Sample Category Title

Trade Idea: EUR/GBP – Sell at 0.8620

EUR/GBP - 0.8571

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term down

Original strategy :

Sell at 0.8620, Target: 0.8520, Stop: 0.8660

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.8620, Target: 0.8520, Stop: 0.8660

Position : -

Target : -

Stop : -

As the single currency has rebounded again after finding support at 0.8511, retaining our view that further consolidation above last week’s low at 0.8485 would be seen and another bounce to 0.8590-00 cannot be ruled out, however, renewed selling interest should emerge around 0.8620-25, bring another decline later, below said support at 0.8511 would bring test of 0.8485, break there would add credence to our view that top has been formed at 0.8788 and bearishness remains for this fall from there to bring retracement of early upmove, hence further weakness to 0.8470 would be seen but oversold condition should prevent sharp fall below 0.8450.

In view of this, we are looking to sell euro on recovery as 0.8620-25 should limit upside. Only above 0.8660-65 would defer and suggest low is possibly formed, risk rebound to 0.8680, then 0.8700 but price should falter below said resistance at 0.8735, bring further choppy trading later.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

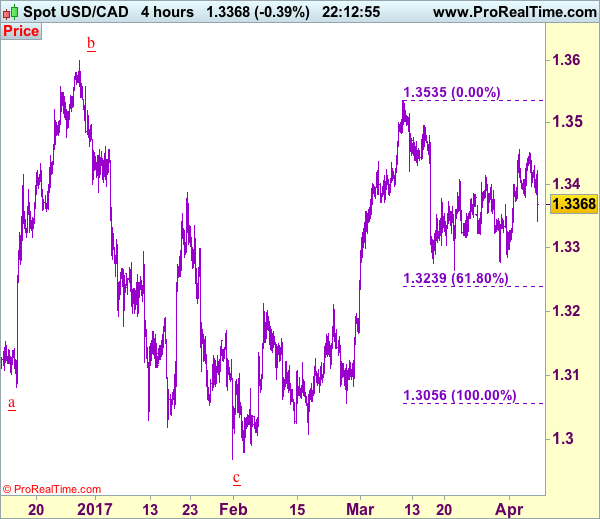

Trade Idea: USD/CAD – Exit long entered at 1.3375

USD/CAD - 1.3375

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term up

Original strategy :

Bought at 1.3375, Target: 1.3550, Stop: 1.3315

Position: - Long at 1.3375

Target: - 1.3550

Stop: - 1.3315

New strategy :

Exit long entered at 1.3375

Position: - Long at 1.3375

Target: -

Stop:-

As the greenback has slipped again in US morning in part due to the release of soft US NFP data, suggesting top has possibly been formed at 1.3456 earlier this week and downside risk has increased for weakness to 1.3310-20, however, break of 1.3277 support is needed to signal another leg of decline from 1.3535 top is underway for test of 1.3264, below there would add credence to this view and extend weakness to 1.3235-40 (61.8% Fibonacci retracement of 1.3056-1.3535) and then 1.3200-10.

In view of this, would be prudent to exit long entered at 1.3375 and stand aside for now. Above 1.3430-35 would revive bullishness and bring retest of 1.3456 resistance, break there would add credence to our view that the correction from 1.3535 has ended and bring further gain to 1.3495-00 but break there is needed to signal upmove has resumed for retest of 1.3535, once this level is penetrated, this would extend recent recent upmove from 1.2969 to 1.3575-80 but previous chart resistance at 1.3599 should hold on first testing.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

Elliott Wave Analysis: USDCHF Trading In Wave 1) As Part Of An Uptrend

On the updated chart of USDCHF, we see price undergoing a nice sharp and strong rally to the upside, probably as an indication for a low in place. If that is the case, then recent big three wave pattern to the downside is completed as a contra-trend move, therefore more gains may follow in days ahead. At the moment we see price trading in the first wave 1) that may find a potential top in sessions ahead and make a minimum three wave reversal to the downside for wave two. Possible support can then be around 0.9900.

USDCHF, 4H

Job Gains, Growth and Wage Fundamentals

Job gains were disappointing in March, primarily due to retail trade restructuring and some weather effects. Wage gains are consistent with labor productivity and inflation trends. FOMC on track for June.

Jobs Up 98,000 in March: One-off Weakness in 2017

Nonfarm payrolls rose a disappointing 98,000 in March, lowering the three-month average to 178,000 jobs. Over the past five years, there has been one month of weakness in jobs in the first quarter of the year, and three of those cases came in March.

Hiring in the services sector slowed sharply in March, with employers adding only 61,000 new positions-less than half the pace of the prior two months. Weakness was particularly noted in retail and likely reflects the impact of ongoing restructuring in that sector as well as difficulty adjusting for the timing of the Easter holiday. Retail has now been down sharply two months in a row.

In the goods sector, manufacturing employment posted another monthly gain (up 11,000), while mining employment continued its comeback as commodity prices have improved. Hiring in construction, however, was up just 6,000 jobs, likely reflecting some seasonal payback.

Wages: Not an Isolated Number but Part of the Economic System

Wages reflect the economic fundamentals of the labor market, and those fundamentals include productivity and inflation. Wages are not "low" arbitrarily as if some evil force keeps wages low.

As illustrated in the middle graph, wage growth tracks the trend in labor productivity growth and inflation over the past 50 years. This makes economic sense since nominal wage growth over the long-run should be the product of the growth in a worker's output per hour worked and the change in the price level. During the current cycle, analysts have repeatedly commented on low productivity, and inflation has been persistently below the FOMC's target of two percent. Moreover, nominal wage gains have also been real gains in several sectors such as information, manufacturing, wholesale trade and the private sector in general, where nominal wage growth has exceeded the pace of inflation as measured by the Fed's benchmark, the PCE deflator.

Rough Time to Be Part of the Establishment

Strength in the household survey in March suggests the payroll survey likely exaggerates any weakening in the labor market. The unemployment rate fell to a new cycle low of 4.5 percent. Encouragingly, the decline was driven entirely by more workers finding employment while the participation rate held steady. Broader measures of labor market slack also signaled that the labor market is tightening, with the U-6 unemployment rate, which includes people working part-time for economic reasons, falling to 8.9 percent. With the household survey failing to corroborate the weak payroll numbers, this report does not deter our current expectation for the Fed to hike again in June.

U.S. March Payroll Employment Moderates to 98K

Highlights:

- Payroll employment rose a smaller-than-expected 98K following gains of 219K and 216K in February and January, respectively. Market expectations had been for a much stronger 180K increase. At the margin inclement weather is some regions may have had a dampening impact on hiring.

- The gain in service-producing jobs moderated to 61K from 125K in February while goods-producing employment gain dropped to 28K from February's outsized 96K jump. Government employment rose slightly by 9K which reversed a 2K decline in February.

- The separate, and more volatile, household employment survey tally indicated a more pronounced 472K surge in employment. With the household labour force only up 145K, the unemployment rate sank to 4.5% from February's 4.7%. Market expectations had been for this rate to remain unchanged at 4.7%.

- Average hourly earnings, the main wage measure in the report, rose 2.7% over the past year both in March and in the first quarter. This measure has been steadily increasing from 2.1% in 2014, 2.3% in 2015 and 2.6% in 2016.

Our Take:

The increase in payroll employment moderated significantly in March though such may indicate more U.S. labour markets approaching capacity limits rather than a sign of weakening in labour demand. Indications of tightening labour markets were clearly conveyed by the unemployment rate unexpectedly dropping by a significant 0.2 percentage points to 4.5%. As well, wage growth continues to trend higher. Though job growth may be moving towards a more moderate pace, higher wages should keep incomes rising to sustain GDP growth close to the economy's potential rate. Sustained above-potential growth was a factor that returned the Fed to tightening mode late last year. With the economy moving ever closer to capacity, policy will be more focused on pulling back on the unneeded liquidity in the system. This is expected to keep the central bank tightening going forward via raising fed funds along with a shrinking of the balance sheet. Our forecast assumes fed funds being hiked by 25 basis points two more times this year followed by four hikes in 2018 with this official rate finishing next year at 2.50%.

Canada’s Job Gains Beat Expectations Again!

Highlights:

- 19K jobs created in March and labour force rebounded sharply by 47K

- Unemployment rate increased to 6.7%

- Full-time jobs up 18K with 1K rise in part-time. In Q1 2017, 139K full-time positions were created

- Service sector employment fell 2K while goods producers created 22K positions as manufacturers added 24K workers

- The participation rate recovered to 65.9% backed by a 0.3ppt rise in participation by prime-aged workers

- Hours worked jumped 1.1% in March skating the year ago rate back into positive territory

- Wage growth remains disappointing, earnings for permanent workers up only 0.9% from year ago

Our Take:

The run of employment gains kept going in March with this morning's report showing 19.4K positions were added. That means 276K more people were working compared to a year earlier. This jibes with the strong acceleration in real GDP that started in the middle of 2016. Heading into next week's Bank of Canada meeting this data run gives the Bank a lot of think about. Real GDP is on track to beat the Bank's forecasts for a third consecutive quarter and the unemployment rate at 6.7% remains below the 10-year pre-recession average, a time when the economy was considered to be at full-employment. See our assessment of current conditions here.

To be sure, the weak wage growth suggests that there remains residual slack in the labour market. Hours worked also remained tepid as even with March's rebound hours stood 0.2% lower in the first quarter than a year earlier. We expect wages and hours worked will catch-up to the strong gains in employment and growth in the months ahead. We will watch closely to see how the Bank incorporates the data into their forecasts. The Governor's commentary last month hinted that he thinks it will take some time before the economy will reach full employment meaning rate hikes are unlikely to be on the table anytime soon.

Dollar Volatility Rekindled by Mixed Employment Report

The Greenback was explosively volatile during trading on Friday after March's mixed job report prompted investors to offload and reload Dollar positions in a fighting bid to be on the winning trade. Although the disappointing headline NFP figure was a tepid 98k in March, the jobless rate unexpectedly dropped to the lowest level in almost 10 years at 4.5%. With average earnings hitting the 0.2% expectations, it may be fair to say that the report was a mixed bag with a unique touch. The immediate market reaction has seen expectations rapidly diminish over the Federal Reserve raising rates in June with the probability dropping to 61%. Although the Dollar initially found itself exposed to downside shocks in the immediate aftermath of the release, prices have fully recovered with the Dollar Index trading towards 100.90 as of writing. While there is a possibility of the Dollar edging higher as bulls cheer the unexpected drop in unemployment rates, gains could be limited if the probability of the Federal Reserve hiking rates in June drops further. From a technical standpoint, a breakout above 101.00 on the Dollar Index could open a path higher towards 101.50.

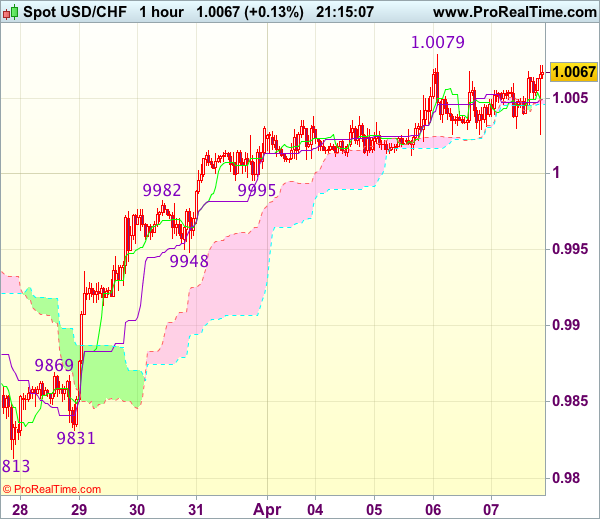

Trade Idea Update: USD/CHF – Buy at 0.9950

USD/CHF - 1.0065

Original strategy :

Buy at 0.9950, Target: 1.0050, Stop: 0.9915

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9950, Target: 1.0050, Stop: 0.9915

Position : -

Target : -

Stop : -

The greenback remained confined within near term established range and further sideways trading is in store before recent rise from last week’s low at 0.9813 resumes, above resistance at 1.0079 would extend further gain to previous resistance at 1.0109, however, loss of upward momentum should prevent sharp move beyond latter level and reckon 1.0140-50 would hold, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy dollar on pullback as support at 0.9948 should limit downside. Below 0.9925-30 would abort and signal top is formed instead, bring correction to 0.9905-10 but reckon previous resistance at 0.9869 would hold from here.

Weekly Focus: CPI Release ahead

Market movers ahead

- In the US, the coming week brings CPI figures for March. We forecast CPI core increased 2.3% y/y while headline likely increased 2.8% y/y, i.e. we expect to see the acceleration in inflation turn into deceleration. Note that while these numbers are well above 2%, the Fed is more concerned about PCE core inflation, which is still below 2%.

- The coming weeks also bring a few speeches by FOMC members, where the focus is on the Fed's intention to start quantitative tightening soon, see FOMC minutes: Quantitative tightening is moving closer, 5 April.

- In the euro area, the Sentix investor confidence and German ZEW expectations are due out next week.

- In the UK, the most important data release next week is the CPI inflation data for March. We expect total CPI rose 0.4% m/m in March implying an unchanged inflation rate at 2.3%. We still expect CPI inflation to move higher this year and to peak around 3%. Despite higher inflation, the Bank of England will likely remain on hold through the Brexit negotiations, see also Bank of England Review: Maintains neutral stance with hawkish twist, 16 March.

Global macro and market themes

- Mounting signs that the global business cycle is peaking.

- We expect a pause in the equity bull market and that risk factors move back to the fore.

- We still expect the bond bear market is over for now.

- Fading reflation supportive for the USD. We expect short-term USD strength but weakening longer term.

- Positive start to Trump-Xi meeting - but differences on trade will come into focus in H2.

Trade Idea Update: GBP/USD – Sell at 1.2450

GBP/USD - 1.2396

New strategy :

Sell at 1.2450, Target: 1.2350, Stop: 1.2485

Position : -

Target : -

Stop : -

As the British pound has dropped again and broke below indicated feel at 1.2400, adding credence to our view that rebound from 1.2377 has ended at 1.2559 and reset of this level would be seen, however, break there is needed to confirm early fall from 1.2616 has resumed for weakness to 1.2350, then towards 1.2325-30 but near term oversold condition should limit downside today and reckon 1.2300 would hold from here.

In view of this, would not chase this fall here and would be prudent to sell cable on recovery as 1.2450-60 should limit upside. Above 1.2480 would defer and suggest low is formed instead, risk test of resistance at 1.2506 first, break there would confirm, then a stronger rebound to 1.2525-30 would follow.