Sample Category Title

Dollar Darts Ahead, Article 50 Next

Bull markets rarely end in collapse and the US dollar proved that on Tuesday as it roared back to life. The Australian dollar was the top performer while the pound lagged. Japanese retail sales are up next but the big story in the day ahead will be Article 50. After closing both EURCAD and EURAUD trades at a profit, one of pairs will be re-opened later ahead of the Asia Wednesday session. More on the charts rationale in the Premium video below.

We wrote yesterday about how the US dollar was at a crossroads. On Monday, it tumbled early but instead of continuing to wilt, it bounced and that underscored the indecision in the market.

Today, strong economic data and more signs of renewed political resolve gave the dollar a lift. As the gains mounted, the US dollar erased all of Monday's losses to leave it virtually flat on the week.

What had looked like a breakout in EUR/USD is now a trade wracked with questions.

What's clear is that the US dollar won't seriously stumble so long as economic data is improving. On Tuesday, US consumer confidence jumped to 125.6 compared to 114.0 expected; that's the best in 17 years. The Richmond Fed also hit the best since 2010.

The Fed's Fischer made an appearance but offered little we didn't know. He said two more hikes this year was his baseline and that the risks were balanced.

Two things will keep markets off balance in the days ahead. The first is looming quarter end and Japanese fiscal year end. The second is the UK announcement due on Wednesday.

In theory, the announcement is 100% expected and it should be fully priced in. May will likely make the announcement in parliament at noon and the letter will be delivered to Donald Tusk 30 minutes later.

The danger is that GBP flows accelerate after the announcement. In particular, the net cable position is at the most-short on record and that leaves the pair vulnerable to a squeeze.

Before May takes the spotlight, the economic data to watch in Asia-Pacific trading comes at 2350GMT when Japanese retail is released. The BOJ is showing no signs of easing off the gas pedal but a reading better than the +0.3% m/m expected would be a small step in that direction (albeit still not a JPY mover).

AUD/NZD Musings

Back after a long weekend and ready to get stuck into the markets!

Straight back into it and as you can see, we've been watching one particular daily horizontal support/resistance level in AUD/NZD on the blog for a while.

While price has well and truly held above it now, it was this short term coiling type price action that caught my attention, shown here clearly on the 4 hourly chart:

AUD/NZD 4 Hourly:

My only issue with this sort of coiled price type setup is that it's almost too good to be true!

Yes, that might sound a little ridiculous but the textbook clean setups rarely hold their levels to the pip and this is largely why I preach waiting for confirmation of higher time frame levels holding and then entering on short term pullbacks.

So with that in mind, we see price above that horizontal level that's acted as strong support/resistance on both sides dating back literally years. While price is above this level, it's short term pullbacks we'd be looking to buy.

What Dollar Demise

What dollar demise?

The USD regained some semblance of composure overnight as rises in equities, oil prices, and yields provided the scrim for a bustling overnight session where the Greenback showed it’s fortitude while consumers found their confidence. While the Dollar is not out of the weeds by any stretch, US economic data was convincing. The US Consumer Confidence Index came in at 125.6 versus 114.0 as expected, the highest reading since 2000 suggesting the US economic climate will continue to run hot, despite the Presidential approval rating indicating a high degree of discontent among Americans with the current political landscape.

Further underpinning the Greenback were comments from House Speaker Ryan suggesting that the GOP were unified when it comes to tax cuts. News from media website Axios claimed that the Trump administration is looking at driving tax reform and infrastructure concurrently, which was also viewed dollar bullish. After getting hung out to dry by the Tea Party Bulwark House Freedom Caucus, President Trump looks set to dangle the infrastructure carrot in front of the Democrats to win House support, hopefully buffeting GOP ultra conservatives who would likely oppose increasing budget deficits to spend on infrastructure.

With the market underpricing the Fed dot plots, comments from Fed Chair Stanley Fischer also added to the dollar appeal. Widely considered part of Dr Yellen’s inner circle, Fed Chair Fischer sided with the three hike camp for 2017 that reinforced the Firewall around the 2.3% critical support level for US 10 year yields.

Despite the short-term noise, it’s difficult to home in on any particular chrysalis for yesterday’s price action. The randomness of profit taking and position cutting in a session that for the most part, was devoid of any significant conviction suggests that G-10 continues to trade within a very defined channel all the while dollar bulls look for glimmers of hope to re-engage the USD.

Australian Dollar

The AUD flirted with and finally ceded the .76 level overnight, then quickly bounced higher on the improved risk outlook and firming commodity and energy prices. The dormancy in the Aussie dollar suggested a lack of conviction and reinforced that the price action overnight was little more than short-term position squeezes.

With no clear catalysts, I can only lean on rebounding oil prices as the commodity driver. Reuters reported that Libya’s NOC had declared force majeure on loadings of Sharara crude from the Zawiya terminal, confirming earlier reports that Libyan oil output dropped after Sharara/Wafa fields were said to close. The production disruptions will weigh on supply and support oil prices.

The bump in oil prices should have some legs and could provide a welcoming underpin for risk assets through today’s session, keeping the Aussie well clear from overnight lows.

Euro

Short term overbought indicators likely spooked Euro traders, and it took little than a slight dollar bid to chase the near term weaker EUR longs out the back door. However, the market was also weighing comments by ECB chief economist, Peter Praet, who suggested it was premature to discuss a QE exit. Nevertheless, it was the express elevator down after taking the stairs up for EUR bulls. But let’s face it, markets never go up in a straight line, and if we discount Praet’s comments, which are likely erroring dovish until the French election risk completely evaporates, it could be far too early for the market to give up on this possible major positioning event in the EUR.

Japanese Yen

The stable equity market and higher US yields supported the USDJPY trade overnight, with the downside looking less ominous as we enter hump day. The market will likely concede the short trade for the time being. The US consumer confidence report will have the dollar bulls gloating that the dollar’s demise was premature, which will provide short-term dollar support.

Consumer Confidence Strengthens Further in March

Consumer confidence jumped 9.5 points in March to 125.6, easily topping expectations and marking the highest level since December 2000. Both the current conditions and future expectations series improved.

The Strength in Consumer Confidence Is Hard to Dismiss

Consumer confidence once again significantly topped expectations. The overall index surged 9.5 points in March and data for February were also revised 1.3 points higher. The surge in the Consumer Confidence Index reported since the election is hard to dismiss as merely a post-election bounce. Overall consumer confidence has risen 24.8 points since October and coincides with improvement in other consumer surveys, as well as surveys of manufacturers, small businesses, homebuilders and corporate CFOs. Moreover, the gains in consumer confidence far exceed what occurred in previous elections and reflect a much more encouraging appraisal of both current and future economic conditions. The cutoff date for the preliminary survey was March 16, which preceded the demise of the proposed revision of the Affordable Care Act and ensuing stock market pullback surrounding it. We would expect to see some pullback in coming months, particularly if expectations for tax cuts are scaled back.

More Than Animal Spirits

The improvement in consumer sentiment likely reflects a legitimate improvement in business conditions. Consumers' assessment of current economic conditions rose 8.7 points to 143.1, largely on the strength of a surge in the proportion of consumers stating that they believe that jobs are plentiful and a coinciding drop in the proportion stating jobs are not so plentiful. The proportion of consumers reporting that jobs were hard to get also fell further in March and is now at its lowest level of this cycle. The improvement comes on the heels of two strong employment reports and additional strengthening in the number of job openings in the JOLTS survey, as well as a rise in the number of voluntary quits.

The strong improvement in the labor market indicators is exactly what the Fed said they need to see in order to continue to nudge interest rates back to normal. The strength in the labor market may be needed to offset any concerns raised by what looks like will be another disappointing first quarter real GDP report. We are looking for just 1.1 percent growth in the first quarter, largely due to milder winter weather, which reduced heating use and a wider trade deficit tied to the early Lunar New Year.

Expectations for future economic conditions jumped 9.9 points to 113.8. The largest improvement came in the proportion of consumers expecting more jobs to be created over the next six months. A growing proportion of consumers also expect their income to rise over the next six months while fewer expected a decrease. Consumers' improved assessment of their income prospects is evident in purchasing plans for automobiles and major appliances, which both rose solidly in March. Plans to purchase a home also remain at a fairly high level but gave back part of the prior months gain.

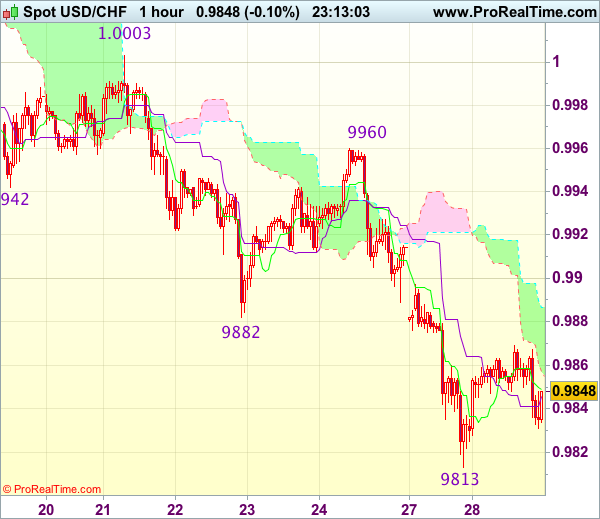

Trade Idea Wrap-up: USD/CHF – Sell at 0.9910

USD/CHF - 0.9843

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9849

Kijun-Sen level : 0.9846

Ichimoku cloud top : 0.9887

Ichimoku cloud bottom : 0.9957

Original strategy :

Sell at 0.9910, Target: 0.9800, Stop: 0.9945

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9910, Target: 0.9800, Stop: 0.9945

Position : -

Target : -

Stop : -

The greenback found support at 0.9813 yesterday and recovered, suggesting consolidation above this level would be seen and corrective bounce to 0.9880 is likely but upside should be limited to 0.9900-10 and bring another decline later, below said support at 0.9813 would confirm recent decline has resumed and extend weakness to 0.9795-00, however, loss of downward momentum should prevent sharp fall below 0.9770-75 (100% projection of 1.0171-0.9942 measuring from 1.0003), bring rebound later.

In view of this, would not chase this fall here and we are looking to sell dollar on subsequent rebound as 0.9900-10 should limit upside. Only above said resistance at 0.9960 would abort and signal low is formed, bring retracement of recent decline towards indicated previous resistance at 1.0003.

Gold Steady as US Consumer Confidence Soars to 16-year High

Gold continues to have a quiet week. In Tuesday's North American trade, gold is trading at $1255.06 per ounce. On the release front, CB Consumer Confidence rocketed to 125.5, crushing the estimate of 113.9. There was also good news on the manufacturing front, as the Richmond Manufacturing Index improved to 22, well above the forecast of 16 points.

CB Consumer Confidence surprised the markets by climbing to 125.5 in March, its highest level since December 2000. Clearly, consumers remain optimistic about the US economy, and a major contributor to this sentiment is the red-hot labor market, which remains close to capacity. An increase in consumer confidence often translates into stronger consumer spending, which would be bullish for the US dollar, which has headed lower since the Federal Reserve rate hike on March 15. We'll get a look at consumer spending data on Friday, with the release of Personal Spending.

Donald Trump suffered his first major setback as president last week, as his bill to replace the Affordable Care Act was pulled before it even went to a vote. Trump is used to giving the orders in the private sector and on reality TV, but he didn't get his way on healthcare, despite the Republicans enjoying a majority in Congress. This bruising defeat has sent the US dollar sharply lower, and sent market jitters higher. Trump's administration has stumbled out of the starting gate, and after more than two months in office, he has yet to provide any details over even an outline of economic policy. The inquiry into the Trump administration's links with Russia is gathering steam, and is another cause for concern for nervous investors. Trump has said he will now focus on tax reform, but he has his work cut out, trying to convince a skeptical Congress and general public that he can deliver the goods and pass new, effective legislation.

Gold prices are sensitive to rate moves, so investors continue to look for clues about what the Federal Reserve has planned for the remainder of 2017. The Fed's rate statement and dot plot indicated that the Fed is looking at another two hikes in 2017, which would make three in total. This forecast was reiterated by Chicago Fed President Charles Evans earlier this week. Although one could make a strong case that three rate hikes in 2017 would be impressive, the markets appear disappointed, and would like four hikes, given the strong performance of the US economy. The Fed's cautious approach has reduced investors' appetite for risk, which has been good news for gold, a safe-haven asset.

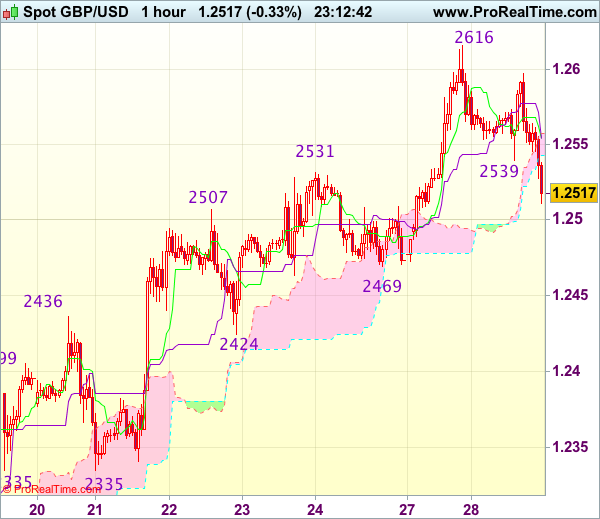

Trade Idea Wrap-up: GBP/USD – Buy at 1.2470

GBP/USD - 1.2515

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2551

Kijun-Sen level : 1.2551

Ichimoku cloud top : 1.2557

Ichimoku cloud bottom : 1.2543

Original strategy :

Buy at 1.2490, Target: 1.2600, Stop: 1.2455

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2470, Target: 1.2590, Stop: 1.2435

Position : -

Target : -

Stop : -

Cable’s retreat after rising to 1.2616 yesterday suggests consolidation below this level would be seen and initial downside risk remains for weakness to 1.2490-00, however, reckon support at 1.2469 would limit downside and bring another upmove later, above said resistance at 1.2616 would extend recent rise from 1.2109 to 1.2635-40 but loss of upward momentum should prevent sharp move beyond 1.2670-80 and price should falter below previous resistance at 1.2706, risk from there is seen for a retreat later.

In view of this, would not chase this rise here and would be prudent to buy cable on further subsequent retreat as said support at 1.2469 (Friday’s low) should limit downside. Only below 1.2422-24 (38.2% Fibonacci retracement of 1.2109-1.2616 and previous support) would abort and signal top is formed, bring retracement of recent upmove to 1.2390-00 and possibly towards 1.2360-65 (50% Fibonacci retracement).

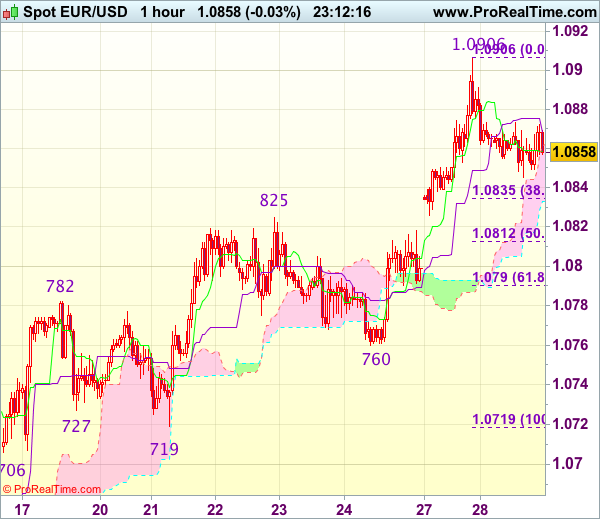

Trade Idea Wrap-up: EUR/USD – Buy at 1.0800

EUR/USD - 1.0863

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.0859

Kijun-Sen level : 1.0868

Ichimoku cloud top : 1.0862

Ichimoku cloud bottom : 1.0833

Original strategy :

Buy at 1.0800, Target: 1.0900, Stop: 1.0765

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0800, Target: 1.0900, Stop: 1.0765

Position : -

Target : -

Stop : -

As the single currency has retreated after surging to 1.0906 yesterday, suggesting consolidation below this level would be seen and pullback to 1.0835 (38.2% Fibonacci retracement of 1.0719-1.0906) is likely, however, reckon downside would be limited to 1.0810-15 (50% Fibonacci retracement), bring another rise later, above said resistance at 1.0906 would extend recent upmove to 1.0930-35 (61.8% Fibonacci retracement of 1.1300-1.0340) but loss of near term upward momentum should prevent sharp move beyond 1.0955-60 and price should falter below 1.0990-00.

In view of this, would not chase this rise here and we are looking to buy euro on subsequent pullback as 1.0800-10 should limit downside. Only below support at 1.0760 would abort and signal top is formed, bring retracement of recent upmove to 1.0730 but 1.0719 support should remain intact.

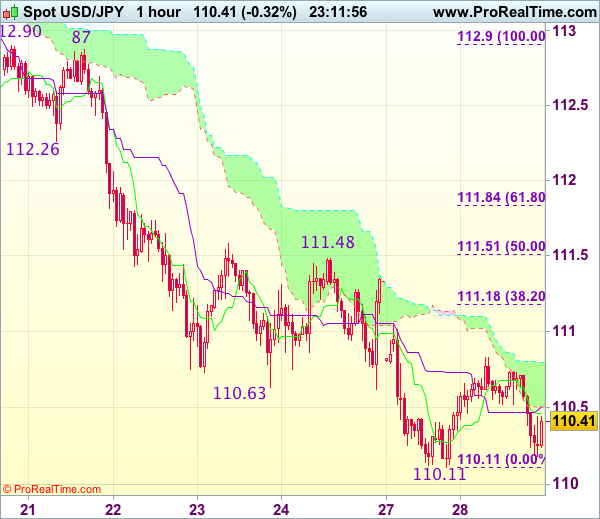

Trade Idea Wrap-up: USD/JPY – Sell at 111.20

USD/JPY - 110.43

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 110.46

Kijun-Sen level : 110.51

Ichimoku cloud top : 110.80

Ichimoku cloud bottom : 110.50

Original strategy :

Sell at 111.20, Target: 110.20, Stop: 111.55

Position : -

Target : -

Stop : -

New strategy :

Sell at 111.20, Target: 110.20, Stop: 111.55

Position : -

Target : -

Stop : -

Although dollar retreated after meeting resistance at 110.83, as long as support at 110.11 holds, further consolidation would be seen and another corrective bounce to 110.95-00 cannot be ruled out, however, reckon upside would be limited to 111.15-20 (38.2% Fibonacci retracement of 112.90-110.11) and price should falter well below resistance at 111.48, bring another decline later, below said support at 110.11 would signal recent decline is still in progress and may extend weakness to 109.95-00 but loss of downward momentum should prevent sharp fall below 109.70-75 and reckon 109.50 would hold.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 111.15-20 should limit upside. Above 111.48-51 (previous resistance and 50% Fibonacci retracement of 112.90-110.11) would abort and signal low is formed, bring a stronger rebound to 111.80-85 first (61.8% Fibonacci retracement).

National Home Prices Edge Higher to Start 2017

National home prices rose 0.6 percent in January, pushing the year-over-year gain to 5.9 percent. Home prices are being supported by steady gains in demand and the continued low level of homes for sale.

U.S. Home Prices Continue to Rise

National home prices continue to edge higher as tight supplies and continued uptrend in home sales push prices higher. The S&P CoreLogic Case-Shiller National Home Price Index rose 5.9 percent over the past 12 months and the 20-City and 10-City indices are up 5.7 percent and 5.1 percent, respectively.

On a regional basis, Seattle, Portland and Denver continue to see the strongest year-to-year price gains.

Prices Have Risen the Fastest in Larger Markets

While only the national home price index has regained its prerecession level, the recovery has been driven by the rebound in the 20-City and 10-City indices, which both fell harder during the housing crisis and rose faster during the ensuing recovery.

Much of the earlier price recovery was dominated by big global coastal markets. Price appreciation has moderated, however, as European and Latin American buying has diminished.