Sample Category Title

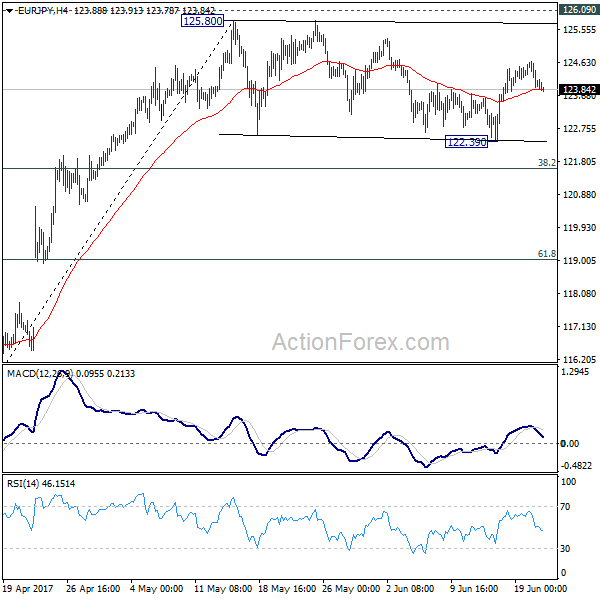

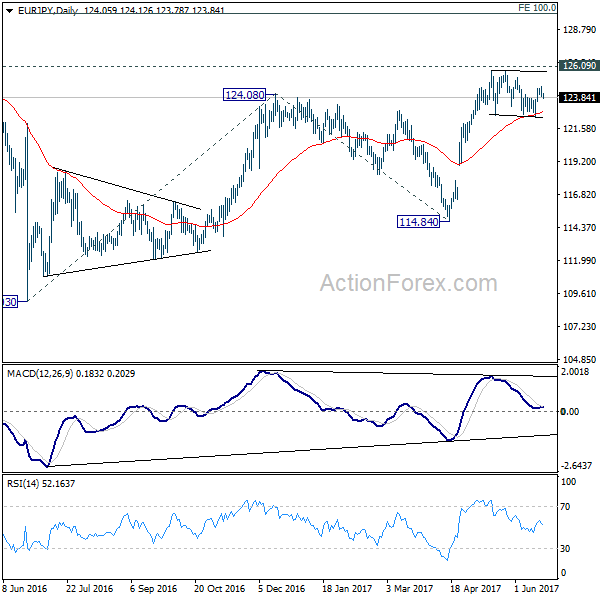

EUR/JPY Daily Outlook

Daily Pivots: (S1) 123.79; (P) 124.21; (R1) 124.51; More...

EUR/JPY's consolidation from 125.80 is set to extend further and intraday bias is turned neutral first. In case of another fall, downside should be contained by 38.2% retracement of 114.84 to 125.80 at 121.61 to bring rebound and then rise resumption. On the upside, decisive break of 126.09 resistance will extend the whole rebound from 109.03 to 100% projection of 109.03 to 124.08 from 114.84 at 129.89.

In the bigger picture, focus is staying on 126.09 support turned resistance. Decisive break there will confirm completion of the down trend from 149.76. And in such case, rise from 109.20 is at the same degree and should target 141.04 resistance and above. Meanwhile, rejection from 126.09 and break of 114.84 will extend the fall from 149.76 through 109.20 low.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.0844; (P) 1.0862; (R1) 1.0873; More...

Intraday bias in EUR/CHF remains neutral for the moment. On the upside, break of 1.0908 will indicate that pull back from 1.0986 has completed a 1.0837 already. In that case, intraday bias will be turned to the upside for retesting 1.0986/0999 resistance zone. Below 1.0837 will extend the correction. Still, we'd expect strong support from 1.0791/0872 support zone to bring rebound.

In the bigger picture, the price actions from 1.1198 are seen as a corrective move. Such correction could have completed after defending 38.2% retracement of 0.9771 to 1.1198 at 1.0653. Decisive break of 1.0999 resistance will target a test on 1.1198 high. For now, this will be the preferred case as long as 1.0791 support holds.

Market Update – Asian Session: China A-Shares Included In MSCI

Asia Mid-Session Market Update: China A-Shares included in MSCI; Toshiba finalizes preferred bidder selection for chip unit

US Session Highlights

(US) Treasury Sec Mnuchin: Confirms Tax receipts are running little lower than expected - CNBC

(US) Fed’s Rosengren (moderate, non-voter): Low rate environment likely to persist into the future; likely to make fighting recessions tougher - comments from Amsterdam

(US) Q1 CURRENT ACCOUNT: -$116.8B V -$123.6BE

(US) May Philadelphia Fed Non-Manufacturing General Regional Business Conditions: 33.6 v 25.6 prior

Lower energy prices took their toll on stocks as the main indices all but wiped out yesterday's gains. More hawkish comments from various Fed officials also gave investors less confidence in pushing prices higher. Today's worst performer in S&P was Energy, down 1.3%, best sector was Health Care gaining 0.3%

US markets on close: Dow -0.3%, S&P500 -0.7%, Nasdaq -0.8%

Best Sector in S&P500: Health Care

Worst Sector in S&P500: Energy / Consumer Discretionary

Biggest gainers: REGN +5.0%; ALXN +2.5%; LEN +2.1%

Biggest losers: FTR -7.6%; CMG -7.3%; OKE -5.4%

At the close: VIX 10.9 (+0.5pts); Treasuries: 2-yr 1.35% (+1bps), 10-yr 2.15% (-4bps), 30-yr 2.74% (-5bps)

US movers afterhours

LZB Reports Q4 $0.57 v $0.46e, Rev $412.7M v $401Me; authorizes share repurchase for up to 6M shares (12.3% of shares outstanding); +12.6% afterhours

RHT Reports Q1 $0.56 v $0.52e, Rev $676.8M v $647Me; Guides Q2 ~$0.67 v $0.65e, Rev $695-702M v $677Me ; +10.1% afterhours

ADBE Reports Q2 $1.02 v $0.94e, Rev $1.77B v $1.73Be; Guides Q3 ~$1.00 v $0.95e, R$1.82B v $1.8Be; +3.6% afterhours

Politics

(US) Republican candidate Karen Handel to win special congressional House election in Georgia 6th district, allowing Republic part to keep its seat

(BR) Brazil federal police said to have found evidence that President Temer received bribes - press

Key economic data

(AU) AUSTRALIA MAY SKILLED VACANCIES M/M: 1.2% V +0.9% PRIOR

(AU) AUSTRALIA MAY WESTPAC LEADING INDEX M/M: 0.0% V -0.1% PRIOR

(JP) Japan Apr All Industry Activity Index M/M: 2.1% v 1.6%e

Speakers and Press

China

(CN) MSCI plans to add 222 China A Large Cap stocks, representing on a pro forma basis approximately 0.73% of the weight of the MSCI Emerging Markets Index at a 5% partial Inclusion Factor.

(CN) MSCI CEO: Expects initial inflows from China A-share inclusion to be $17-18B

(CN) S&P Global chief ratings officer Kraemer: China rating has a negative outlook, signaling that a downgrade is a real possibility

Japan

(JP) Bank of Japan (BOJ) Apr 27th Policy Meeting Minutes: Momentum toward price goal not firm enough; High chance exports will continue to show solid gains; Risks to economy are skewed to downside.

(JP) Japan govt (Cabinet office) expected to raise economic assessment in its June report on June 22nd - Nikkei

Australia/New Zealand

(NZ) According to New Zealand's Home Loan Affordability Reports, typical first home buyers in Auckland need over 7 years to save a 20% downpayment on median wages - NZ press

(NZ) ANZ economist: Today's dairy auction prices disappointed amid lower participation from China - NZ Press

Korea

(KR) South Korea FTC chair and Finance Minister to hold a meeting today about the economy - press

Asian Equity Indices/Futures (00:30ET)

Nikkei -0.5%, Hang Seng -0.6%, Shanghai Composite +0.2%, ASX200 -1.6%, Kospi -0.6%

Equity Futures: S&P500 -0.2%; Nasdaq -0.2%, Dax -0.1%, FTSE100 -0.4%

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.1125-1.1140; JPY 111.20-111.50; AUD 0.7555-0.7585; NZD 0.7220-0.7245

Aug Gold +0.4% at 1,247/oz; Aug Crude Oil -0.1% at $43.47/brl; July Copper -0.1% at $2.55/lb

(CN) PBOC to inject combined CNY40B v CNY10B prior in 7-day reverse repos

(CN) PBOC SETS YUAN MID POINT AT 6.8193 V 6.8096 PRIOR; Weakest Yuan fix since May 31st and 2nd straight weaker setting

(KR) Bank of Korea (BOK) sells KRW2.4T in 2-yr monetary stabilization bonds; avg yield 1.63% v 1.58% prior

(AU) Australia Finance Ministry (AOFM) sells A$800M in 2.75% 2028 bonds; avg yield 2.5124% v 2.4988% prior; bid-to-cover 2.69x v 3.26x prior

Asia equities notable movers

Australia

Yowie Group (YOW) -4.7%; Cuts FY17 Rev growth guidance to 55% from 70%; Guides FY18 Rev +55-70%

QBE (QBE) -9.8%; Top 3 operating divisions on track to report results in line with budget; Emerging markets experienced much higher than expected claims in Jan-May, H1 combined op ratio may reach 110% (update)

Retail Food Group (RFG) -10.2%; Cuts FY17 Underlying Net profit growth ~15% y/y (prior 20%)

Japan

Toshiba (6502) -1.3%; Selects INCJ-led group that includes Bain, SK Hynix, and DBJ as preferred bidder for chip unit sale; Aim to complete chip sale by end of FY17/18 - Japan press

Kubota (6326) -2.2%; CLSA Cuts 6326.JP to Outperform from Buy

Hong Kong

Midland Holdings Limited (1200) +6.0%; Announces profit alert: Guides H1 Net profit v loss HK$134M y/y

UBA Investments Limited (768) +4.6%; Reports FY Net profit HK$4.8M v loss HK$10.2M y/y

EVA Precision Industrial Holdings (838) +2.4%; Guides H1 Net +170% y/y

Aussie Trading Lower In The Morning Session

For the 24 hours to 23:00 GMT, the AUD declined 0.24% against the USD and closed at 0.7579.

LME Copper prices declined 0.2% or $13.5/MT to $5673.5/MT. Aluminium prices rose 1.5% or $27.5/MT to $1889.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7574, with the AUD trading 0.07% lower against the USD from yesterday's close.

Overnight data revealed that Australia's Westpac leading index fell 0.02% MoM in May. In the previous month, the index had registered a revised drop of 0.08%.

The pair is expected to find support at 0.7550, and a fall through could take it to the next support level of 0.7526. The pair is expected to find its first resistance at 0.7611, and a rise through could take it to the next resistance level of 0.7648.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Current Account Surplus Narrowed In April

For the 24 hours to 23:00 GMT, the EUR declined 0.13% against the USD and closed at 1.1135.

On the macro front, the Euro-zone's seasonally adjusted current account surplus narrowed more-than-expected to a level of €22.2 billion in April, following a revised surplus of €35.7 billion in the prior month, while markets expected the region's current account surplus to narrow to a level of €31.3 billion.

Separately, in Germany, the producer price index dropped more-than-anticipated by 0.2% on a monthly basis in May. The index had advanced 0.4% in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.1135, with the EUR trading flat against the USD from yesterday's close.

The pair is expected to find support at 1.1114, and a fall through could take it to the next support level of 1.1094. The pair is expected to find its first resistance at 1.1160, and a rise through could take it to the next resistance level of 1.1186.

With no crucial economic releases in the Euro-zone today, investors look forward to the US existing home sales for May and MBA mortgage applications data, both slated to release later in the day.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

BoE’s Carney – Not The Right Time To Hike Interest Rates

For the 24 hours to 23:00 GMT, the GBP declined 0.82% against the USD and closed at 1.2629, after the Bank of England (BoE) Governor, Mark Carney, doused expectations of an interest rate hike any time soon, stating that the nation's economic outlook is marred by the uncertainties of Brexit. Carney warned that given the dwindling consumer spending and business investment in the nation and given the still subdued domestic inflationary pressures, the central bank would wait to see how Brexit negotiations play out.

In the Asian session, at GMT0300, the pair is trading at 1.2628, with the GBP trading marginally lower against the USD from yesterday's close.

The pair is expected to find support at 1.2569, and a fall through could take it to the next support level of 1.2509. The pair is expected to find its first resistance at 1.2723, and a rise through could take it to the next resistance level of 1.2817.

Looking ahead, market participants will focus on UK's public sector net borrowing data for May, slated to release in a few hours.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

BoJ Minutes – Members Comfortable With Fluctuations In Government Debt Purchases

For the 24 hours to 23:00 GMT, the USD declined 0.25% against the JPY and closed at 111.35.

In the Asian session, at GMT0300, the pair is trading at 111.29, with the USD trading marginally lower against the JPY from yesterday's close.

According to minutes of the Bank of Japan's (BoJ) April meeting minutes, policymakers grew more optimistic about Japanese exports and industrial production, but expressed caution on inflation expectations. Further, the policymakers agreed that the amount of government debt purchases will fluctuate under its quantitative easing programme, but this was unlikely to affect its guidance.

On the data front, Japan's all industry activity index recorded a rise of 2.1% on a monthly basis in April, more than market expectations for a gain of 1.6% and after recording a revised drop of 0.7% in the prior month.

The pair is expected to find support at 111.10, and a fall through could take it to the next support level of 110.90. The pair is expected to find its first resistance at 111.64, and a rise through could take it to the next resistance level of 111.98.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

SECO Cuts Switzerland’s Economic Growth Forecast For 2017

For the 24 hours to 23:00 GMT, the USD declined 0.07% against the CHF and closed at 0.9748.

Yesterday, the State Secretariat for Economic Affairs (SECO), in its quarterly economic forecasts report, trimmed Switzerland's 2017 growth outlook by 0.2% to 1.4%, citing subdued inflation in the nation. Meanwhile, projection for 2018 was retained at 1.9%.

In the Asian session, at GMT0300, the pair is trading at 0.9744, with the USD trading a tad lower against the CHF from yesterday's close.

The pair is expected to find support at 0.9725, and a fall through could take it to the next support level of 0.9705. The pair is expected to find its first resistance at 0.9765, and a rise through could take it to the next resistance level of 0.9785.

Investors look forward to the Swiss National Bank's quarterly bulletin report, scheduled to release later in the day.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Loonie Trading Marginally Lower This Morning

For the 24 hours to 23:00 GMT, the USD rose 0.35% against the CAD and closed at 1.3271.

In economic news, Canada's wholesale sales advanced above expectations by 1.0% on a monthly basis in April, following a revised 1.2% rise in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.3278, with the USD trading a tad higher against the CAD from yesterday's close.

The pair is expected to find support at 1.3226, and a fall through could take it to the next support level of 1.3175. The pair is expected to find its first resistance at 1.3307, and a rise through could take it to the next resistance level of 1.3337.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

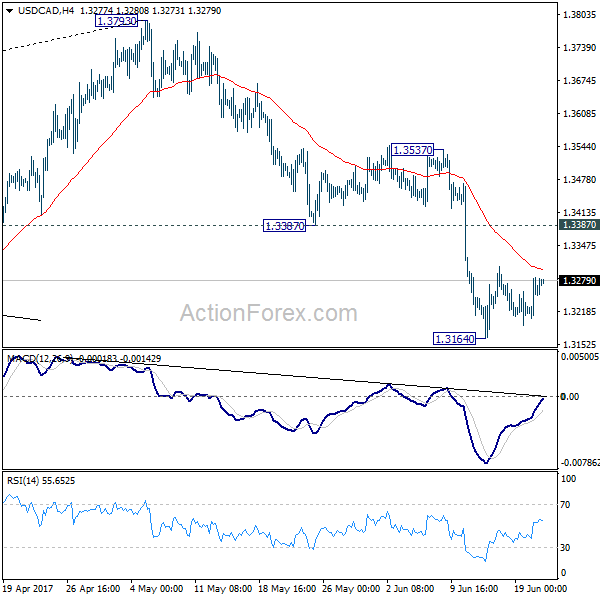

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3218; (P) 1.3252; (R1) 1.3300; More....

Intraday bias in USD/CAD remains neutral as consolidation from 1.3164 continues. Another recovery could be seen. But upside should be limited by 1.3387 support turned resistance and bring fall resumption. We're holding on to the view that corrective rise from 1.2460 has completed at 1.3793 already. Below 1.3164 will target 1.2968 cluster support, 61.8% retracement of 1.2460 to 1.3793 at 1.2969.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. Rise from 1.2460 is seen as the second leg and has completed at 1.3793, ahead of 61.8% retracement of 1.4689 to 1.2460 at 1.3838. Break of 1.3222 should now indicate the start of the third leg while further break of 1.2968 should confirm. In that case, USD/CAD should decline through 1.2460 support to 50% retracement of 0.9406 to 1.4869 at 1.2048.