Sample Category Title

The Weekly Bottom Line

HIGHLIGHTS OF THE WEEK

United States

- Investors perceived this week's political developments in the U.S. as likely to delay the implementation of pro-growth policies. As a result, they risk assets sold off midweek in favor of gold and treasuries. Risk appetite appeared to make a comeback toward the end of the week along with some reversal in earlier trends, particularly among American equities.

- Underneath the political noise, the economy continued to emit mostly positive signals which included a rise in industrial production and capacity utilization, and falling jobless claims. Homebuilding appeared to be a soft spot at first glance, but the details reveal a better story.

- The Fed will keep an eye out for financial market stress, but is likely to continue focusing on signals from the economy. So far, the outlook for the second quarter remains solid, with growth currently tracking north of 3% annualized. As such, odds are still in favor of a June hike.

Canada

- The economic data out this week lifted our tracking for first quarter real GDP growth to 4% annualized. Real retail spending was up 1.2% in March, driven by spending on autos, while manufacturing shipments rose 0.2%. Both indicators were up 1.9% for the first quarter.

- While the Canadian economy is on track for its best three-quarter streak in almost three years, soft inflation and uncertainty over the near-term housing outlook are likely to keep the Bank of Canada on hold until early to mid next year.

UNITED STATES - CUTTING THROUGH POLITICAL NOISE

To say that political events dominated headlines this week may be somewhat of an understatement. The U.S. administration found itself in hot water once again over allegations of misconduct. Mounting political pressure reached a boiling point with the appointment of a special prosecutor to probe Trump-Russia ties. Financial markets perceived these developments as likely to delay the implementation of pro-growth policies such as tax reform and infrastructure spending, and quickly sold off risk assets. By midweek global stock markets followed the rapid decline in American indices (Chart 1). The trade-weighted U.S. dollar gave up all of its gains recorded since the U.S. election. In commodities, oil retained its upward trend and is poised to end the week above $50/bbl, buoyed by news that Russia and Saudi Arabia may extend their production cuts along with a report from EIA showing falling U.S. inventory levels.

Political turmoil was not limited to the U.S.. The president of Brazil was accused of bribery, sending both the national stock market and currency plunging 9% and 7% respectively the day after news broke. Under such global disorder investors poured their money in safe heaven assets, with gold gaining around $25/oz on the week and sending U.S. Treasury yields lower. However, risk appetite returned by the end of the week with some reversal in earlier trends, particularly among American equities. The heightened volatility was reflected in the VIX index, which spiked to a month high at midweek but subsided quickly thereafter.

Underneath the political noise, the economy continued to emit mostly positive signals. Industrial production rose 1.0% in April - the biggest monthly gain in more than three years. Capacity utilization also rose to 76.7% - the best level since late 2015, boding well for future business investment. Weekly jobless claims fell unexpectedly, with levels now resting near decade-lows seen as further signs of a tightening labor market. Lastly, homebuilding appeared to be a soft spot at first glance, but the details revealed a better story. The headline was pulled down by the volatile multifamily segment, while the single family segment retained its upward trend (Chart 2). The latter is a much larger and better indicator of economic conditions, and its advance is reflective of continued progress in the labor market. We expect this trend to continue as rising wages support household formation and demand for new homes.

Looking at the big picture there are two main points worth highlighting. First, investors will continue to pay close attention to political events because the implementation of pro-growth policies remains the cornerstone needed to validate today's rich stock valuations. Intuitively, this suggests potential for further volatility in the weeks and months ahead. Second, the Fed too will keep an eye on such developments, not because it has placed much emphasis on the pro-growth policies to begin with, but rather because a market downturn could weigh on the real economy. Unless it sees concrete signs of this occurring, it is likely to continue focusing on underlying signals from the economy, particularly those related to inflation where recent readings have disappointed. So far, the outlook for the second quarter remains solid, with growth currently tracking north of 3% annualized. As a result, market participants will continue to price in a June Fed hike, with odds from CME Group currently pegged at 74%.

CANADA - A WINNING STREAK

Financial markets in Canada this week took their cue from rising political uncertainty in the United States. Interest rates, the loonie and the TSX all dipped. In contrast, the economic news was overwhelmingly positive. While still awaiting the final tally, we now have data on the vast majority of Canadian economic indicators for the first quarter of the year. Taking this into account, TD Economics estimates that Canadian real GDP grew by a stunning 4% annualized rate over the first three months of the year, following a solid end to 2016 and marking the best three quarter streak since 2013. While the Bank of Canada will remain on hold a little bit longer, the case for a rate hike as early as spring of next year is certainly mounting.

The Bank of Canada does not target economic growth directly, but rather inflation, which exhibits a lagged response to growth. This week's consumer price report should give pause to anyone expecting an immediate central bank response. All measures of inflation watched most closely by the Bank of Canada are well below its 2% target and have been trending lower since January of this year, suggesting that the economy may have more slack than estimated. Still, with real GDP growth to hold at a healthy 2% to 2.5% pace following Q1's tunrout, slack is being absorbed quickly. As a result, inflation is likely to move higher, reaching the bank's target of 2% by late next year.

Moreover, while this week's manufacturing report showed that the export-heavy sector is picking up momentum, economic growth is still largely being driven by domestic, interest-rate-sensitive sectors. The retail spending report this week pointed to a 2% gain in real spending in Q1, mostly due to sharp gains in auto sales. Meanwhile, record housing activity during the quarter supported construction activity and services related to home buying. Both personal consumption expenditure and residential investment are expected to account for all of the economic growth in the first quarter.

Beyond an anticipated temporary break in activity, the Canadian housing market is likely to remain a key driver of economic growth throughout our forecast horizon. In the near-term, TD economics believes that housing market activity is likely to back off due to a lagged response to changes to mortgage regulation implemented in October of last year, along with the introduction of a nonresident buyer's tax and the expansion of rent control in Ontario. Indeed, market activity in Ontario reversed quickly in April, with a sharp 7% reduction in sales and a record spike in listings across the Greater Toronto Area. Following BC's lead, we do think that markets in Ontario will take a pause over the next few months. However, markets in BC have also shown that the impact of such measures can be temporary and have very little impact on price growth. Housing activity is starting to bounce back in the province and home price growth is still holding at a hefty double-digit pace.

The bottom line is that while the economy is picking up steam, the combination of low inflation and more restrictive housing policy measures will bide the Bank of Canada some time to raise rates at least until the spring of next year.

Week Ahead Political Risk to Drive Dollar

James Comey to Testify in Russia probe

The US dollar is lower across the board and has given all the 2017 gains to end up near pre-elections levels. The turmoil in Washington continues to be the main driving factor for markets with the potential testimony of former FBI Director James Comey on Wednesday the biggest event risk for the greenback. The U.S. Federal Reserve has sent mixed signals via non-voting members on the path of rate hikes but the market still holds a 78.5 probability of higher rates when the US central bank meets in June.

The Bank of Canada (BoC) will release its rate statement on Wednesday, May 24 at 10:00 am EDT. The central bank is heavily expected to hold rates unchanged despite growing pressure from a heating up house market in major cities. The CAD has been caught between a falling dollar and the more aggressive tone of the US regarding NAFTA renegotiation. The US has set in motion the process needed to renegotiate the deal in late August. The Fed will release the minutes from the April Federal Open Market Committee (FOMC) meeting on Wednesday at 2:00 pm. The Fed hosted no press conference in April, leaving the market to wait for the minutes to gather insights into the views of the central bank on the path of rates for the reminder of the year.

Organization of the Petroleum Exporting Countries (OPEC) members met on Wednesday, Thursday and Friday, as part of a panel to discuss the different scenarios ahead of the Thursday, May 25 meeting with non-OPEC members. Sources said that there is no agreement on the final scenario with additional cuts an option as US shale production continues to ramp up.

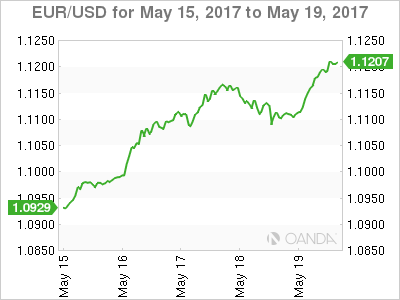

The EUR/USD gained 2.466 percent in the last five days. The single currency is trading at 1.1190 after the USD had a dismal week as more information around US President Donald Trump's communications were shared after the dismissal of FBI Director James Comey. There has been limited economic data in Europe and the US with the currency pair trading on investor's risk aversion as political risk focus shifted from Europe to the US.

The U.S. Federal Reserve was active in the markets via the comments of Cleveland Federal Reserve President Loretta Master who was hawkish calling for more rate hikes and warning about waiting too long to hike. On the other side was James Bullard President of the St Louis Fed that called the current path overly aggressive and that the market hasn't quite bought in to the central bank messaging. The minutes from the FOMC in April will shed more light into what are the different viewpoints inside the rate setting board ahead of the June 13/14 two day meeting that is anticipated will end with higher rates, but current political turmoil and underperforming economic data has put the rate policy decision into question.

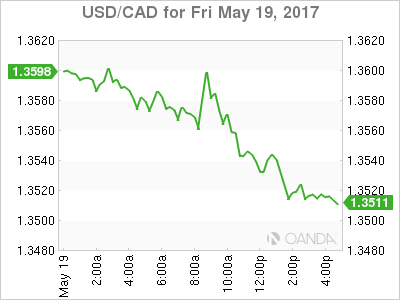

The USD/CAD lost 0.267 percent in the last 24 hours. The pair is trading at 1.3560. The USD has retreated versus the loonie by 1.077 on a weekly basis as political drama has engulfed the Trump administration and President's Trump handling of information with Russia. The price of oil is rising after a 1.8 million barrel drawdown in weekly US crude inventories and the continued press releases by OPEC members supporting the extension of the production cut agreement.

The financial troubles at alternative lender Home Capital Group was responsible for Moody's downgrading the six Canadian banks as their risk has grown. Canadian household debt is reaching record levels as historic low rates have fuelled an appetite for credit that has turned the real estate market into a bubble. There has been multiple warnings but its almost a running joke as home owners dismiss the statements from the OECD, World Bank, ratings agencies, the government and the central bank as the boy who cries wolf. The reality is that without higher rates the wolf will certainly not come, but rates will be higher as macro conditions could force the BoC into a raising rates and then it will find Canadian households even deeper in debt.

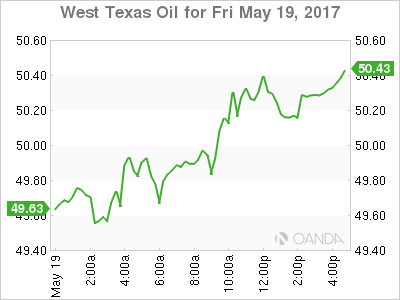

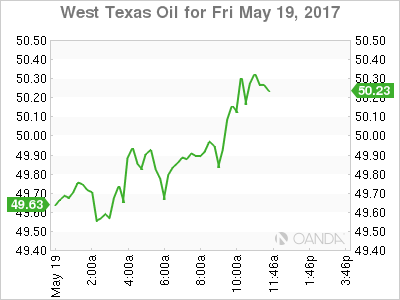

Oil prices gained 2.81 percent on Friday. The price of West Texas Intermediate is trading at $50.19 closing a week where crude gained 5.4 percent after the Saudi Arabia and Russia press release on the OPEC cut extension and the drawdown in weekly oil inventories in the US. The market will be watching next week's inventories released on Wednesday at 10:30 am and the OPEC meeting on May 25 where more details about the extension will be announced. The oil market has been caught between the OPEC's efforts to reduce the glut of oil in the market, but as prices have risen so has the levels of US shale production.

Gold has gained 1.741 in the last five days. The yellow metal is trading at $1,251.23 after risk aversion has driven investors to seek a safe haven. The gold rally lost momentum on Friday but is on target to book one of the best weeks for the metal. The uncertainty around the US President and Russian contacts is a developing story that has driven VIX higher and boosted gold as a result. Next week will be an important one for the commodity and the USD as former FBI director could appear before congress to answer questions regarding what Trump did and didn't tell him about the FBI's investigations into his campaign connections to Russia.

Market events to watch this week:

Tuesday, May 23

- 4:00 am EUR German Ifo Business Climate

- 5:00 am GBP Inflation Report Hearings

Wednesday, May 24

- 8:45am EUR ECB President Draghi Speaks

- 10:00 am CAD BOC Rate Statement

- 10:00 am CAD Overnight Rate

- 10:30 am USD Crude Oil Inventories

- 2:00 pm USD FOMC Meeting Minutes

- 10:00pm NZD Annual Budget Release

Thursday, May 25

- 4:30 am GBP Second Estimate GDP q/q

- All Day ALL OPEC Meetings

- 8:30 am USD Unemployment Claims

Friday, May 26

- 8:30 am USD Core Durable Goods Orders m/m

- 8:30 am USD Prelim GDP q/q

*All times EDT

BoC Policy Meeting, OPEC & Non-OPEC Gathering, FOMC Minutes, Key Data in Focus

Next week's market movers

- The Bank of Canada is expected to stand pat once again. We see the case for policymakers to shift to an even more cautious tone than previously, in light of the recent tariffs from the US.

- In Vienna, major OPEC and non-OPEC producers will meet. The latest comments suggest that November's oil output-cut deal is very likely to be extended by 9 months.

- In the US, the minutes from the latest FOMC meeting could shed some light on whether the Committee is indeed set to hike in June should economic data hold up.

- We also get key economic data from Germany, Eurozone, the UK, the US, and Japan. On

On Monday, we have a quiet calendar day, with no major events or indicators due to be released.

On Tuesday, Eurozone's preliminary manufacturing and services PMIs for May will be in focus, though no forecast is available for any index yet. April's composite survey was particularly upbeat, indicating that the bloc's economy is growing at an encouragingly robust pace. What's more, the report shows that price pressures remain elevated with the price index suggesting that core inflation will trend higher in coming months. Should May's survey indicate similar results, we think that this could enhance even further speculation regarding an increasingly more optimistic ECB at its upcoming meetings, especially since the bloc's latest "hard data" are already consistent with such a move by the Bank.

From Germany, we get the Ifo survey for May. Without a forecast available, we see the case for both the current conditions and the expectations indices to have risen. We base our view on the ZEW survey for the month, which indicated that both the expectations and the current conditions assessments of financial analysts rose during the month. The survey showed that the prospects for the Eurozone as a whole are improving, a factor that strengthens the economic environment for German exports. We expect the Ifo survey to indicate a similarly upbeat message coming from German businesses, especially considering that Eurozone's political risks are now out of the way.

On Wednesday, all eyes will be on the Bank of Canada rate decision. The forecast is for the Bank to remain on hold once again. Policymakers maintained a neutral tone the last time they met, balancing every upbeat comment about the economy with a worried follow-up remark. The key message we got was that Canadian economic data are improving, but the Bank thinks it is too soon to materially alter its stance, mainly due to uncertainties related to the outlook for trade. Indeed, BoC policymakers now probably feel vindicated about their cautious stance, considering that shortly after that policy meeting, the US imposed tariffs on Canada. Given also that recent economic data have been soft, with the core CPI falling further in April and February's GDP stagnating, we consider it likely that the BoC will maintain, if not amplify further, its concerned message.

In the US, the main event will be the release of the minutes from the FOMC's May policy gathering, where the Committee kept its policy unchanged and offered very few hints with regards to the timing of the next rate hike. The most noteworthy point in the statement was that policymakers view the slowdown in Q1 GDP as transitory, implying this softness will not deter them from hiking rates again in the near-term should growth rebound in Q2. Indeed the Atlanta Fed GDPNow model adds credibility to that scenario by indicating that GDP growth rebounded to 4.1% in Q2. Besides that point, the statement was more or less a reiteration of the previous one and as such, we expect investors to scan the minutes for any clear clues as to whether the next hike is likely to come as early as June. At the time of writing, the probability for such action rests at roughly 78% and if the minutes confirm the Bank is likely to act soon in case economic data evolve as it expects, we think that probability is likely to rise further.

On Thursday, the highly anticipated meeting between major OPEC and non-OPEC oil producers will take place in Vienna. The latest comments from the oil ministers of Saudi Arabia and Russia, the largest OPEC and non-OPEC producers respectively, suggest that they have agreed to extend the November oil-output cut deal until March 2018, an extension of 9 months at the current volume of 1.8 mbpd. Heading into the meeting, we think that more optimistic comments regarding the prospect of such an extension could keep oil prices supported. Chatter for deeper production cuts could lift prices further. However, if all we finally get is a 9-month extension, we see further upside in oil prices as likely being limited. In our view, most, if not all, the good news are probably already priced in following the comments from the Saudi and Russian ministers. As such, in order for oil prices to rally significantly, we believe that producers have to deliver something over and above what the market currently expects, namely an extension of a full year and/or deeper production cuts.

As for the bigger picture, we stick to our long-term view that even in case of the anticipated accord, a long-term healthy uptrend in oil prices is still unlikely. The continued increase in US production – evident by the latest EIA data as well as the recovery in the Baker Hughes oil rig count – is likely to keep a lid on any significant gains in the precious liquid's price. In addition, there is also the risk that the nations which are exempted from the production cuts, Libya and Nigeria, raise their output notably, thereby offsetting some of the cuts from the other producers.

With regards to the economic data, from the UK we get the 2nd estimate of GDP for Q1. Without a forecast available, we see the case for the 2nd reading to be in line with the preliminary figure and confirm that economic growth slowed notably from Q4. This data release will also include business investment data for Q1, which we expect to attract a lot of attention considering that investment surprisingly declined the previous quarter. This generated concerns that the first real impact of Brexit-related uncertainties had shown up, as firms appeared hesitant to invest in the UK ahead of the impending Brexit negotiations. As a result, we expect investors to pay close attention to the Q1 print, in order to determine whether this was a one-off, or if Brexit jitters have already began to weigh on economic growth.

.

.

On Friday, during the Asian morning, Japan will release its CPI data for April, though no forecast is available for any figure yet. Our own view is that both the headline and core rates likely rose during the month, which we base on the nation's Tokyo CPI prints for the same month. Both the headline and the core Tokyo rates rose by more than anticipated. Even though something like that would probably be encouraging news for BoJ policymakers, as long as both the nationwide rates remain stuck close to 0%, we do not expect the Bank to alter its current policy framework.

.

.

In the US, durable goods orders for April are due to be released. The forecast is for the headline rate to have fallen, while the core rate that excludes transportation equipment, is expected to have risen following a stagnant print in March. We share the view for a decline in the headline print, considering the slowdown in civilian aircraft orders in April, while we see the risks surrounding the core forecast as skewed to the downside. We base our view for the core print on the nation's ISM manufacturing PMI, which showed that new orders slowed down notably during the month.

.

.

As for the rest of the US data, we also get the 2nd estimate of Q1 GDP. Expectations are for economic growth to have been revised upwards, albeit slightly. However, we doubt that it will have much market impact, given that the Fed has already pointed that the growth softness throughout the quarter was transitory. As a result, we think that investors will pay more attention to incoming US data for Q2, as well as the Atlanta Fed GDPNow model, in order to get a better picture of whether economic activity have rebounded. Any signs of such a rebound may strengthen the case for a June hike further.

.

.

Soft CPI Not Likely to Influence Monetary Policy in Canada

Canadian consumer prices picked up in March, but not enough to lift the year-over-year rate as the consensus had expected. Consumer spending picked up in March, though the strength was concentrated in autos.

Recent Soft Inflation Not Likely to Influence Monetary Policy

After an unexpected slowing in Canadian CPI in March, consumer prices picked up in April, but not as much as expected. The monthly increase of 0.4 percent kept the year-over-year rate of CPI inflation unchanged at 1.6 percent. Headline CPI inflation had been running at 2.0 percent earlier this year, spot-on the midpoint of Bank of Canada's (BoC) 1.0 percent to 3.0 percent target range.

Still, we do not expect the latest inflation figures to substantively influence the BoC's policy at its meeting next week. In fact, the inflation story is more or less living up to the Bank's expectations. Following its April 12 meeting the BoC said that "CPI inflation is expected to dip in the months ahead, as the temporary factors unwind, and then return to 2 per cent later in the projection horizon as the output gap closes."

Strength in Retail Sales Concentrated in Autos

In a separate report also released this morning, Canadian retailers reported a 0.7 percent improvement in March sales after a drop in sales the prior month. The better-than-expected rebound was mostly a function of the strength in motor vehicle sales. Excluding autos, sales were actually down 0.2 percent. On balance we remain cautious on the outlook for the ability of consumer spending to sustain Canadian economic growth in the way that it has thus far in this expansion.

Consumer spending has added to GDP growth in Canada for 31 consecutive quarters. That is almost eight years without a miss. Understandably, that spending growth has been accompanied by a run-up in aggregate measures of consumer debt. As the bottom chart at right shows, households in Canada have been leveraged more than they have been historically. Fast-growing home prices (arguably overheated in some markets) are compelling many Canadians to take on more debt as prices continue to rise.

Somewhat counter-intuitively, the cost of living in the country's hottest real estate markets is not holding back the pace of retail sales locally. On a provincial basis, retailers in Ontario reported a 0.9 percent increase in sales during March and British Columbia saw a pick-up of 2.3 percent.

Together, the store sales in these two provinces comprise roughly half of all retail sales in Canada. Both markets have seen year-over-year increases in retail sales (7.5 percent in Ontario and 8.9 percent in British Columbia) that are above the national average of 6.9 percent.

On the brighter side, the labor market remains supportive of consumer spending. Yesterday, Statistics Canada reported a 0.5 percent decline in unemployment insurance claims in March in the latest affirmation of job market strength in Canada.

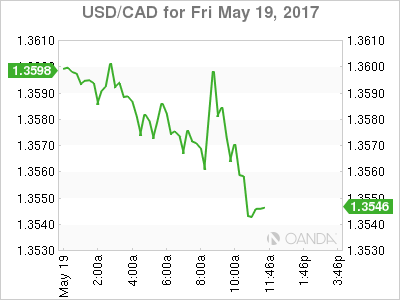

Canadian Dollar Higher as Retail Sales Rises in April

The USD/CAD pair is trading at 1.3569 the lowest level for the USD as the Canadian dollar appreciates on Friday. Higher oil prices have boosted the loonie versus the greenback but mixed economic data released this morning pared some of those gains. Retail sales in April beat expectations with a 0.7 percent gain, but stripping away the more volatile components such as auto sales disappointed with a 0.2 percent contraction when a 0.2 percent gain was anticipated. Inflation missed the target with a 0.4 percent gain as falling food prices offset the rise of gasoline.

The week of May 15 to 19 was on paper a quiet one with few major releases scheduled. Political risk as has been the case since last summer took over as the main driving factor in global markets. The Brazilian president's troubles joined the US political turmoil and drove safe havens higher as uncertainty in two major economies adding to two elections , one in the United Kingdom and the Parliamentary elections in France coming in June.

The Canadian dollar is trading at a tree week high as two of the three major factors for the loonie have stabilized. The price of crude has risen after the Organization of the Petroleum Exporting Countries (OPEC) and Russia have announced a commitment to an extension which will probably be announced in full on their May 25 meeting. The USD is lacking momentum as investors struggle to price in the turmoil in Washington that could end with the impeachment of President Trump. Despite the FBI and Russia distractions the Trump administration has carried out the first step in NAFTA renegotiations and has started to brief Congress and the House giving 90 days to being formal talks with Canada and Mexico. The 14 month low of the Canadian dollar came as tariffs and stronger statements about NAFTA were issued earlier in the month.

The USD/CAD lost 0.267 percent in the last 24 hours. The pair is trading at 1.3560. The USD has retreated versus the loonie by 1.077 on a weekly basis as political drama has engulfed the Trump administration and President's Trump handling of information with Russia. The price of oil is rising after a 1.8 million barrel drawdown in weekly US crude inventories and the continued press releases by OPEC members supporting the extension of the production cut agreement.

The Bank of Canada (BoC) will release its rate statement on Wednesday, May 24 at 10:00 am EDT. The central bank is heavily expected to hold rates unchanged despite growing pressure from a heating up house market in major cities. The financial troubles at alternative lender Home Capital Group was responsible for Moody's downgrading the six Canadian banks as their risk has grown. Canadian household debt is reaching record levels as historic low rates have fuelled an appetite for credit that has turned the real estate market into a bubble. There has been multiple warnings but its almost a running joke as home owners dismiss the statements from the OECD, World Bank, ratings agencies, the government and the central bank as the boy who cries wolf. The reality is that without higher rates the wolf will certainly not come, but rates will be higher as macro conditions could force the BoC into a raising rates and then it will find Canadian households even deeper in debt.

Oil prices gained 2.81 percent on Friday. The price of West Texas Intermediate is trading at $50.19 closing a week where crude gained 5.4 percent after the Saudi Arabia and Russia press release on the OPEC cut extension and the drawdown in weekly oil inventories in the US. The market will be watching next week's inventories released on Wednesday at 10:30 am and the OPEC meeting on May 25 where more details about the extension will be announced. The oil market has been caught between the OPEC's efforts to reduce the glut of oil in the market, but as prices have risen so has the levels of US shale production.

Market events to watch this week:

Tuesday, May 23

- 4:00 am EUR German Ifo Business Climate

- 5:00 am GBP Inflation Report Hearings

Wednesday, May 24

- 8:45am EUR ECB President Draghi Speaks

- 10:00 am CAD BOC Rate Statement

- 10:00 am CAD Overnight Rate

- 10:30 am USD Crude Oil Inventories

- 2:00 pm USD FOMC Meeting Minutes

- 10:00pm NZD Annual Budget Release

Thursday, May 25

- 4:30 am GBP Second Estimate GDP q/q

- All Day ALL OPEC Meetings

- 8:30 am USD Unemployment Claims

Friday, May 26

- 8:30 am USD Core Durable Goods Orders m/m

- 8:30 am USD Prelim GDP q/q

*All times EDT

Greece: Tsipras Votes On New Austerity Policies

- Opportunity For The Brave In MXN - Peter Rosenstreich

- Brazil Politicians Back Under The Spotlights - Arnaud Masset

- Greece: Tsipras Votes On New Austerity Policies - Yann Quelenn

- China Online

Economics - Opportunity For The Brave In MXN

US political uncertainty finally took its toll on EM FX and global risk sentiment. After five months of nearly uninterrupted strength, speculations on President Trump impeachment and halt of his pro-growth agenda send investors running from EM risk. Unlike passed pullbacks the suddenness and aggressiveness of the selling shocked many. However, we remain constructive on EM FX as we haven't seen any material shifts. House speaker Paul Ryan was quick to address this fact, highlighting that efforts on healthcare and tax reform were still taking place.

A republican controlled congress can still push the "Trump" agenda even while the president is lawyering up. Removing the transitory political uncertainty we still have an positive environment with low interest rates and volatility (despite temporary surge), solid growth outlook and fading threat of protectionism (a weaker administration is a clear upside for trade dependent EMs). Interesting, the financial markets instability has decreased the probably of additional hikes after June, further supporting EM yield differentials. The nation most exposed to Trumps punitive trade policy has been Mexico. Declining prospect of a significantly redefined NAFTA and domestic hawkish monetary policy makes long MXN a key opportunity. While much of the Trump trade is has already unwound, we still think there are gains to be made given the market repositioning.

Last week's Banxico monetary policy decision saw an unanimous vote to raise the reference rate 25bp to 6.75%. The rational was the balance of risk on inflation were still skewed to the upside. As probably of second round effect pushing inflation higher had increase, which has already pushed reads (10 straight months of upwards trend) and outlook higher. The culprits are the weaker peso, tightening labor conditions and wages and top line items such as gasoline, perishable goods and transport cost.

The cyclical rebound that we expect in the US, after a soft 1Q will also push inflations expectation higher. Mexican general elections 1st July will further keep Banxico on a restrictive policy path as uncertainy could trigger outflows.

We don't expected Banxico to completely decouple from the Fed tightening cycle. Yet unless inflation prints moderate in the coming months they will have to address these elevated levels. Current outlook has raised the probability that Banxico will have to increase rates again after the Fed hikes in June. The prospect of a hawkish central banks, calming sentiment and 25bp more of tighten (at least) before ending its hiking cycle should support MXN against the USD.

Economics - Brazil Politicians Back Under The Spotlights

Brazilian assets fell sharply on Thursday at the market opening in São Paulo as the political uncertainty rose by another notch. The Brazilian real fell more than 7% against the greenback with USD/BRL rising at around 3.3760 compared to Wednesday's close of 3.1349 after Brazilian newspaper reports about President Michel Temer.

On the equity side, the situation was not bright either as sell-off in Brazilian equities triggered a circuit-breaker that halted trading after futures on the Bovespa crashed 10% at the Thursday open. In one day, the Brazilian stock market erased almost entirely the gains accumulated since the New Year as the Bovespa closed the session at 61,597.

Investors were caught by surprise as the political situation seemed to settling down as the business-friendly Brazilian President successfully managed to ease foreign investors' concerns. Traders' panicked reaction sent option's implied volatility on USD/BRL through the roof with the 1m measure spiking to 24% from 13.5% a day earlier. The 1m 25 delta risk reversal measure, which is the difference between the price of a call and a put, spiked to 5.74%. Despite the fact that Temer tried to reassure markets, financial indicators continued to move in the other direction with treasury yields and CDS exploding.

Investors reacted aggressively to the news therefore we may see a temporary stabilisation of Brazilian assets morning, especially since the global risk-off sentiment is easing with global equities recovering this morning. On Friday, the real recovered 2.30% against the greenback with USD/BRL heading towards 3.25, while the Bovespa index rose 1.70%. However, investors are more than accustomed with the Brazilian political landscape and they know that it may take months before an equilibrium may be reached again. At the moment, the outlook is quite uncertain as Temer denied bribery allegations and rejected calls to quit, demanding a "full and rapid investigation".

We expect Brazilian assets to continue stabilising. However, investors will remain on their toes as the political turmoil will not vanish overnight. Therefore we would remain cautious regarding the BRL's outlook, even though there will be some opportunities in the short-term as investors pay more attention to local developments.

Economics - Greece: Tsipras Votes On New Austerity Policies

It has been a while since Greece was at the top of the market news. We consider the Greek debt is still a key issue for the European Union so we are still monitoring the country. The Hellenic country is now back into recession (printing two consecutive growth negative quarters). First quarter GDP printed at -0.1% q/q while last year final GDP has been released at -1.2% q/q. The massive austerity policies over the last few years has not been really useful so far.

Greece is having strong difficulties to repay its debt as we mentioned several times over the last two years. Last week, in order to be able to pay the next €6 billion installments, Tsipras and the parliament approved the pension cuts in order to get €7 billion bailout. At this point, who can still believe that this is going to end up well? This is a never ending story, the cost of servicing the debt is way too massive so we firmly believe that no positive issue will be found in the medium-term. Greece cannot devalue its currency and so it is then forced to devalue internally, for instance its public aid (pensions in particular).

Since February 2015, Greece has repaid €35.4 billion and by the end of 2018 Greece must repay €28 billion (including €2.7 billion of interest). To put that into perspective, the 2016 nominal GDP was €176 billion. The economy must then expand by at least more than 1.5% next year just to reimburse the interest. And it is important to note that next year repayments are less than half of what Greece will need to pay in 2019.

We don't see how Greece will be able to reimburse this debt as it is clear that the country won't be able to print a growth above the cost of servicing its debt. In the short-term, everything looks decent on the single currency side but what will happen when Portugal or Spain have issues as deep as Greece. Uncertainties are far from over on the euro side.

Themes Trading - China Online

Chinese stocks are still reeling from the all-out collapse of local equity markets. Yet while valuations have suffered, the fundamentals remain enticing.

China is undisputedly the largest internet market in the world in terms of its user base, with 620 million users - nearly double that of India and triple that of the USA. Yet the penetration rate is only 45%, compared with 84% for the USA, which means there is significant room for growth. According to Kantar Retail, China has become the world's largest e-commerce market, with sales of $589 billion in 2015. China has developed its own online offering catering to the country's unique culture. Western companies have had a challenging time breaking into the market due to structural and cultural issues. The result has been the incubation of innovative world-class private enterprises. As China shifts from investment- to consumption-led growth, these agile entrepreneurs will also benefit from support and protection from Beijing. With valuations in the single digits, these names offer significant upside potential.

For this theme, we included social media, search engines, retail and B2B commerce, travel and key hardware manufacturers.

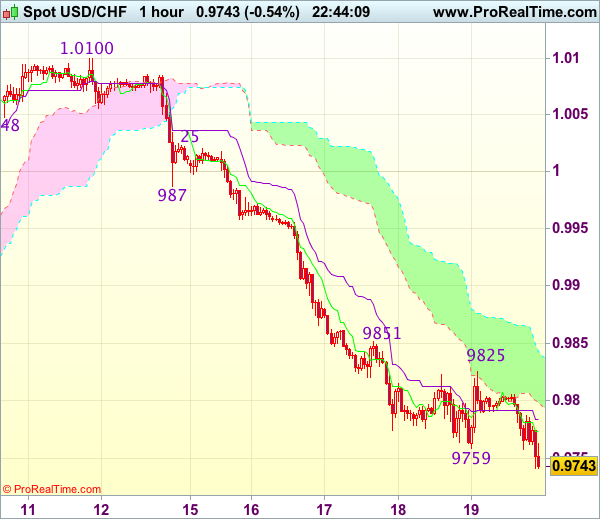

Trade Idea Wrap-up: USD/CHF – Sell at 0.9850

USD/CHF - 0.9750

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9773

Kijun-Sen level : 0.9783

Ichimoku cloud top : 0.9843

Ichimoku cloud bottom : 0.9799

Original strategy :

Sell at 0.9850, Target: 0.9750, Stop: 0.9885

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9850, Target: 0.9750, Stop: 0.9885

Position : -

Target : -

Stop : -

As dollar has fallen again after brief recovery, suggesting recent selloff from 1.0344 top is still in progress and bearishness remains for this move to extend further weakness to 0.9735-40 (76.4% retracement of 0.9550-1.0344), then towards 0.9700, however, near term oversold condition should prevent sharp fall below 0.9675-80 and reckon 0.9650 would hold from here, risk from there is seen for a rebound to take place later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 0.9850-55 should limit upside. Above 0.9870-80 would defer and risk rebound to 0.9900 but upside should be limited to 0.9940-50 and price should falter well below previous support at 0.9987, bring another decline.

Trade Idea Wrap-up: GBP/USD – Stand aside

GBP/USD - 1.3026

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2960

Kijun-Sen level : 1.2960

Ichimoku cloud top : 1.2992

Ichimoku cloud bottom : 1.2957

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite falling sharply from 1.3048 to 1.2889, the subsequent stronger-than-expected rebound has dampened our near term bearishness and gain to 1.3048 resistance (yesterday’s high) cannot be ruled out, however, break there is needed to signal recent upmove has resumed an extend further gain to 1.3075-80 and possibly towards 1.3100-10 later.

In view of this, would not chase this rise here and would be prudent to stand aside in the meantime. Below 1.2955-60 would prolong consolidation and risk weakness to 1.2930-40 but said support at 1.2889 should remain intact and bring another rebound later.

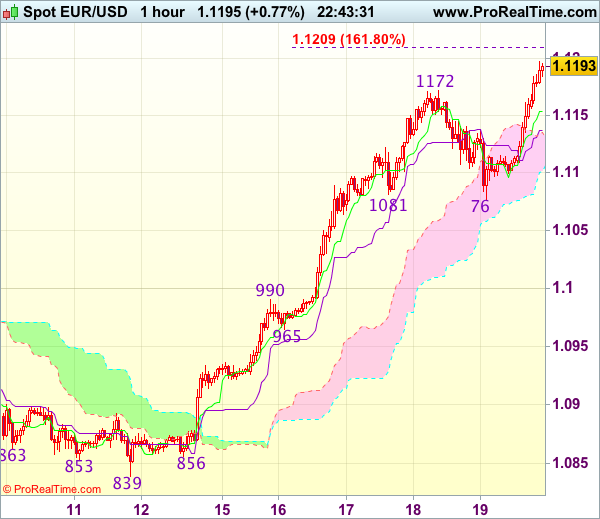

Trade Idea Wrap-up: EUR/USD – Stand aside

EUR/USD - 1.1190

Most recent candlesticks pattern : N/A

Trend : Up

Tenkan-Sen level : 1.1153

Kijun-Sen level : 1.1137

Ichimoku cloud top : 1.1135

Ichimoku cloud bottom : 1.1101

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although current break of indicated previous resistance at 1.1172 confirms recent upmove has resumed and may extend further gain to 1.1205-10 (1.618 times projection of 1.0839-1.0990 measuring from 1.0965), loss of momentum should limit upside and reckon 1.1250 would hold from here, risk from there is seen for a retreat later.

In view of this, would not chase this rise here and would be prudent to stand aside in the meantime. Below the Tenkan-Sen (now at 1.1153) would defer and bring test of the Kijun-Sen (now at 1.1137), break there would suggest top is possibly formed, risk correction to 1.1100 but reckon support at 1.1076 (yesterday’s low) would hold from here.

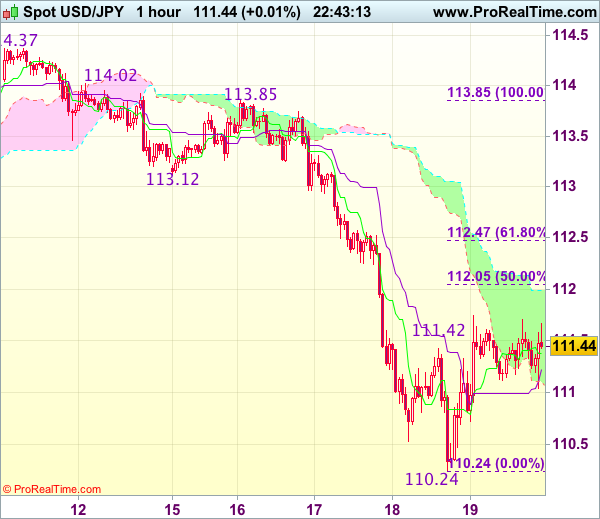

Trade Idea Wrap-up: USD/JPY – Sell at 112.05

USD/JPY - 111.45

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 111.37

Kijun-Sen level : 111.22

Ichimoku cloud top : 111.99

Ichimoku cloud bottom : 111.11

Original strategy :

Sell at 112.05, Target: 110.85, Stop: 112.40

Position : -

Target : -

Stop : -

New strategy :

Sell at 112.05, Target: 110.85, Stop: 112.40

Position : -

Target : -

Stop : -

Dollar’s rebound after falling to 110.24 suggests consolidation above this level would be seen and corrective bounce to 112.00-05 (50% Fibonacci retracement of 113.85-110.24) cannot be ruled out, however, reckon upside would be limited and bring another decline later, below 110.70-75 would suggest the rebound from 110.24 has ended, bring retest of this level first.

In view of this, would not chase this fall here and would be prudent to sell dollar on subsequent recovery as 112.05-10 should limit upside and bring another decline. Above 112.35-40 would defer and signal low is formed instead, risk a stronger rebound to 112.65-70.