Sample Category Title

Trade Idea Update: GBP/USD – Stand aside

GBP/USD - 1.3021

Original strategy :

Sold at 1.2990, stopped at 1.3025

Position : - Short at 1.2990

Target : -

Stop : - 1.3025

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Despite falling sharply from 1.3048 to 1.2889, the subsequent stronger-than-expected rebound has dampened our near term bearishness and gain to 1.3048 resistance (yesterday’s high) cannot be ruled out, however, break there is needed to signal recent upmove has resumed an extend further gain to 1.3075-80 and possibly towards 1.3100-10 later.

In view of this, would not chase this rise here and would be prudent to stand aside in the meantime. Below 1.2955-60 would prolong consolidation and risk weakness to 1.2930-40 but said support at 1.2889 should remain intact and bring another rebound later.

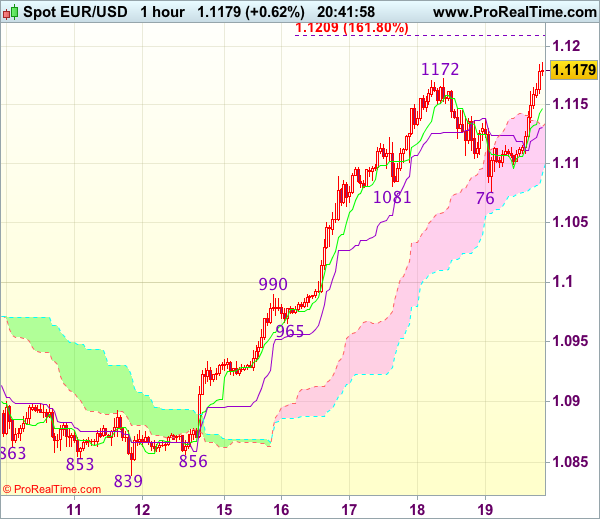

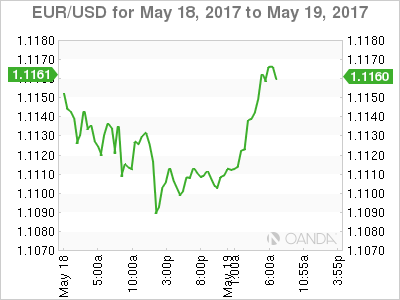

Trade Idea Update: EUR/USD – Stand aside

EUR/USD - 1.1178

Original strategy :

Buy at 1.1055, Target: 1.1155, Stop: 1.1020

Position : -

Target : -

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although current break of indicated previous resistance at 1.1172 confirms recent upmove has resumed and may extend further gain to 1.1205-10 (1.618 times projection of 1.0839-1.0990 measuring from 1.0965), loss of momentum should limit upside and reckon 1.1250 would hold from here, risk from there is seen for a retreat later.

In view of this, would not chase this rise here and would be prudent to stand aside in the meantime. Below the Tenkan-Sen (now at 1.1147) would defer and bring test of the Kijun-Sen (now at 1.1131), break there would suggest top is possibly formed, risk correction to 1.1100 but reckon support at 1.1076 (yesterday’s low) would hold from here.

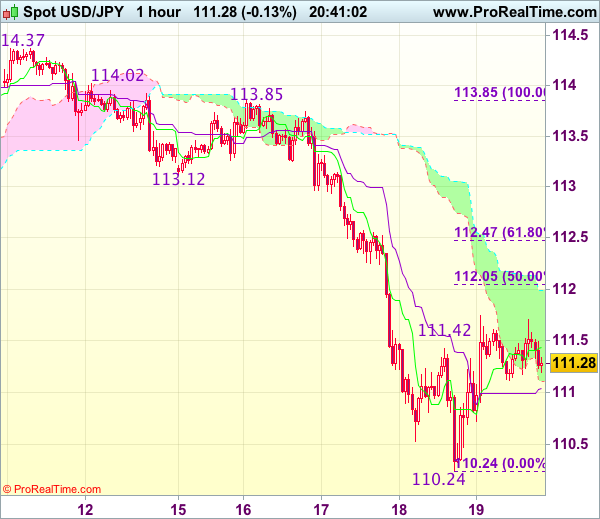

Trade Idea Update: USD/JPY – Sell at 112.05

USD/JPY - 111.31

Original strategy :

Sell at 112.05, Target: 110.85, Stop: 112.40

Position : -

Target : -

Stop : -

New strategy :

Sell at 112.05, Target: 110.85, Stop: 112.40

Position : -

Target : -

Stop : -

Dollar’s rebound after falling to 110.24 suggests consolidation above this level would be seen and corrective bounce to 112.00-05 (50% Fibonacci retracement of 113.85-110.24) cannot be ruled out, however, reckon upside would be limited and bring another decline later, below 110.70-75 would suggest the rebound from 110.24 has ended, bring retest of this level first.

In view of this, would not chase this fall here and would be prudent to sell dollar on subsequent recovery as 112.05-10 should limit upside and bring another decline. Above 112.35-40 would defer and signal low is formed instead, risk a stronger rebound to 112.65-70.

GBP/CHF Could Start Correction Soon

The GBP/CHF has formed a regular bullish divergence at Daily L5 support and currently shows a potential for upside correction. The POC zone 1.2665-75 (Multiple bottom, ATR pivot, historical buyers) might spike the price towards L4 and L3 (1.2759 and 1.2828). Have in mind that L4 (1.2759) is a strong resistance and price needs to break above potential head and shoulders pattern to proceed further up. At this point the price is supported by POC zone and bullish divergence and until 1.2759 is hit we should see an upside price action.

Equities Bounce Back After Midweek Sell-Off

It's been one of the quieter days of the week so far in terms of major news flow or economic data and yet, equities are anything but flat as we near the US open, with the events of the previous days continuing to have an impact.

Trump distraction fades as markets bounce back from midweek sell-off

Wednesday's sell-off in equity markets got many people worried about whether the political circus in the US was finally starting to take its toll on investor appetite at the near-record levels. What we've seen since though would clearly suggest otherwise and instead indicate that the moves two days ago were nothing more than a combination of the usual Trump distraction combined with technical levels giving way.

The distraction is obviously undesirable, especially if it develops into anything more, but as it is investors appear relatively confident that it will pass, leaving the administration to focus on the policies that are largely responsible for markets being at these levels, tax reform and spending. The last few months has been something of a waiting game for investors as we await further news on taxes and fiscal stimulus, leaving the S&P and Dow bouncing around between 2,320 and 2,405, and 20,350 and 21,170, respectively. Only a break below here would suggest to me that investors are losing confidence.

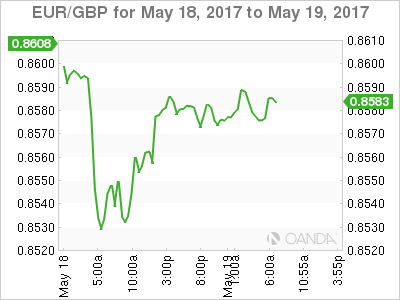

FTSE weighed down by GBP rebound following Thursday's mini flash crash

In Europe, the FTSE's run this morning has been a little hampered by sterling's resurgence, which comes following a mini flash crash after the European session on Thursday. The stronger pound can weigh on the FTSE, due to its substantial foreign exposure, and that appears to be happening today. The pound is still currently looking a little overextended at these levels and last night's moves are another reminded of its vulnerability. Should it fail to break above 1.3048 against the dollar, it may suggest the pair has topped for now.

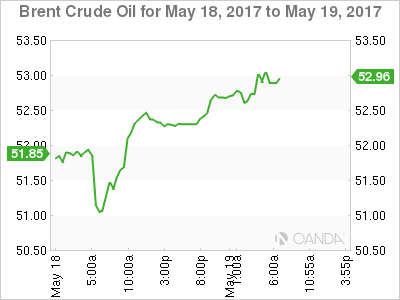

Oil boosted by reports that OPEC considering deepening and extending cuts

Oil is trading higher once again today, supported once again by the prospect of a nine month extension to the current output deal. Reports this morning that OPEC is considering not just extending but also deepening the cuts in a bid to bring the market back into balance is likely supporting the move, with Brent and WTI now on course for their seventh winning session in eight. Of course, just because OPEC is considering this and the Russian energy minister has suggested a willingness to support an extension, it doesn't mean it will happen, especially with regards to the deeper cuts as reported this morning.

EUR/USD Bulls Approach Major Resistance at 1.1200

EUR/USD has remained bullish and rallied notably around 2.7% since May 15, helped by the recent slump in the USD.

EUR/USD saw a correction on May 18, as a result of the rebound of USD.

Friday morning, during early European session, EUR/USD rallies again and approaches the significant psychological resistance level at 1.1200, due to the weakening of USD.

Currently, the bullish momentum remains strong, the short term moving averages still edge up.

If the resistance level at 1.1200 is broken, we can expect that the price will go further up.

Conversely, if the bulls fail to break the resistance, we will likely see a correction.

The resistance level is at 1.1170, followed by 1.1200.

The support line is at 1.1130, followed by 1.1100.

CAC Steady Ahead Of Eurozone Current Account, Consumer Confidence

The France CAC index has edged higher in the Friday session. Currently, the CAC is trading at 5370.80, up 0.50 percent. On the release front, it's a quiet day. The eurozone current account surplus came in at EUR 34.1 billion in March. This was lower than the February reading, but beat the estimate of 32.3 billion. Later in the day, we'll get a look at consumer confidence, which is expected to improve to -3 points.

Global stock markets have suffered losses this week, and the CAC index has dropped 1.9%, largely due to the political turmoil in Washington, which has made investors jittery. The Trump administration has not had much success in damage control, and there is no sign of the political firestorms letting up any time soon. President Trump has endured a rocky start to his term, but last week may have been his worst one of all. The US Justice Department, under strong pressure from Congress, has appointed a former FBI director as a special prosecutor to investigate possible Russian involvement in the US presidential election as well as any connection between Trump and the Russians during the election campaign. President Trump fired back on Thursday, angrily denouncing this move as a “witch hunt”. The media and the Democrats have had a field day with Trump's troubles, and even Republicans are expressing unease with an administration that appears rudderless and is staggering from crisis to crisis. Trump has been relentlessly dogged by accusations of being cozy with the Russians, and his meeting with the Russian foreign minister last week was a public relations disaster, as the president came under heavy criticism for releasing classified information at the meeting. The latest string of controversies has had a chilling effect on global stock markets, and the downward trend could continue if the crisis in Washington worsens.

The eurozone economy is showing stronger growth, and inflation levels have also picked up. Final CPI for April posted a strong gain of 1.9%, matching the forecast. This was considerably higher than the March gain of 1.5%. Eurozone inflation is once again closing in on the ECB's target of 2.0%, which could increase pressure on the ECB to consider tapering its ultra-loose monetary policy. However, the ECB seems content to hold course on interest rates and its quantitative easing program, and the central bank will be reluctant to make any moves with key elections coming up in France and Germany.

EURJPY – Follows Through Higher On Recovery

EURJPY - The pair faces further move higher following strong strength during Friday trading today. On the downside, support comes in at the 124.00 level where a break if seen will aim at the 123.50 level. A cut through here will turn focus to the 123.00 level and possibly lower towards the 122.50 level. On the upside, resistance resides at the 125.00 level. Further out, we envisage a possible move towards the 125.50 level. Further out, resistance resides at the 126.00 level with a turn above here aiming at the 126.50 level. On the whole, EURJPY faces further upside pressure.

Dollar Licks Wounds, But Next Week Is A Big Test

Global equities have inched higher overnight, while the 'big' dollar has held most of its gains on strong U.S economic data as some market risk appetite returns despite caution over political turbulence in the U.S.

Despite the rebound, investors remain on 'high' alert as they have become more sensitive to White House headlines and accusations as concerns grow over the strength of the global economy at a time when some Fed policy members are suggesting further tightening.

With no U.S data on the docket for today, the market will be preparing itself for a multiple event-risks in the week ahead. These events include the testimony by former FBI director James Comey at a Senate hearing and an OPEC meeting in Vienna, May 25.

Note: Federal Reserve Bank of St. Louis President James Bullard speaks to the Association for Corporate Growth at Washington University's in St. Louis (09:15 EST).

1. Stocks find a small reprieve

Asian indices were mixed overnight, tracking a day of stabilization on Wall St. where equities recovered, treasury yields found support and Fed Funds futures outlook for a June hike was back above +70%.

In Japan, the Nikkei edged up (+0.2%) up on financial shares, but has managed to record its first weekly drop in five-weeks. The broader Topix index climbed +0.3%, after sliding -1.3% on Thursday. The gauge has lost -1.3% for the week.

Down-under, the Aussie S&P/ASX 200 Index fell -0.2% percent, capping its worst week since last November.

In Hong Kong, the Hang Seng Index rose +0.2% and the Shanghai Composite was little changed.

Brazil's Ibovespa Index tumbled -8.8%, along with the BRL on Thursday, the most in seven-month, as a political crisis returned to the country after last year's impeachment process. Brazil Supreme court has reportedly opened investigation into President Temer over obstruction of justice.

In Europe, indices are trading higher, tracking positive gains from Asia and the U.S yesterday. Financials are supporting the Eurostoxx, while commodity stocks are better supported on the FTSE 100.

U.S stocks are set to open in the black (+0.2%).

Indices: Stoxx50 +0.4% at 3233, FTSE +0.4% at 7465, DAX +0.4% at 12639, CAC-40 +0.6% at 5324, IBEX-35 +0.5% at 10737, FTSE MIB +0.6% at 21424, SMI +0.6% at 8990, S&P 500 Futures +0.2%.

2. Oil prices climb on hopes output cuts would be extended, gold shines

Ahead of the U.S open, oil futures are trading atop of their one month high on growing optimism that OPEC, and some non-OPEC members, will extend output cuts to curb a persistent glut in crude.

The key benchmarks are heading for their second week of gains.

Brent crude is up +28c, or +0.5%, at +$52.79 and is on track for a +4% climb this week, its second week of gains.

U.S light crude oil (WTI) is up +29c, or +0.6%, at +$49.64 a barrel, highest since April 26. The contract is also heading for a weekly increase of almost +4%.

OPEC ministers meet in Vienna on May 25 to decide production policy for the next six-months. The market is expecting producers to prolong their agreement to limit production, perhaps by up to nine-months.

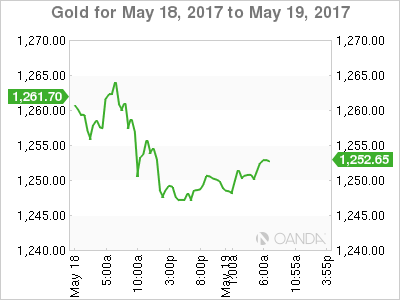

Gold prices (+0.3% to +$1,250.46) have edged higher overnight and are on track for their biggest weekly gain since mid-April as the dollar softens and amid the ongoing political crisis in the U.S. The yellow metal slipped -1.1%yesterday due to profit taking in its biggest one-day percentage drop since May 3 to snap a five-day rally.

3. Global yield curves flatter on the week

Political anxiety surrounding the Trump presidency continues to stoke demand for haven bonds. This week it drove the yield on the 10-year Treasury note to trade atop of this years low yield set in April (+2.175%).

Adding support for U.S debt is the political crisis in Brazil. After the biggest one-day rally in 12-months on Wednesday, the pace of gains for U.S product seems to be somewhat moderating as we close out the week, and as U.S economic data point to improving growth outlook.

Note: The yield on U.S 10's has climbed +1 bps to +2.24%. It ended Thursday flat after earlier sliding to as low as +2.18%.

Fed-funds futures are showing +74% odds that the central bank will raise short-term interest rates by its June 13-14 meeting, up from Wednesday's +63% odds.

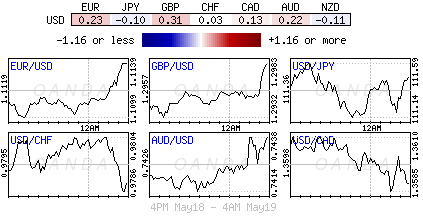

4. Dollar not out of the woods yet

The FX market continues to see some headwinds for the 'mighty' USD as the apparent disarray consuming President Trump's Administration and possible impact on his agenda for the time being.

The EUR (€1.1167) is once again encroaching on the psychological €1.1200 handle on the back of stronger German inflation numbers (see below) and recent ECB speak appearing to have the central bank build the case for autumn QE decision

Sterling (£1.3010) is again making a test above the £1.30 handle. It has failed to get above the psychological level several times over the past week, however, to many, £1.3000 is the key pivot and now a lot of the structural shorts out there post-Brexit will be looking to wind back. Short-term sterling bulls are now targeting £1.3350/1.3400.

USD/JPY (¥111.51) was lower, trading down through ¥112 handle as the JPY currency is having its best week in more than a month aided by demand for safer assets.

5. German PPI records biggest jump in five years.

Euro data this morning shows that price pressure is building in German factories.

Producer prices jumped +3.4% year-on-year in April, marking the strongest gain since December 2011. Digging deeper, the increase was led by higher prices for intermediate goods, which rose +4.3%.

Note: In the last report, it was predominately energy prices that had largely supported the index.

However, ex-energy, Germany's PPI rose sharply too. It was up +2.8% y/y, its strongest gain in six-years. Analysts are expecting rising factory-gate prices could further support German CPI, which hit +2% last month.

The markets focus now turns to the ECB and the possibility of when to begin ending QE.

Markets Stabilize But Investors Remain Alert

Global stocks displayed subtle signs of stability during Friday's trading session as investors re-evaluated the explosive Trump developments which rattled financial markets this week. Asian shares were a mixed bag amidst cautious trading while European equities edged cautiously higher. With the spiralling uncertainty over Donald Trump's political future raising questions over his ability to deliver the heavily anticipated pro-growth policies, gains on Wall Street are likely to be limited. It is becoming increasingly clear that the controversies blanketing Trump have left investors jittery with most seeking concrete answers to what the future may hold. Markets may turn extremely sensitive moving forward and any additional news on this Trump episode should spark more volatility.

Dollar bears are back in town

The Greenback gasped for air on Thursday with prices temporarily reversing earlier losses after stronger-than-expected U.S economic data diverted some attention away from the Trump woes. Short-term bulls were inspired further by the hawkish comments from Loretta Mester, CEO of the Federal Reserve Bank of Cleveland, which renewed expectations of a U.S interest rate increase in June.

The fact that the Dollar has found itself under renewed selling pressure on Friday continues to highlight how the focus remains on the political instability in Washington and growing uncertainty over the future of Trump's administration. With those who were heavily optimistic over Trump's proposed fiscal policies now having second thoughts amidst this uncertainty, the Dollar could become a seller's best friend.

Sterling blocked by 1.30 gate keeper

Sterling smashed through the stubborn $1.30 resistance during Thursday's trading session following the much better than expected British retail sales growth that quelled some Brexit concerns. Retail sales were resilient in April rising 2.3% despite consumers feeling the pinch from wage growth lagging behind inflation. Although short-term Pound bulls may attempt to exploit the positive data and vulnerable Dollar to elevate the GBPUSD higher, gains still remain limited, especially when factoring the growing uncertainty over Brexit negotiations. From a technical standpoint, the GBPUSD still remains at risk of trading lower to 1.2775 if bulls fail to secure a solid daily close above 1.3000. In an alternative scenario, a daily close above 1.3000 should open a path higher towards 1.3250.

OPEC vs U.S Shale

Oil markets lurched higher on Friday as optimism grew over big oil-producing countries extending output cuts to stabilize the markets. Although OPEC may be commended on their ability to repeatedly boost the markets on production cut talks, the effects seem to be wearing out. Oil prices may be exposed to further volatility moving forward as the fierce tug of war between OPEC bulls and U.S Shale bears get underway. While most expect production cuts to be extended until March 2018, I think it's more of a question on how U.S Shale exploits this opportunity to pump more oil into the markets. From a technical standpoint, investors will be paying very close attention to how prices react to the psychological $50 level.

Commodity spotlight – Gold

Gold price traded higher during early trading on Friday and was on track for the biggest weekly gain since April as political unrest in Washington weighed heavily on risk sentiment. Although the metal experienced a sharp technical correction on Thursday, this had nothing to do with a change of bias.It came down to profit taking and a slightly appreciating U.S Dollar. Bulls still remain in control despite the depreciation with prices destined to appreciate higher as uncertainty quickens the flight to safety. From a technical standpoint, buyers need to secure a daily close above $1260 for an incline higher towards $1275.