Sample Category Title

Hot U.S. Labor Market Cools Off in March

Non-farm payrolls increased by 98k in March, well below the consensus expectation of 180k. Downward revisions to the previous two months results in a cumulative 38k jobs vanishing from the statistics, but leaves job gains above 200k in both months.

Private payrolls rose 89k (consensus: 175k).The slowdown in private payroll employment was observed across both goods and service sectors, as well as in almost all broad industry categories. Private services hiring rose 61k, less than half the pace from the previous month. Still, hiring in the services sector was driven by business services (+56k), and health care & education (+16k). Goods hiring slowed materially as well, with manufacturing (+11k) and construction (+6k) recording much more subdued job gains after the strong showing at the start of the year. Government hiring (+9k) remained modest, with federal level hiring dropping by 1k.

Despite the unexpectedly weak payroll print, the household survey showed a strong change in employment of 472k, pushing the unemployment rate down by 0.2 percentage points to 4.5%. A smaller influx of people into the labor force helped keep the participation rate at 63.0% and unchanged on the month. Other underemployment measures were also lower, with the broadest measure (U-6) down 0.3pp to 8.9% - the lowest reading since December 2007.

Average hourly earnings rose by 0.2% during the month, matching consensus expectations. Moreover, wage growth for February was revised up slightly (+0.1 ppt) to 0.3% m/m. Year-over-year wage growth eased from 2.8% to 2.7% in March.

Average weekly hours were unchanged at 34.3.

Key Implications

Undoubtedly, the headline payrolls print was disappointing particularly when taken together with the strong reading from the huge ADP print mid-week (+263k) and the consensus expectation for a gain of 180k. However, there was a risk that today's print was set to disappoint as there were a number of temporary factors at play. For one, unusually warm weather in January and February likely helped pull forward activity in the construction sector. Furthermore, the snowstorm that hit much of the eastern U.S. during the survey reference week likely contributed to the disappointing payroll print.

But there are still some nuggets of good news tucked away in the details of this report. The household survey showed a reduction in all unemployment indicators, suggesting that labor market slack continues to be absorbed. Hourly wages advanced, while average hours remained broadly unchanged, all of which should help support consumer spending in the months ahead. Moreover, 98k jobs is likely just above trend employment growth for an economy that is operating near full employment. Overall, this report will is unlikely to change the Federal Reserve's calculus as they consider their next moves to tighten monetary policy.

Canada’s Streak of Job Gains Keeps Going

Canada kept churning out jobs in March, adding another 19.4k net new positions. More workers were drawn to labour markets, creating an uptick in the participation rate that left the unemployment rate 0.1 percentage point higher at 6.7%.

This fourth straight monthly gain in employment was matched with a fourth straight monthly gain in full-time employment, which was up 18.4k on net.

The relative outperformance of the private sector also continued, adding 13.7k net positions (vs a 12.7k decline in public sector employment). This marks the seventh month in a row of private sector outperformance. With the public-private employment split nearly even, the overall gains in employment were driven largely by self-employment, which rose 18.4k positions on net.

In a break from recent trends, it was the goods-producing sectors that led the way (+21.8k), with gains in manufacturing (+24.4k) and construction (+8.3k) offsetting modest declines elsewhere. On the service side, strong gains in business support services (+18.2k), trade (+16.9k), and information (+10.7) were offset by declines in education (-14.9k), transportation (-12.8k), and a number of other sectors, leaving overall employment in services down 2.4k on the month.

Looking across the country, Alberta led the way, adding 20k net positions, entirely in full-time work. Other provinces reported more mixed performances, with employment falling 11.2k positions in Ontario, and down 5.1k net positions in Saskatchewan.

Hours worked finally ticked back up in March, rising 0.7% year-on-year, halting a three-month decline. The recent soft trend in the hourly wage rate continued however, rising just 0.9% y/y - this measure has only averaged 1.0% growth year-on-year so far in 2017.

Key Implications

There is just no stopping Canadian jobs gains, which once again broke through market expectations. The recent trend of solid full-time employment gains, the turn-around in hours worked, and a seeming stabilization of the participation rate are all signs of a Canadian economy that has started 2017 on the right foot.

Once again, if there is a soft spot to be found, it has to be in the wage data, which is testing depths last seen in the late 1990s. It is difficult to square the soft wage data with the solid employment gains and generally robust economic indicators more broadly, while other data, including less-timely employer-based surveys, still point to healthy wage gains.

Heading into the Bank of Canada's Wednesday policy interest rate decision, the jobs data will likely have only a marginal impact. It is possible that Governor Poloz may point to the still-soft wage data to reinforce his recent dovish tone, but more likely is a continued focus on the sources of growth and the perceived differences in economic slack vis-à-vis the United States.

Trade Idea Update: EUR/USD – Sell at 1.0725

EUR/USD - 1.0620

Original strategy :

Sell at 1.0725, Target: 1.0610, Stop: 1.0760

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0725, Target: 1.0610, Stop: 1.0760

Position : -

Target : -

Stop : -

As the single currency has remained weak after recent selloff, adding credence to our bearish view that the decline from 1.0906 is still in progress for further weakness towards previous chart support at 1.0600, however, a sustained breach below the latter level is needed to retain downside bias for subsequent selloff to 1.0570-75 and possibly towards 1.0550.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 1.0720-30 should limit upside. Only a firm break above resistance at 1.0773 would suggest low is formed instead, bring a stronger rebound to 1.0800 but resistance at 1.0827 should remain intact.

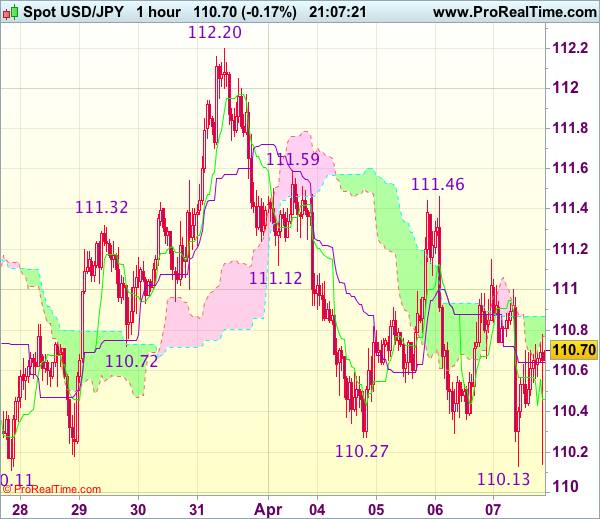

Trade Idea Update: USD/JPY – Stand aside

USD/JPY - 110.90

Original strategy :

Sell at 111.30, Target: 110.30, Stop: 111.65

Position : -

Target : -

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the the greenback slipped again in NY morning, as dollar has rebounded again after holding above indicated support at 110.11, retaining our view that further consolidation above this level would be seen and corrective bounce to 111.10-15 cannot be ruled out, however, reckon upside would be limited and resistance at 111.46 should remain intact, bring another decline later, below said support at 110.11-13 would confirm medium term decline has resumed for further subsequent fall to 109.80-85 (1.618 times projection of 112.20-111.12 measuring from 111.59) but price should hold above 109.50-55 (100% projection of 112.20-110.27 measuring from 111.46).

In view of this, would be prudent to stand aside in the meantime. Only above 111.46 resistance would abort and prolong choppy trading above 110.11 support, bring rebound to 111.59, then towards 111.90-00 later but price should falter well below said resistance at 112.20.

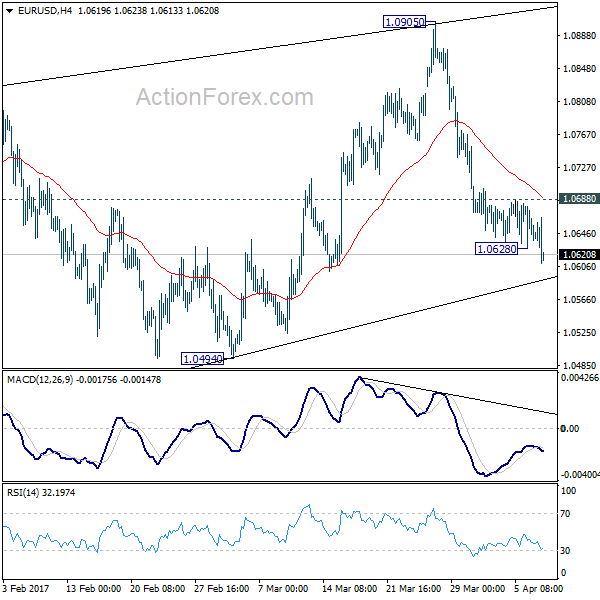

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0619; (P) 1.0652 (R1) 1.0675; More....

EUR/USD's fall resumed by taking out 1.0628 temporary low. Intraday bias is turned back to the downside for 1.0494 support. As noted before, corrective rise from 1.0339 is completed at 1.0905. And more importantly, larger down trend is probably resuming. Decisive break of 1.0494 support will confirm this bearish case and target 1.0339 low. On the upside, break of 1.0688 resistance will indicate short term bottoming and bring stronger rebound first.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.

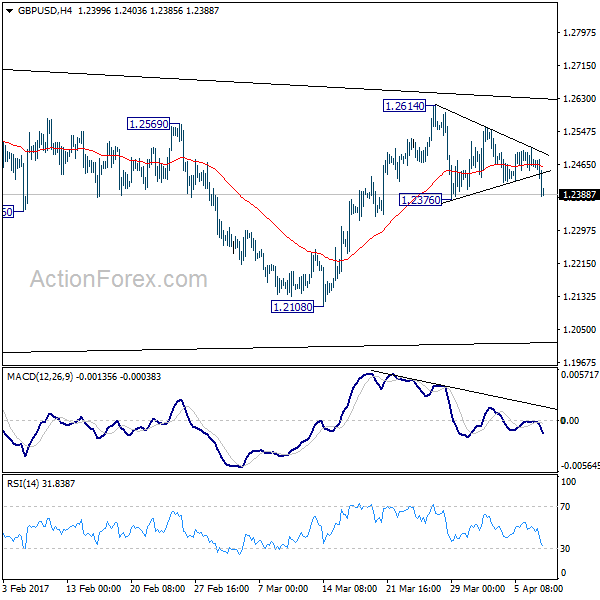

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2444; (P) 1.2474; (R1) 1.2499; More...

GBP/USD's sharp fall in early US session argues that fall from 1.2614 is possibly resuming. Intraday bias is cautiously on the downside for 1.2376. Break will confirm and target 1.2108 support level. Overall, price actions from 1.1946 are viewed as a consolidation pattern. Decisive break of 1.2108 will be an early sign of larger down trend resumption. On the upside, break of 1.2614 will extend the rise from 1.2108. But upside should be limited by 1.2705/2774 resistance zone to bring larger down trend resumption eventually.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term reversal yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

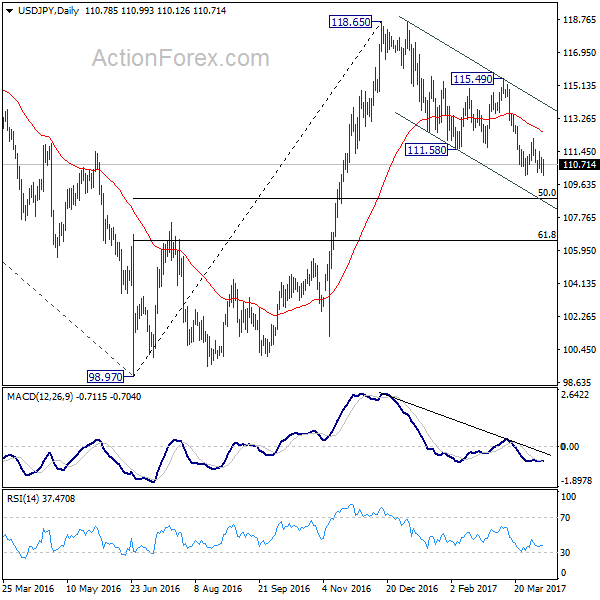

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.34; (P) 110.74; (R1) 111.19; More....

USD/JPY is still bounded in range above 110.10 and intraday bias remains neutral. More consolidation could still be seen. But, break of 112.19 resistance is needed to indicate short term reversal. Otherwise, outlook will stay bearish for another fall. Break of 110.10 will extend the whole decline from m 118.65 and target 50% retracement of 98.97 to 118.65 at 108.81. On the upside, however, break of 112.19 resistance will indicate short term reversal and turn bias back to the upside for 115.49 resistance.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Nonetheless, sustained trading below 55 week EMA (now at 111.16) will extend the consolidation from 125.85 with another fall through 98.97 before completion.

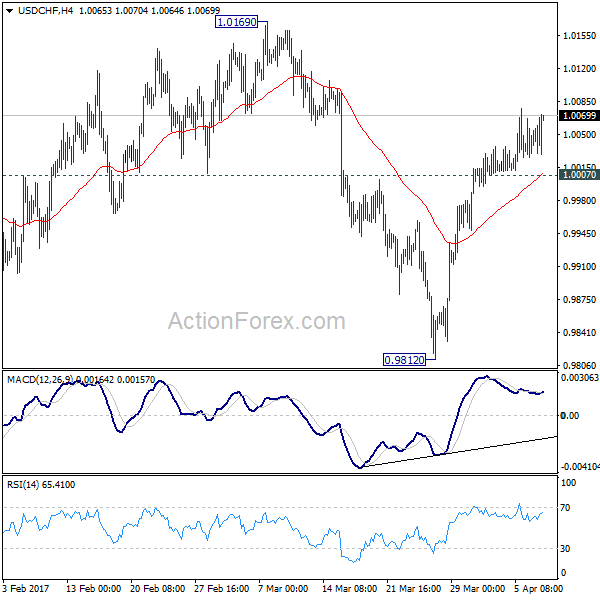

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0028; (P) 1.0047; (R1) 1.0069; More.....

USD/CHF's rally from 0.9812 is still in progress with 1.0007 minor support intact and further rise should be seen. We mentioned before that corrective decline fall from 1.0342 should have finished with three waves down to 0.9812 already. Rise from 0.9812 is expected to taken 1.0169 resistance next. Break of 1.0169 should confirm this bullish case and target a test on 1.0342 high. On the downside, below 1.0007 will bring deeper correction, possibly back to 0.9812 low.

In the bigger picture, USD/CHF is staying in medium term sideway pattern between 0.9443/1.0342. In any case, decisive break of 1.0342 resistance is needed to confirm underlying strength. Otherwise, we'll stay neutral in the pair first. In case of another fall, we'd expect strong support from 0.9443/9548 support zone.

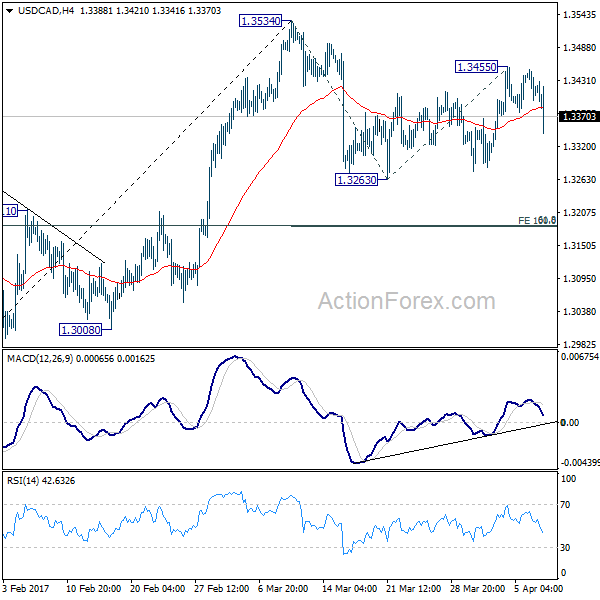

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3390; (P) 1.3420; (R1) 1.3442; More....

USD/CAD's sharp fall and break of 1.3373 minor support suggests that recovery from 1.3263 has completed with three waves up to 1.3455. The corrective structure in turns indicates that decline from 1.3534 is resuming. Intraday bias is turned back to the downside for 1.3263 support and below. Fall from 1.3534 is still viewed as a correction for the moment. Hence, we'd expect strong support from 1.3184 cluster level (61.8% retracement of 1.2968 to 1.3534 at 1.3184, 100% projection of 1.3534 to 1.3263 from 1.3455 at 1.3814 too) to contain downside and bring rebound. On the upside, break of 1.3455 will turn bias back to the upside for 1.3534 resistance.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg from 1.2460 is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. Break of 1.2968 will argue that the third leg has already started and should at least bring at retest of 1.2460 low. However, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

Non-Farm Payroll Grew Only 98k, USD/CAD Dives but Not a Disaster for Dollar Yet

US non-farm payroll report comes in much weaker than expected. Only 98k jobs were created in March, around half of expectations of 177k only. Prior month's figure was also revised down from 235k to 219k. Unemployment rate dropped 0.2% to 4.5%, hitting the lowest level in nearly 10 years. Average hourly earnings posted 0.2% mom rise in March, below expectation of 0.3%. Released from Canada, employment rose 19.4k in March versus expectation of 5.7k. Unemployment rate rose to 6.7%. Notable weakness is seen in USD/CAD after the releases, as Canadian dollar is additionally supported by surge in oil price. Some buying is seen in the Japanese yen, on risk aversion and possibly on expectation of fall in treasury yields too. Meanwhile, dollar is so far steady against European majors.

US launched military strike in Syria, Russia Condemned, China Xi Overshadowed

Gold and WTI Crude oil jump today on news that US launched military strike on the airfield in Syria in response to the government's use of chemical weapons on civilians. Stocks, however, are relatively steady with just mild safe haven flows. Russian President Vladimir Putin condemned the US strike as "act of aggression against a sovereign state". Meanwhile, Putin suspended the 2015 memorandum of understanding on air operation. And, Putin's spokesman said that the risk on confrontation between US and Russia as "significantly increased". Also, Putin ordered additional measures to strengthen Syria's air defenses to protect the "most sensitive" infrastructure assets of the country. The development overshadows the meeting between Trump and Chinese President Xi Jinping.

BoE Carney: Brexit negotiations a litmus test for responsible financial globalization

BoE Governor Mark Carney said today that "how Brexit negotiations conclude will be a litmus test for responsible financial globalization." And, the EU and UK are "ideally positioned to create an effective system of deference to each other's comparable regulatory outcomes, supported by commitments to common minimum standards and open supervisory cooperation." Meanwhile, Carney also said that " level of planning is uneven across firms" regarding Brexit. And, "plans may not be being sufficiently tested against the most adverse potential outcomes - for example, if there is no withdrawal or trade agreement in place when the UK exits from the EU."

Release from UK, industrial production dropped -0.8% rose 2.8% yoy in February, versus expectation of 0.2% mom, 3.7% yoy. Manufacturing production dropped -0.1% mom, rose 3.3% yoy, versus expectation of 0.3% mom, 3.9% yoy. Construction output dropped -1.7% mom in February. Trade deficit widened to GBP -12.5b in February. NIESR GDP estimate rose 0.5% in March.

ECB Praet: Premature to discuss reduction of asset purchases

ECB chief economist Peter Praet said in a TV interview that it's "premature" to discuss further reduction of asset purchases. He warned earlier this week that "if investors start perceiving that the path of the policy rate is subject to upward uncertainty ... long-term interest rates will be pushed higher and asset purchases will become less effective." ECB President Mario Draghi also said that there was no "sufficient evidence to materially alter our assessment of the inflation outlook". Therefore, "reassessment of the current monetary policy stance is not warranted at this stage." And those include "interest rates, asset purchases and forward guidance."

Also released from Europe, German industrial production rose 2.2% mom in February, trade surplus widened to EUR 2.1b in February. Swiss unemployment rate was unchanged at 3.3% in March. Swiss foreign currency reserves rose to CHF 683.0b in March.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3390; (P) 1.3420; (R1) 1.3442; More....

USD/CAD's sharp fall and break of 1.3373 minor support suggests that recovery from 1.3263 has completed with three waves up to 1.3455. The corrective structure in turns indicates that decline from 1.3534 is resuming. Intraday bias is turned back to the downside for 1.3263 support and below. Fall from 1.3534 is still viewed as a correction for the moment. Hence, we'd expect strong support from 1.3184 cluster level (61.8% retracement of 1.2968 to 1.3534 at 1.3184, 100% projection of 1.3534 to 1.3263 from 1.3455 at 1.3814 too) to contain downside and bring rebound. On the upside, break of 1.3455 will turn bias back to the upside for 1.3534 resistance.

In the bigger picture, price actions from 1.4689 medium term top are seen as a correction pattern. The first leg has completed at 1.2460. The second leg from 1.2460 is likely still in progress and could target 61.8% retracement of 1.4689 to 1.2460 at 1.3838. We'd look for reversal signal there to start the third leg. Break of 1.2968 will argue that the third leg has already started and should at least bring at retest of 1.2460 low. However, sustained trading above 1.3838 would pave the way to retest 1.4689 high.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | JPY | Labor Cash Earnings Y/Y Feb | 0.40% | 0.50% | 0.50% | 0.30% |

| 05:00 | JPY | Leading Index Feb P | 104.4 | 104.6 | 104.9 | |

| 05:45 | CHF | Unemployment Rate Mar | 3.30% | 3.30% | 3.30% | |

| 06:00 | EUR | German Industrial Production M/M Feb | 2.20% | -0.20% | 2.80% | 2.20% |

| 06:00 | EUR | German Trade Balance (EUR) Feb | 21.0B | 19.4B | 18.5B | |

| 07:00 | CHF | Foreign Currency Reserves Mar | 683.0B | 674.0B | 668.2B | |

| 08:30 | GBP | Industrial Production M/M Feb | -0.70% | 0.20% | -0.40% | |

| 08:30 | GBP | Industrial Production Y/Y Feb | 2.80% | 3.70% | 3.20% | |

| 08:30 | GBP | Manufacturing Production M/M Feb | -0.10% | 0.30% | -0.90% | |

| 08:30 | GBP | Manufacturing Production Y/Y Feb | 3.30% | 3.90% | 2.70% | |

| 08:30 | GBP | Construction Output M/M Feb | -1.70% | 0.00% | -0.40% | |

| 08:30 | GBP | Visible Trade Balance (GBP) Feb | -12.5B | -10.9B | -10.8B | |

| 12:00 | GBP | NIESR GDP Estimate Mar | 0.50% | 0.60% | 0.60% | |

| 12:30 | CAD | Net Change in Employment Mar | 19.4K | 5.7k | 15.3k | |

| 12:30 | CAD | Unemployment Rate Mar | 6.70% | 6.70% | 6.60% | |

| 12:30 | USD | Change in Non-farm Payrolls Mar | 98K | 177k | 235k | 219K |

| 12:30 | USD | Unemployment Rate Mar | 4.50% | 4.70% | 4.70% | |

| 12:30 | USD | Average Hourly Earnings M/M Mar | 0.20% | 0.30% | 0.20% | 0.30% |

| 14:00 | CAD | Ivey PMI Mar | 56.3 | 55 |