Sample Category Title

Week Ahead US Employment Data and Fed Minutes

US economic data and European risk to guide markets

The US dollar is mixed as it gained against the EUR, CHF, NZD and JPY but lost ground against the CAD, GBP and AUD. Political risk continues to impact markets as US uncertainty, the official triggering of Brexit and the upcoming French elections make investors anxious even as energy markets rebound thanks to a possible extension to the Organization of the Petroleum Exporting Countries (OPEC) production cut deal. On the diplomatic front Chinese President Xi Jinping will visit the US and is scheduled to meet US President Donald Trump for the first in-person meeting on April 6–7.

Following a week with scarce data, the first week of April will feature the Reserve Bank of Australia (RBA) rate decision on Tuesday, April 4 at 12:30 am EDT and the releases of the meeting minutes from the March meetings from the US Federal Reserve on Wednesday, April 5 at 2:00 pm EDT and the European Central Bank (ECB) on Thursday, April 6 at 7:30 am EDT. US data will grab the spotlight as manufacturing and non-manufacturing PMIs, crude inventories and jobs data are released.

US employment data will be released this week with the ADP private payrolls leading the charge on Wednesday, April 5 at 8:15 am EDT (12:15 pm GMT). After a strong reading last month of 298,000 forecasters are expecting the number of jobs to slow down, but to remain above 200,000. The US non farm payrolls (NFP) to be published on Friday, April 7 at 8:30 am (12:30 pm GMT) is expected add 180,000 jobs to the US economy keeping the unemployment rate at 4.7 percent with a slight rise in wages of 0.2 percent. The jobs component has been validating the decision of the Fed to move rates higher, but as inflation becomes central to the conversation the wage growth indicator will be key on Jobs Friday.

The EUR/USD lost 1.018 in the last five trading days. The single currency is trading at 1.0697 after the USD has recovered from political shocks as the Trump administration is reassessing its strategy to push pro-growth policies into other branches of the government. The partisan divide in the US will continue to restrain any forward momentum resulting from positive economic indicators. The EUR has gained from US uncertainty, but has lost ground as US fundamentals remain strong and Fed speakers continue to fan the flames of further rate hikes in 2017.

Germany continues to be the engine of the EU and strong retail sales (1.8 percent) beat the estimate but inflation in the Union was lower than the estimate at 1.5 percent which puts less pressure on the European Central Bank (ECB) as it has put itself in a position where it might still have a QE program while needing to hike rates if inflation keeps climbing rapidly.

Next week will be more US focused as employment indicators will be releases as well as the meeting notes from the March Federal Open Market Committee (FOMC) which resulted in a 25 basis points interest rate hike. The US non farm payrolls (NFP) report is the biggest economic release and could end up helping the dollar get out of the current funk due to political stagnation.

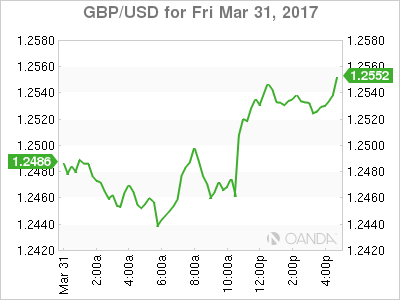

The GBP/USD gained 0.349 percent in the last week. The pound is trading at 1.2535 higher than the lows of the week at 1.2377 which is a good sign considering Article 50 kickstarted the Brexit process on Wednesday. The estimated two year length of the process and the fact that it is the response and negotiations with Europe that will drive markets have kept the GBP at current levels. The currency will remain tied to political events as there is still a gap between what the UK think it can negotiate and what Europe considers fair for a nation leaving its Union.

The European parliament will make an official statement regarding Brexit on April 4 with a deadline later in the month to prepare a joint document on the Union's points to negotiate. Final approval of the document is on April 29 when the European Commission will outline the rules for the negotiation. Given that the currency market has already priced in the initial Brexit move last year the spotlight now moves on the negotiation and on the potential impact of the French elections on the EUR. Given the rise of Marine Le Pen and her National Front even though a Frexit looks like an unlikely outcome worse was said about Brexit.

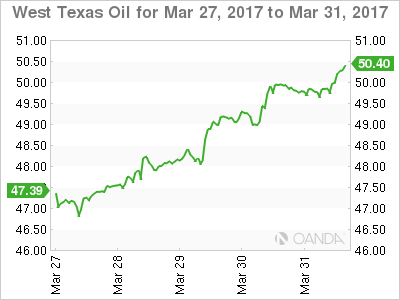

Oil rose 5.582 percent in the last five days. West Texas is trading at $49.95 and has broken above the $50 price level awaiting more details on a possible extension of the Organization of the Petroleum Exporting Countries (OPEC) production cut agreement. The original deal was only for six months, but given a combination of the effects of the agreement and the oversupply in the market the price of energy has bounced from the lowest levels since producers started reducing their output in January. The price is still far from 2017 highs of 54.53 but the threat of US shale producers and others who are not part of the OPEC and non-OPEC agreement continues as they are ramping up production and reactivating drilling sites. The OPEC will meet in May 25 with the deal extension sure to be on the agenda.

Market events to watch this week:

Sunday, April 2

- 9:30pm AUD Retail Sales m/m

- 9:45pm CNY Caixin Manufacturing PMI

Monday, April 3

- 4:30am GBP Manufacturing PMI

- 10:00am USD ISM Manufacturing PMI

- 9:30pm AUD Trade Balance

Tuesday, April 4

- 12:30am AUD Cash Rate

- 12:30am AUD RBA Rate Statement

- 4:30am GBP Construction PMI

- 5:15am AUD RBA Gov Lowe Speaks

- 8:30am CAD Trade Balance

- Tentative NZD GDT Price Index

Wednesday, April 5

- 4:30am GBP Services PMI

- 8:15am USD ADP Non-Farm Employment Change

- 10:00am USD ISM Non-Manufacturing PMI

- 10:30am USD Crude Oil Inventories

- 2:00pm USD FOMC Meeting Minutes

Thursday, April 6

- 7:30 am EUR ECB Meeting Minutes

- 8:30am USD Unemployment Claims

Friday, April 7

- 4:30am GBP Manufacturing Production m/m

- 8:30am CAD Employment Change

- 8:30am USD Average Hourly Earnings m/m

- 8:30am USD Non-Farm Employment Change

*All times EDT

S&P 500, New Highs above 2401 Still Favored But…

S&P 500 (cash) near term outlook:

Big picture view from early March of at least a few weeks of correcting from the Mar 1st high at 2401 (wave iv in the rally from the Jan 23rd low at 2257) and with eventual new highs after (within wave v) remains in place. In the Mar 24th email warned of potential, near term volatility on the US health care vote. The market did indeed pop lower, reaching that long mentioned bullish trendline from Dec (then at 2322) and before rapidly reversing higher. Though further gains above that 2401 high are still favored, that bearish trendline from Mar 1st (currently at 2378/01) may provide a few days/week of consolidating first (see in red on daily chart below). Nearby support is seen at 2348/51 and that bullish trendline from Dec (currently at 2327/30). A final note, though gains above 2401 are still favored, the magnitude may be more limited (and versus the start of a more major, new upleg). The market no doubt remains overbought in the bigger picture, lots of longer term resistance lies just above (see longer term below) and that series of 5 months spikes higher in the vix occurs again over the next few weeks (see 2nd chart below). Bottom line : gains above that 2401 high still favored but the big picture magnitude of further upside is a question.

Strategy/position:

Reached the buy target from the Mar 24th email at 2325 on Mar 27th (3 pts above the bull trendline from Dec) and for now, would stop on a close 3 pts below. However, with gains above that 2401 high potentially limited, will want to get much more aggressive in such upside (to reflect that risk).

Long term outlook:

Long held view an extended period of broad ranging higher (at least another few months) but with the pullbacks becoming more significant as the long term upside momentum slows, remains in place. Note as discussed above, the upside pattern from Jan as well as Nov and even last July (currently within wave 3) are still not "complete" and in turn argues a further period of "net" upside as these patterns unfold. But with the market very overbought after the last few years of sharp gains and nearing lots of longer term resistance, use the term "net" as the bigger picture upside is likely to become more "difficult"/limited and thus the expected period of a broad, ranging higher (with increasing pullbacks). Lots of long term resistance is above that Mar 1st high at 2401 at the rising trendline from Apr 2016 (currently at 2323/28) and the very long term ceiling of the bull channel from 2009 (currently at 2455/70, see weekly chart/2nd chart below) and adds to the nearer term view that bigger picture gains above 2401 may be limited. HoweverBottom line : still favor at least another few months of "net" upside, but with the pullbacks along the way potentially becoming more significant as the long term upside momentum starts to slow.

Long term strategy/position:

With further upside likely to become more rangy (as the longer term upside momentum slows), will generally stay with that approach of waiting for bigger picture pullbacks to buy and then being aggressive with stops on gains.

Current:

Nearer term : long Mar 27th at 2325 for gains above 2401.

Last : long Mar 10th at 2369, stopped Mar 21 below t-line from Nov (2370, closed at 2344).

Longer term: min few more months of upside, likely to range higher (good pullbacks along the way).

Last : same as shorter term above.

USDCHF: Remains On The Offensive With Eyes On 1.0100 Zone

USDCHF: The pair looks to extend its upside pressure after closing strongly higher the past week. On the downside, support lies at the 0.9950 level. A turn below here will open the door for more weakness towards the 0.9900 level and then the 0.9850 level. On the upside, resistance resides at the 1.0100 level where a break will clear the way for more strength to occur towards the 1.0150 level. Further out, resistance comes in at the 1.0200 level. Its daily RSI is bullish and pointing higher suggesting further strength. All in all, USDCHF faces further price strength.

Copper Elliott Wave View: 5 Waves Calling Higher

In this technical blog, lets take a quick look at the 1 hour Copper Elliott wave view from March 09 lows. In which the the metal was showing 5 waves bounce from March 09 (2.5593) low & the bounce was impulsive rather then corrective sequence. Thus suggesting the cycle from (2.5593) low could be following the Elliott wave Zig-zag pattern. Where the cycle from (2.5593) low ended at March 20 peak (2.6979) that we have labelled as Minute wave ((a)) of the zig-zag pattern. According to Elliott wave theory Zigzag is a 3 wave structure having internal subdivision of (5-3-5) swing sequence. The internal oscillations are labeled as A, B, C where A = 5 waves, B = 3 waves and C = 5 waves. This means that A and C can be impulsive or diagonal waves. However the A and C waves must meet all the conditions of wave structure 5, such as: having an RSI divergence between wave subdivisions, ideal Fibonacci extensions, ideal retracements etc. The cycle from (2.5593) low to (2.6979) was in 5 waves sequence, then the 3 wave dip in Minute wave ((b)) was expected to hold above (2.5593) low for next leg higher in Minute ((c)) leg higher into the direction of previous wave ((a)) or for 3 swings bounce at least.

Copper 1 hour chart

Below is the 1 hour March 27 NY updated chart showing the pullback happening in the metal within Minute wave ((b)), as Elliott wave double three structure from (2.6979) peak, where first leg lower ended in Minutte wave (w) at (2.5863) & Minutte wave (x) at (2.6544), then based on the correlations with US dollar & other commodities i.e OIL, Natural GAS & Metals, Copper was expected to stay above (2.5593) invalidation level.

Copper 1 hour March 27 NY updated chart

Since then Metal pulled back as expected, the pull back went quite deep but it was still holding above the Invalidation level (2.558) and as far as price stays above there, we were expecting Minute wave (( b )) to complete and metal to turn higher, as shown below

Copper 1 hour March 28 Asia updated chart

False Positive In European Inflation

FX Markets - False Positive In European Inflation

European investors have been cautiously watching last week's EU inflation data for likely forces driving the ECB's monetary policy strategy. Since February, consumer price inflation accelerated to its fastest pace since January 2013 and markets have been debating the rationale and sustainability of the ECB ultra-loose monetary stimulus policy. In addition, headline inflation which is trending higher towards the central bank's objective of below but close to 2%, with divergent core inflation, exuding persistent weakness, is a concern for Draghi.

The data release is expected to temporarily suspend demand for exiting accommodating positioning. Eurozone flash HICP inflation dropped 0.5% to 1.5% in March below consensus of 1.8% while core inflation slid to 0.7% y/y from 0.9% in February, below expectations for 0.8% print. HICP components indicate that all three indexes contributed to the fall in headline inflation.

With the "courgette shortage" fading, fresh food prices have moderated, sending food, alcohol, and tobacco price inflations to 1.8% from 2.5%. In addition, with crude prices falling energy price inflation also weakened to 7.3% from 9.3%. Overall seemingly headline inflation peak of 2.0% in February seems like an anomaly and unlikely to concern the ECB. However, with solid economic data including stronger labour-market outlook we suspect that underlying inflationary trend is on track and March data is a temporary. We could see core inflation climb to 1.1% by June supported by Easter related price increases. Less important are expectations that headline inflation will rebound to 1.8% by June.

The ECB spent much of last week trying to control market chatter over the exit. ECB members have been increasingly concern that the market is getting ahead of itself by misreading communications.

Dovish comments from ECB members such as Nowotny have done little to shift our European outlook. Yet, between data and comments our suspicion remains, that calls for the end of extreme policy setting (negative rates, easy lending, and bond purchases) are getting heard. ECB board member Coeure stated that it was "legitimate" for the ECB to review its pledge to keep rate at record low levels.

Overall, we don't expect to see actual changes in asset purchases and negative interest rates until 2018. However, in between the dovish guidance we suspect there will be hints of tightening. We suspect that we will get higher deposit rate before QE ends in a strategy to keep the market off guard. We remain constructive on EURUSD barring any shift in the French election outlook.

Economics - Brazilian Government Caps Spending

In spite of rising global uncertainty, emerging market currencies have been rather resilient over the last couple of weeks. However, one has to acknowledge that volatility also increased temporarily as investors preferred to remain cautious in the event that Donal Trump had to face another setback in implementing his programme. After completely erasing losses from last November and returning to around 3.05 in February, the Brazilian real has been trading in a volatile range since then, moving between 3.06 and 3.20 as investors await further clarity on the US outlook to emerge.

It goes without saying that local developments in EM countries have been largely ignored recently - with the exception of the political turmoil in South Africa last week - as market participants were too busy trying to anticipate Trump's next move. In Brazil, the economy is slowly gearing up as the central bank progressively eases its monetary policy. The Selic rate is currently at 12.25% but the market anticipates the benchmark rate to reach 9% by the end of the year as inflation is expected to return within the BCB's target range of 4.5% +/-1.5%.

All in all, looking at the hard data it seems as though Brazil is on the right track, however on the domestic side, the political situation is in complete upheaval and the uncertainty that stems from it should prevent the real from returning quickly towards its pre-recession levels. Moreover, the austerity measures planned by the government will further delay a speedy recovery as the lower classes of the Brazilian society are losing purchasing power. On the other hand, it will restore confidence and attract foreign investments. In the short-term BRL gains cannot be ruled out as investors are still chasing returns and Brazil's temporary stability is quite attractive. Nevertheless, the market is in wait-and-see mode and has slightly shifted to risk-off.

Economics - UK: The Exit Process Has Finally Begun

Nine months after the Brexit vote, Theresa May has finally started the exit process by triggering Article 50 of the Lisbon Treaty. The UK Prime Minister has spoken in front of the House of Commons last Wednesday. A letter has then be delivered by 1.30pm to Donald Tusk. Negotiations should last at least two years but the UK will still benefit many bilateral agreements in the meanwhile.

The pound fell the day before from 1.2460 to 1.2380 against the dollar. In our view, we believe that the markets are still overly pessimistic about the UK situation. Recent economic data is improving, but we also believe that the pound should appreciate in the medium-term. It is clear that economists widely missed the target with their doomsday prophecies and ironically, it is this very market pessimism that is supporting the UK economy by increasing the competitiveness of its exports.

Now that Brexit is officially a done deal, the next questions will revolve around the nature and tone of negotiations. 27 counterparts must accept and agree with the UK's terms with each country holding a veto over these conditions. It is for this reason that it is so difficult for countries to renegotiate treaties in general. For this reason, we find the promise to renegotiate treaties somewhat scammy.

Last week, in the two days following the triggering of Article 50, the Footsie 100 has risen and is now trading 16% higher than pre-Brexit levels. It makes the increase even more impressive since the 2016 Brexit vote also sparked a sell-off

Now our view for the negotiations is that we believe there won't be any hard Brexit. It is nonetheless clear that negotiations will be tough with all members having to agree on the final deal, which means that the next two years will be a serious rollercoaster ride.

We are also bullish on the pound which we should further appreciate this year. Strengthening of the pound is now very likely especially as Europe faces a veritable minefield with the upcoming French and German elections. Time to reload GBP.

Themes Trading - Swiss Small Gems

Switzerland's stability has provided ideal soil for global brands to develop. The Swiss National Bank's commitment to hold interest rates negative "for some time" should convince domestic savers to move their savings into stocks while allowing the Swiss franc to further devalue. With a weaker Swiss franc, companies will regain some of the competitive edge they have lost. However, Swiss companies rely more on brand quality and innovation than on pure price competitiveness. Outside the blue chip names are small cap companies that are perfect for value investors, offering a P/E of 15x (compared with 18x for US small caps) and attractive dividend yields.

This theme was built using companies with market capitalizations below CHF 2 billion, P/E less than 18 and used a standard GARP (growth-at-areasonable price) model to uncover the most attractive stocks.

Swiss Small Gems theme can now be trading in an easy to execute Strategic Certificate.

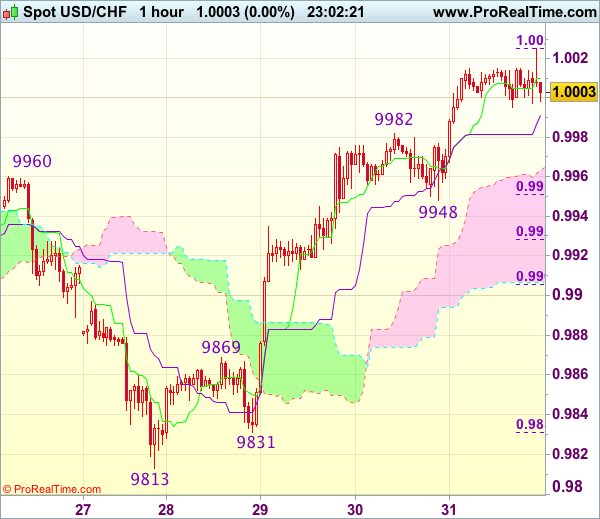

Trade Idea Wrap-up: USD/CHF – Buy at 0.9950

USD/CHF - 1.0006

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.0010

Kijun-Sen level : 0.9991

Ichimoku cloud top : 0.9963

Ichimoku cloud bottom : 0.9907

Original strategy :

Buy at 0.9950, Target: 1.0050, Stop: 0.9915

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9950, Target: 1.0050, Stop: 0.9915

Position : -

Target : -

Stop : -

As the greenback has eased after rising to 1.0025 in NY morning, suggesting minor consolidation below this level would be seen and pullback to 0.9980 cannot be ruled to, however, reckon 0.9948-51 (previous support and 38.2% Fibonacci retracement of 0.9831-1.0025) would limit downside and bring another rise later, above said resistance at 1.0025 would extend the rise from 0.9813 towards previous support at 1.0060 (now resistance) but loss of upward momentum should prevent sharp move beyond resistance at 1.0109.

In view of this, would not chase this rise here and would be prudent to buy dollar on pullback as said support at 0.9948 should limit downside. Below 0.9925-30 (50% Fibonacci retracement of 0.9831-1.0025) would abort and signal top is formed instead, bring correction to 0.9905 (61.8% Fibonacci retracement) but reckon previous resistance at 0.9869 would hold from here.

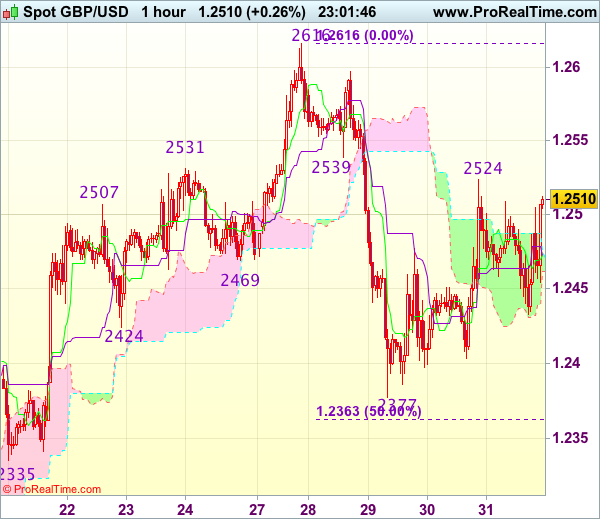

Trade Idea Wrap-up: GBP/USD – Stand aside

GBP/USD - 1.2511

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2476

Kijun-Sen level : 1.2476

Ichimoku cloud top : 1.2476

Ichimoku cloud bottom : 1.2462

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As cable has rebounded again after finding support at 1.2433, retaining our view that further consolidation above this week’s low at 1.2377 would be seen and another bounce to 1.2524 and possibly 1.2550 cannot be ruled out, however, as broad outlook remains consolidative, reckon upside would be limited to 1.2575-80 and price should falter below 1.2600, bring retreat later.

On the downside, whilst pullback to the Kijun-Sen (now at 1.2478) cannot be rued out, reckon downside would be limited to 1.2450 and said support at 1.2433 should hold. Only break of 1.2433 support would revive bearishness and suggest the rebound from 1.2377 has ended, bring weakness to 1.2400, break there would confirm and retest of 1.2377 would follow.

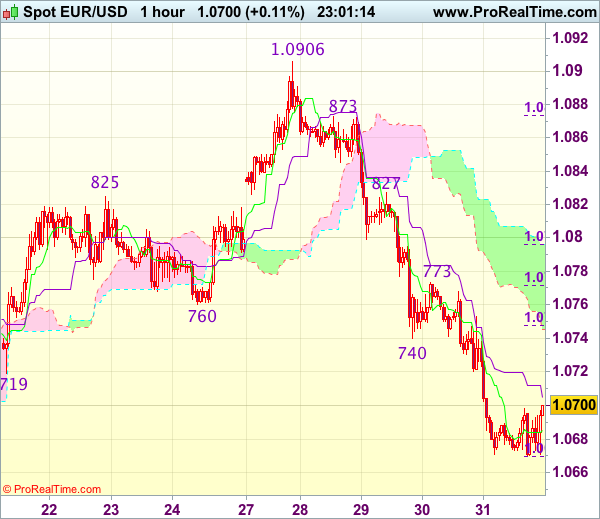

Trade Idea Wrap-up: EUR/USD – Sell at 1.0765

EUR/USD - 1.0690

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.0686

Kijun-Sen level : 1.0705

Ichimoku cloud top : 1.0796

Ichimoku cloud bottom : 1.0745

Original strategy :

Sell at 1.0745, Target: 1.0645, Stop: 1.0780

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0765, Target: 1.0645, Stop: 1.0800

Position : -

Target : -

Stop : -

As this week’s selloff has kept euro under pressure, adding credence to our bearish view that top has been formed at 1.0906 and bearishness remains for the decline from there to extend further weakness to 1.0660, then 1.0640, however, near term oversold condition would limit downside and reckon previous strong support at 1.0600 would hold from here, bring rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 1.0765-70 should limit upside. Only a firm break above resistance at 1.0773 would suggest low is formed instead, bring a stronger rebound to 1.0800 but resistance at 1.0827 should remain intact.

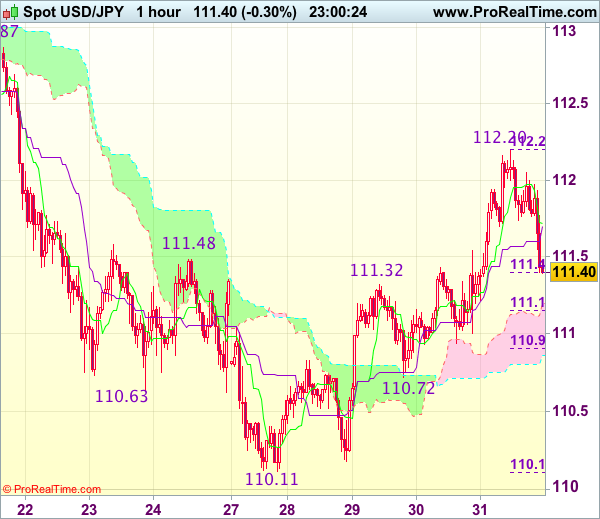

Trade Idea Wrap-up: USD/JPY – Stand aside

USD/JPY - 111.47

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 111.72

Kijun-Sen level : 111.70

Ichimoku cloud top : 111.20

Ichimoku cloud bottom : 110.86

Original strategy :

Buy at 111.30, Target: 112.30, Stop: 110.95

Position : -

Target : -

Stop : -

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As the greenback has retreated after intra-day initial rise too 112.20, suggesting top has possibly been formed there and downside risk is seen for weakness to 111.10-15 (50% Fibonacci retracement of 110.11-112.20), however, break of 110.91 (61.8% Fibonacci retracement) is needed to add credence to this view, bring further fall to support at 110.72 first.

On the upside, expect recovery to be limited to 112.00 and said resistance at 112.20 should hold from here, bring another retreat. Only break of resistance at 112.20-26 would revive bullishness and extend the rise from 110.11 to 112.50-55 but price should falter below previous resistance at 112.87-90, bring retreat later. As near term outlook has turned mixed, would be prudent to stand aside for now.

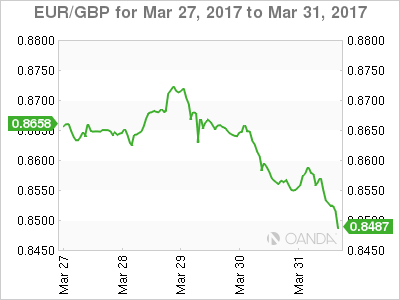

Trade Idea: EUR/GBP – Sell at 0.8620

EUR/GBP - 0.8586

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term down

Original strategy :

Sell at 0.8620, Target: 0.8520, Stop: 0.8660

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.8620, Target: 0.8520, Stop: 0.8660

Position : -

Target : -

Stop : -

As the single currency has remained under pressure after this week’s selloff, adding credence to our view that top has been formed at 0.8788 and downside bias remains for the fall from there to bring retracement of early upmove, hence further weakness to 0.8520-25 would be seen, however, oversold condition should prevent sharp fall below 0.8509 support, risk from there has increased for a rebound to take place later.

In view of this, we are looking to sell euro on recovery as 0.8620-25 should limit upside. Only above 0.8660-65 would defer and suggest low is possibly formed, risk rebound to 0.8680, then 0.8700 but price should falter below said resistance at 0.8735, bring further choppy trading later.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.