Sample Category Title

Losses For The Cable Looking Likely As Technicals Deteriorate

Key Points:

- Downside risks are increasing as resistance refuses to yield.

- Technical bias is becoming bearish despite the recent rally.

- Losses could extend as far as the 1.2667 mark.

The Cable has been running into some stiff resistance over the past week and it looks as though it can’t quite muster the momentum to breakout to the upside. What’s more, the pair’s fundamentals have been rather mixed which makes establishing a firm bias somewhat difficult. Due to this, we may have to rely on the technicals to get a feel for what could be on the way in the days to come.

First and foremost, we can’t ignore the presence of the bullish channel that has been making itself felt over the past few months. Specifically, the current position of the Cable relative to the upside of the channel will be generating some notable selling pressure as it is fast becoming apparent that the bulls don’t have the juice to breakout into the 1.30 – 1.35 band.

However, this structure isn’t the only thing likely to be weighing on the GBP as a number of instruments are also signalling that support is evaporating. For instance, the stochastics are undoubtedly in overbought territory which will surely be gearing the bears up for a comeback. Furthermore, the MACD oscillator is mid-signal line crossover which typically denotes a shift in trend direction.

If we do see the Cable make an about face and move into decline once again, we currently expect to see it fall back to around the 1.2667 handle. Here, support should prove to be rather robust as the 38.2% Fibonacci level and the 100 day EMA should work in concert to limit losses substantially. Also worth mentioning, this price coincides with a reoccurring reversal point which can only add to overall support around this level.

Ultimately, whilst we have taken a fairly technical view, don’t ignore the fundamentals entirely as they could still generate some intra-day volatility or muddle the decent back to support. This being said, both US and UK figures have been rather mixed recently which could mean they largely offset one another, leaving the pair especially open to technical influence.

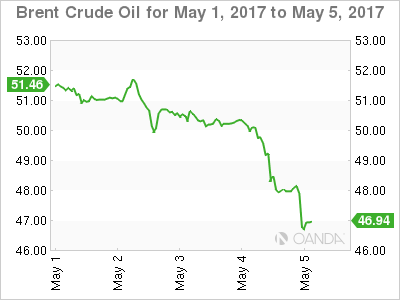

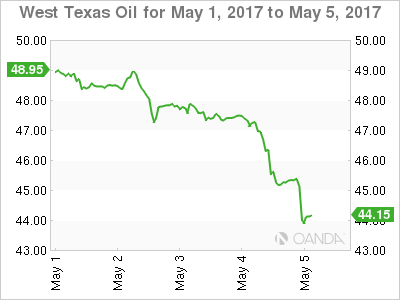

Oil Collapses In Asia As Commodity Rout Continues

Global commodities are routed overnight as China growth jitters and the spectre of higher U.S. rates saw long-term bullish positioning being pushed off the cliff. Oil, in particular, having fallen 5% overnight, has collapsed another 2% in Asian trading.

OIL

There was no light at the end of the tunnel for OPEC and Non-OPEC producers overnight, in fact, the light turned out to be the train coming the other way, as both Brent and WTI crashed just shy of 5 % in North American trade. As previously highlighted, OPEC has been looking down the barrel so to speak, of resurgent supply from Nigeria and Libya amongst OPEC and of course, American shale which combined have completely offset the 1.8 million barrel per day production cut agreement.

With commodities collapsing on China growth wobbles and the prospect of higher U.S. interest rates back on the table, it is evident that many long-term structural longs threw in the towel and headed for the door en masse overnight. OPEC will be faced with some stark choices going forward as the global supply glut clearly isn’t going to roll over and die anytime soon. The potential deflationary shock will be felt in the halls of power in Japan and Europe as well, where officials will be fretting about the collapse in oil and commodities undermining their inflation targeting.

Back to the here and now, we are in somewhat uncharted territory technically on both Brent and WTI, with both tanking in Asia by around 2% as I write. The move looks suspiciously stop loss driven as the overnight lows are taken out.

Brent spot opened at 48.10 this morning with resistance at 50.40 and 51.00. Support was at the overnight low at 47.80, but with this now well and truly gone there is nothing but clear air until 45.50 from a chart perspective.

WTI spot opened at 45.30 but has collapsed 2% as I write. Resistance at 47.00 and 48.00 seem to be distant memories now as upport initially at the overnight low at 45.10 and then 44.40 breaks. opening up a possible move to 42.00.

From a technical perspective, the break of 44.40 now opens up the possibility of a move to the 42.00 region.

PRECIOUS METALS

GOLD

The reverse alchemy in the precious metals markets continued overnight, as they looked more leaden than golden with gold itself off another 1% in New York trade. To be fair, this wasn’t a bad result given the general carnage seen in the commodity space overall. Potential China growth wobbles and the uncomfortable reality of higher U.S. interest rates being put back on the table by this week’s FOMC sees the safe haven unwind in gold continue to gather momentum.

The recent day’s price action could be implying that there are a lot of structural longs in gold that had been put on in the last months, at what are not very unattractive levels. Suggesting that, like crude oil, overnight, there may be more pain ahead.

Gold trades at 1228.30 in early Asia having fallen to 1225.50 overnight and this represents initial intra-day support. Key support lies just below at 1221.00 the 100-day moving average, with a close under there suggesting a move to the 1195/1200 region.

Resistance is at 1240 initially, the breakdown level and now a major daily pivot point. Above here the 200-day moving average at 1251.75 and the 1260 form resistance.

RBA Upbeat On Long-Term Outlook, Warns That Low Wages A Risk To The Economy

For the 24 hours to 23:00 GMT, the AUD declined 0.24% against the USD and closed at 0.7408.

LME Copper prices declined 1.7% or $93.5/MT to $5543.0/MT. Aluminium prices declined 0.3% or $6.5/MT to $1909.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.739, with the AUD trading 0.24% lower against the USD from yesterday's close.

Earlier in the session, the Reserve Bank of Australia (RBA), in its quarterly statement on monetary policy, forecasted that Australian economy would grow between 2.75% to 3.75% in 2018, up from its previous prediction of 2.5% to 3.5%. The central bank further warned that slow wage growth looks set to continue for Australian workers and remains a potential drag on the economy and that it had no plan to shift the cash rate from a record low of 1.5% for the rest of 2017.

Overnight data indicated that Australia's AIG performance of construction index advanced to a level of 51.9 in April, after registering a reading of 51.2 in the previous month.

The pair is expected to find support at 0.7371, and a fall through could take it to the next support level of 0.7352. The pair is expected to find its first resistance at 0.7417, and a rise through could take it to the next resistance level of 0.7444.

Moving ahead, Australia's building approvals, NAB business confidence, retail sales and Westpac consumer confidence data, all slated to release next week, will be on investors radar.

The currency pair is trading below its 20 Hr and 50 Hr moving averages

Euro-Zone’s Services Sector Expanded To A 6-Year High Level In April

For the 24 hours to 23:00 GMT, the EUR rose 0.84% against the USD and closed at 1.0980, amid expectations that the centrist candidate, Emmanuel Macron, will win the second and final round of French presidential election, scheduled on Sunday.

Euro added to gains following the release of upbeat services sector data in the Euro-zone. The final Markit services PMI in the Euro-zone was revised higher to a level of 56.4 in April, from a flash estimate of 56.2, maintaining its six-year high level, thus indicating that the regional economy is off to a strong start in the second quarter. The PMI had recorded a level of 56.0 in the previous month. Additionally, the region's seasonally adjusted retail sales advanced more-than-expected by 0.3% MoM in March, compared to a revised rise of 0.5% in the previous month, while markets expected for a gain of 0.1%.

Separately, growth in Germany's services sector fell less than initially estimated to a level of 55.4 in April, compared to a drop to a level of 54.7 registered in the preliminary print. In the previous month, the PMI had recorded a reading of 55.6.

Macroeconomic data released in the US showed that the number of Americans filing for fresh jobless claims fell to a three-week low level of 238.0K in the week ended 29 April 2017 and higher than market consensus for a drop to a level of 248.0K. In the previous week, initial jobless claims had recorded a level of 257.0K. Additionally, the nation's trade deficit surprisingly narrowed to a level of $43.7 billion in March, compared to a revised deficit of $43.8 billion in the prior month, while market participants had envisaged the nation's deficit to widen to a level of $44.5 billion. Moreover, the nation's factory orders rose less-than-anticipated by 0.2% MoM in March, compared to a revised rise of 1.2% in the prior month. Markets were anticipating factory orders to rise 0.4%. Further, the nation's final durable goods orders climbed 0.9% in March, advancing for the third consecutive month, compared to a revised rise of 2.3% in the prior month. The preliminary figures had indicated a rise of 0.7%.

In the Asian session, at GMT0300, the pair is trading at 1.0976, with the EUR trading slightly lower against the USD from yesterday's close.

The pair is expected to find support at 1.0903, and a fall through could take it to the next support level of 1.0830. The pair is expected to find its first resistance at 1.1019, and a rise through could take it to the next resistance level of 1.1062.

Going ahead, market participants await the release of the European Commission's economic growth forecasts report along with Germany's construction PMI data for April, slated to release in a few hours. Additionally, in the US, crucial non-farm payrolls and unemployment report, both for April, slated to release later in the day, will garner significant amount of market attention.

The currency pair is trading/showing convergence with its 20 Hr and 50 Hr moving average.

UK’s Services Sector Unexpectedly Expanded To A 4-Month High Level In April

For the 24 hours to 23:00 GMT, the GBP rose 0.41% against the USD and closed at 1.2921, after data showed a robust performance in UK's services sector.

UK's Markit services PMI unexpectedly advanced to a four-month high level of 55.8 in April, suggesting that the economy is regaining momentum after a lacklustre performance in first quarter. The PMI had registered a level of 55.0 in the prior month, whereas markets expected for a fall to a level of 54.5.

Moreover, the nation's net consumer credit advanced £1.6 billion in March, surpassing market consensus for a rise of £1.2 billion. In the prior month, net consumer credit had climbed by a revised £1.5 billion.

On the other hand, the nation's number of mortgage approvals for house purchases declined more-than-anticipated to a level of 66.8K in March, hitting its lowest level in six months. In the prior month, mortgage approvals had recorded a revised level of 67.9K.

In the Asian session, at GMT0300, the pair is trading at 1.2913, with the GBP trading 0.06% lower against the USD from yesterday's close.

The pair is expected to find support at 1.2851, and a fall through could take it to the next support level of 1.2790. The pair is expected to find its first resistance at 1.2952, and a rise through could take it to the next resistance level of 1.2992.

With no economic releases in UK today, market participants will anxiously await BoE's interest rate decision, scheduled next week. Also, investors will look forward to Britain's industrial and manufacturing production along with the nation's construction output, NIESR GDP estimate and trade balance data, all set to release next week.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Japanese Yen Trading A Tad Lower In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.16% against the JPY and closed at 112.50.

In the Asian session, at GMT0300, the pair is trading at 112.56, with the USD trading marginally higher against the JPY from yesterday’s close.

The pair is expected to find support at 112.22, and a fall through could take it to the next support level of 111.88. The pair is expected to find its first resistance at 112.97, and a rise through could take it to the next resistance level of 113.38.

Amid a public holiday in Japan today, trading trend in the JPY is expected to be determined by global macroeconomic events.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Swiss SECO Consumer Sentiment Surprisingly Fell In April

For the 24 hours to 23:00 GMT, the USD declined 0.83% against the CHF and closed at 0.9859.

In economic news, Switzerland’s SECO consumer confidence index unexpectedly fell to a level of -8.0 in April, compared to a reading of -3.0 in January. Markets expected the index to climb to a level of 3.0.

In the Asian session, at GMT0300, the pair is trading at 0.9864, with the USD trading a tad higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9828, and a fall through could take it to the next support level of 0.9792. The pair is expected to find its first resistance at 0.9928, and a rise through could take it to the next resistance level of 0.9992.

Next week, market participants will closely monitor Switzerland’s unemployment rate and consumer price inflation data.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Canada’s Trade Deficit Sharply Narrowed In March

For the 24 hours to 23:00 GMT, the USD rose 0.16% against the CAD and closed at 1.3751.

On the macro front, Canada's international merchandise trade deficit narrowed more-than-anticipated to a level C$0.14 billion in March, amid a rise in exports. Markets expected the nation's international merchandise trade deficit to narrow to a level of C$1.0 billion, following a revised deficit of C$1.1 billion in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.3770, with the USD trading 0.14% higher against the CAD from yesterday's close.

The pair is expected to find support at 1.3720, and a fall through could take it to the next support level of 1.3670. The pair is expected to find its first resistance at 1.3797, and a rise through could take it to the next resistance level of 1.3824.

Ahead in the day, traders will focus on Canada's unemployment rate data for April, to gauge strength in the nation's labour market.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Elliott Wave View: NZDUSD Downside Resumes

Revised Elliott Wave view in NZDUSD suggests the decline from 3/21 high (0.709) is unfolding as a triple three Elliott Wave structure where Minute wave ((w)) ended at 0.6905, Minute wave ((x)) ended at 0.7053, Minute wave ((y)) ended at 0.6844 and Minute second wave ((x)) is proposed complete at 0.6968. Minute wave ((z)) is in progress and unfolding as a double three Elliott Wave structure where Minutte wave (w) ended at 0.6835 , and Minutte wave (x) is in progress to correct cycle from 5/2 high before pair resumes lower again. We don’t like buying the pair and expect bounces in Minutte wave (x) to find sellers in 3, 7, or 11 swing for more downside provided that pivot at 0.6968 high remains intact.

NZDUSD 1 Hour Elliott Wave Chart

Market Morning Briefing: Dollar Has Reversed Its Gains Ahead Of The US Jobs Data Tonight

STOCKS

Dow (20951.47, -0.03%) closed lower and lack of any directional momentum just now is keeping the price stable. While below 21000, we could expect a test of 20800-20600 levels before again starting to rise from there.

Dax (12647.78, +0.96%) has broken the resistance on the daily candle charts but looking at the 3-day and weekly charts, the index is at crucial resistance levels and if it breaks on the upside, further rally towards 12750 and higher is possible. Else a corrective dip from current levels could be expected.

Shanghai (3098.24, -0.93%) has just broken below 3100 and may re-test 3075. A break below 3075 could be an important cue to initiate a fresh fall else a sharp bounce from 3075 is needed to take it towards 3150/75 and higher.

Nifty (9359.90, +0.51%) has been moving in line with expectation. Important resistance at 9400 remains intact and could hold in the medium term.

COMMODITIES

Gold (1228) had failed to close above 1239 levels and moved lower against our expectation. It is hovering around its crucial support of 1228. A close below 1228could open up 1188 levels as well. The bias would remain bearish while it is trading below 1256 levels. The scrip id highly oversold in near term time frame thus a possibility of a corrective bounce towards 1240-50 can’t be ruled out.

Similar kind of chart has been formed in silver (16.32) also as it is trading below 16.94 levels. The bias will remain bearish while it is trading below 17.50 levels though a possibility of a rise towards 17 levels can’t be ruled out due to short term oversold condition.

Copper (2.50) is hovering around its crucial support at 2.50 levels, within its trading range of 2.45-2.54. A close below 2.50, which is less preferred, could open up 2.45 levels as well.

WTI (45.41) had moved lower in line with our expectation and hovering around its support at 45.35 levels. A close below that could open up 44.58 and 41.62 levels respectively. Brent (51.73) may consolidate within 50-52 levels for few more sessions though the possibility of a corrective bounce towards resistance can’t be ruled out. We will remain bearish while Brent and WTI are trading below 53 and 51 levels respectively.

FOREX

Dollar has reversed its gains ahead of the US Jobs data tonight and the second round of French election on Sunday but the major trend is still not clear at the moment. By Monday, clarity can be expected.

Dollar Index (98.82) has lost all its gains made in the previous session after its failure to rise above the resistance of 99.50 we have been watching for the last week. Immediate support comes at 98.50 below which comes the major support of 98.30-20 which may hold on the first testing.

Euro (1.00980) has risen sharply as it tests the resistance zone of 1.0970-1.1000 now. A break above 1.10 may open up much higher levels starting with 1.1100 but we would prefer to wait for the breakout to take place first.

Dollar Yen (112.58) is stalling near the resistance of 113.00 as expected but it is not clear yet if the resistance will be able to reject the price sharply enough to trigger any considerable correction. Wait and watch for another couple of sessions.

Pound (1.2918) has bounced back exactly from our support of 1.2830 and our immediate target of 1.3000 may be met in the next 1-3 sessions.

The crash in the commodities this week has hit Aussie (0.7388) hard. The currency is testing the support of 0.7380-70 repeatedly for the last 2 sessions which must be protected by the bulls for any immediate chance of recovery. Failure to hold 0.7370 may open up much lower levels of 0.7300 but the chances of a bounce back can’t be fully discarded yet.

It has been one of the quietest days for Dollar Rupee (64.1750) in the recent weeks as it barely moved away from 64.20 in the entire session. On the other hand, this crash in volatility implies a sharp move coming in the next 2-4 sessions and the direction can be down if the pair fails to rise above 64.40 in the meanwhile.

INTEREST RATES

The Japan-US 10Yr (2.34%) is rising as expected and could heads towards 2.4% in the coming sessions. In that case we could expect a rise in Nikkei an d Dollar Yen too in the near term.

The German-US 10Yr (-1.97%) and the 2yr (-2.01%) have bounced from immediate support levels and have decent potential on the upside. While the yield spread looks bullish, Euro could head higher in the near term.

The US and the UK yields are rising and could move up for the next 2-sessions while the Japan yields are almost stable. The German yields have also moved up sharply and are heading immediate resistance levels from where a rejection is possible.