Sample Category Title

Swiss National Bank Remains On Hold

'As long as the process of political stabilisation continues in Europe, the need for foreign exchange interventions should diminish.' — Maxime Botteron, Credit Suisse

As markets expected, the Swiss National Bank left its loose monetary policy and interest rates unchanged at its meeting on Thursday amid the high degree of uncertainty in Europe. Policymakers voted to leave the Libor rate at -0.75% and the three-month Libor target range at -1.25% to -0.25%. The Bank remained highly in favour of negative interest rates and was committed to forex interventions amid the significantly overvalued Swiss Franc. Nevertheless, the SNB noted that the global economy and labour markets were recovering as expected, while inflation growth remained moderate in the majority of developed economies. According to the Bank's forecasts, the domestic economy is expected to expand 1.5% this year, whereas inflation is set to rise 0.3%. In 2018 and 2019 the inflation rate is expected to climb 0.3% and 1.0%, respectively. The Bank expressed optimism over the economic outlook for the global economy. Also, monetary conditions in the United States are expected to 'gradually normalise' in the upcoming months. Thursday's data also showed that the Central bank bought $48.4B in Swiss francs this year.

British Retail Sales Suffers In May, Bank Of England Leaves Policy And Rates Unchanged

'A slowdown in household consumption, and GDP as a whole, had recently begun, and it was too early to judge with confidence how large and persistent it would prove to be.' — Mark Carney, Bank of England

British retail sales dropped more than expected last month, pointing to high inflationary pressures driven by the weak Pound. The Office for National Statistics reported on Thursday that retail sales dropped 1.2% month-over-month in May, following the preceding month's upwardly revised gain of 2.5% and falling behind analysts' expectations for 0.9% drop. May's fall suggested that the sharp rise in inflation after the country's decision to leave the European Union started to put significant pressure on households that are the main GDP contributors. On an annual basis, retail sales climbed 0.9% during the reported month, whereas analysts anticipated a rise of 1.7%. Earlier this week, Visa reported that UK consumers cut their spending for the first time in almost four years in May. Later in the day, the Bank of England left its policy and interest rates at 0.25% but moved closer to the rate-rise trail, as three out of eight policymakers voted to raise rates, lifting the Sterling against other major currencies. However, some analysts suggested that the BoE would continue tolerating inflation above the 2% target for some time.

Initial Jobless Claims Drop To 237K, Federal Reserve Banks Release Manufacturing Indices

'At present, it appears the labor market data rather than the inflation data are in the driving seat for data-dependent Fed policy.' — John Ryding, RDQ Economics

The number of Americans filing for unemployment benefits dropped more than expected last week. The Labour Department reported on Thursday that initial jobless claims fell 8K to 237K in the week ended June 9, while market analysts anticipated a slighter decrease to 241K during the reported week. According to analysts, the US labour market is at or close to full employment, with the unemployment rate a 16-year low of 4.3%. Thursday's data also showed that the number of people continuing to receive jobless benefits rose 6K to 1.94M in the week ending June 3. Other data released by the Federal Reserve showed that import prices dropped 0.3% last month, following the prior month's downwardly revised rise of 0.2% and falling behind expectations for a 0.1% increase. Also, the New York State Fed reported that its Manufacturing Index for the region surged to 19.8 in June, up from May's -1.0, whereas the Philadelphia Fed's Manufacturing Index for the Philadelphia State fell to 27.6 points in June, whereas analysts anticipated a steeper drop to 25.5 from May's 38.8.

Bank Of Japan Keeps Policy And Rates Unchanged

'Wages and the labor market are most closely linked to consumer prices. The labor market has tightened even further, so I think the BOJ wanted to highlight that point by upgrading its assessment on consumer spending.' — Hiroshi Miyazaki, Mitsubishi UFJ Morgan Stanley Securities

The Bank of Japan left its monetary policy and interest rates unchanged at its meeting on Friday but expressed optimism over the economic outlook for the domestic economy and its export sector. As expected, policymakers voted to keep the Bank's short-term interest rates at -0.1% and the yield on the 10-year Japanese government bond around zero. Moreover, the Central bank left the balance of its holdings increases at an annual pace of 80T yen ($729.33B). The BoJ's meeting followed the US Federal Reserve's meeting, at which US policymakers raised interest rates for the second time this year, predicted one more rate hike in 2017 and outlined a plan for shrinking the Bank's balance sheet. The BoJ pointed to low private consumption and attributed its weakness to subdued inflation growth. The Bank said that overseas economies, including emerging ones, continued expanding at a moderate pace. As to the domestic economy, the Bank said that the economy was stepping on a path of a moderate expansion. The BoJ is expected to remain on hold until it sees some improvement in inflation.

Technical Outlook: GBPUSD – Strong Resistance At 1.2800 Zone Caps Post-BoE Rallies For Now

Cable retested key 1.2800 resistance zone (daily cloud top/55SMA/daily Tenkan-sen) on rally after surprise BoE rate vote o Thursday but upside remains limited for now. Strong signal of indecision was generated by double long-legged Dojis on Wed/Thu, with mixed technical studies (bearishly aligned dailies and neutral to positive techs on lower timeframes). The pair needs to break out of initial 1.2700/1.2800 range to generate stronger direction signals. In absence of economic releases from the UK, focus turns towards US housing data, due later today. Bullish scenario on sustained break above 1.2800 zone would open resistances at: 1.2841/46 (daily Kijun-sen/Fibo 61.8% of 1.2977/1.2635 downleg), 1.2858 (falling 20SMA and 1.2883 (falling 30SMA). Alternatively, loss of 1.2700 support zone (near Fibo 61.8% of 1.2635/1.2617 recovery leg) would weaken near-term structure and re-focus near-term base at 1.2640 zone, reinforced by 100SMA.

Res: 1.2795, 1.2806, 1.2817, 1.2846

Sup: 1.2750, 1.2722, 1.2704, 1.2690

Silver Gold And Oil Limp Into Friday

Gold, Silver and Crude are battered and bruised as the week ends with a stronger U.S. Dollar twisting the knife.

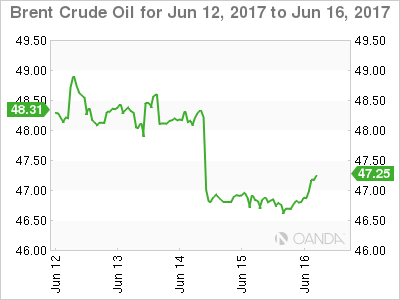

Crude oil limps into the last day of the week with both Brent and WTI down about 30 cents from the previous day’s lows, but still mired at the bottom of their recent ranges. Oil is unlikely to find solace into the weekend either with tonight’s Baker Hughes Rig Count expected to deliver its now weekly increase of operational rigs which totalled 927 as of last week.

With both contracts now in sight of the May panic liquidation lows, Opec and Non- Opec may find some cold comfort that at these levels many U.S. shale producers are maybe breaking into a cold sweat now as well. Much will depend on how much forward production shale has hedged via the selling of oil futures and we should get more visibility into this as we roll into the end of the month. But with U.S. shale production expected to hit 10 million bpd in 2018, this will only put off the day of reckoning for them as well.

Brent spot was trading at 46.80 this morning with initial support at 46.50 followed by the all-important May low at 46.30 just behind. A break of this level potentially opens up a test of Novembers low at 43.00. Daily resistance lies distant at 49.00.

WTI spot was trading at 44.40 with initial support around the overnight low of 44.15 followed by May’s panic sell-off low at 43.50. Beyond this level potentially sees a test of the November low at 42.00. Again, resistance is distant at 46.50.

PRECIOUS METALS

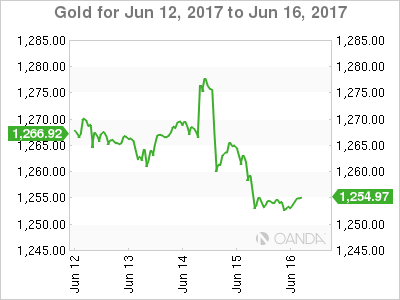

U.S. short end yields surged overnight sending the U.S. Dollar higher across the board and nipping any nascent rally in gold and silver in the bud after a tough week for both. Wednesday’s potentially bullish technical indicators are now a distant memory as gold in particular eyes a critical support region.

In the absence of any geopolitical risk to help them, the price action in both gold and silver of late seems to imply that traders still have plenty of short-term long positioning on their books. Quite a lot of it most likely at less than salubrious levels above 1280.00 and 17.5000 respectively. It may leave both metals vulnerable to a further washout into the weekend if the U.S. Dollar strength persists.

GOLD

Gold is trading at 1254.15 this morning with the critical support region of 1240/1245 lying just below. It contains a daily double bottom and the 100 and 200-day moving averages with a daily close below signalling a deeper technical correction. Resistance lies at 1266 initially and then 1280 with the 1296/1300 but a distant memory.

SILVER

Silver broke it’s 100 and 200-day moving averages a week ago, and both lie at 17.5000 and form significant resistance now. Silver trades at 16.7900 this morning with support nearby at 16.6400, the overnight low and then 16.4150.

Elliott Wave Analysis: USDJPY Showing A Completed Big Correction, A Change In Trend Can Be Happening

USDJPY is displaying a strong rally away from 108.50 region, where a corrective wave 2 of a higher degree was completed. Current impulsive activity can be now start of a minimum three wave rise, that will ideally reach levels at 113.0 and above. A breach above the 110.82 level is an indication and a confirmation, that a change in trend is happening, so more gains can be in for the pair.

USDJPY, 4H

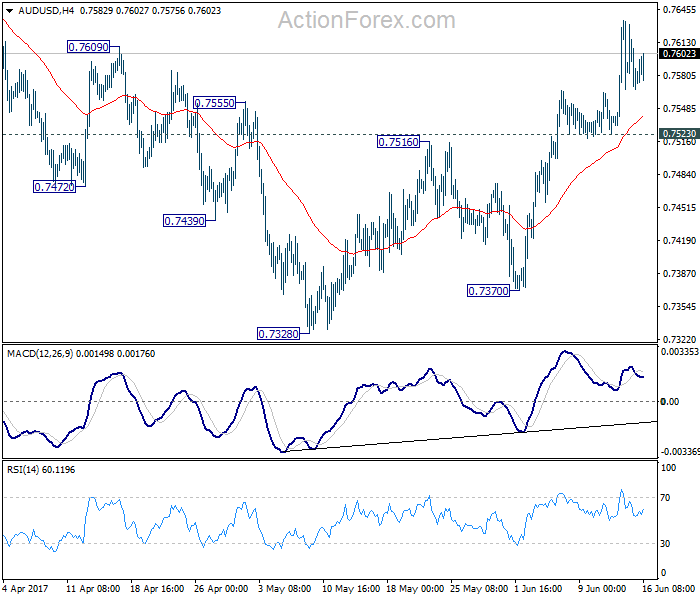

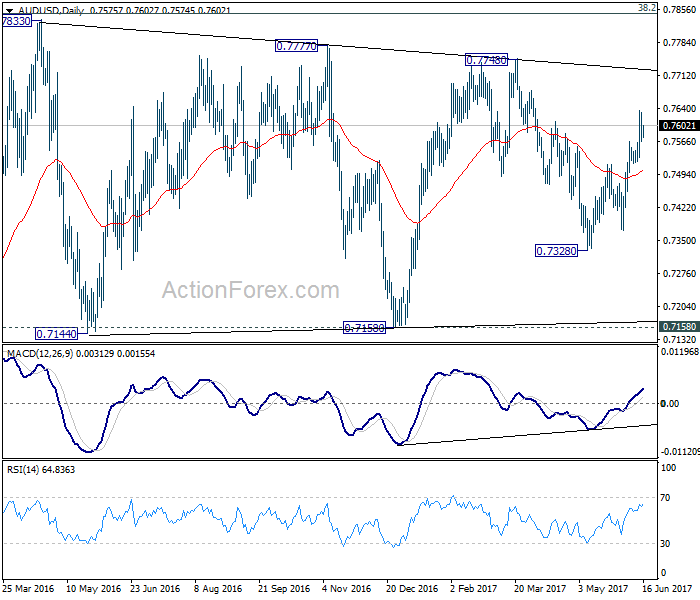

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7554; (P) 0.7592; (R1) 0.7617; More....

Further rise remains mildly in favor in AUD/USD for 0.7748 resistance and above. There is no clear sign of range breakout yet. So, we'll be cautious on topping again as it approaches medium term fibonacci level at 0.7849. Meanwhile, break of 0.7523 will argue that rebound from 0.7328 is possibly completed. In that case, intraday bias will be turned back to the downside for 0.7370 support.

In the bigger picture, we're still treating price actions from 0.6826 low as a corrective pattern. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8091) and above.

Bank Of Japan Maintains Massive Stimulus, Yen Declines

The Bank of Japan held steady on its accommodative stance as its two-day meeting came to an end. At a time when major central banks around the world have either started normalizing rates or signaled that they're on a path of doing so, the BoJ's current stance is expected to add downside pressure on the Japanese currency.

As anticipated, the BoJ maintained the 0.1% interest it charges banks for holding reserves with the central bank. Moreover, it made no changes to the yield target of around zero percent for 10-year Japanese government bonds and maintained its flexibility in engaging in bond purchases depending on the state of the economy.

Additionally, the Bank was more optimistic on private consumption supporting the economy as well as on growth from overseas economies, signaling its confidence on the existence of positive momentum for the nation which heavily relies on exports to fuel growth.

In terms of reaction in the forex markets, the yen is falling for a second straight day versus the dollar. The Japanese currency is looking set to record its biggest weekly loss in more than a month as analysts are discounting any expectations of monetary tightening coming soon from the Japanese central bank.

As European markets were getting ready to commence their trading day, BoJ Governor Haruhiko Kuroda started giving his press conference explaining the Bank's policy decisions. Among others, Kuroda said that “there's some distance to achieving (the Bank's) 2% inflation” target and that it will “take some time” for inflation to pick up, adding that at the moment it is inappropriate to discuss exiting the Bank's ultra-loose monetary policy. As Kuroda talked dolar/yen rose to the two-week high of 111.37. Before his comments the pair was trading at 111.06.

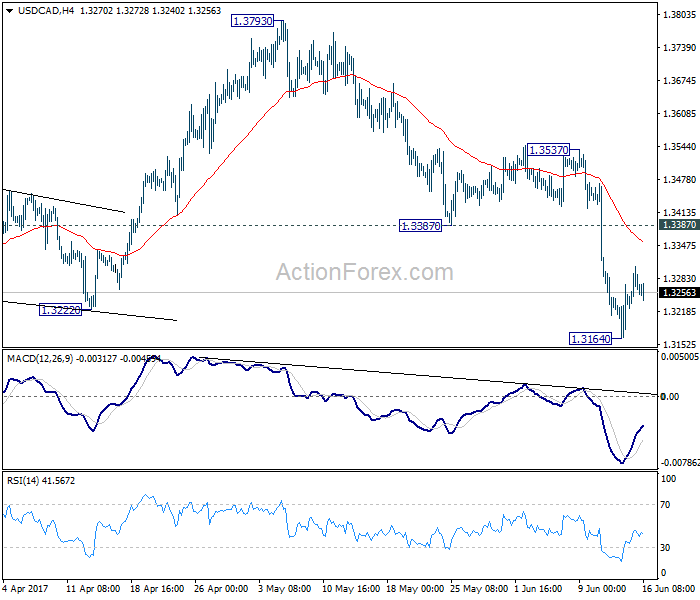

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3225; (P) 1.3267; (R1) 1.3309; More....

Intraday bias in USD/CAD remains neutral for consolidation above 1.3164 temporary low. Upside of recovery should be limited by 1.3387 support turned resistance and bring fall resumption. We hold on to the view that corrective rise from 1.2460 has completed at 1.3793 already and deeper decline is expected. Below 1.3164 will target 1.2968 support first. Break there should confirm our view and target 1.2460 and below.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. Rise from 1.2460 is seen as the second leg and has completed at 1.3793, ahead of 61.8% retracement of 1.4689 to 1.2460 at 1.3838. Break of 1.3222 should now indicate the start of the third leg while further break of 1.2968 should confirm. In that case, USD/CAD should decline through 1.2460 support to 50% retracement of 0.9406 to 1.4869 at 1.2048.