Sample Category Title

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7417; (P) 0.7443; (R1) 0.7480; More...

AUD/USD's corrective recovery is still in progress and could extend higher. But upside is expected to be limited below 0.7555 resistance to bring fall resumption. Below 0.7388 minor support will turn bias to the downside. Break of 0.7328 will extend the decline from 0.7748 to 0.7144/7158 support zone. However, firm break of 0.7555 will argue that fall from 0.7748 is completed and turn bias back to the upside.

In the bigger picture, we're still treating price actions from 0.6826 low as a corrective pattern. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8115) and above.

Dollar Recovers With Weak Momentum in Quiet Session

Dollar recovers broadly in a quiet Asian session today but momentum is very week so far. The economic calendar is rather light today and trading might remain subdued. Nonetheless, volatility could build up again as the week goes with some key events scheduled. The list includes US budget proposal, FOMC minutes, BoC rate decision, Eurozone sentiment data, OPEC meeting, etc. While for now, some consolidations could be seen, the greenback will more likely extend recent fall ahead, than not. In other markets, Gold retreats mildly but is staying solid above 1250 handle. WTI crude oil extends recent rise and is on course for 53.76/55.24 resistance zone.

Trump to deliver first budget proposal on Tuesday

US President Donald Trump will deliver his first major budget proposal on Tuesday. It's reported there is a proposal for balancing the federal budget within 10 year through steep cuts to safety net and discretionary spending. One of the key point to note is possibly the massive USD 800b cut over 10 years on Medicaid. The Congressional Budget Office has estimated that this could impact healthcare benefits of 10 million low-income Americans over the decade. And, the inclusion of Medicaid cut is seen as significant by some analysts because there are clear rejections on it from a number of Senate Republicans. While the House has voted to cut Medicaid funding, Senate Republicans have already indicated that they would start from scratch. Such inclusion could further enlarge the division between Trump and some Republicans at the time of political turmoil in Washington.

CEBR: Brexit could cost GBP 36b annually

In UK, an analysis conducted by the Centre of Economic Business Research (CEBR) for the Open Britain organization noted that the lost of EU single market in services after Brexit could cost UK companies up to GBP 36b annually. The reported pointed out that "about a third of the losses from single market withdrawal result from lost businesses in financial services." The impact could be particularly negative on financial services, telecommunications and transport. It elaborated that "the free movement of services can also be seen to directly touch on immigration if people are coming to the UK to offer their services as self-employed individuals or if firms exercise their mobility rights while wanting to carry their workforce over." And, the overall impact on UK's GDP would be between 1.4% and 2.0%, equivalent to GBP 25b to GBP 36b a year.

OPEC to agree on production cut extension

Oil prices continue to surge ahead of an OPEC meeting this Thursday. Saudi Arabia's energy minister Khalid al-Falih said "everybody I talked to... expressed support and enthusiasm to join in this direction" of extending the product cut agreement by a further nine months til next March. And, he's optimistic that continuation with the same level of cuts, plus eventually adding one or two small producers, if they wish to join, will be more than adequate to bring the five-year balance to where they need to be by the end of the first quarter 2018." WTI crude oil is trading at 50.8 at the time writing, up 0.9% comparing to last week's close. Recent rebound in WTI is expected to extend further to 53.76/55.24 resistance zone in near term.

In this week's calendar...

Released today, UK Rightmove house price rose 1.2% mom in May. Looking ahead, FOMC minutes and BoC rate decisions will be the main focuses this week. Markets will look into FOMC minutes on hints to solidify the expectations of a June hike. BoC will very likely keep monetary policies unchanged. In additional to that, Euro will look into Eurozone PMIs and Germany Ifo for further affirmation of improvements in economy. UK inflation report hearing will also be watched. Here are some highlights for the week ahead"

- Tuesday: Japan all industries index; Swiss trade balance; Eurozone PMIs; German Ifo; UK inflation report hearings, public sector net borrowing; Canada wholesale sales; US PMIs, new home sales

- Wednesday; New Zealand trade balance; German Gfk consumer sentiment; BoC rate decision, FOMC minutes, US existing home sales

- Thursday: UK GDP revision, BBA mortgage approvals; US jobless claims, trade balance, wholesale inventories

- Friday: Japan CPI; US durable goods orders, GDP revision, U of Michigan sentiment

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7417; (P) 0.7443; (R1) 0.7480; More...

AUD/USD's corrective recovery is still in progress and could extend higher. But upside is expected to be limited below 0.7555 resistance to bring fall resumption. Below 0.7388 minor support will turn bias to the downside. Break of 0.7328 will extend the decline from 0.7748 to 0.7144/7158 support zone. However, firm break of 0.7555 will argue that fall from 0.7748 is completed and turn bias back to the upside.

In the bigger picture, we're still treating price actions from 0.6826 low as a corrective pattern. And, as long as 38.2% retracement of 0.9504 to 0.6826 at 0.7849 holds, long term down trend from 1.1079 is expected to resume sooner or later. Break of 0.6826 low will target 0.6008 key support level. However, firm break of 0.7849 will indicate that rise from 0.6826 is developing into a medium term rebound, rather than a sideway pattern. In such case, stronger rise should be seen to 55 month EMA (now at 0.8115) and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | Rightmove House Prices M/M May | 1.20% | 1.10% | ||

| 23:50 | JPY | Trade Balance (JPY) Apr | 0.10T | 0.25T | 0.17T | 0.11T |

| 13:00 | CNY | Conference Board Leading Index Apr | 0.90% | |||

| 14:00 | USD | Fed's Harker Speaks in New York | ||||

| 14:30 | USD | Fed's Kashkari Speaks |

US Dollar Remains Under Pressure

Market movers today

It is a very quiet start to the week with no important data today. Two Fed speakers are due to speak. Harker (voter, hawkish) and Kashkari (voter, dovish) may give more insight into the scope for a rate rise in June.

In the rest of the week, German ifo (Tuesday), Euro Flash PMI (Wednesday) and the OPEC meeting (Thursday) will be in focus.

In the Scandi count ries, employment data and retail sales figures in Denmark are due out .

Selected market news

Asian stocks are edging higher this morning, following caut ious gains on Wall Street on Friday, though the US dollar remains under pressure as Washington's political turmoil undermines confidence in the out look for Trump's economic policy. Market focus this week is likely to remain cent red on what is happening around Trump. In his inaugural t rip overseas, US President Donald Trump called on Arab leaders to do their fair share to drive out terrorism from their count ries in a speech in Saudi Arabia on Sunday. More ‘headlines' will hit the market as the trip progresses, with the NATO meeting and the G7 summit at the weekend being the most important events.

Meanwhile, North Korea fired another ballistic missile into waters off its east coast yesterday, its second missile test in a week. This also complicates plans by South Korea's new President Moon Jae-in to seek ways to reduce the conflict with his neighbour. Tensions are rising fast between the US and North Korea and a furtherescalation of the conflict is likely if North Korea cont inues with plans to carry out another nuclear test (see also Research: The rising risk from North Korea - and what it means for markets, 27 April 2017).

With political risks in Europe somewhat abat ing, after Emmanuel Macron's win in the French presidential election, focus today shifts back to Greece's debt problems, as eurozone finance ministers meet in Brussels to discuss the issue of debt relief. The Greek parliament narrowly approved another reform package last week, containing spending cuts and reduct ions in pensions and tax allowances, t riggering renewed st reet protests. The open issue, however, remains a possible debt relief for the country, which the IMF demands as a prerequisite to participate in further funding, but EU leaders, especially Germany, are still opposing. A deal is needed for Greece to draw its next instalment of bailout aid and make a EUR7.5bn debt repayment in July; however, it is quest ionable whether an agreement between the part ies can be reached today. Should a deal on debt relief be found, Greece might issue its first sovereign bond in three years as early as July, to test market appet ite before its bailout programme expires in mid-2018, according to Greek officials.

OPEC and other oil producers seemed on course to an agreement to extend supply cuts at the meeting on Thursday, with Saudi Arabia saying most part icipants are on board with the plan to rein in a global supply glut . An extension of the supply cuts seems also largely priced into the oil market now, with Brent crude trading at USD54.1bl this morning.

Aussie Dollar Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the AUD rose 0.57% against the USD and closed at 0.7455 on Friday.

LME Copper prices rose 1.93% or $106.0/MT to $5596.0/MT. Aluminium prices rose 1.73% or $33.0/MT to $1938.0/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7443, with the AUD trading 0.16% lower against the USD from Friday’s close.

The pair is expected to find support at 0.7413, and a fall through could take it to the next support level of 0.7383. The pair is expected to find its first resistance at 0.7471, and a rise through could take it to the next resistance level of 0.7499.

Moving ahead, consumer confidence index for the week ended 21 May, due for release at night, will be assessed by market particpants.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Consumer Confidence Reached Its Highest Level Since July 2007 In May

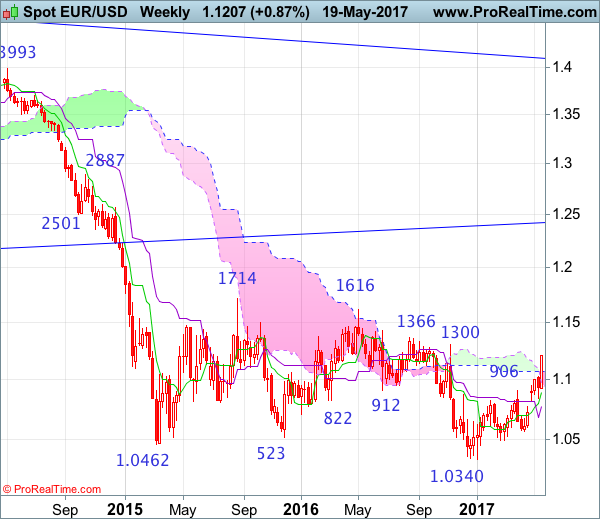

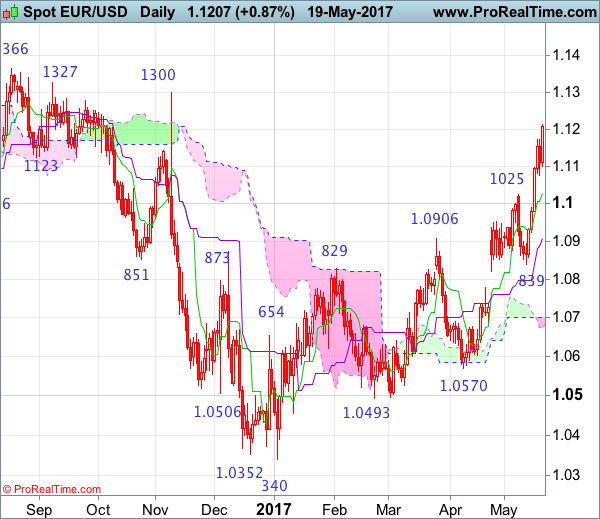

For the 24 hours to 23:00 GMT, the EUR rose 0.86% against the USD and closed at 1.1202 on Friday.

On the macro front, the Euro-zone's consumer confidence index rose less than expected to a level of -3.3 in May, reaching its best level in a decade as the region shrugged off populist political risks in 2017. Markets expected for an advance to a level of -3.0, after recording a level of -3.6 in the prior month.

Additionally, the Eurozone's seasonally adjusted current account surplus eased to €34.1 billion in March from a revised figure of €37.8 billion recorded in the last month.

Elsewhere, Germany's producer prices climbed 3.4% YoY in April to their highest level in nearly six years, surpassing market expectations for a gain of 3.2% and following a rise of 3.1% in the previous month.

The greenback fell against its major peers on Friday, as political uncertainty continued to weigh on the currency and depressed investor sentiment.

In the US, St. Louis Federal Reserve (Fed) President James Bullard stated that central bank's proposed interest rate hikes might be too aggressive, citing that the nation's economy had slowed since March and inflation had also dipped, thus making the case for a continued go-slow approach.

In the Asian session, at GMT0300, the pair is trading at 1.1190, with the EUR trading 0.11% lower against the USD from Friday's close.

The pair is expected to find support at 1.1122, and a fall through could take it to the next support level of 1.1053. The pair is expected to find its first resistance at 1.1235, and a rise through could take it to the next resistance level of 1.1279.

With no economic data in the Euro-zone today, traders will look forward to the US Chicago Fed National Activity index for April, scheduled later in the day, for further direction in the currency pair.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

UK CBI Industrial Trends Total Orders Unexpectedly Rose In May

For the 24 hours to 23:00 GMT, the GBP rose 0.7% against the USD and closed at 1.3033 on Friday.

Data revealed that the CBI industrial trends total orders surprisingly advanced to 9.0 in May, mainly driven by faster growth in export orders, against market consensus to remain unchanged at 4.0 as reported in the previous month.

Over the weekend, Rightmove house prices rose 1.2% on a monthly basis in May in the UK, from 1.1% gain recorded in the last month.

In the Asian session, at GMT0300, the pair is trading at 1.2995, with the GBP trading 0.29% lower against the USD from Friday’s close.

The pair is expected to find support at 1.2943, and a fall through could take it to the next support level of 1.2891. The pair is expected to find its first resistance at 1.3043, and a rise through could take it to the next resistance level of 1.3091.

In absence of any major economic releases in the UK today, market participants will look forward to global macroeconomic events for direction.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading Lower In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.3% against the JPY and closed at 111.15 on Friday.

Over the weekend, macro data indicated that Japan's Merchandise total trade balance narrowed more than expected to ¥481.7 billion in April, from ¥614.7 billion reported in the previous month. Markets expected the figures to decrease to ¥520.7 billion. Moreover, the nation's exports jumped 7.5% YoY in

April, less than analysts' expectations of 8.0% gain, helped by strong demand in Asia for semiconductors, semiconductor-making equipment and steel. Exports had risen 12.0% in the prior month. On the other hand, imports rose 15.1%, more than expectations of 14.8% rise, after recording a 15.8% growth in the previous month.

In the Asian session, at GMT0300, the pair is trading at 111.45, with the USD trading 0.27% higher against the JPY from Friday's close.

The pair is expected to find support at 111.08, and a fall through could take it to the next support level of 110.72. The pair is expected to find its first resistance at 111.75, and a rise through could take it to the next resistance level of 112.06.

Going forward, traders will keep a close eye on preliminary reading of Japan's Nikkei manufacturing PMI data for May, slated to release overnight, to gauge strength in the nation's manufacturing sector.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Swiss Franc Trading Lower This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.66% against the CHF and closed at 0.9730 on Friday.

In the Asian session, at GMT0300, the pair is trading at 0.9736, with the USD trading 0.06% higher against the CHF from Friday’s close.

The pair is expected to find support at 0.9704, and a fall through could take it to the next support level of 0.9671. The pair is expected to find its first resistance at 0.9787, and a rise through could take it to the next resistance level of 0.9837.

With no major economic data in Switzerland today, market participants will look forward to Swiss trade balance figures for April, scheduled to release tomorrow.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Canada’s Annual Inflation Remained Steady In April

For the 24 hours to 23:00 GMT, the USD declined 0.7% against the CAD and closed at 1.3515 on Friday.

Macroeconomic data showed that Canada's consumer price inflation rose less than expected 1.6% YoY in April, matching the gain in March, as higher energy costs offset a seventh consecutive decline in grocery prices. Markets were expecting consumer prices to rise 1.7%. Moreover, the nation's retail sales advanced 0.7% on a monthly basis in March, exceeding market projections of 0.4% gain, buoyed by increased purchases at new and used cars dealers. Retail sales recorded a revised drop of 0.4% in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.3526, with the USD trading 0.08% higher against the CAD from Friday's close.

The pair is expected to find support at 1.3486, and a fall through could take it to the next support level of 1.3446. The pair is expected to find its first resistance at 1.3585, and a rise through could take it to the next resistance level of 1.3644.

On the occasion of Victoria Day in Canada today, trading trends in the currency pair will be determined by global macroeconomic factors.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

EUR/USD Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting star

• Time of formation: 03 May 2016

• Trend bias: Down

Daily

• Last Candlesticks pattern: Shooting star

• Time of formation: 3 May 2016

• Trend bias: Sideways

EUR/USD – 1.0946

The single currency only retreated to as low as 1.0839 last week before rising again (we recommended to buy euro at 1.0800 last week and missed the entry), the subsequent rally above 1.1025 resistance adds credence to our bullish view that the erratic upmove from 1.0340 low is still in progress, hence further gain to previous resistance at 1.1300 would be seen, however, near term overbought condition should limit upside to 1.1327 and previous chart resistance at 1.1366 should hold from here, risk from there is seen for a retreat later.

On the downside, whilst initial pullback to 1.1150 cannot be ruled out, reckon downside would be limited to support at 1.1076 would risk test of previous resistance at 1.1025 (now support as well as current level of the Tenkan-Sen) but only a daily close below there would suggest top is possibly formed instead, risk weakness to 1.0950-60 but the Kijun-Sen (now at 1.0907) would limit downside and price should stay well above said support at 1.0839.

Recommendation: Buy at 1.1120 for 1.1320 with stop below 1.1020.

On the weekly chart, last week’s rally formed a long white candlestick, adding credence to our view that the erratic rise from 1.0340 low is still in progress and test of previous resistance at 1.1300 is likely, however, a break of previous resistance at 1.1366 is needed to retain bullishness and signal early downtrend has ended at 1.0340, bring further rise to 1.1428 but reckon 1.1500 would hold and price should falter well below another previous chart resistance at 1.1616.

On the downside, expect pullback to be limited to 1.1120-30 and bring another rise later to aforesaid upside targets. Below the upper Kumo (now at 1.1070) would defer and risk weakness to 1.1025 (previous resistance now support) but break there is needed to signal top is formed instead, bring further fall to 1.0965-70 but support at 1.0922 (last week’s low) should remain intact, price should stay well above last week’s low at 1.0839, bring another rise later.