Sample Category Title

European Open Briefing: Asian Stock Markets Were Mixed

Global Markets:

- Asian stock markets: Nikkei gained 0.70 %, Shanghai Composite fell 0.25 %, Hang Seng rose 0.30 %, ASX 200 lost 0.60 %

- Commodities: Gold at $1258 (+0.20 %), Silver at $16.97 (+0.80 %), WTI Oil at $48.75 (-0.20 %), Brent Oil at $51.50 (-0.10 %)

- Rates: US 10-year yield at 2.32, UK 10-year yield at 1.09, German 10-year yield at 0.32

News & Data

- Japanese Nikkei Services PMI Apr: 52.2 (prev 52.9)

- Japanese Nikkei Composite PMI Apr: 52.9 (prev 52.9)

- Australia ANZ Roy Morgan Consumer Confidence 30-Apr: 111.3 (prev 111.2)

- South Korean CPI (MoM) Apr: -0.1% (exp 0.1%; prev 0.0%)

- South Korean CPI (YoY) Apr: 1.9% (exp 2.1%; prev 2.2%)

- South Korean Nikkei Manufacturing PMI Apr: 49.4 (prev 48.4)

- PBoC Fixes USDCNY Reference Rate At 6.8956 (prev fix 6.8931 prev close 6.8970)

Markets Update:

Asian stock markets were mixed. A weak Chinese manufacturing PMI release put Chinese markets under pressure. The ASX 200 declined as well. Meanwhile, the Nikkei and Hang Seng Index managed to close the day with a gain.

EUR/USD is still consolidating. Flows were light yesterday, as most of European markets were closed for a public holiday. Volatility is likely to pick up again today, and there is a fair number of data releases as well. Key support is noted at 1.0780, while resistance is seen at 1.0950 and 1.10.

Similar price action was seen in GBP/USD, which consolidated between 1.2880 and 1.2910. The outlook for the pair is still positive, and a test of 1.30 seems likely in the near-term. Meanwhile, USD/JPY remains bid. It is approaching 112, and there is a key resistance level around 112.20. A break above would signal that the pair could reach 113 quickly.

Upcoming Events:

- 08:45 GMT – Italian Manufacturing PMI

- 08:50 GMT – French Manufacturing PMI

- 08:55 GMT – German Manufacturing PMI

- 09:00 GMT – Euro Zone Manufacturing PMI

- 09:30 GMT – UK Manufacturing PMI

Market Update – Asian Session: China Caixin Manufacturing PMI Echoes Slowdown Of Official Prints

Asia Mid-Session Market Update: China Caixin Manufacturing PMI echoes slowdown of official prints; RBA on hold with a more upbeat tone

US Session Highlights

Blue chips slowed down today, with the Dow posting a small loss, while the broader stock market continued its rally. A possible US government shutdown seems averted, with more talk of a vote by this week on a new healthcare bill. Despite some weaker than expected economic data, investors returned to risky assets in particular techs. Apple rose more than 2%, helping propel the NASDAQ to a new high just short of 6,100. Congress and the White House averted a government shutdown by agreeing to a bipartisan federal funding bill of around $1T over the weekend. The deal should be voted through by end of the week and would include an increase in defense and homeland security spending. UK PM May said today that the UK would not agree to any Brexit bill without having an agreement on trade post-Brexit first. Her words come after various EU officials have stated there will be no post-Brexit negotiations until the conditions of UK's exit from the union have reached an advanced stage.

US markets on close: Dow -0.1%, S&P500 +0.2%, Nasdaq +0.7%

Best Sector in S&P500: Technology

Worst Sector in S&P500: Telecommunications

Biggest gainers: MAC +3.6%; LRCX +3.0%; ALXN +2.9%

Biggest losers: AMG -5.9%; NWL -3.6%; BBBY -3.4%

At the close: VIX 10.11 (-7bps); Treasuries: 2-yr 1.28% (-0.4bps), 10-yr 2.32% (-0.4bps), 30-yr 3.01% (-0.4bps)

US movers afterhours

ANGI: IAC's HomeAdvisor confirms to combine with Angie's List; shareholders can elect to receive one ANGI Homeservices share or $8.50/shr in cash; +41.4% afterhours

LMNX: Reports Q1 $0.28 v $0.08e, R$77.8M v $74.0Me; Guides Q2 Rev $74-79M v $75.3Me; +16.2% afterhours

THC: Reports Q1 -$0.52 v -$0.53e, R$4.81B v $4.85Be; announces agreement with Humana- Guides Q2 -$0.20 to -$0.10 v -$0.05e, R$4.85-5.05B v $4.89Be, adj EBITDA $550-600M; +13.7% afterhours

APTS: Reports Q1 FFO $0.36 v $0.34e, R$66.6M v $55.5Me; affirms FY17 FFO $1.40-1.48 v $1.47e, R$285-315M v $234Me (prior $1.40-1.48 v $1.48e; +7.9% afterhours

CYH: Reports Q1 $0.08 v $0.06e, R$4.49B v $4.34Be; +3.4% afterhours

AMD: Reports Q1 -$0.04 v -$0.05e, R$984M v $983Me; -11.2% afterhours

Key economic data

(CN) CHINA APR CAIXIN PMI MANUFACTURING: 50.3 V 51.3E; 7-month low; 10th straight month of expansion

(AU) RESERVE BANK OF AUSTRALIA (RBA) LEAVES CASH RATE TARGET UNCHANGED AT 1.50% (AS EXPECTED)

(JP) JAPAN APR SERVICES PMI: 52.2 V 52.9 PRIOR; COMPOSITE PMI: 52.9 PRIOR

(JP) JAPAN APR MONETARY BASE Y/Y: 19.8% V 20.3% PRIOR; MONETARY BASE END OF PERIOD: ¥462.2T V ¥447.3T PRIOR

(JP) Bank of Japan (BOJ) March 15th Policy Meeting Minutes: Members agreed to closely examine consumer price trend

(KR) SOUTH KOREA APR CPI M/M: -0.1% V 0.1%E; Y/Y: 1.9% V 2.1%E; CORE Y/Y: 1.3% V 1.3%E

(KR) SOUTH KOREA APR PMI MANUFACTURING: 49.4 V 48.4 PRIOR

Asia Session Notable Observations, Speakers and Press

Asian equity markets traded mixed, tracking US indices. Kospi was among the top performers rising to record highs, while Australia saw declines on weakness in energy and metals stocks. Crude oil prices faltered overnight with Libya disclosing higher production and Kuwait also forecasting increased output in the medium term. In FX, dollar majors traded in narrow rangers. AUD/USD was most volatile, sliding after a disappointing China Caixin Manufacturing PMI before lifting to its highs after an upbeat RBA policy statement.

China Caixin Manuf PMI came in below estimates at 50.3 V 51.3E, which was also its 7-month low. Slower increases in output and new orders were attributed to the decline, along with softer growth in new orders that forced manufacturers to cut payrolls at the fastest pace since January. Slowing growth was also felt in the prices components as the rate of input price inflation softened to a seven-month low. Recall over the weekend, China official manufacturing and non-manufacturing PMIs also hit 6-month lows.

RBA decision saw rates remain at 1.50% as widely expected, but the policy statement was surprisingly more upbeat after last month's dour assessment of employment. RBA noted improvement in global growth boosting demand for Australian exports, noted employment was now a bit stronger, forecast growth reaching 3% level over next few years, and also anticipating further increase in underlying inflation. AUD/USD rose some 20pips on the RBA statement while the yield on Australia 3-year ticked up 1bps.

China

(CN) China foreign exchange trade system (CFETS): Started a trading platform for credit-default swaps today - Chinese press

(CN) Despite slowing profit growth among China's top banks in Q1, their NPL ratios have also trended down - Chinese press

(CN) China Securities Regulatory Commission (CSRC) approves IPO applications for 10 companies; Will be allowed to raise combined CNY5.8B - Chinese press

Japan

(JP) Japan Fin Min Aso: Output gap is improving; Jobless rate has fallen below 3% - press

(JP) Japan Center for Economic Research (JCER): Japan Mar GDP estimated at -1.3% m/m; First contraction in 3 months - Nikkei

Australia/New Zealand

(NZ) According to Realestate.co.nz, number of homes available for sale in Auckland has hit a 5-year high, even as many other regions see record lows - NZ press

Korea

(KR) Moody's: Geopolitical risk for Korea has broadened on rise in risk of conflict on Korean peninsula

(KR) China-Korea border town of Dandong said to be "urgently" recruiting Korean-Chinese interpreters in the event of "emergency situation" in North Korea - Korean press

(KR) Korea's Kospi rises over 1% above 2,225, above its record close

Asian Equity Indices/Futures (00:00ET)

Nikkei +0.7%, Hang Seng +0.3%, Shanghai Composite -0.2%, ASX200 -0.5%, Kospi +0.8%

Equity Futures: S&P500 -0.1%; Nasdaq flat, Dax +0.2%, FTSE100 +0.5%

FX ranges/Commodities/Fixed Income (00:00ET)

EUR 1.0895-1.0920; JPY 111.75-112.00; AUD 0.7520-0.7550; NZD 0.6900-0.6935

June Gold +0.2% at 1,258/oz; June Crude Oil -0.2% at $48.75/brl; July Copper -1.2% at $2.63/lb

SLV iShares Silver Trust ETF daily holdings rise to 10,308 tonnes from 10,1273 tonnes prior

(CN) PBOC SETS YUAN MID POINT AT 6.8956V 6.8931 PRIOR; Weakest Yuan fix since Apr 11th

(CN) PBOC skips open market operations v injection CNY80B prior in 7-day, 14-day and 28-day reverse repos; First skip after 9 straight injections; Drains net CNY70B

Asia equities notable movers

Yamaha, 7951.JP, +16%, earnings

Belle International Holdings, 1880.HK, +15.6%, privatization

BYD, 285.HK, +8.4%, earnings

Hyundai Motor, 005380.KR, +4.9%, broker note

Japan Display, 6740.JP, -5.7%, revises outlook

KEPCO, 052690.KR, -3.8%, earnings

Pilbara Minerals, PLS.AU, +16.9%, signs financing agreement

MG Unit, MGC.AU, -12.1%, trading update

Woolworths WOW.AU +1.2%, Reports Q3

ANZ ANZ.AU -2.2%, Reports H1

China’s Caixin Manufacturing PMI Fell To 50.3 In April From 51.3 – The Lowest Level Since September 2016

Market movers today

Emmanuel Macron is still leading comfortably in the opinion polls ahead of the second round of the French election and the market looks priced for his victory. Nevertheless, the market will continue to monitor whether Marine Le Pen can manage a last minute run.

Markets will keep a close watch should more details surface about a potential upcoming plan on US infrastructure spending and tax reform today.

The OPEC meeting is now only about three weeks away and the cartel is said to aim for consensus about a strategy on crude production before the meeting. The oil market in particular will monitor potential comments from OPEC today.

Final euro area PMI manufacturing indices and UK, Norway and Sweden PMI manufacturing indices are due for publication this morning.

In Denmark, currency reserves data is due for publication today. The krone strengthened against the euro at the beginning of April but not to the same extent as in February and March, when it triggered intervention by the central bank. Therefore, Danmarks Nationalbank probably stayed on the sidelines in April.

Selected market news

China's Caixin manufacturing PMI fell to 50.3 in April from 51.3 – the lowest level since September 2016. Along with US ISM manufacturing, which fell to 54.8 in April from 57.2 in March, it supports our view that the industrial cycle in the US has peaked. While the news out of China has weighed a bit on the price of LME copper overnight , it is not enough to mitigate the positive impulse of the news from yesterday (cf. below) that a plan on infrastructure spending in the US may be on its way.

In an interview yesterday, former Fed chairman Ben Bernanke said that the Fed is probably aiming for a balance sheet of USD2.3-2.8trn from the current level of around USD4.5trn. We expect the Fed to announce further details on its plan to reduce its balance sheet at the June meeting.

There were two important pieces of news from the White House yesterday. Reince Priebus (White House Chief of Staff) said in a CBS interview that he expects a health bill to pass the House of Representatives this week. He added, ‘I think we'll have tax reform by the end of the year'. President Trump said in an interview with CBS that an infrastructure plan is set to be released in two to three weeks' time. However, it is likely to be even more difficult for Trump to pass his infrastructure plan than his tax reform.

Daily Technical Analysis: GBP/USD Triangle Chart Pattern Emerges Around 1.29

Currency pair GBP/USD

The GBP/USD is building a trend channel (red/green) within wave C (orange). A bounce at the support trend line (green) could see price continue towards the Fibonacci targets of wave 5 (purple) whereas a break below support (green) could see price correct back to the previous support (blue).

The GBP/USD has retraced back to the 50% Fibonacci level of wave 4 (pink), which could be confirmed if price breaks above resistance (red) and invalidated if price breaks below the 61.8% Fibonacci level.

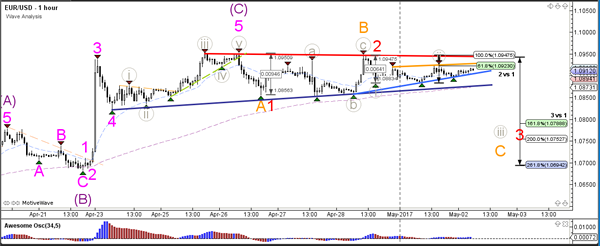

Currency pair EUR/USD

The EUR/USD is in a consolidation pattern which is best indicated by the support (blue) and resistance (red) trend lines. A bullish break above resistance (red) would indicate a potential uptrend continuation towards the 78.6% Fibonacci level of wave 2 (green) whereas a bearish break could start a reversal and indicate the completion of the ABC zigzag (purple).

The EUR/USD reversal or retracement pattern is invalidated if price manages to break above the resistance trend lines (red/orange). A larger reversal or correction could take place if price breaks below the support trend lines (blue).

Currency pair USD/JPY

The USD/JPY has completed the wave 4 (brown) correction at the support trend line (green) and is now continuing towards the Fibonacci targets of wave 5 (brown).

The USD/JPY broke the contracting triangle (dotted red) chart pattern and a bullish breakout is developing within a wave 5 (brown). A new resistance level (red) needs to be broken before the wave 5 (brown) can continue.

Reversal Could Be On The Way For A Volatile AUD

Key Points:

- Consolidating wedge shaping up.

- Most technical readings hinting at a reversal.

- Losses could see the pair retreat to last week's lows.

The Aussie Dollar has been extremely volatile recently, experiencing large daily swings that now seem to be tracing out a falling wedge structure. As a result of this and a number of other technical readings, we could be about to encounter yet another acute rout for the pair which might see the prior week's lows challenged yet again. This being said, given the voracity of the prior two sessions' bullishness, it may be worth taking a closer look at exactly what technical readings are indicating that momentum has run dry before delving into where we can expect to see the pair plunge.

On that note, of the available indicators, the clearest case for a reversal is provided by the EMA bias. Specifically, not only are the 12, 20, and 100 day averages in the most bearish configuration possible but the 100 day measure is also well positioned to provide some dynamic resistance. If that wasn't reason alone to be suspicious of an imminent reversal, this zone of resistance is also in line with the 78.6% Fibonacci retracement which can only cap upside risks further.

Aside from the EMA's, the Parabolic SAR and the Bollinger bands provide additional evidence that we should see a reversal in fairly short order. Starting with the Parabolic SAR, the instrument is clearly bearish and in little danger of inverting any time soon. Indeed, it would require a breakout from the consolidating wedge structure to see this happen which is looking unlikely. This is primarily a result of the Bollinger bands which are fairly divergent, this typically being a signal that chances of a breakout are slim.

Due to the rather clear technical bias developing above, the question remains as to where we expect to see the Aussie Dollar tumble in the near-term. Luckily, we have some fairly strong zones of support on offer which provide a fair guideline. In particular, the 0.7442 level is looking rather robust due to it being a well-tested historical reversal point. However, the fact that this price also intersects with the downside of the wedge also signals that losses could be limited to around this level.

Ultimately, keep an eye on this pair as the technical forecast seems relatively robust even though we could see some notable volatility following the RBA and Fed interest rate announcements. Importantly, the technical bias could limit the upsides on offer and dramatically exacerbate any losses as a result of any unexpected changes to either the Australian Cash rate or the US FFR.

Cable Likely To Retain Its Bullish Disposition In The Days Ahead

Key Points:

- Price action likely to continue moving towards the 1.3184 target.

- Watch for volatility around the Fed's rate decision.

- A short period of moderation possible given RSI levels.

The Cable had a relatively positive week despite the fact that the UK Advance GDP figures slipped to 0.3% q/q. However, this was offset by a softer USD following the uptick in Unemployment Claims to 257k whilst the Core Durable Goods Orders fell into contraction at -0.2% m/m. Subsequently, the pair rose throughout most of last week to close at 1.2944 but it remains to be seen if the pair can retain its bullishness over the next few days. Subsequently, we review the salient events from last week and discuss some of the potential risks in the days ahead.

Last week proved relatively positive for the Cable despite the disappointing UK Advance GDP figures, which came in well below estimates at 0.3% q/q. This initially caused a small selloff but the pair quickly rebounded when the US Unemployment Claims surprisingly ticked higher to 257k whilst the Core Durable Goods Orders took a hit at -0.2% m/m. Subsequently, the Cable was fairly buoyant and rose to a high of 1.2964 before pulling back to close the week out at 1.2944.

Looking ahead, it's going to be an incredibly volatile week for the Cable with the UK Manufacturing, Construction, and Services PMI figures all due out over the next few days. Most of the market estimates provide for a relatively robust set of results and this is likely to provide some further follow through for the recent bullishness. However, watch out for plenty of volatility inducing events on the U.S. side of the fence with a critical Federal Reserve vote on rates, along with the NFP figures, due out. In particular, the FOMC vote is likely to be closely monitored and, although the central bank is unlikely to raise rates, could bring about plenty of volatility in the aftermath. In fact, Fed Chair Yellen's statement following the event is seen to be critical for the markets forward guidance.

From the technical perspective, the Cables recent rally suggests that the ongoing move back towards the medium term target at 1.3184 is still in play. However, the RSI Oscillator is now close to overbought levels and we could be facing a short term period of moderation. Regardless, price action still retains its position well above the 100 day MA which is why out initial bias remains bullish for the week ahead. Support is currently in place for the pair at 1.2754, 1.2625, and 1.2547. Resistance exists on the upside at 1.2965, 1.3121, and 1.3335.

Ultimately, the Cable is likely to retain its bullish disposition for the remainder of the week as long as it can hold above the key 1.2878 mark. However, it's highly likely that it will suffer from some sharp volatility with both the Fed's FOMC decision and the NFP results and this could cause a temporary cessation to the rally. Subsequently, consider your positioning ahead of these risk events but expect the pair to return to an upward trajectory in short order following any swings.

RBA Keeps Interest Rate On Hold

For the 24 hours to 23:00 GMT, the AUD rose 0.67% against the USD and closed at 0.7526.

Over the weekend, data revealed that Australia's AIG performance of manufacturing index advanced to a level of 59.2 in April, compared to a reading of 57.5 in the previous month.

Separately, in China, Australia's largest trading partner, the NBS manufacturing PMI eased to a level of 51.2 in April, compared to a level of 51.8 in the previous month. Moreover, the nation's NBS non-manufacturing PMI declined to a level of 54.0 in April, compared to a level of 55.1 in the prior month.

LME Copper prices rose 0.04% or $2.0/MT to $5688.5/MT. Aluminium prices declined 1.3% or $24.5/MT to $1930.0/MT.

Earlier in the session, the Reserve Bank of Australia (RBA), at its latest monetary policy meeting, opted to leave the official cash rate on hold at its historic low of 1.50%, as widely expected. The RBA Governor, Philip Lowe repeated Australia's housing market concerns, stating that housing prices continue to vary considerably around the country.

Elsewhere, China's Caixin/Markit manufacturing PMI index registered an unexpected drop to a level of 50.3 in April, confounding market expectations of a rise to a level of 51.3. The PMI had recorded a level of 51.2 in the previous month.

In the Asian session, at GMT0300, the pair is trading at 0.7540, with the AUD trading 0.19% higher against the USD from yesterday's close.

The pair is expected to find support at 0.7495, and a fall through could take it to the next support level of 0.7449. The pair is expected to find its first resistance at 0.7567, and a rise through could take it to the next resistance level of 0.7593.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Euro Trading A Tad Higher, Ahead Of The Euro-Zone’s Unemployment Rate Data

For the 24 hours to 23:00 GMT, the EUR rose 0.15% against the USD and closed at 1.0909.

On Friday, data indicated that the Euro-zone's flash consumer price index (CPI) climbed more-than-anticipated by 1.9% on an annual basis in April, jumping back to the European Central Bank's (ECB) target of just below 2.0%. Markets expected the CPI to advance 1.8%, following a rise of 1.5% in the prior month.

Separately, Germany's retail sales unexpectedly climbed 0.1% MoM in March, compared to a revised advance of 1.1% in the previous month, while market participants envisaged for a flat reading.

Macroeconomic data released in the US indicated that the ISM manufacturing activity index dropped more-than-expected to a level of 54.8 in April, expanding at its weakest pace in four months, thus adding to the narrative of a slowdown in the nation's economic momentum. Markets were expecting the index to ease to a level of 56.5, compared to a level of 57.2 recorded in the previous month. Moreover, the nation's construction spending unexpectedly eased 0.2% on a monthly basis in March, defying investor consensus for a gain of 0.4% and after recording a revised advance of 1.8% in the previous month. Also, the nation's final Markit manufacturing PMI declined to a level of 52.8 in April, confirming the preliminary print and compared to a level of 53.3 in the previous month.

In other economic news, the nation's personal spending remained flat for a second straight month in March, confounding market expectations for a rise of 0.2%. In the prior month, personal spending had registered a revised flat reading. On the contrary, the nation's personal income gained 0.2% in March, falling short of market expectations for a rise of 0.3%. In the prior month, personal income had recorded a revised rise of 0.3%.

On Friday, the preliminary gross domestic product (GDP) data revealed that the US annualised GDP growth expanded 0.7% on a quarterly basis in the first quarter of 2017, growing at its weakest pace in 3 years, as consumers pulled back sharply on spending. The nation's GDP grew 2.1% in the prior quarter, whereas market expected for an expansion of 1.0%. Moreover, the nation's final Reuters/Michigan consumer sentiment index rose less-than-expected to a level of 97.0 in April, compared to a preliminary print of 98.0 and after registering a reading of 96.9 in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.0911, with the EUR trading slightly higher against the USD from yesterday's close.

The pair is expected to find support at 1.0888, and a fall through could take it to the next support level of 1.0864. The pair is expected to find its first resistance at 1.0929, and a rise through could take it to the next resistance level of 1.0946.

Going ahead, investors will look forward to the final Markit manufacturing PMI for April across the Euro-zone along with the Euro-zone's unemployment rate data for March, slated to release in a few hours.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average

GBP/USD: UK’s Economic Growth Sharply Slowed In The First Quarter Of 2017

For the 24 hours to 23:00 GMT, the GBP declined 0.11% against the USD and closed at 1.2897.

On Friday, data indicated that UK's flash gross domestic product (GDP) climbed 0.3% QoQ in the first three months of 2017, expanding at its slowest pace in twelve months, as a spike in inflation continued to weigh on household incomes. The nation's GDP advanced 0.7% in the previous quarter, whereas markets anticipated for an advance of 0.4%. Meanwhile, the nation's BBA mortgage approvals fell to a level of 41.1K in March, compared to a revised level of 42.3K in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.2906, with the GBP trading 0.07% higher against the USD from yesterday's close.

The pair is expected to find support at 1.2877, and a fall through could take it to the next support level of 1.2847. The pair is expected to find its first resistance at 1.2936, and a rise through could take it to the next resistance level of 1.2965.

Trading trends in the pair today is expected to be determined by the release of Britain's Markit manufacturing PMI for April, slated to release in a few hours.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Members Agreed To Closely Monitor Japan’s Inflation: BoJ Minutes

For the 24 hours to 23:00 GMT, the USD rose 0.15% against the JPY and closed at 111.85.

In the Asian session, at GMT0300, the pair is trading at 111.84, with the USD trading slightly lower against the JPY from yesterday's close.

Earlier today, minutes of the Bank of Japan's (BoJ) March monetary policy meeting showed that policymakers agreed to keep a close watch on consumer prices. Further, they indicated that tighter labour conditions and rebounding energy prices are having a short-term effect on consumer prices.

On the data front, Japan's Nikkei services PMI fell to a level of 52.2 in April, compared to a reading of 52.9 in the prior month.

The pair is expected to find support at 111.50, and a fall through could take it to the next support level of 111.17. The pair is expected to find its first resistance at 112.07, and a rise through could take it to the next resistance level of 112.31.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.