-month high.

EUR/GBP is pushing higher towards resistance given at 0.8866 (12/06/2017 high). Other support can be found at 0.8652 (08/06/2017 low).

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.

EUR/CHF Pushing lower.

EUR/CHF's bearish pressures are back. Yet, we believe that the medium-term pattern suggests us to see continued bearish pressures towards hourly support that can be found at 1.0792 (03/05/2017 low).

In the longer term, the technical structure is mixed. Resistance can be found at 1.1200 (04/02/2015 high). Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).