Sample Category Title

Yen Quiet Ahead of Japanese Retail Sales

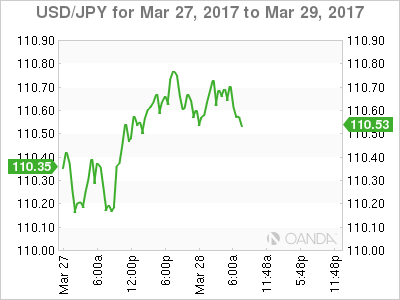

The Japanese yen has edged higher in the Tuesday session. In the North American session, USD/JPY is trading at 110.40. On the release front, today's highlight in the US is CB Consumer Confidence, which is expected to dip to 113.9 points. Japan will release Retail Sales, with the indicator expected to dip to 0.7%.

Donald Trump is used to getting his way in the private sector and on reality TV, but he had to swallow a bitter pill last week as he suffered his first major setback as president. His bill to replace the Affordable Care Act was pulled before it even went to a vote on the House floor, despite the Republicans enjoying a majority in Congress. This bruising defeat has sent the US dollar sharply lower, and sent market jitters higher. Trump's administration has stumbled out of the starting gate, and after more than two months in office, he has yet to provide any details over even an outline of economic policy. The inquiry into the Trump administration's links with Russia is gathering steam, and is another cause for concern for nervous investors. Trump has said he will now focus on tax reform, but he has his work cut out, trying to convince a skeptical Congress and general public that he can push his agenda through Congress.

On Monday, the Bank of Japan released a summary of the minutes of its policy meeting on March 16. There were no surprises, as policymakers said the BoJ's ultra-easy monetary stance would continue as long as inflation remains well below the target of 2 percent. Japan's economy has improved in recent months, boosted by a stronger manufacturing sector and an increase in exports, but domestic demand remains soft, resulting in weak inflation levels. We'll get a look at consumer indicators this week, with the release of retail sales on Tuesday, followed by household spending and Tokyo Core CPI on Thursday.

EURUSD: Hesitates, Faces Pullback Threats

EURUSD: With the pair now seen threatening a move lower, it looks to extend corrective pullback. On the upside, resistance comes in at 1.0900 level with a cut through here opening the door for more upside towards the 1.0950 level. Further up, resistance lies at the 1.1000 level where a break will expose the 1.1050 level. Conversely, support lies at the 1.0800 level where a violation will aim at the 1.0750 level. A break of here will aim at the 1.0700 level. All in all, EURUSD faces pullback threats on price failure.

FTSE Attempted to Fill Monday’s Gap

FTSE attempted to fill Monday's gap on extension of bounce from fresh low at 7179, but rally was so far short-lived, failing to benefit more on bullish signal from yesterday's Hammer.

Pound's correction lower provided temporary relief to the index, but prevailing tone on daily chart remains negative and keeps the downside at risk.

We look for today's close below cracked 55SMA (currently at 7230) for strong bearish signal for fresh attack at 7279 low (also daily cloud top / Fibo 61.8% of 7024/7444 upleg) that marks pivotal point and trigger for further downside.

The price may spend some time in consolidation, with upside attempts expected to hold below 7250 and keep negative near-term structure.

Conversely, extended recovery through 7250/80 pivots would generate initial reversal signal, with lift above 7311 (converged daily Tenkan-sen / Kijun-sen line, still in bullish setup), needed to confirm.

Res: 7231; 7250; 7280; 7311

Sup: 7210; 7179; 7123; 7100

Dow is Consolidating in 20500 Zone

Dow is consolidating in 20500 zone on Tuesday after extension of pullback from 21160 peak hit fresh low at 20355 on Monday. Rising 55SMA contained dip, offering solid support at 20393 today.

Yesterday's strong downside rejection that left long-tailed Doji candle, signals indecision that may result in extended consolidation.

Upside attempts were so far capped by falling and thickening hourly cloud that prevents near-term studies of further strengthening.

Daily technicals are weak and favor renewed attacks at 55SMA, break of which would expose the top of rising daily cloud (currently at 20318), which is expected to ideally contain correction from 21160.

Meantime, extended upticks cannot be ruled out, with initial barrier at 20607 (broken Fibo 38.2% of 19713/21160) and daily Tenkan-sen (currently at 20692) expected to cap.

Res: 20539; 20607; 20663; 20692

Sup: 20498; 20437; 20393; 20355

Markets Take a Risk Pause, Brexit Divorce Next

Tuesday March 28: Five things the markets are talking about

The GOP's healthcare failure has not derailed market sentiment about fiscal stimulus it has temporarily modified it.

For now, with the pendulum of U.S political momentum having swayed in favor of 'gridlock' continues to hamper the "big" dollars natural progress and pressure both bond yields and equity prices.

However, in relatively quiet trading, that pace of decline has subsided somewhat overnight. To reignite capital markets bullish momentum investors will want to see concrete details about U.S tax reforms, infrastructure spending and deregulation.

It's believed that President Trump is prepared to work more with the Democrats, after feeling burned by sectors of his own party, while combining tax reform with an infrastructure investment initiative that may be an easier sell to the 'left.'

Remember, legislative gridlock stateside is not unusual, just look to the final years of the Obama administration, yet the stock market and the U.S dollar performed somewhat admirably.

U.K. Prime Minister Theresa May will tomorrow formally trigger the start of two-years of Brexit negotiations with a letter announcing Britain's planned withdrawal from the EU.

1. Global equities stop the bleeding

The selloff in riskier global assets has eased, with most equity markets resuming their upward trajectories as the dollar steadies after U.S stocks staged a recovery on Monday.

In Japan, the Nikkei share average rebounded (+1.1%) from a more than six-week low overnight as a rally in the yen (¥110.66) paused and investors bought high-yield stocks before they went ex-dividend. The broader Topix gained +1.3%.

In Hong Kong, stocks resisted China's downdraft and followed Asia higher on cautious hopes that U.S. President Trump would eventually be able to pass his planned economic stimulus policies. The Hang Seng index rose +0.6%, while the China Enterprises Index also gained +0.6%.

In China, stocks fell overnight on concerns about tightening liquidity conditions after the People's Bank of China (PBoC) refrained from injecting short-term funds into the banking system for the third consecutive session. The blue-chip CSI300 index fell -0.2%, while the Shanghai Composite Index lost -0.4%.

In Europe, equity indices are trading generally higher across the board. Banking stocks are mixed in the Eurostoxx, while commodity and mining shares support the FTSE 100.

U.S stocks are set to open little changed (+0.1%).

Indices: Stoxx50 +0.3% at 3,446, FTSE flat at 7,294, DAX +0.6% at 12,067, CAC-40 flat at 5,017, IBEX-35 +0.4% at 10,346, FTSE MIB +0.4% at 20,205, SMI +0.2% at 8,611, S&P 500 Futures +0.1%

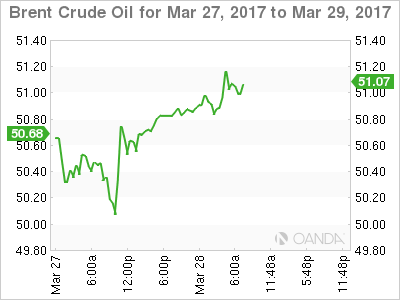

2. Oil rises on weak dollar, but bloated supply still weighs, gold steady

Currently, oil prices are being supported by a weaker dollar, but these prices gain are somewhat capped by surging U.S production and market uncertainty over whether an OPEC-led supply cut is big enough to rebalance the global market.

Prices for front-month Brent crude futures have gained +18c from Monday's close to +$50.93 per barrel, while West Texas Intermediate (WTI) crude futures are up +20c at +$47.93 a barrel.

Note: The greenback has lost -3% in March vs. G10 currencies on U.S political doubts.

Soaring production stateside and packed inventories have made U.S WTI crude much cheaper than international Brent, which is being supported above $50 per barrel by last Nov. OPEC-led output cut.

Note: Last weekend, an OPEC and non-OPEC Joint Compliance Committee agreed to review whether oil output cuts should be extended by six-months. They stopped short of an earlier draft statement that said the committee recommended keeping the Nov. measure in place.

Ahead of the U.S open, gold prices (+$1,253.83) are steady as investors look to see if President Trump would be able to enact promised tax cuts and infrastructure spending.

Note: The 'yellow' metal has already rallied sharply from its Mar. 15 low ($1,197.18) following a less-hawkish-than-expected policy statement from the Fed.

3. Global yields struggling to climb

The uncertainty surrounding the Trump administration's ability to deliver on policy proposals is weighing on investor expectations for higher U.S interest rates.

Bets that the Fed will raise rates in June have fallen to +48.5% from +54% on Friday. Also, the market is pricing in a +52% chance that the Fed will raise rates at least two more times this year, compared to +55% on Friday.

This week's supply concentrates on shorter-dated U.S Treasuries, which explains why short-term product is underperform longer-dated bonds.

Despite lower yields, foreign demand for yesterday's $26B U.S 2-year auction (+1.26%) was the highest since Feb 2016. A proxy for foreign demand, indirect bidding, was +53.6%. The bid-to-cover ratio (overall demand) was 2.73 vs. the average of 2.64 for the past six-sales.

Note: The alternative product for the Euro investor is the German 2-year Schatz, but the similar maturity currently has a yield below zero (-0.71%).

U.S 10 year notes are little changed, up +1 bps at +2.39%.

4. Dollar Vols for the 'big-three' rise

With the U.S dollar having weakened to a four-month low amid fears the Trump administration won't be able to deliver on its policy goals has volatility (Vols) in some major currency pairs trading atop of their multi-week highs.

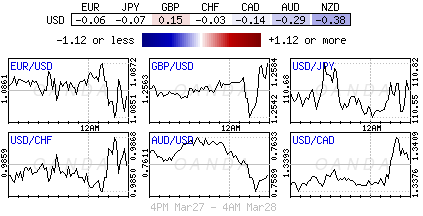

Implied volatility for JPY over the next-month has risen to its highest level since March 3. Implied volatility in the EUR is at its highest level since Feb. 23. While GBP is little changed week-over-week, despite the pound topping £1.2600 yesterday for the first time since Feb 1.

Note: U.K. Prime Minister Theresa May will tomorrow formally trigger the start of two-years of Brexit negotiations with a letter announcing Britain's planned withdrawal from the EU.

EUR/USD is steady at €1.0860, USD/JPY at ¥110.65 and GBP/USD moving back towards the psychological £1.26 level.

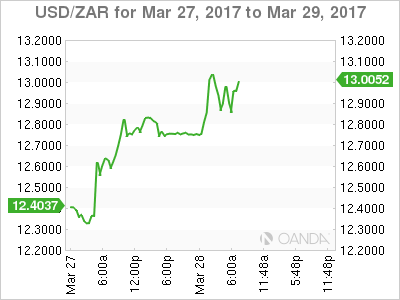

5. Rand Collapses As Zuma Threatens to Sack Finance Minister

South Africa's rand (ZAR) took another tumble overnight when President Zuma's suddenly decided to recall his finance minister, Pravin Gordhan, from London. Investors are viewing this as a sign of escalating tensions between the two.

Note: The general feeling is that the only thing standing between South Africa and a multi-agency downgrade of its sovereign debt to junk status is Mr. Gordhan.

The ZAR lost more than -2% to $13.0968 outright, after having dropped -2.4% yesterday in its steepest intraday loss in six-months.

Yields in dollar-denominated sovereign debt and local government benchmark bonds also jumped. Prior to this drop, the currency had gained +9.5% year-to-date, making it a top EM performer.

USD/CAD – Canadian Dollar Under Pressure At 1.34 On Trump Concerns

USD/CAD has posted small gains on Tuesday, continuing the upward trend which marked the Monday session. Currently, the pair is trading at the 1.34 level. On the release front, it's another quiet day. In the US, today's highlight is CB Consumer Confidence, which is expected to dip to 113.9 points. The sole event in Canada is a speech from BoC Governor Stephen Poloz in Oshawa.

Donald Trump is used to getting his way in the private sector and on reality TV, but he had to swallow a bitter pill last week as he suffered his first major setback as president. His bill to replace the Affordable Care Act was pulled before it even went to a vote on the House floor, despite the Republicans enjoying a majority in Congress. This bruising defeat has sent the US dollar sharply lower, and sent market jitters higher. Trump's administration has stumbled out of the starting gate, and after more than two months in office, he has yet to provide any details over even an outline of economic policy. The inquiry into the Trump administration's links with Russia is gathering steam, and is another cause for concern for nervous investors. Trump has said he will now focus on tax reform, but he has his work cut out, trying to convince a skeptical Congress and general public that he can deliver the goods and pass new, effective legislation.

Weaker oil prices could weigh on the soft Canadian dollar. West Texas crude has dropped 1.0% in March, and dipped to $47.05 last week, its lowest level since the end of November. Crude headed lower after Crude Oil Inventories posted a strong surplus of 5.0 million barrels, crushing the estimate of 1.9 million. The weekly indicator has recorded only two declines in 2017, as US oil drillers continue to enter the market and ratchet up US oil production. This, together with increased US shale production, has more than offset OPEC's production cuts. Last week, OPEC announced it was considering extending the production cut agreement by another 6 months, until the end of 2017, but it's doubtful that such a move will prop up oil prices.

Staying Positive In USDJPY Despite Near-Term Weakness

Trump administration's failure to repeal and replace Obamacare has hurt market sentiment, triggering concerns over the feasibility of the president's pro-growth policy agenda. In the FX market, US dollar fell across the board amidst concerns that reflation trades since Trump's victory is over. The DXY index dived to a 4-month low of 98.86 on Monday before recovery. USDJPY also plunged to 110.09, lowest since November 18, 2016, before stabilizing. As we mentioned in the January report, it would not be surprising to see USDJPY correct to 110-112 in 1Q17. Therefore, the current price movement has not yet derailed our forecast although Trump's implementation ability has surprised to the downside. While it cannot be ruled out that the currency pair might break below 110 briefly, we retain the forecast that USDJPY should recover to 115 and then to 117 later this year.

Trump pulled the healthcare bill (AHCA) from the House minutes before vote, due to the lack of support, last Friday. The House healthcare vote was important, in a sense that it is the first Congressional vote on a key policy issue and it has big implication on the advancement of the wider tax reform agenda. While the government has decided to move on and focus on tax reform bills which are thought to be simpler, investors are concerned the failure of AHCA would provide less fiscal headroom for the tax plans, not to mention the divisions within Republicans. The White House aims at passing the comprehensive tax reform legislation by August, well before the 2018 mid-terms. However, the obstacles are obvious as there are limited sources of revenue to offset the proposed tax cuts, which are substantial. The border adjustment tax (BAT) proposal is another challenge.

Besides AHCA's failure, recent USD weakness has been driven by a less-hawkish-than-expected Fed. Following the March rate hike, the Fed is expected to remain on the sideline at least until June, although the market has recently priced in lower chance of such a move. The March rate hike was not unanimous with Minneapolis Fed President Neel Kashkari favoring leaving the monetary policy unchanged. The FOMC statement showed virtually no change in the macroeconomic projections and maintained three rate hikes this year in the median dot plot.

Median Dot Plots Continued to Project 3 Rate Hikes in 2017 and 2018

USD's liquidity conditions remain upbeat. USDJPY basis swap spreads showed that the cost to borrow dollars in exchange for yen reached 23.8 bps last Friday before returning to 30-ish levels. Narrowing in cross currency basis suggests reduction in hedging cost. It also signals abundance USD funding relative to JPY's, pressuring USDJPY in the near-term.

In the medium-term, we remain positive over USDJPY, or US dollar in general. The next move for the Fed is a rate hike, rather than a rate cut. Policymakers would turn more upbeat should incoming macroeconomic data remain strong. Moreover, we believe USD as well as Treasury yields would be lifted as we come closer to the next rate hike.

USD And Indices Bounce As Technical Support Holds

US equity markets are poised to open slightly higher on Tuesday, building on the recovery we saw throughout yesterday's session after indices started the week lower in response to Donald Trump's failed healthcare bill.

Equity markets rebound after questions raised over Trump's ability to deliver

The failure to generate support for the bill despite delivering a last ditch ultimatum to lawmakers is seen as potentially being a sign of weakness and even political naivety from Trump which has cast doubt on whether he'll face similar problems when it comes to his other policies. Ultimately, the more than 15% rally in equity markets, along with the rise in the US dollar and Treasury yields, since Trump's victory has been built on the belief that he will deliver and if doubts are in fact creeping in, those gains will start to disappear.

Another explanation could simply be that investors are capitalising in on Trump's healthcare issues – a policy that was not a key driver of the rally since November – and locking in some profit on the move. Once markets get back to more attractive levels, we may once again see the dips being bought and optimism in Trump to deliver on tax reform and fiscal stimulus will suddenly return as well. With Trump promising to move on to tax reform now that the healthcare bill failed, we may not have to wait too long for investors to become more optimistic again. That said, if tax reform fails then investors will not be so forgiving.

Key technical support levels being tested in the Dow, S&P and USD

If the latter is true, then the question becomes at which point do investors start seeing value again. The Dow and S&P both rebounded yesterday off their 55-day SMA, the first time they've threatening to break below here since shortly after the election in November. The fact that this coincided with a similar bounce in the US dollar index of its 200-day SMA would suggest both are testing significant support levels at the moment and a break of these could trigger further losses.

Yellen one of four Fed officials making an appearance today

There isn't much to watch on the economic calendar today, with CB consumer confidence and API oil inventories the only notable releases. We will, however, hear from four Fed officials including Chair Janet Yellen. Given how markets have responded to the dovish hike this month, it will be interesting to see whether policy makers remain along these lines or start talking up the prospect for another hike in June.

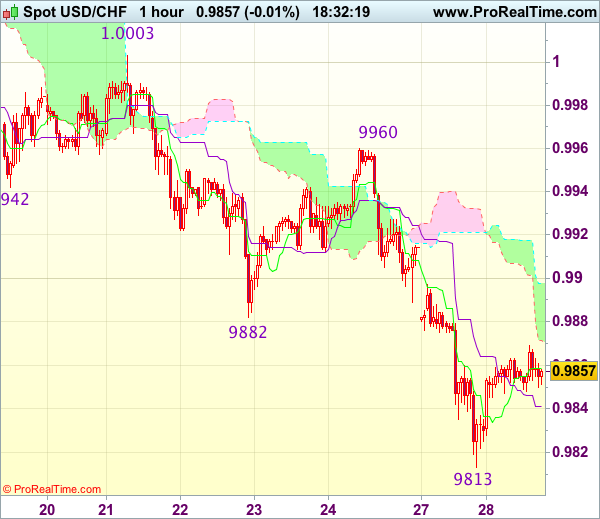

Trade Idea Update: USD/CHF – Sell at 0.9910

USD/CHF - 0.9855

Original strategy :

Sell at 0.9910, Target: 0.9800, Stop: 0.9945

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9910, Target: 0.9800, Stop: 0.9945

Position : -

Target : -

Stop : -

The greenback found support at 0.9813 yesterday and has recovered, suggesting consolidation above this level would be seen and corrective bounce to 0.9880 is likely but upside should be limited to 0.9900-10 and bring another decline later, below said support at 0.9813 would confirm recent decline has resumed and extend weakness to 0.9795-00, however, loss of downward momentum should prevent sharp fall below 0.9770-75 (100% projection of 1.0171-0.9942 measuring from 1.0003), bring rebound later.

In view of this, would not chase this fall here and we are looking to sell dollar on subsequent rebound as 0.9900-10 should limit upside. Only above said resistance at 0.9960 would abort and signal low is formed, bring retracement of recent decline towards indicated previous resistance at 1.0003.

DAX Punches Above 12,000 As Investors Await Next Trump Move

The DAX Index has edged upwards on Tuesday, as the DAX trades at 12,069.50. It's a quiet day on the release front, with no eurozone events on the schedule. On Wednesday, Germany releases Import Prices, which is expected to dip to 0.4%.

The DAX has pushed above the symbolic 12,000 level this week, bolstered by an excellent reading from German Ifo Business Climate, which rose to 112. 3 points. This marked its highest level since July 2011. The release underscores high optimism in the business sector, despite rumblings of protectionism from the US and the uncertainty in Europe over the imminent Brexit negotiations. Germany, the largest economy in Europe, continues to post strong numbers, which has been good news for the eurozone economy. Last week's PMIs pointed to expansion in the manufacturing and service sectors. German and eurozone Manufacturing PMIs both beat their estimates and hit their highest levels since 2011. Later this week, Germany releases key indicators, including CPI, retail sales and unemployment claims. One soft spot in the economy, however, is consumer confidence. GfK German Consumer Climate lost ground for a second straight month, as the indicator dropped to 9.8 in March, its lowest level since November 2016. Eurozone Consumer Confidence remains weak, as the indicator posted a decline of -5 in March, almost unchanged from a month earlier. These soft numbers are largely a result of higher inflation, as consumers are concerned about their reduced purchasing power. If inflation levels head higher, consumers could respond by curtailing spending, which could hamper economic growth.

Donald Trump is used to getting his way in the private sector and on reality TV, but he had to swallow a bitter pill last week as he suffered his first major setback as president. His bill to replace the Affordable Care Act was pulled before it even went to a vote on the House floor, despite the Republicans enjoying a majority in Congress. This bruising defeat has sent the US dollar sharply lower, and sent market jitters higher. Trump's administration has stumbled out of the starting gate, and after more than two months in office, he has yet to provide any details over even an outline of economic policy. The inquiry into the Trump administration's links with Russia is gathering steam, and is another cause for concern for nervous investors. Trump has said he will now focus on tax reform, but he has his work cut out, trying to convince a skeptical Congress and general public that he can deliver the goods and pass new, effective legislation