Sample Category Title

Pound Dips as US Consumer Confidence Soars

GBP/USD has edged lower in Tuesday's North American session. Currently ,GBP/USD is trading at 1.2530. On the release front, it's another quiet day, with no UK events on the schedule. In the US, CB Consumer Confidence rocketed to 125.5, crushing the estimate of 113.9. There was also good news on the manufacturing front, as the Richmond Manufacturing Index improved to 22, well above the forecast of 16 points.

The dollar is showing some strength in North American trading, courtesy of a spectacular reading from CB Consumer Confidence. The key indicator surprised the markets by climbing to 125.5, its highest level since December 2000. Clearly, consumers remain optimistic about the economy, and a major factor in this sentiment is the red-hot labor market, which remains close to capacity. An increase in consumer confidence often translates into stronger consumer spending, which would be bullish for the US dollar, which has headed lower since the Federal Reserve rate hike on March 15. We'll get a look at consumer spending data on Friday, with the release of Personal Spending.

Donald Trump suffered his first major setback as president last week, as his bill to replace the Affordable Care Act was pulled before it even went to a vote. Trump is used to giving the orders in the private sector and on reality TV, but he didn't get his way on healthcare, despite the Republicans enjoying a majority in Congress. This bruising defeat has sent the US dollar sharply lower, and sent market jitters higher. Trump's administration has stumbled out of the starting gate, and after more than two months in office, he has yet to provide any details over even an outline of economic policy. The inquiry into the Trump administration's links with Russia is gathering steam, and is another cause for concern for nervous investors. Trump has said he will now focus on tax reform, but he has his work cut out, trying to convince a skeptical Congress and general public that he can deliver the goods and pass new, effective legislation.

Britain departure from the European Union will move into second gear on Thursday, as the government formally gives notice to its EU colleagues of its intent to withdraw from the club. However, actual negotiations between the parties may not commence until June, according to recent statements from EU policymakers. The negotiations are supposed to be conducted over a two-year period, and promise to be tough and perhaps acrimonious. The EU cannot afford to "go easy" on the UK and give it a sweet deal, since this would provide ammunition to euro-skeptics on the continent who also want to quit the EU. For its part, the British government needs to reach what it considers a fair deal, and has threatened to leave the EU without a deal if the EU is intransigent in the negotiations.

USD Struggles as Reflation Trade Fails to Resume

Headlines

European stock markets opened around 0.5% higher in a catch-up move and managed to hold on to gains. US stock markets slightly slip away in the opening.

US eco data were stronger than expected. Consumer confidence increased from 116.1 to 125.6 in March, the highest level since December 2000. The Richmond Fed manufacturing index also beat expectations, rising from 17 to 22, the strongest since April 2010. The US trade deficit was smaller than expected in February and housing prices (S&P CS) increased faster than forecast in January.

The ECB improperly veered into political activity during the eurozone crisis and should withdraw from the "troika" of international bailout monitors, according to anti-corruption watchdog Transparency International.

South Africa's rand plummeted for a second day as speculation intensified that President Jacob Zuma is preparing to fire his finance minister after summoning him back from an overseas investor roadshow. USD/ZAR temporarily rose above 13.

US President Trump will sign an executive order to undo a slew of Obama-era climate change regulations that his administration says is hobbling oil drillers and coal miners, a move environmental groups have vowed to take to court.

The National Bank of Hungary kept its policy rate unchanged at 0.9%, but the central bank raised its CPI forecast for 2017 to 2.6% in its quarterly Inflation Report from 2.4% in the previous report published in December. It did not change the 3% forecast for 2018 and in a new set of data also predicted 3% inflation in Hungary for 2019.

Rates

Jury still out on future reflation trade

Global core bonds traded with a small upward bias today in an insignificant trading session. The jury is still out on the future of the reflation trade with several markets giving different signals. Stocks and oil prices rise, while the dollar (USD/JPY) and yields are slightly lower. At the time of writing, changes on the German yield curve range between -1.1 bp (5-yr) and +0.8 bps (2-yr). Changes on the US yield curve vary between +0.9 bps (2-yr) and -1.2 bps (30-yr). On intra-EMU bond markets, 10-yr yield spread changes versus Germany narrow up to 3 bps (Italy) with Greece (-14 bps) outperforming.

Intraday, the Bund opened slightly lower in a catch-up move with WS yesterday. During Monday's US trading session, risk sentiment turned positive again, partly reversing the correction on the reflation trade after Friday's failed health care bill. There was no follow-though Bund selling and the Bund/US Note future even traded with an upward bias throughout today's session. A miserable German Schatz auction, a smaller than expected February trade deficit and higher than forecast housing data (S&P CS) had no impact on trading. Today's rise of global core bonds occurred despite rising oil prices and stock markets. There are plenty central bank speakers tonight, but the topics of their speeches suggest that they won't touch upon monetary policy/sensitive information for markets.

The German Finanzagentur's €4B 2-yr Schatz auction (€4B 0% Mar2019) went miserably. Total bids amounted only €3.19B, way below the €5.49B average at the previous 4 Schatz auctions and below the amount on offer. As the Bundesbank set aside €1.11B for secondary market operations, the official bid cover was 1.1 instead of 0.8. The auction tailed 1.3 cent, which is also unusual for Schatz auctions. The US Treasury continues its end-of-month refinancing operation tonight with a $34B 5-yr Note auction. Currently, the WI trades around 1.91%. .

Currencies

USD struggles as reflation trade fails to resume

USD traders still haven't found a clear guide in the wake of the debacle of the US healthcare vote on Friday. Yesterday evening, the dollar decline slowed as US equities found their composure. However, it is too early for investors to engage further in the reflation trade. Uncertainty and a further (modest) slide in core yields weighs on USD/JPY. After a strong performance yesterday, the euro didn't go anywhere today. EUR/USD is locked in the mid 1.08 area.

Overnight, Asian equities joined yesterday's intraday rebound in the US, but the gains were modest. This was also the case for the comeback of the dollar. USD/JPY rebounded temporary to the 110.80 area, but returned soon to the mid 110 area. EUR/USD hovered in the 1.0865 area. So, yesterday's top just north of 1.09 was still within reach.

European investors didn't really know which card to play. European equities caught up with yesterday's late session rebound in the US but there was no trigger to start a new sustained up-leg in the global reflation trade. Indecisiveness again prevailed. USD/JPY stabilized in a narrow range in the mid 110 area. EUR/USD also didn't go anywhere and settled near 1.0850. The German 2-yr auction went quite difficult. There was no direct impact on the euro, but lingering market speculation on an early reduction of ECB policy stimulation suggests that USD sentiment will have to improve in quite a profound way to support a sustained comeback of the dollar against the euro anytime soon.

Risk sentiment deteriorates slightly as US traders joined the action. The move was probably still due to investors adapting positions in the wake of the Trumpcare debacle. The US February trade deficit was slightly smaller than expected at $64.8B, but didn't help the dollar. Contrary to what was the case yesterday, USD/JPY again faced the strongest headwinds. The pair is trading in the 110.30 area. The recent low (110.10 area) is again on the radar. The loss of the dollar against the euro remains limited. EUR/USD is going nowhere in the mid 1.08 area.

Sterling traders await formal start of Brexit procedure

There were again no eco data in UK today. So, sterling trading was driven by technical considerations. Investors were looking forward to tomorrow's formal start of the Brexit procedure as UK PM May will send a letter to EU's Tusk to activate article 50 of the Lisbon Treaty. Sterling traded with a positive bias early in the session, but returned (modest) gains against the dollar and the euro later. The activation of Article 50 is of course no surprise, but the letter might also contain some indication on the UK's negotiation targets. So, it might be a first technical move in a long Brexit saga. For now, sterling remains unmoved. EUR/GBP trades in the 0.8650 area. Cable is at 1.2550.

Turbulence in Store for Trump and the US?

What you may have missed last week - and what to watch out for this week...

- A busy week for the UK and its trading partners

- Turbulence in store for Trump and the US?

- European energy dampened by the Dollar

- Surprises in store for New Zealand

A busy week for the UK and its trading partners

World markets are braced for an exciting week ahead, as UK Prime Minister, Theresa May, fires the Article 50 starting gun and the UK's trade negotiations across the globe begin in an official capacity. With the level of "certainty" that the triggering of Article 50 brings, Sterling is doing well, but the week ahead is likely to see currency market volatility as events unfold.

There will also be a veritable flurry of UK economic data, which, when teamed with the Article 50 launch, could cause some ups and downs for Sterling against its major currency partners. Key data due to be released includes house price index stats, UK mortgage data, Quarter Four Gross Domestic Product (GDP) figures, and the UK government's figures regarding the current account deficit.

Turbulence in store for Trump and the US?

The US Dollar has weakened as President Donald Trump has failed to launch his second major policy change after being thwarted by his own party. What he termed as the demolition of Obamacare has become an embarrassment for the President and his supporters. Final Q4 GDP growth figures are expected for the US this week, too, which are anticipated to be much the same as the previous assessments, although you never know in these unprecedented times. The US Dollar is at levels against the Euro not seen since a brief spike at the end of 2016, hovering around the $1.08 mark.

European energy dampened by the Dollar

The Euro, meanwhile, has crept up a little recently, but its fortunes are tied closely to the US Dollar and its recent weakness. Europe is also expecting some important news on the economic front – European Central Bank (ECB) and European Union (EU) speakers are scheduled this week; and there will be the final March inflation data, alongside business and consumer confidence indices. These are always a good benchmark of the economic state of play. The ECB is still confident that the European economic expansion will continue but events in Europe are playing out against a backdrop of contentious presidential elections in France and Germany, which have the capacity to deal a considerable blow to the Euro.

Surprises in store for New Zealand

On the other side of the globe, New Zealand released their latest trade balance figures. The markets had forecast a small surplus but the data actually showed a deficit of 18 million New Zealand Dollars. The Reserve Bank of New Zealand (RBNZ) kept interest rates at 1.75% as, was widely anticipated but the NZ Dollar is under pressure in spite of improving commodity markets which benefit NZ exporters.

Elliott Wave Analysis: Silver Trading In A Bullish Impulse

On the hourly chart of Silver, we see commodity undergoing a nice impulsive sequence to the upside, with price specifically trading in sub-wave v of three. That said, current sub-wave v may extend its gains towards the 161.8 or even higher to the 261.8 Fibonacci projected ratio, before making a new reversal to the downside. After sub-wave v of three finds a top, a minimum three wave correction may follow into the following wave 4.

SILVER, 1H

Trade Idea: EUR/GBP – Hold long entered at 0.8620

EUR/GBP - 0.8663

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term down

Original strategy :

Bought at 0.8620, Target: 0.8750, Stop: 0.8600

Position : - Long at 0.8620

Target : - 0.8750

Stop : - 0.8600

New strategy :

Hold long entered at 0.8620, Target: 0.8720, Stop: 0.8600

Position : - Long at 0.8620

Target : - 0.8720

Stop : - 0.8600

As the single currency found support just above last week’s low at 0.8605 and has rebounded, retaining our bullishness and as long as this support holds, mild upside bias remains for another rebound, a break of indicated resistance at 0.8700 would bring test of 0.8727, above there would suggest low is formed, then gain to 0.8760 would follow, break there would suggest the pullback from 0.8788 has ended, bring retest of this level, a breach there would extend the rise from 0.8403 low to 0.8800 and later 0.8825-30.

In view of this, we are holding on to our long position entered at 0.8620. A firm break below 0.8605 (50% Fibonacci retracement of 0.8422-0.8788) would defer and suggest top has possibly been formed at 0.8788, risk test of 0.8560-65 (61.8% Fibonacci retracement) but support at 0.8547 should remain intact.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

Trade Idea: USD/CAD – Stand aside

USD/CAD - 1.3379

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term up

Original strategy :

Exit short entered at 1.3400,

Position: - Short at 1.3400

Target: -

Stop: -

New strategy :

Stand aside

Position: -

Target: -

Stop:-

The greenback edged higher and further consolidation above 1.3326 support would be seen, a firm break above 1.3415 would signal low has been formed at 1.3264 last week, bring a stronger rebound to 1.3450 and possibly test of resistance at 1.3479 but only break of 1.3495 resistance would indicate the pullback from 1.3535 has ended and bring retest of this level later.

In view of this, would be prudent to stand aside for now. Below 1.3326 would revive bearishness, bring retest of said last week’s low at 1.3264, break there would add credence to our view that top has been made at 1.3535 earlier this month, bring further fall to 1.3235-40 (61.8% Fibonacci retracement of 1.3056-1.3535) but previous resistance at 1.3210 would hold due to loss of downward momentum.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

Brent Oil Returned above 200 SMA

Brent oil returned above 200 SMA ($50.80), following several unsuccessful attempts to clearly break below it, with one of downticks also briefly probing below psychological $50.00 support.

Overall structure remains weak and sees risk of renewed attempts lower and final break below 200SMA and $50 support.

Daily Tenkan-sen ($51.17) limits upside attempts for now, however, room for further upticks exists.

Strong resistance zone between $52.34 and $52.63 (Fibo 38.2% of $56.62/$49.70 downleg / falling 20SMA / 16 Mar lower top) should cap extended recovery actions, before broader bears resume.

Below $50.00/$49.70 triggers, next good support lies at $49.1 (Fibo 61.8% of $43.56/$58.36).

Res: 51.17; 51.33; 51.57; 52.34

Sup: 50.80; 50.00; 49.70; 49.21

Dollar Crossroads

In a perfect world, every breakout is clean and steady but on Monday the US dollar fell below some critical levels but bounced instead of wilting. We look at what's coming next. Yellen's speech about labout markets due at 12:50 ET (17:50 London). After closing both EURCAD and EURAUD trades at a profit, one of the traded will be re-opened later this evening. Which one will it be? Find out in the Premium video due up shortly.

Yen is again the best performer. followed by the franc and pound, while Kiwi and Aussie are the worst performers. As the healthcare deal fell apart on Friday, it held together. But on Monday as the Republican party looked like it was straining, the dollar began to crumble.

We have been writing about the burgeoning positive signs in the euro for weeks and on Monday it finally broke out. EUR/USD was the big technical story as it broke the February and December highs as it gapped higher. It continued through the 200-day moving average and 1.09 as levels cascaded.

It was similar in GBP/USD and USD/JPY as important levels were tested. What finally stopped the selling was support at 110.00 in USD/JPY and GBPUSD resistance at 1.2640. That held and then sentiment began to turn. The S&P 500 proved it's a juggernaut once again as it erased a 22-point decline to finish just 2 points lower.

Economic news is light. Fundamentally the focus remains on politics. Talk that Republicans hadn't yet given up on healthcare was perhaps the positive spark but that might be stretching it.

Another factor to note was quarter-end and Japanese fiscal year end. Flows will be lumpy and the market will thin in the days ahead. Ideally, the dollar would break and it would extend but given the politics and calendar, it's not a surprise that the market is tentative. There isn't a screaming reason to sell dollars even if Republicans stumbled further. What we will probably see is a continue paradigm where the US dollar has small gains on good news and large losses on bad news.

The Asia-Pacific calendar is light but we note that Japanese economic minister Ishihara said authorities are closely watching market moves. That's soft jawboning but expect more if USD/JPY breaks 110.00.

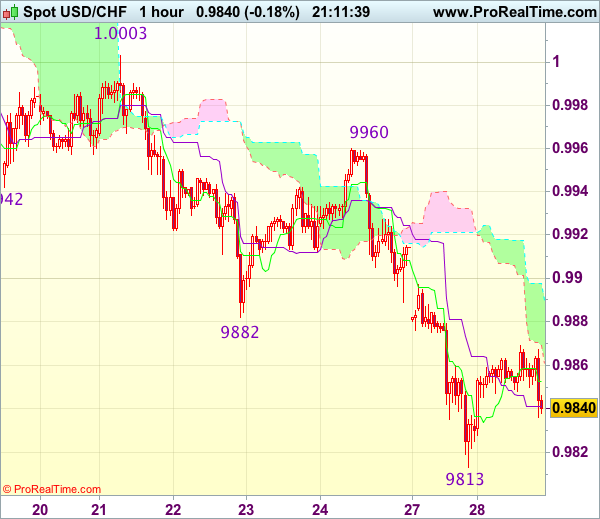

Trade Idea Update: USD/CHF – Sell at 0.9910

USD/CHF - 0.9840

Original strategy :

Sell at 0.9910, Target: 0.9800, Stop: 0.9945

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9910, Target: 0.9800, Stop: 0.9945

Position : -

Target : -

Stop : -

The greenback found support at 0.9813 yesterday and has recovered, suggesting consolidation above this level would be seen and corrective bounce to 0.9880 is likely but upside should be limited to 0.9900-10 and bring another decline later, below said support at 0.9813 would confirm recent decline has resumed and extend weakness to 0.9795-00, however, loss of downward momentum should prevent sharp fall below 0.9770-75 (100% projection of 1.0171-0.9942 measuring from 1.0003), bring rebound later.

In view of this, would not chase this fall here and we are looking to sell dollar on subsequent rebound as 0.9900-10 should limit upside. Only above said resistance at 0.9960 would abort and signal low is formed, bring retracement of recent decline towards indicated previous resistance at 1.0003.

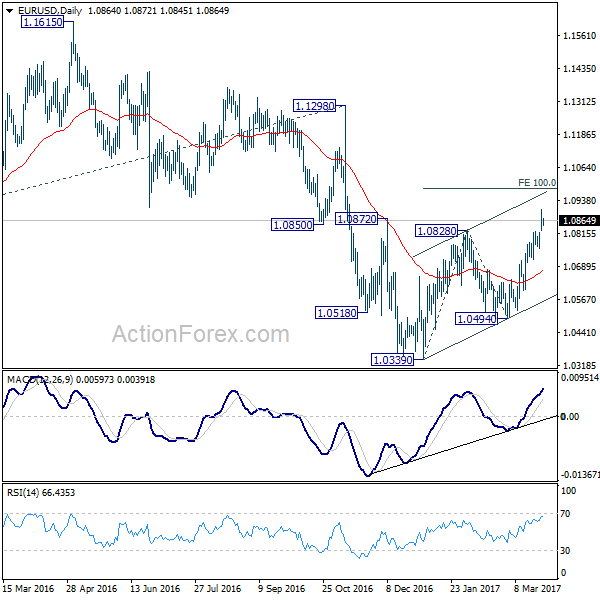

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0822; (P) 1.0864 (R1) 1.0904; More.....

A temporary top is in place at 1.0905 and intraday bias in EUR/USD is turned neutral for some consolidations. Further rise is expected as long as 1.0760 minor support holds. Above 1.0905 will turn bias to the upside for 100% projection of 1.0339 to 1.0828 from 1.0494 at 1.0983. At this point, we're still treating rise from 1.0339 as a correction. Hence, we'd expect strong resistance from 1.0983 to limit upside and bring near term reversal. On the downside, break of 1.0760 support will turn bias back to the downside for 1.0494 support. However, firm break of 1.0983 will dampen our view and put focus on 1.1298 key resistance.

In the bigger picture, as long as 1.1298 key resistance holds, whole down trend from 1.6039 (2008 high) is still expected to continue. Break of 1.0339 low will send EUR/USD through parity to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. However, considering bullish convergence condition in weekly MACD, break of 1.1298 will indicate term reversal. this would also be supported by sustained trading above 55 week EMA.