Sample Category Title

The Weekly Bottom Line

HIGHLIGHTS OF THE WEEK

United States

- U.S. economic data disappointed on a variety of fronts this week, but much can be chalked up to weatherrelated disruptions to the data.

- A paltry 89k payrolls gain was the biggest disappointment, but we are inclined to look past one month's result and focus on a new cyclical low in unemployment and continued improvement in measures of underemployment. These should also help support a rebound in consumer spending through the remainder of 2017.

- In other news, the Fed is starting to discuss the process of unwinding its holdings of Treasuries and mortgage-backed securities (MBS). It pledged that moves will be well-telegraphed and are likely to start later this year.

Canada

- It is getting more and more difficult to ignore the good news out of the Canadian economy. This was evident again this week as labour market data showed a fourth straight month of consensus-busting job growth.

- The economy generated 19.4k jobs in March, almost all of them full-time (+18.4k). While the unemployment rate ticked up to 6.7% (from 6.6%), this was due to more people joining the labor market - arguably a good problem to have.

- Canada may have started the year with more slack than its southern neighbor, but the differential is closing. Even with a slowdown in economic growth relative to its recent torrid pace, slack is likely to continue to diminish. As it does, the case for the Bank of Canada to move off the sidelines will strengthen.

UNITED STATES - BLAME IT ON THE WEATHER

March payrolls data disappointed expectations, with only 98k new jobs in March, and downward revisions to hiring in January and February. A softer reading was expected after two heady months, but a 200+ reading in the closely watched ADP report earlier in the week had raised hopes. Hiring slowed across both the goods and services sectors, although it was more dramatic in services. Despite the unexpectedly weak payroll print, the household survey showed employment gain of 472k, pushing the unemployment rate down by 0.2 percentage points to 4.5%.

We are inclined to look past one month's payrolls disappointment. Weather played a role in the March data on two fronts. Unusually warm weather in January and February likely pulled forward activity in the construction sector. And, data on curtailment of hours due to bad weather was nearly ten times larger than average in March, impacting hours worked, earnings and potentially hiring.

The job market should continue to provide a solid foundation for consumer spending this year, with the unemployment rate near pre-recession lows in March, and continued improvement in measures of underemployment.

Other data this week confirmed that consumers took a breather once again in Q1, but we expect a rebound in spending in Q2, much like we saw last year. Q1 weakness has become a pattern. Consumer spending growth averaged 2% in Q1 over the past 4 years, while the other three quarters of the year have averaged above 3% (see chart). Eventually, this pattern will be fixed by adjustment to "seasonal adjustment," but for now we are inclined to discount Q1 weakness.

The Fed minutes also provided a peek into the FOMC's discussion of how and when it will start the process of normalizing its balance sheet, now that normalizing rates is underway. Through the course of its asset purchase program, the Fed accumulated $4.5 trillion in Treasuries and MBS. Since purchases ended, the Fed has been reinvesting the principal payments, keeping its balance sheet steady.

Although things are still at the discussion phase, Fed members already agree on a few things. First, the process of ending reinvestments should be gradual and predictable, and rely primarily on passive phasing out of reinvestments. Second, most members agreed that the change in reinvestment policy should come this year. Third, the FOMC was unanimous that any policy change should be well telegraphed to the public. Our recent forecast calls for the Fed to hike rates in two 25 basis point moves, likely in June and September, and then lay out the plan to start winding down reinvestments. Once reinvesting principal payments is completely phased out, the balance sheet will passively shrink as the securities mature.

Markets are watching closely since removing the Fed from these markets could reduce demand for these securities, lowering prices, and taking yields higher, all else equal. Our latest forecast calls for a continued rise in Treasury yields, and balance sheet normalization is one of the forces expected to take yields higher. The Fed has control of this process. If the Fed doesn't like the market reaction as it winds down reinvestments, it has the discretion to slow down or stop the pace of adjustment. This helps to mitigate the risks of an undesirable spike in yields.

CANADA - I GET KNOCKED DOWN, BUT I GET UP AGAIN

It is getting more and more difficult to ignore the good news out of the Canadian economy. This was evident again this week as labour market data showed a fourth straight month of consensus-busting job growth. The economy generated 19.4k jobs in March, almost all of them full-time (+18.4k). While the unemployment rate ticked up to 6.7% (from 6.6%), this was due to more people joining the labor market - arguably a good problem to have.

The positive turn in economic momentum has come as data in the United States has moved in the opposite direction. Job growth south of the border slowed in March to just 98k. On a year-on-year basis, employment growth in Canada has been running faster than in the United States for the past three months. The difference is not large, but it marks a change from the previous four years in which the U.S. was adding jobs at a relatively faster clip (Chart 1).

The divergence is not just a jobs story. Even with the pullback in exports in February that returned the country's trade balance to a slight trade deficit (following three months in surplus), Canada's economy is tracking growth of 3.4% (annualized) in the first quarter. Meanwhile, stateside, real GDP looks to advance by just 1.0%.

The outperformance in Canadian economic data relative to the U.S. may reflect the fact that Canada simply has a bigger hole to fill. Indeed, countries with more slack should be expected to grow relatively faster. Despite the slowdown in job growth in the U.S., the unemployment rate fell to 4.5% in March, widely considered its long-run (or natural rate).

Yet, it is not so straightforward to make the case that Canada has a lot more slack than America. On a comparable basis, the Canadian unemployment rate was 5.4% (seasonally adjusted) in March, 0.9 percentage points above the U.S. rate. But, Canadian unemployment rates have always run higher than U.S. rates. The current differential is the same as it was prior to the Great Recession, and lower than its longer-run historical average of 1.3 percentage points (Chart 2). By other metrics, the Canadian labor market is the tightest it's been since the recession. The employmentto- population ratio of core working age people (25 to 54) rose to 82.3% in March, its highest level since mid-2008.

The worry among policymakers is that Canadian economic growth is built on shaky foundations. Canada has seen false starts before - economic growth started last year with similar spark. However, that was largely an export story, and net-trade is likely to subtract from growth in the this year. At the same time, the current strength in key housing markets is unsustainable over the medium term, but there appears little on the horizon to impede near term momentum. Finally, government stimulus dollars should begin translating more meaningfully into activity this year, helping to maintain Canada's growth trajectory.

All told, Canada may have started the year with more slack than its southern neighbor, but the differential is closing swiftly. Even with a slowdown in economic growth relative to its recent torrid pace, slack is likely to continue to diminish. As it does, the case for the Bank of Canada to move off the sidelines will strengthen.

US Jobs Miss Raises Questions about Economy, Retail Sales and Inflation Next for Dollar

US jobs miss raises questions about economy

The US dollar will finish the week ending on April 7 on a high note despite the US non farm payrolls (NFP) missing expectations. The greenback is only lower against the JPY as other major pairs have fallen as risk aversion following the geopolitical events around the globe. The US airstrike against Syria in particular caused a wave of USD selling but as the day went on the currency recovered along with the risk appetite of investors. Members of the G7 will meet in Italy on Monday for a two-day prescheduled meeting that has risen in importance given current events.

US earnings seasons will kick off next week with Financials leading the charge. The sector has been one of the winners in the Trump trade and as such has suffered by the loss in momentum as the future of the pro-growth policies remains cloudy. Fed Chair Janet Yellen will speak on Monday with room for some insight on the Fed minutes released this week that show the central bank is debating on when to reduce the 4.5 Trillion bonds in its balance sheet.

The Bank of Canada (BoC) will release its monetary policy report on Wednesday, April 12 at 10:00 am EDT (2:00 pm GMT) with no change expected to the benchmark interest rate. The highlight of the week in economic data will be the US retail sales and inflation data to be published on Friday, April 14 at 8:30 am EDT (12:30 GMT). Employment gains in the United States continue to be solid despite the latest disappointing NFP report but it's worth noting that retailers lost 29,700 jobs in March after losses of 30,000 in February. Core inflation is forecasted flat at 0.0 percent while core retail sales could come in at 0.2 percent.

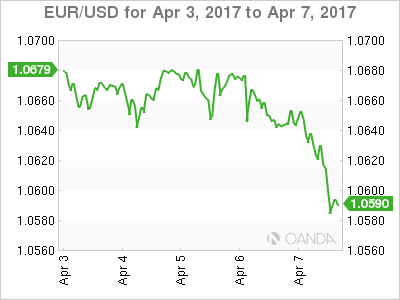

The EUR/USD lost 0.906 percent during the last five trading sessions. The single currency is trading at 1.0587 after the US dollar bounced back from overnight losses. The USD gained on both fronts against the EUR, when investors sought safety after the US airstrike against Syria they bought JPY, gold and US treasuries, even after a NFP miss the USD was bid as few institutional traders will leave longs ahead of a weekend after so much geopolitical anxiety. French elections concerns are lower after the latest televised debate, but situations in Italy and elections later in the year in Germany have not painted an encouraging scenario for European unity.

Mario Draghi said on Thursday that the policies of the European Central Bank (ECB) remain appropriate and even despite positive signs of recovery it is too soon to talk about reducing stimulus. This means that the divergence between the Fed and the ECB will only grow as the Fed slowly but surely continues on a tightening path while the ECB is still unsure when it will abandon its expansionary policies. Fed Chair Janet Yellen's words on Monday could further put the US central bank on a more proactive path than the ECB, who is still struggling with having a coordinated response when big members such as Germany haven't bought in to the long term plans.

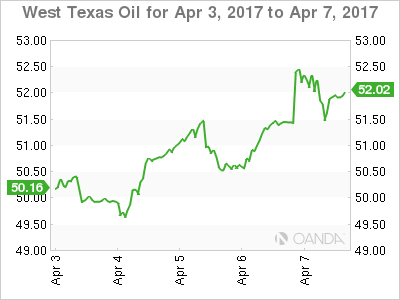

Oil prices in the US rose 3.368 percent during the last week. The price of West Texas is trading at $51.91 after the US attack on Syria made crude prices jump. Donald Trump made the call while hosting Chinese President Xi Jinping so political risk was already high.

There is ample evidence of oversupply in the market, yet the price is still rising even as there are more US producers waiting to ramp up production. Asian markets that have been limited by the OPEC cut, have turned to US oil which reduces the overall negative impact of increased US crude. China has surpassed Canada as the main destination of US oil.

A disruption in Canadian supplies after the shutdown of the Syncrude oilseeds facility in Alberta has also helped WTI march higher even before the fears of lower supply as a result of the US intervention in Syria.

Gold rose 0.232 percent in the last five days. The price of the yellow metal is trading at $1,251.78 although intraday volatility on Friday had it as high as $1,270.64. The combined effect of the ongoing China-US summit in Florida, the US airstrike in Syria, the terrorist attack in Stockholm and the weaker than expected NFP jobs report had investors seeking a safe haven and flowing into gold.

Near the end of the Friday session the USD had managed to recover from overnight losses. The metal traded in a 2 percent range as geopolitical events reduced the risk appetite of market participants.

Market events to watch this week:

Monday, April 10

- 4:00pm USD Fed Chair Yellen Speaks

Tuesday, April 11

- 4:30am GBP CPI y/y

Wednesday, April 12

- 4:30am GBP Average Earnings Index 3m/y

- 10:00am CAD BOC Monetary Policy Report

- 10:30am USD Crude Oil Inventories

- 11:15am CAD BOC Press Conference

- 9:30pm AUD Employment Change

- Tentative CNY Trade Balance

Thursday, April 13

- 8:30am CAD Manufacturing Sales m/m

- 8:30am USD PPI m/m

- 8:30am USD Unemployment Claims

- 10:00am USD Prelim UoM Consumer Sentiment

Friday, April 14

- 8:30am USD CPI m/m

- 8:30am USD Core CPI m/m

- 8:30am USD Core Retail Sales m/m

- 8:30am USD Retail Sales m/m

*All times EDT

Elliott Wave View: Natural Gas Short-term

This is a quick update to the post from yesterday where we called blue (x) completed in Natural Gas (NG #F) at 3.235. However, price has been unable to break higher so far and after a failed test of 3.347 peak, we have seen another dip and a double three Elliott wave correction in wave (x) now seems more likely towards 3.235 - 3.208 area which is 50 - 61.8 Fibonacci retracement area of the rally from 3.122 low. From this area and as far as pivot at 3.122 low remains intact, we can expect Natural Gas to turn higher again and reach the target between 3.45 - 3.587 are from where a larger 3 wave pull back can be seen at least to correct the cycle from 3/17 (2.882) low if not from 2/22 (2.523) low.

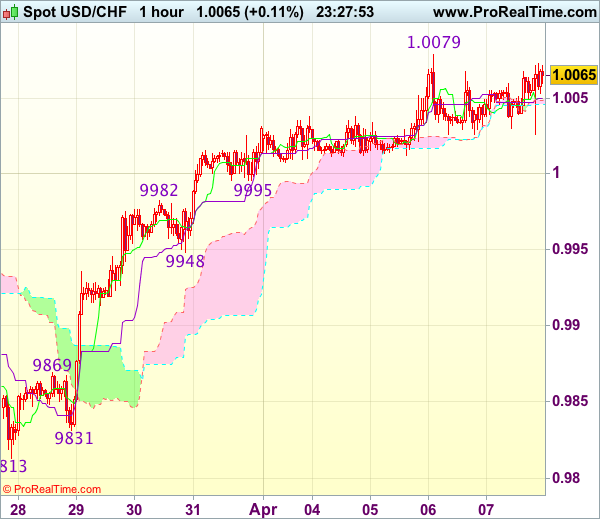

Trade Idea Wrap-up: USD/CHF – Buy at 0.9950

USD/CHF - 1.0063

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.0050

Kijun-Sen level : 1.0050

Ichimoku cloud top : 1.0050

Ichimoku cloud bottom : 1.0046

Original strategy :

Buy at 0.9950, Target: 1.0050, Stop: 0.9915

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9950, Target: 1.0050, Stop: 0.9915

Position : -

Target : -

Stop : -

The greenback remained confined within near term established range and further sideways trading is in store before recent rise from last week’s low at 0.9813 resumes, above resistance at 1.0079 would extend further gain to previous resistance at 1.0109, however, loss of upward momentum should prevent sharp move beyond latter level and reckon 1.0140-50 would hold, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and would be prudent to buy dollar on pullback as support at 0.9948 should limit downside. Below 0.9925-30 would abort and signal top is formed instead, bring correction to 0.9905-10 but reckon previous resistance at 0.9869 would hold from here.

Trade Idea Wrap-up: GBP/USD – Sell at 1.2450

GBP/USD - 1.2399

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.2426

Kijun-Sen level : 1.2441

Ichimoku cloud top : 1.2478

Ichimoku cloud bottom : 1.2465

Original strategy :

Sell at 1.2450, Target: 1.2350, Stop: 1.2485

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.2450, Target: 1.2350, Stop: 1.2485

Position : -

Target : -

Stop : -

As the British pound has dropped again and broke below indicated feel at 1.2400, adding credence to our view that rebound from 1.2377 has ended at 1.2559 and reset of this level would be seen, however, break there is needed to confirm early fall from 1.2616 has resumed for weakness to 1.2350, then towards 1.2325-30 but near term oversold condition should limit downside today and reckon 1.2300 would hold from here.

In view of this, would not chase this fall here and would be prudent to sell cable on recovery as 1.2450-60 should limit upside. Above 1.2480 would defer and suggest low is formed instead, risk test of resistance at 1.2506 first, break there would confirm, then a stronger rebound to 1.2525-30 would follow.

Trade Idea Wrap-up: EUR/USD – Sell at 1.0725

EUR/USD - 1.0620

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.0639

Kijun-Sen level : 1.0639

Ichimoku cloud top : 1.0659

Ichimoku cloud bottom : 1.0656

Original strategy :

Sell at 1.0725, Target: 1.0610, Stop: 1.0760

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0725, Target: 1.0610, Stop: 1.0760

Position : -

Target : -

Stop : -

As the single currency has remained weak after recent selloff, adding credence to our bearish view that the decline from 1.0906 is still in progress for further weakness towards previous chart support at 1.0600, however, a sustained breach below the latter level is needed to retain downside bias for subsequent selloff to 1.0570-75 and possibly towards 1.0550.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 1.0720-30 should limit upside. Only a firm break above resistance at 1.0773 would suggest low is formed instead, bring a stronger rebound to 1.0800 but resistance at 1.0827 should remain intact.

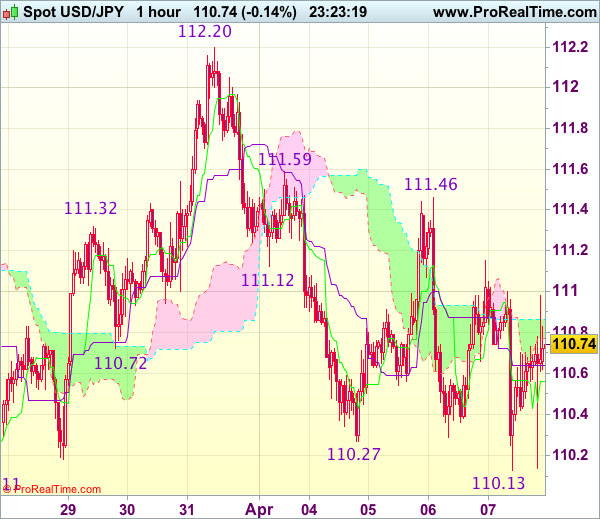

Trade Idea Wrap-up: USD/JPY – Stand aside

USD/JPY - 110.78

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 110.56

Kijun-Sen level : 110.64

Ichimoku cloud top : 110.87

Ichimoku cloud bottom : 110.77

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although the the greenback slipped again in NY morning, as dollar has rebounded again after holding above indicated support at 110.11, retaining our view that further consolidation above this level would be seen and corrective bounce to 111.10-15 cannot be ruled out, however, reckon upside would be limited and resistance at 111.46 should remain intact, bring another decline later, below said support at 110.11-13 would confirm medium term decline has resumed for further subsequent fall to 109.80-85 (1.618 times projection of 112.20-111.12 measuring from 111.59) but price should hold above 109.50-55 (100% projection of 112.20-110.27 measuring from 111.46).

In view of this, would be prudent to stand aside in the meantime. Only above 111.46 resistance would abort and prolong choppy trading above 110.11 support, bring rebound to 111.59, then towards 111.90-00 later but price should falter well below said resistance at 112.20.

French Election: Mélenchon Risk To Euro Is Underestimated

- Buy EM Specifically INR - Peter Rosenstreich

- Fed Plans To Unwind Its Balance Sheet - Arnaud Masset

- French Election: Mélenchon Risk To Single Currency Is Underestimated - Yann Quelenn

- Oil Recovery

FX Markets - Buy EM Specifically INR

Emerging market currency had an extremely busy week, while G10 markets were in wait-and-see mood. Political uncertainty in South Africa spiked driving ZAR weakness. The much anticipated, but marginally earlier then suggested, EURCZK floor was removed. While US missile strikes on Assad regime highlighted increased tension between the US and Russia causing RUB to fall 1.0% overnight. Yet, despite the idiosyncratic risk of each currency we remain bullish on the asset class and view pullbacks as opportunity to reload EM longs. The external environment remains supportive as globally, activity indicators show stronger economic performance and commodities (oil) prices inched higher. Specifically we remain bullish on INR for two key reasons. First is the hawkish monetary policy meeting and secondly, the resiliency of the INR to external geopolitical events.

The Reserve Bank of India (RBI) held the benchmark policy repo rate unchanged at 6.25% but raised the reverse repo rate by 25bp to 6% (narrowing policy rate corridor). Despite that fact that adjustment of the repo rate is slightly more operational, the move does have hawkish overtones above neutral policy stance. But, the RBI's upwards revision in the inflation projection by 25bp to 4.75% for 2017-2018 was a clearly hawkish signal. Annual growth is projected at 7.4%, for 2017 and the RBI sees improvement in advanced economies as supporting further economic acceleration. We suspect the probability of the RBI cutting rates this year is significantly low consider the growing inflation pressure (despite inflation falling to 3.4% well below 5% target level) and health growth backdrop.

While there is a lack of core drivers, non-market related events continue to inject short term volatility.

Mounting expectations for Trump tax reform, French presidential elections and contentious Brexit negotiations suggest that hype will cloud real fundamentals. Yet so far the INR has proved surprising resilience to external events. While investor quickly rotated to safe-haven FX trades (JPY, USD and gold) on the news of US military aggression, INR appreciations continued un-interrupted. In the last 3-months INR has gained 5.80% against the USD at a time when US treasury rates were on a rollercoaster ride. Indian economy has become a magnet for capital inflows which could force that RBI to attempt to limited INR strength. But current RBI FX interventions have been limited indicating comfort with INR levels. If nothing else investors can enjoy a high carry with INR.

Economics - Fed Plans To Unwind Its Balance Sheet

Given the lacklustre pace of recovery of the US economy, most participants expected the Fed to stick to its initial plan: gradual rate tightening. Instead, the minutes of the March FOMC meeting revealed that the members discussed extensively the strategy to start unloading the $4.5 trillion of bonds and mortgage-backed securities that currently sit on its balance. Technically, the Fed did not actually discuss selling those assets but rather changing the committee's reinvestment policy later this year. Indeed, the central bank is currently reinvesting all principal payments from its Treasury, agency debt and agency MBS portfolios, which has the effect to maintain unchanged the nominal size of its portfolio.

Until now, Fed members were only vaguely discussing about unwinding its bonds portfolio. In addition, the balance sheet discussions only recently started to gain traction. The market did not expect the Fed to move that fast as most analyst were expecting the Fed would start finetuning its reinvestment policy in the middle of 2018. This surprise move caught investors off guard and forced them to reassess the US economic outlook as well as the effect on the USD. Indeed, choosing to unload the balance sheet instead of tightening short-term rate has the advantage to limit, to some extent, USD appreciation.

At present, it is difficult to know what the real effects of unwinding the balance sheet are going to be. In such a situation, the market's response was rather muted, translating perfectly the fact that we are entering new territory. In addition, the reflation trade in the US is, more than ever, being questioned by market participants as President Trump's administration has been unable to carry out any of its planned reforms so far. Moreover, the unpredictability of Trump's foreign policy will also keep investors on the back foot, which would eventually prevent the USD to appreciate significantly.

Nevertheless, the backdrop of political uncertainty in the European Union favours the greenback in the short-term, especially against the euro and the pound sterling. Indeed, the sharp increase in implied volatility - 25 delta risk-reversal slid to -3.51% on Friday - suggests that the market is becoming increasingly worried about French election. Due to its safe haven status, the Japanese yen remains the best candidate for upside surprise against the USD.

Economics - Mélenchon Risk To Single Currency Is Underestimated

The second debate of the French Presidential Election was broadcast earlier last week, during which the 11 candidates had the chance to expose their views on many different topics. Emmanuel Macron, who is leading the polls for the final win, was hardly attacked by the other candidates. No candidate performed badly and so it was very hard to find a winner.

There are only two weeks remaining until the first round of the French Election. We know that whatever may happen in those last few weeks, declarations from candidates may still have an impact on the markets. Francois Fillon has not renounced, despite being considered out of the race in February, and we may see him increasing again in polls. His chance of a final victory is still alive.

Regarding Emmanuel Macron, many socialists are now supporting him. What should we believe from that? We believe that their endorsement is less in a desire to counter the National Front, but rather to participate in the likely new presidential majority.

A few weeks ahead of the first round on April 23rd, there is some disappointing data on the French industrial side. February's industrial production declined by -1.6% m/m, well below the market's consensus at -0.3%. On an annualized basis, the decline is around -0.7%. Manufacturing production also declined strongly in February to -0.6% y/y. This is the worst contraction for French industry since September.

In the markets, we can see the CAC 40 is improving more slowly than the Euro Stoxx 50. We try to measure investors' fear and we believe banks' stocks price are a good proxy for that. It is clear that their volatility is increasing.

The end of the Hollande mandate is rather difficult and the new President will definitely have a hard time pushing the French economy. This very weak data illustrates why there has been a boost towards more sovereignty over the last few years and the rise of the nationalism.

Currency-wise, we do not see the euro improving should Macron or Francois Fillon get elected. There is also a growing risk for the monetary union as we believe Jean-Luc Mélenchon's chance of winning is underestimated. His performances in those kind of debates are always one of the most accomplished, if not the best. And his "Plan B" is that in the case of negotiation failure, he would not hesitate to ask for a Frexit referendum. So we now assume that Euro downside risks are not anymore only due to Marine Le Pen.

The markets are still betting on a Macron victory but we assume his inexperience is going to be tough to overcome against his major competitors. The markets seem calm and the first round is going to provide us with a decent gauge. For now, markets are still not pricing a Le Pen victory. In terms of currency, the Euro is consolidating against the USD between 1.06 and 1.07 and we believe that there is more room for further downside in the short-term.

Themes Trading - Oil Recovery

Cuts in crude oil production and growing demand indicate that crude prices should continue to grind higher in 2017. In an unexpected move, OPEC silenced skeptics by orchestrating the first production cut in eight years between OPEC and non-OPEC countries. The agreement sent crude prices soaring. After four years of depressed crude prices as a result of a global supply glut, the group's three largest producers – Saudi Arabia, Iraq and Iran – overcame significant disagreement to move to reduce global oil inventories. The agreement was unprecedented, with Russia and Mexico also joining in to cut output.

As oil market dynamics continued to tighten, certain companies are better positioned to take advantage of improving oil prices. This Oil Recovery theme is designed to exploit rising prices by selecting companies mostly active in the upstream segment, which would benefit the most from a barrel above $60. To enhance risk diversification, the portfolio is structured using an equally-weighted risk contribution approach. In summary, this means the allocation is calculated in such a way that each stock contributes on an equal basis to the portfolio's total risk. This approach allows for lower volatility and, in so doing, increases the risk/ reward ratio.

Bank of Canada Policy Decision, Key Data in Focus

Next week's market movers

- In Canada, we expect the BoC to remain on hold and maintain its relatively dovish tone despite the latest improvements in the profile for economic growth.

- We also get key economic data from the US, the UK, Norway and Sweden.

On Monday, we have a relatively quiet calendar day. The only indicator that could attract market attention is Norway's CPI for March.

On Tuesday, we get the UK CPI data for March. Without any forecast available, we see the case for both the headline and the core rates to have risen further. This view is based on the services PMI for the month, which showed that prices charged by service provides increased at the fastest rate for eight-and-a-half years. Considering that services account for the vast majority of UK GDP, a reasonable argument can be made that inflationary pressures in the overall economy continue to pick up rapidly. We expect a confirmation of that from the CPIs to fuel speculation regarding some future tightening by the BoE. Even though the latest commentary from BoE policymakers suggests that the Bank is in no hurry to raise rates, we believe that rapidly accelerating inflation could lead to some more hawkish dissents among the Committee.

We also get Sweden's CPI figures for the same month.

On Wednesday, all eyes will be on the Bank of Canada rate decision, though no forecast is available yet. The BoC has maintained a concerned tone in most of its recent communications. At the press conference following the January gathering, Governor Poloz unexpectedly said that another cut remains on the table should downside risks materialize, while in the latest policy statement, the Bank hinted that there are still "significant uncertainties" weighing on the outlook for exports. The Bank has also previously stressed that the strength of the Canadian dollar is muting that outlook. Even though economic data have improved somewhat since the latest meeting, particularly with regards to economic growth, we doubt that this is enough to lead to a change in the officials' dovish rhetoric. Our own view is that the Bank will probably remain on hold once again, but it will leave the door wide open for a near-term rate cut if needed. By providing dovish hints and essentially talking down the currency, the BoC can ensure that Canada's exports remain competitive. It is also worth noting that this meeting includes a press conference as well, so even in case the statement has a more or less neutral tone, we could still get some concerned comments from Governor Poloz.

In the UK, employment data for February are due out. In the absence of a forecast, we see the likelihood for the unemployment rate to have held steady, while the average weekly earnings rate may have rebounded somewhat, following two consecutive months of declines. Our expectations emanate from the services PMI for the month, which showed that a moderate pace of job creation was maintained in the UK's largest sector, and that firms reported higher wage bills.

On Thursday, we have a relatively quiet day, without any major market moving events or indicators due to be released.

On Friday, markets will remain closed in all G10 nations, in celebration of the Good Friday holiday.

Nevertheless, there is no rest for the statistical services of the US, which will release the nation's CPI and retail sales data, all for March. With regards to the CPIs, without any forecast yet, we see the case for both the headline and the core rates to have remained unchanged, with risks skewed to the downside. The Price sub-indices of the nation's ISM manufacturing and non-manufacturing PMIs showed mixed results in the month. The manufacturing Prices index rose further, but its non-manufacturing counterpart tumbled notably. Considering though that the service sector accounts for a much bigger percentage of the US economy, we think that a slowdown in that price index may be more significant. What's more, the slowdown in the yearly change of oil prices enhances the likelihood for a pullback in the headline rate, in our view.

As for retail sales, both the headline and the core rates are expected to have risen, albeit slightly. We see the risks surrounding these forecasts as skewed to the upside, considering the nation's consumer confidence indices for the month. Even though the U of M index rose only slightly, the Consumer Board figure skyrocketed, reaching a level last seen in 2000. This suggests that US consumers may be feeling increasingly more optimistic, something that may show up in the retail sales figures too.

No Negative Fall-out from Mediocre Payrolls

Headlines

European stock markets didn't lose additional ground after a risk-off opening following the US' missile strike against Syria. US stocks also trade narrowly mixed, ignoring an ambiguous payrolls report.

March net job growth increased by 98k, way below market consensus of 180k while the previous two month's numbers were downwardly revised by 38k. The unemployment rate unexpectedly declined from 4.7% to 4.5% while average hourly earnings rose by 0.2% M/M and 2.7% Y/Y, in line with forecast.

Greece's international creditors have hailed progress on the reforms demanded of the country, saying the "big blocks" to releasing bailout cash to Athens had been cleared. Eurogroup Dijsselbloem confirmed a deal had been struck on the reforms demanded of the left-wing government in return for its latest tranche of rescue cash.

UK manufacturing and construction unexpectedly shrank in February, adding to signs that the economy lost momentum in the first quarter. Factory output fell 0.1% from January. Total industrial production declined 0.7% as unseasonably warm weather reduced demand for energy. Construction dropped 1.7%, the most in almost a year.

German industrial output surged in February (2.2% m/m) and the trade balance swelled (€19.9B) as the engine room of Europe's largest economy fired on all cylinders to satisfy robust foreign demand that is assuaging angst about rising protectionism.

Sweden should start planning for how to deal with the end of its quantitative easing programme, Riksbank deputy governors Ohlsson has said, in a notable shift of tone from the central bank's recent dovishness in official statements.

The Czech central bank's foreign currency reserves soared by a record €17.1B in March, reaching 70% of GDP as the central bank intervened heavily to defend its weak-crown policy. The bank lifted the EUR/CZK 27 peg yesterday after nearly three and a half years which saw a total of around €73B in interventions.

China's foreign exchange reserves rose again in March but by less than expected as authorities in the world's second largest economy fight with halting capital outflows and have seen a stabilisation in the renminbi this year.

Fitch has become the second major ratings agency this week to cut the South African government's sovereign credit rating to junk status (BB+), after the ousting of respected finance minister Pravin Gordhan knocked confidence in President Jacob Zuma's commitment to sound economic policies.

Rates

Test of key US yield support fails twice

The US 5-yr and 10-yr yield tested key support, respectively at 1.8% and 2.3% on two separate occasions today. The test failed twice, suggesting that yields could move back higher, more comfortable within their trading ranges (1.8%- 2.14% for 5 yr and 2.3%-2.64% for 10yr). The first test occurred overnight after the US conducted missile attacks against Syria. The initial risk-off move cross markets (including higher opening for the Bund) didn't gain traction during European dealings. Markets retreated going into the US payrolls report, amid strong German production data. A disappointing headline March payroll number triggered a second, more intense test of key support levels. Job growth disappointed by 130k, taking into account downward revisions to the previous two month's numbers. An unexpected decline of the unemployment rate, to 4.5% (lowest since May 2007) countered the weak headline reading. Average hourly earnings also printed in line with forecasts (0.2% M/M, 2.7% Y/Y). A break lower in yield terms eventually didn't occur, sending (US) yields back higher. The jury is still out, but we think that this one-off payrolls' miss won't derail the Fed's normalization intentions, suggesting higher yields.

At the time of writing, the German yield curve bull flattened with yields 2.5 bps (2-yr) to 3.8 bps (30-yr) lower. Changes on the US yield curve range between - 0.1 bp (2-yr) and -2.9 bps (10-yr). On intra-EMU bond markets, 10-yr yield spread changes versus Germany 10-yr yield vary between -2 bps and +1 bp with Greece outperforming (-18 bps). Greece reached a deal on economic reforms with its bailout monitors, paving the way for the payout of the next bailout tranche.

Currencies

USD: no negative fall-out from mediocre payrolls

The events in Syria had little impact on European trading in general and on the dollar in particular. The dollar held tight ranges going into the US Payrolls. The report was mixed to slightly softer than expected. The dollar dropped briefly lower immediately after the report, but the losses were soon reversed. USD/JPY survived another test of the lows and is again trading in the high 110 area. The US currency even succeeded small gains against the euro with EUR/USD changing hands in the 1.0620 area.

Overnight, Asian markets were hit by a (temporary?) risk-off reaction on the US missile strike against Syria. Markets followed the 'standard risk-off procedure'. Equities and US bond yields declined. The yen rebounded. The oil price jumped as markets feared more instability in the region. However, the reaction was limited and an important part of the moves was already reversed at the European market opening. USD/JPY dropped close to the recent lows in the low 110 area, but the test was again rejected and the pair returned to the 110.60 area. EUR/USD was little changed in the 1.0650 area.

On the newswires, there were plenty of news articles and analysis on the consequences of the US strike against Syria. However, for markets in general and for FX trading in particular, it was basically a non-event. Equities opened slightly lower but without follow-through selling. USD./JPY settled in an extremely tight sideways range in the 110.60 area. The dollar even gained slightly ground during the morning session, drifting to the 1.0630 area.

The US payrolls were unable to give clear guidance for USD trading. The headline figure showed a unexpectedly sharp slowdown in payrolls growth (89K from 221k, 170k was expected). However the unemployment rate declined to the lowest level in almost 10-yr (4.5%). The dollar (and other markets) initially reacted briefly to the poor headline figure. USD/JPY again tested the recent low below 110.20. EUR/USD spiked to the mid 1.06 area. However, the USD downside was blocked. Core yields also reversed an initial spike lower, further supporting the dollar. USD/JPY trades currently just below 111. EUR/USD is changing hands in the 1.0620 area. In a broader perspective, the USD gains are negligible, but USD-bulls might get some comfort as the USD avoided losses on a mediocre report. To be confirmed.

Sterling loses slightly ground after poor UK data

There were plenty of eco data on the UK eco calendar today including the Halifax House prices, the output data and the external trade data. They were not the most important ones and some of them could be considered as a bit outdated. Even so, each of the data series came out weaker than expected. It was enough to trigger a modest correction of sterling. EUR/GBP rebounds to the 0.8550/60 area. Sterling lost slightly further ground after the payrolls, driven by the comeback of the dollar. Cable dropped below the 1.24 big figure. In this move EUR/GBP gained a few more ticks (currently in the 0.8570 area).