Sample Category Title

Non-Farm Payroll First, Middle East Second

Friday April 7: Five things the markets are talking about

Momentum in the U.S labor market was strong going into last month, however bad weather during non-farm payroll's (NFP) mid-March sample week pose the risk of weather-related delays in hiring.

Market consensus is looking for a headline print atop of +180k mark, which would be a very healthy rate of monthly growth, but off the Jan and Feb pace of +235k. A weaker print will have the market revising U.S Q1 GDP expectations.

Note: Advance indicators this week are mixed. Tuesday's ADP did not see any weakness for Mar., but instead recorded a solid gain (+263k vs. +184k), extending both Jan and Feb's trend. In contrast, the employment-index of the ISM non-manufacturing report Wed. points to a slowdown in hiring. Yesterday's U.S weekly jobless claims posted the largest drop in two years (+234k vs. +251k).

The U.S unemployment rate is expected to hold steady atop of its nine-year low of +4.7%.

Investors are also watching developments from the summit in Florida between Trump and Chinese President Xi Jinping.

Note: Expect the market to remain very nervous after Trump's missile attack on Syria last night – the capital market move, since dissipated, triggered an instant reaction across everything from stocks to commodities and currencies.

The attack caused a knee-jerk shift into safe-havens, although the impact was moderate as it is being interpreted as a "one-off" proportionate response.

1. No surprise, global equities mixed response to Syria missile attack

Japan's Nikkei (+0.4%) share average edged up in choppy trade overnight, but gains were limited as the U.S missile strike on Syria curbed investors' risk appetite. The broader Topix index climbed +0.7%.

In China, the Shanghai Composite Index rose +0.2%, and completed a +2% gain for the holiday-shortened week. In Hong Kong, the Hang Seng dropped -0.4%, while Singapore's Straits Times Index fell -0.3%.

In Europe, equity indices are trading lower amid geopolitical tensions. Banking stocks are leaning on Eurostoxx 600, while the FTSE 100 is slightly outperforming as oil stocks trade higher in line with Brent and WTI contracts.

U.S stocks are set to open in the red (-0.1%).

Indices: Stoxx50 -0.5% at 3,474, FTSE -0.1% at 7,294, DAX -0.6% at 12,161, CAC-40 -0.4% at 5,102, IBEX-35 -0.7% at 10,442, FTSE MIB -0.3% at 20,238, SMI -0.5% at 8,598, S&P 500 Futures -0.1%

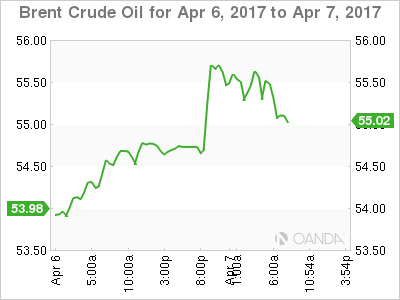

2. Oil jumps in knee-jerk reaction to Syria

Oil futures surged more than +2% to a one-month high overnight after the U.S launched its missile attack on a Syrian airbase. However, prices have since retreated a tad as there seemed no immediate threat to supplies.

Ahead of the attack, Brent crude futures were trading atop of +$55.62 then jumped to +$56.08 per barrel and up +1.3% from yesterday's close. U.S West Texas Intermediate (WTI) crude futures also climbed by more than +2%, to a high of +$52.94 a barrel, before receding to +$52.46, up +1.45%.

Note: Although Syria has limited oil production; its location in the Middle East and alliances with big oil producers raises concerns about spreading conflict that could disrupt crude shipments. Both Russia and Iran, staunch allies of Syria, condemned the attacks.

However, in oil supply fundamentals, markets remain oversupplied, even with efforts led by the OPEC to cut supplies to support global prices.

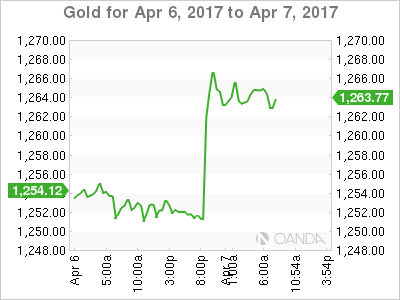

Gold rose more than +1% overnight to hit a five-month high as investors sought safe-haven assets. The yellow metal is trading at +$1,263.53 per ounce. The markets see higher prices in the short-term, at least until there is some clarity around Syria and if the "one-off" airstrike develops into something more.

3. Safe haven flows dominate bond prices

Bonds were amongst the biggest gainers across the various asset classes following the first Middle East military strike by the Trump administration.

Core European government bonds opened higher amid the broad flight-to-quality move after the Syria strikes. However, these early gains have since faded. Currently, 10-year Bund yields are trading lower by -2 bps to +0.24%.

Note: In typical risk-off fashion, Euro core bonds outperformed, while Italian and Spanish 10-year yields were little changed.

U.S. Treasury yields dropped to their lowest level in over four-months at +2.29% in risk averse trading, yields have since found support with 10's trading atop of +2.32% ahead of non-farm payrolls (NFP).

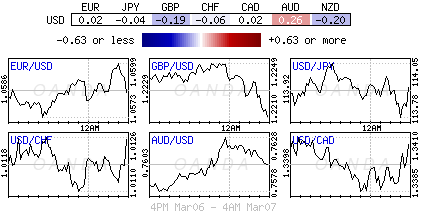

4. Safe haven trade dominates currency proceedings

Geopolitical has been able to keep market risk appetite sidelined, however, its boosted safe-haven assets after U.S launched numerous missile strikes on a Syrian airbase deemed responsible for recent chemical attack on civilians.

USD/JPY tested the lower end of the psychological ¥110 level on the initial reports of the U.S missile attack, but has since stabilized back to this week's mid-¥110 area (¥110.60). Another go to currency of choice during stress, the CHF ($1.0054) is little changed from its opening level in Asia.

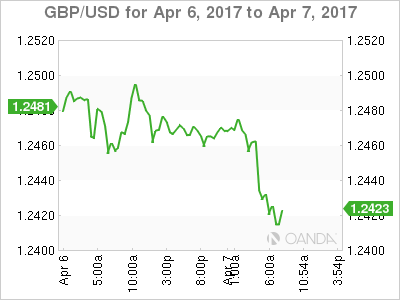

The pound (£1.2425, down -0.3%) is softer after Feb Industrial Production and Trade data (see below) came in worse then expectations.

5. U.K Industrial Production and Trade data miss expectations

U.K. manufacturing output was weaker than expected in February, falling by -0.1% from January compared to a forecast rise of +0.3%. The year-to-year rise was also weaker, at +3.3% as against a +3.8% expected.

There was a larger fall in industrial production over the month as a warmer-than-usual Feb. reduced demand for electricity. Output was down +0.7% from Jan. as against a forecast drop of -0.1%.

Note: January's figures for both manufacturing and industrial production were slightly revised, but still recorded month-to-month decline – it's been a weak start to 2017.

Other data showed that U.K.'s deficit widened in Feb, although that was largely due to imports of big-ticket items. The U.K imported £12.5B more than it exported.

Canadian Dollar Edges Lower Ahead Of Canadian, US Job Data

USD/CAD is almost unchanged in the Friday session, as the pair trades slightly above the 1.34 line. On the release front, job numbers are in the spotlight on both sides of the border. Canada releases Employment Change and the unemployment rate, while the US releases three key events – Nonfarm Payrolls, Average Hourly Earnings and the unemployment rate.

Weak oil prices in the first quarter of 2017 have weighed on the Canadian dollar, which has been unable to make any inroads against its US counterpart. US crude continues to trade just above the $50 level, as the tug-of-war between OPEC and the US producers continues. The glut of oil worldwide remains as higher US production has offset OPEC cuts. US Crude Inventories continue to show surpluses, most of which have been higher than the forecast. This was the case again last week, with US crude inventories posting a strong gain of 1.6 million, surprising the markets which had forecast a decline. The indicator has posted 12 surpluses in the last 13 weeks, which has helped keep a lid on higher oil prices throughout 2017.

There were no surprises from the Federal Reserve policy minutes, which were released on Wednesday. The minutes had a slightly hawkish tone, as policymakers noted upside risk to the US economy. However, policymakers remain divided on whether inflation will rise to the Fed target of 2.0% percent. The minutes also stated FOMC members were in favor of taking steps to trim the $4.5 trillion balance sheet, which has ballooned since the Fed implemented its aggressive quantitative easing program back in 2008. However, the Fed is unlikely to make any moves in this front till later in the year, as President Trump’s fiscal policy remains a big question mark. So what’s next for the Federal Reserve? According to the CME’s Fed Watch, the odds of a rate hike at the May meeting are just 5 percent, while the likelihood of a rate hike in June stand at 63 percent. . Fed policymakers appear divided on how many more times the Fed will press the rate trigger. Last week, FOMC member Eric Rosengren called for three more hikes, saying the Fed should raise rates in June, September and December. Rosengren said that employment and inflation levels were close to the Fed’s targets, and that three additional hikes were needed in order to prevent the US economy from overheating. However, a majority of FOMC members are in favor of just two more hikes this year.

The Dollar, Yen, Swiss Franc and Gold Jump as Tension Rises in Middle East

- 'The global financial system is moving from fragility to resistance' says Mark Carney

- The Dollar, Yen, Swiss Franc and gold jump as tension rises in Middle East

- Market looks towards the Non-Farm Payroll later today

In the UK, Mark Carney's speech at 10:00 BST was billed as a top tier announcement, although what he was actually speaking about was not confirmed before the speech. Carney's announcement was watched eagerly for any snippet of monetary policy speak, which can have a profound effect on the strength of Sterling. Carney discussed the security and responsibilities of the financial system in the UK and said that "the global financial system is moving from fragility to resistance" and highlighted the UK's role as a key international financial centre.

However, he pointed out risks that need to be addressed globally, of not working together with other countries' financial systems and the risks that poses to liquidity and funding; and the risks to the UK's financial system, due to its complexity and size. He discussed the need for resilience and risk management in light of Brexit. Carney also emphasised the importance of Brexit globally by saying, "How the Brexit negotiations conclude will be a litmus test for responsible financial globalisation" and speaking positively about the UK's strong position in the negotiations. He was keen to point out the opportunities for increased trade and globalisation that this presents.

The outcomes of this morning's speech provided a boost for the Pound, which bodes well for this afternoon's release of the National Institute of Economic and Social Research (NIESR) Gross Domestic Product (GDP) Estimate for the UK, with it expected at 0.6% - anything wide of the mark could result in volatility for the Pound, but this morning's discussions may just have given Sterling the helping hand it needed.

Traders will be looking for safe havens this morning with tensions in the Middle East ratcheting up as the US bombed an airfield in Syria overnight. The airbase allegedly responsible for launching the chemical weapons attack earlier this week. The US administration have stated that there can be no future in Syria for Mr Assad and this will now complicate relationships between themselves and Russia. The Dollar, Yen, Swiss Franc and gold have gained on the news.

The main event today in the US today will be US non-farm payrolls at 13:30 BST and with the week's precursor ADP figure overshooting the mark, positive things are expected for today. How much of this is already priced in is hard to tell.

Markets are expecting a rise of 180,000 and although as mentioned, the private report was better than expected. Building activity has picked up and the housing market has been largely buoyant, this could translate into a better than expected payroll report sparking further strength in the Dollar.

Spring Jokes

When do monkeys fall from the sky?

During Ape-ril showers!

Can February March?

No, but April May!

What flowers grow on faces?

Tulips (Two-lips)!

Why is everyone so tired on April 1?

Because they've just finished a long, 31 day March!

Technical Outlook: FTSE Is Back Above Daily Cloud As Pound Weakens

FTSE managed to recover and emerge above daily cloud (cloud top lies at 7241), following spikes lower that penetrated deeply into cloud, yesterday and today.

Repeated strong downside rejections are seen as bullish signal, as cloud is still acting as support.

Fresh strength was also boosted by weakness of the pound that is probing below key supports and threatening of further easing.

The upside extension cracked daily Tenkan-sen barrier (7252) that further improves near-term picture.

Near-term studies are in bullish/neutral mode while dailies give mixed signals but expected to remain bullishly aligned while the price is holding above the cloud.

We look for close above daily cloud for firmer bullish signals.

Alternative scenario requires return into daily cloud to generate negative signal and re-focus recent lows at 7195/79.

Res: 7259, 7269, 7281, 7287

Sup: 7252, 7241, 7223, 7195

EUR/GBP Edges Up Post Soft UK Data And Carney’s Speech

EUR/GBP downtrend was held above the significant support line at 0.8500, after hitting a 5-week low of 0.8485 on March 31.

EUR/GBP bulls failed to gain the near-term major resistance level at 0.8600 on April 5, as the pressure at the level is heavy.

The bulls have regained momentum since this morning, as a result of a weakening Sterling caused by underperforming UK industrial and manufacturing data (Feb) and the Bank of England President Carney's statement.

Carney made a speech after the release of the data. He stated that the Brexit negotiation would influence bank regulations and cooperation. The transition period poses a risk to the stability of financial system.

On the 4-hourly chart, the price is heading from the lower band to the middle band by the Bollinger Band indicator, suggesting the bullish momentum is strengthening.

The resistance level is at 0.8565, followed by 0.8580 and 0.8600.

The support line is at 0.8530, followed by 0.8510 and 0.8500.

DAX Unchanged As Markets Eye US-China Summit, Nonfarm Payrolls

The DAX Index is showing little movement in the Friday session. Currently, the DAX is trading at 12,168.00. In economic news, Germany continues to post strong numbers. Industrial Production jumped 2.2%, beating the estimate of -0.1%. Germany’s trade surplus improved to EUR 21.0 billion, beating the forecast of EUR 19.4 billion. The US will release Nonfarm Employment Payrolls, with the markets braced for a drop to 174 thousand.

Investors remain cautious ahead as President Donald Trump and Chinese President Xi Jinping are meeting for a two-day summit. The two leaders will meet on Thursday in Florida. There are plenty of potential sticking points between the US and China, including trade, currencies and North Korea. During the presidential campaign, Trump harshly criticized China for its trade and currency policies, but he has moderated his stance since becoming president. However, any undiplomatic incidents could unnerve investors and trigger volatilty in the stock markets.

The ECB released the minutes of its March policy meeting on Thursday. The minutes indicated that the ECB plans to maintain its monetary policy, with no changes to interest rate levels or the central bank’s asset-purchase scheme. The minutes added that there was “considerable risk surrounding the economic outlook and the robustness of inflation convergence”, which warranted maintaining the downward bias on interest rates. Essentially, the ECB has promised “more of the same”, with the asset-purchase scheme scheduled to remain in place until December. The powerful German central bank is not of the same view, however, as it would like to see tighter monetary policy, given the improvement in the economic data and higher inflation levels. March PMI reports impressed, as German and Eurozone Services and Manufacturing PMIs pointed to expansion. If the Eurozone economy continues to improve, we can expect the calls in favor of higher rates to get louder.

The Federal Reserve released the minutes of its March policy meeting, when the Fed raised rates by a quarter-point, to 0.75%. The minutes had a slightly hawkish tone, as policymakers noted upside risk to the US economy. However, policymakers remain divided on whether inflation will rise to the Fed target of 2.0% percent. The minutes also stated FOMC members were in favor of taking steps to trim the $4.5 trillion balance sheet, which has ballooned since the Fed implemented its aggressive quantitative easing program back in 2008. However, the Fed is unlikely to make any moves on this front till later in the year, as President Trump’s fiscal policy remains a big question mark. So what’s next for the Federal Reserve? According to the CME’s Fed Watch, the odds of a rate hike at the May meeting are just 5 percent, while the likelihood of a rate hike in June stand at 63 percent.

Technical Outlook: US Crude Oil Surged Near $53 Per Barrel On Geopolitical Risk

US oil accelerated strongly higher on Friday and hit one-month high at $52.92 on renewed geopolitical risk on US military action in Syria.

Oil price extends strong rally from $50.75 higher base for the second day, accelerating through $51.97 pivot (Fibo 61.8% of $55.01/$47.06 descend) and hitting the base of thin daily cloud (spanned between 52.96/53.74) so far.

Fresh strong bullish sentiment that has established, neutralized fears of failure to sustain break above psychological $50.00 barrier, opening was for further upside action that may bring in focus key med-term barriers at $55.22/01 (peaks of 03 Jan / 21 Feb).

Oil is also on track for the second straight strong bullish weekly close that also gives positive signal.

Dips on profit-taking should find solid support at $51.59 (55SMA / session low).

Res: 52.92, 53.13, 53.44, 53.78

Sup: 52.24, 51.97, 51.59, 51.41

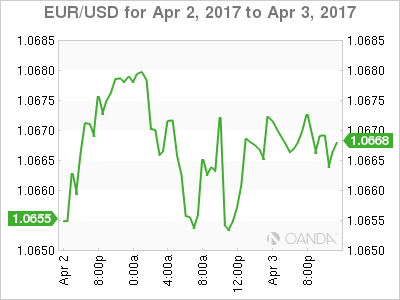

EUR/USD Is Trapped In Megaphone Pattern

Due to latest developments in Syria, Oil and Gold went up understandably, and Equities are having a slight pullback, so all eyes now are on NFP, Average Hourly Earnings and Unemployment data. The NFP report should come out strong as we saw better than expected ADP numbers earlier this week. The USD/JPY has already dropped from POC zone as shown yesterday.

Technically we can see a clear megaphone (aka broadening top) pattern on intraday time frame. The pair has been congested in an extremely tight range, making the range more significant with this pattern. The range is only 63 pips for the last 14 days(!). Within the megaphone pattern we can see a consolidation (green highlight) between D H3 and D L3 levels. Depending on the overall data today we should see higher volatility today in EUR/USD so pay attention to these levels.

1.0658-1.0628 is Major consolidation. Below 1.0628, we might see 1.0613 (D L4) and 1.0588 (D L5). Above 1.0658, 1.0675 and 1.0700 are targets. Overshot to W H3 1.0720 is possible too if the pair spikes above 1.0700.

Investors On Edge Ahead Of Non-Farm Payroll

A strong sense of unease infiltrated the financial markets during trading on Friday with investors staying clear of riskier assets after reports were released that the U.S military launched an airstrike on Syria. The possible threat of geopolitical tensions heightening from the airstrikes has created a risk-off trading atmosphere which left Asian shares mixed. The lack of upside momentum from Asian markets has already contaminated European equities with the diminishing appetite for risk potentially limiting gains on Wall Street this afternoon. It must be kept in mind that participants were already jittery ahead of the Trump-Xi summit and this fresh development may compound to the horrible cocktail of uncertainty.

Trump-Xi summit round 2

Although the Trump-Xi summit has been somewhat overshadowed by the US strike on Syria, investors may still pay very close attention to how the meeting between these two world leaders progresses. While Donald Trump has said that he has developed a friendship with Chinese President Xi Jinping, this may be tested today as the two leaders discuss trade, North Korea, and other important market moving issues. A situation where the outcome of the meeting seems unfavorable and unsuccessful could intensify the risk aversion ultimately boosting Gold.

NFP in the spotlight

The solid ADP report and hawkish Fed minutes this week have allowed the Greenback to regain its attitude with the Dollar Index trading around 100.78 as of writing. With short-term bulls simply looking beyond the Trump uncertainties and focusing on positive economic data, the Dollar could be poised for further upside. Investors may direct their attention towards the pending NFP report this afternoon which could offer some insight to how the US labor force fared in March. A blockbuster NFP figure that exceeds expectations coupled with a surprise rise in average hourly earnings could boost the Dollar further. From a technical standpoint, the breakout above 100.75 could open a path higher towards 102.00.

Gold breaks above $1260

Gold charged to a fresh 5 month high at $1269 during early trading on Friday after reports were released that the U.S military launched an airstrike on Syria which soured risk appetite. With risk aversion set to heighten as markets ponder over the ramifications of the U.S airstrike, Gold and other safe-haven assets may receive a solid boost. While there is a possibility of a positive NFP report pressuring Gold prices, the downside shocks may be limited by the jitters. From a technical standpoint, bulls need a solid daily close above $1260 for a further incline higher towards $1300.

Commodity spotlight – WTI

WTI Crude was propelled towards $52.90 on Friday after the U.S airstrikes on Syria sparked speculations of a threat to supplies. Although the sharp upsurge in prices has turned oil somewhat bullish on the daily charts, the bearish fundamentals remain intact. With the oversupply concerns still a dominant theme in the oil markets, extreme upside gains may be limited. From a technical standpoint, bulls have won the battle this week with prices breaking above $52. For the upside to continue and display sustainability, a solid breakout and daily close above $53 will be needed. In an alternative scenario, bears have a chance to reclaiming control back below $51.

Euro Quiet Ahead of US Nonfarm Payrolls

It's been an uneventful week for EUR/USD, which continues to trade between 1.06 and 1.07. Currently, the pair is trading at 1.0640. On the release front, German indicators continue to impress, as Industrial Trade and Trade Balance both beat expectations. In the US, employment numbers will be in focus, highlighted by Nonfarm Payrolls. The markets are braced for a weak reading of 174 thousand. Traders should be prepared for movement from EUR/USD around the release time of the employment numbers, at the start of the North American session.

The ECB plans to hold the course on monetary policy, according to the minutes of its March policy meeting. The minutes indicated that the ECB plans to maintain its monetary policy, with no changes to interest rate levels or the central bank's asset-purchase scheme. The minutes added that there was 'considerable risk surrounding the economic outlook and the robustness of inflation convergence', which warranted maintaining the downward bias on interest rates. Essentially, the ECB has promised 'more of the same', with the asset-purchase scheme scheduled to remain in place until December. The powerful German central bank is not of the same view, however, as it would like to see tighter monetary policy, given the improvement in the economic data and higher inflation levels. March PMI reports impressed, as German and Eurozone Services and Manufacturing PMIs pointed to expansion. If the Eurozone economy continues to improve, we can expect the calls in favor of higher rates to get louder.

There were no surprises from the Federal Reserve policy minutes, which were released on Wednesday. The minutes had a slightly hawkish tone, as policymakers noted upside risk to the US economy. However, policymakers remain divided on whether inflation will rise to the Fed target of 2.0% percent. The minutes also stated FOMC members were in favor of taking steps to trim the $4.5 trillion balance sheet, which has ballooned since the Fed implemented its aggressive quantitative easing program back in 2008. However, the Fed is unlikely to make any moves on this front till later in the year, as President Trump's fiscal policy remains a big question mark. So what's next for the Federal Reserve? According to the CME's Fed Watch, the odds of a rate hike at the May meeting are just 5 percent, while the likelihood of a rate hike in June stand at 63 percent.