Sample Category Title

Dollar Recovers Ahead Of UK Elections And Comey Testimony

ECB meeting gets second billing as geopolitics to guide market

The USD is mixed against major pairs but has managed to regain some traction against the EUR, CHF, JPY and CAD as the statement from former FBI director James Comey gave the greenback some room ahead of the testimony before the Senate special committee. Comey's statement recounts what he recalls was said between him and President Trump in various occasions when the issues of Russia, Mike Flynn and loyalty. The markets await the questions and answers that will come during Comey's testimony for guidance on the potential impact on major currency pairs.

A conservative majority is the forecasted outcome of Thursday's elections in the United Kingdom. A large majority would boost the pound and validate the decision by Prime Minister Theresa May to call for the snap elections. A small victory would not be so positive for the pound with a hung parliament and a Labour parliament the scenarios that bring more uncertainty to the Brexit negotiations and have a deeper negative connotation for the GBP in the short term. Opinion polls do not have the greatest track record with UK elections having missed in 2015 with the elections, 2016 with Brexit and now facing another considerable test in 2017. The first exit poll is expected at 5:00 pm EDT.

The European Central Bank (ECB) will release its rate statement on Thursday, June 8 at 7:45 am EDT and a press conference to follow at 8:30 am EDT. There is no change in the benchmark rate or the quantitative easing program, but it is expected the central bank cuts its inflation forecast while delivering a dovish statement. The ECB needs to balance a stronger economy with lower inflation expectations and could launch a taper of stimulus while raising rates at the same time.

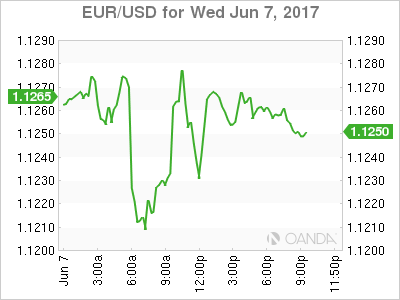

The EUR/USD lost 0.173 percent in the last 24 hours. The single pair is trading at 1.1254 after the statement from former FBI director prior to his testimony tomorrow let off some pressure form the USD. Bloomberg also reported on sources within the ECB saying that the central bank would be downgrading its inflation forecast while at the same time praising European growth in the first quarter. The USD appreciated while the euro fell ahead of the ECB rate statement due tomorrow.

European data has been mixed with service PMIs across the region coming close to estimates with France being the lone exception by missing the forecast. Retail sales underwhelmed and German factory orders fell by 2.1 percent as foreign investment demand is slowing down after a strong start to 2017.

Gold lost 0.52 percent on Wednesday. The yellow metal is trading at $1,287.50 ahead of major geopolitical events. Gold has risen after the Trump administration started losing political capital in 2017. The metal was lower in November as the President-elect made huge promises to reform the taxes and spend on modernizing infrastructure around the US. The pro-growth policies have not yet arrived as the administration was embroiled in healthcare reform and immigration policies that have resulted in major backlash and driven the price of safe havens higher.

Gold traders will be following the testimony before the Senate special committee as well as tuning in the UK elections in case of an upset to the polls forecasting a Conservative majority win.

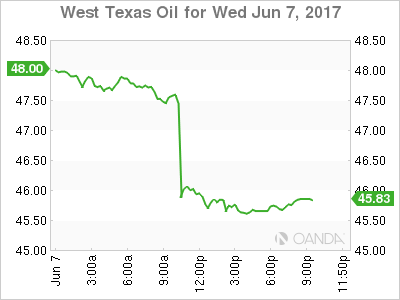

Oil lost 4.799 in the last 24 hours. The West Texas Intermediate is trading at $45.70 after the surprise buildup of US crude inventories this morning. Oil inventories rose 3.3 millions barrels when the forecast called for a drop of 3.5 million barrels. Gasoline inventories also gained as part of a worrisome trend that has seen demand stagnate ahead of the US driving season and putting more pressure on oil prices.

Increasing production from US shale producers has all but offset the best efforts from the Organization of the Petroleum Exporting Countries (OPEC) and other major producers that banded together to extend the production cut agreement until March 2018. The diplomatic situation with Qatar has also raised concerns on how solid is the group as internal rifts are reemerging.

Market events to watch this week:

Thursday, Jun 8

All Day GBP Parliamentary Elections

7:45am EUR Minimum Bid Rate

8:30am EUR ECB Press Conference

8:30am USD Unemployment Claims

Tentative USD Former FBI Director Testimony

Friday, Jun 9

4:30am GBP Manufacturing Production m/m

8:30am CAD Employment Change

8:30am CAD Unemployment Rate

Stepping Up Pattern In EUR/AUD

After the previous EUR/AUD resistance zone was broken and the trade no longer valid, I wanted to take a step back and just highlight the way that price has been acting.

On an obvious bullish tear, we’ve seen the following textbook perfect pattern:

“Break higher > Pullback > Retest previous resistance as support > Repeat”

Just look at the EUR/AUD daily chart and things are pretty self explanatory:

EUR/AUD Daily:

With the most recent pullback highlighted by Aussie dollar strength, the way that the daily candle wasn’t able to close below support shows just how bullish this pair is and keeps the pattern in tact.

Strap In For Super Thursday

Thursday promises to be a rocking day in the foreign exchange market with a trio of major events. We get set. The Australian dollar was the top performer Wednesday while the Canadian dollar lagged. Australian trade balance is due up before the major news begins to hit. A new Premium trade is due tomorrow in addition to the existing 6 trades.

Markets were choppy Wednesday as ECB leaks about softer inflation forecasts and higher growth hit. That was mixed in with the final UK election polls and an early preview of Comey's testimony.

All will be revealed in the day ahead, starting with the ECB. The first sources story said inflation forecast would be cut to 1.5% for this year from 1.7%, largely on energy. It added that 2018 will be cut one tick to 1.5% and 2019 to 1.5% from 1.7%. That was followed by a separate report that said inflation forecast would edge lower and growth would be boosted. The euro fell 70 pips and then recovered on the pair of leaks.

Later, the opening statement from former FBI director Comey was released. In it, he detailed improper requests and hints from the President but it has no bombshells or revelations that hadn't already been reported. In the aftermath, USD/JPY recovered to 109.80 from 109.35.

The final event Thursday will be the UK election. The wide spreads in the polls continued with the showing the Conservatives anywhere from 12 to 1 point ahead of Labour. The final numbers tended to show continued momentum from Labour but not enough to stop May from winning a majority.

Cable touched a two-week high but it was a choppy trade. In anything, watch for last-minute bets in the market on May.

Switching gears to the Asia-Pacific region, yesterday's Australian GDP was in-line with the +0.3% q/q reading expected and the RBA brushed off the soft quarter but the focus now turns to Q2. A big input is trade and April trade balance is due at 0130 GMT. The consensus is for a A$2.0B surplus.

AUD has been perky this week and seasonally it's in a strong June-July period and coming off a recent ebb. A positive surprise would help extend the four-day winning streak. But much bigger moves are coming elsewhere with the ECB, Comey and the UK election results all due later Thursday.

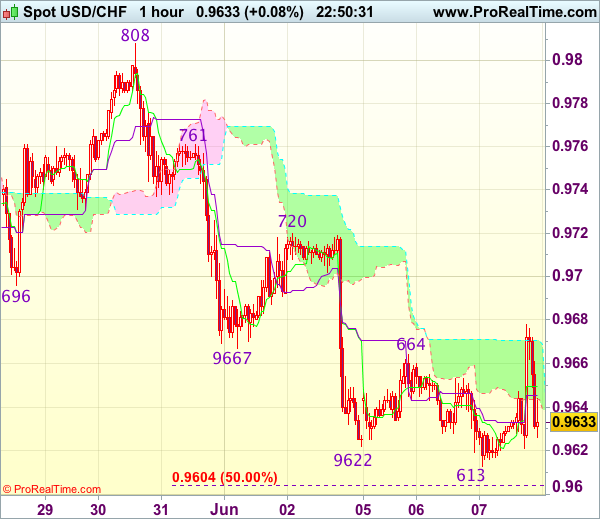

Trade Idea Wrap-up: USD/CHF – Sell at 0.9720

USD/CHF - 0.9644

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9650

Kijun-Sen level : 0.9646

Ichimoku cloud top : 0.9671

Ichimoku cloud bottom : 0.9643

Original strategy :

Sell at 0.9720, Target: 0.9620, Stop: 0.9755

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9720, Target: 0.9620, Stop: 0.9755

Position : -

Target : -

Stop : -

As the greenback has rebounded after marginal fall to 0.9613, suggesting consolidation above this level would be seen and corrective bounce to 0.9680-85 is likely, however, reckon upside would be limited to resistance at 0.9720 and bring another decline later to 0.9600-05 (50% projection of 1.0100-0.9692 measuring from 0.9808) but oversold condition should limit downside to 0.9570 and price should stay above support at 0.9550, risk from there has increased for a rebound to take place later.

In view of this, we are looking to sell dollar on recovery as resistance at 0.9720 should limit upside. Above 0.9740 would abort and signal a temporary low is formed instead, bring a stronger rebound to 0.9761 resistance but price should falter below resistance at 0.9808.

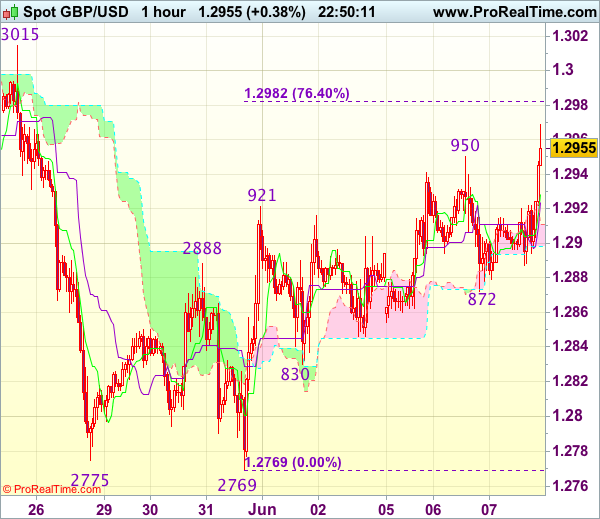

Trade Idea Wrap-up: GBP/USD – Stand aside

GBP/USD - 1.2961

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2928

Kijun-Sen level : 1.2924

Ichimoku cloud top : 1.2911

Ichimoku cloud bottom : 1.2898

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although sterling has risen again after brief pullback and near term upside risk remains for the erratic rise from 1.2769 to extend gain to 1.2980-85, however, as broad outlook remains consolidative, reckon upside would be limited to 1.3000 and indicated previous resistance at 1.3015 should remain intact. Only a break of 1.3015 would signal early upmove has resumed and bring retest of 1.3048.

In view of this, would not chase this move here and would be prudent to stand aside for now. Below the Kijun-Sen (now at 1.2924) would bring test of 1.2885-90 but only break of support at 1.2871 would signal top is formed, bring weakness towards key support at 1.2830.

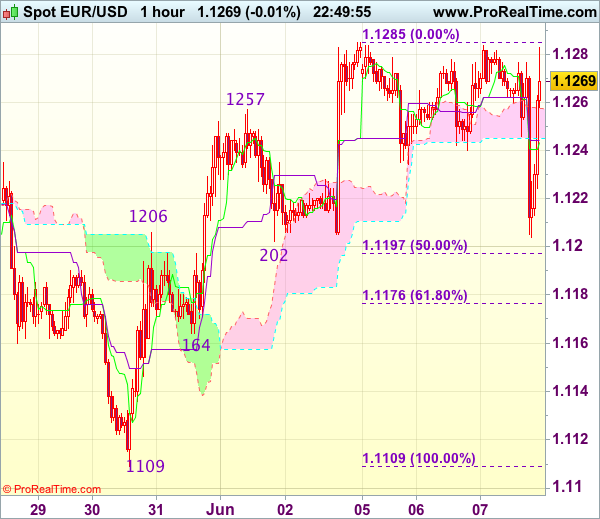

Trade Idea Wrap-up: EUR/USD – Buy at 1.1240

EUR/USD - 1.1264

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 1.1244

Kijun-Sen level : 1.1244

Ichimoku cloud top : 1.1258

Ichimoku cloud bottom : 1.1245

New strategy :

Buy at 1.1240, Target: 1.1340, Stop: 1.1205

Position : -

Target : -

Stop : -

As the single currency found renewed buying interest just above previous support at 1.1202 and has staged another strong rebound, reviving our bullishness and above resistance at 1.1285 would confirm recent upmove has resumed and extend further gain to previous chart resistance at 1.1300, break there would encourage for headway to 1.1340-45 but overbought condition should limit upside to chart point at 1.1366.

In view of this, we are looking to buy euro again on dips as 1.1240-45 should limit downside. Only below support at 1.1202 would abort and suggest top is possibly formed, break of 1.1195-97 (50% Fibonacci retracement of 1.1109-1.1285) would add credence to this view, bring retracement of recent rise to indicated support at 1.1164 first.

Dollar Flat ahead of Triple Threat Thursday; Inflation Concerns Hurt the Euro

Today's European session was light in terms of economic data with notable market reaction only being evidenced after the release of UK house price data. Market participants are now turning their attention to tomorrow's main risk events, which have the capacity to generate significant volatility in the markets.

Tomorrow has been dubbed as "Triple Threat Thursday" as three major risk events will dominate investors' attention. Namely, Brits will be called in to vote in a national election, the European Central Bank will announce its rate decision offering guidance about the eurozone economic outlook going forward and former FBI director James Comey will give a testimony to the U.S. Senate regarding his discussions with President Trump on dropping the investigation into the ex-National Security Advisor Michael Flynn's alleged connections with Russia.

The dollar index, gauging the greenback against the currencies of six major US trading partners, was virtually unchanged from where it opened the day in late European trading hours after previously falling close to yesterday's near seven-month low of 96.52. Dollar / yen was marginally down on the day trading at 109.33. Earlier in the day, the pair fell to the near seven-week low of 109.11 as the yen was helped by the risk-averse mood in the markets and falling US Treasury yields failing to attract investments in the US currency. Any setback to the Trump administration's tax and other fiscal policy plans from Comey's comments tomorrow have the capacity to hurt the dollar.

Out of Germany, industrial orders for the month of April fell far more than anticipated indicating that the industrial sector did not have a robust start in the second quarter of the year. Specifically, orders declined by 2.1% month-on-month with analysts expecting a 0.4% fall. March's number was slightly revised upwards to 1.1% (from 1.0% before). Some analysts attributed the poor numbers to the Easter holidays falling in April this year and expect a recovery in the coming months. Euro / dollar didn't react much to the data.

The euro was hovering around the near seven-month high of 1.1284 hit late last week in the first hours of European trading until a report by Bloomberg suggested that the European Central Bank will cut its inflation forecast in its policy meeting tomorrow. As a result, euro / dollar fell to the six-day low of 1.1203. The single currency has since recovered part of those losses but was still down on the day in late European trading hours.

In terms of UK data, the Halifax house price index showed average UK house prices in the three months to May were, on an annual basis, 3.3% higher relative to the previous year. This marks the slowest growth in four years. Still, the rise in prices was better than the forecasted 3.0%. On a month-on-month basis, prices increased by 0.4% in May, better than the -0.1% expected and the zero growth in prices during April – the result of an upward revision from -0.1%. The housing market has entered a slowdown phase since last June's Brexit vote as consumers are holding spending, among others, due to higher inflation as a result of a weakening pound. Pound / dollar fell after the release of the data eventually reaching its daily low of 1.2887. The pair rebounded later in the day hitting a two-week high of 1.2971 along the way.

The Australian dollar built on momentum from earlier in the day after GDP data showed the nation extended its record expansion. Aussie / dollar extended gains to rise to the seven-week high of 0.7566 during European trading hours.

Finishing with a quick look at oil, the Energy Information Administration's (EIA) weekly report showed a buildup in US crude oil inventories amounting to 3.30 million barrels, vastly diverging from expectations of a drop by 3.46m barrels. WTI crude recorded a steep fall after the release of the data, eventually falling to the near one-month low of $45.92 per barrel. Brent crude was also last down on the day, touching a near one-month low of $48.14 a barrel.

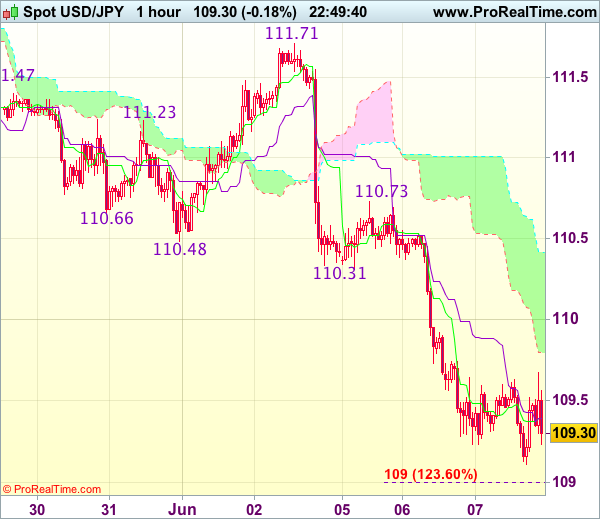

Trade Idea Wrap-up: USD/JPY – Sell at 110.20

USD/JPY - 109.35

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 109.39

Kijun-Sen level : 109.39

Ichimoku cloud top : 110.42

Ichimoku cloud bottom : 109.79

Original strategy :

Sell at 110.20, Target: 109.20, Stop: 110.55

Position : -

Target : -

Stop : -

New strategy :

Sell at 110.20, Target: 109.20, Stop: 110.55

Position : -

Target : -

Stop : -

As the greenback has fallen again after brief recovery, suggesting recent decline from 114.37 is still in progress and bearishness remains for further weakness to 109.00-05 (1.236 times projection of 111.71-110.31 measuring from 110.73), then towards 108.70-75 but near term oversold condition should limit downside to 108.45-50 (1.618 times projection), bring rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as previous support at 110.24 (now resistance) should limit upside and bring another decline. Above previous support at 110.31 would defer and suggest low is formed instead, bring a stronger rebound to 110.60 but break of resistance at 110.73 is needed to add credence to this view.

Flying Yen Hits 7-Week Highs on Worries Over ECB, British Election

The Japanese yen has paused in the Wednesday session, after posting strong gains on Tuesday. In North American trade, the pair is trading at 109.32. On the release front, US Crude Oil Inventories posted a surplus of 3.3 million, surprising the markets, which had forecast a drawdown of 3.1 million. Japan releases Final GDP later in the day, with the markets expecting a strong gain of 0.6 percent. As well, Japan's current account deficit is expected to narrow to JPY 1.62 trillion. On Thursday, the US releases unemployment claims, with the estimate standing at 241 thousand.

As a save-haven currency, the yen tends to gain ground in periods of uncertainty, and unpredictability in Europe this week has boosted the Japanese currency. The ECB meets on Thursday to set interest rates, and reports that the central bank could lower its inflation forecast has unnerved investors and sent the euro lower. The UK is holding elections on Thursday, and what looked like a cakewalk for Theresa May just a few weeks ago has turned into a tight election, as recent terror attacks in Manchester and London have turned the political landscape upside down. Although May's Conservatives are clinging to a lead, a hung parliament, in which no party garners a majority, could throw the country into more political uncertainty. The yen has climbed 1.2% in June, as USD/JPY is at its lowest levels since April 21.

Japan's economy continues to improve, and stronger numbers have buoyed the yen. Wage growth posted a solid gain of 0.5% in April, rebounding from a 0.3% decline in the previous release. The dollar has dropped below the 110 level for the first time since April 25. Stronger global demand has boosted the economy, notably the export and manufacturing sectors. The markets are predicting that Final GDP will be revised upwards to 0.6%, better than the 0.5% gain in Preliminary GDP. If Final GDP matches or beat its estimate, the yen rally could continue.

The Federal Reserve is widely expected to announce a rate hike next week, which would mark the second quarter-point increase in 2017. Even a shockingly soft Nonfarm Payrolls report last week hasn't put much of a dent in these expectations, with a rate hike currently priced in at 91 percent. Another rate hike by the Fed would mark a vote of confidence in the US economy, but Fed policymakers continue to have some concerns. Inflation remains stubbornly low, despite a labor market that remains close to capacity. Fed policy makers are also scratching their heads over soft consumer spending, which has not kept pace with high levels of consumer confidence. As for additional rate hikes in the second half of 2017, the markets remain skeptical, with the odds of a September rate hike at just 22%. However, stronger economic numbers in the third quarter could easily increase the likelihood a September hike.

USDJPY May See Some Support And A Reversal Higher

USDJPY is trading in final stages of a bigger three wave pullback, specifically in wave c. We see a nice impulse unfolding within wave c, that could now be in minor wave iv). This means only wave v) is missing, before a new reversal can take place.

USDJPY, 1H