Sample Category Title

Trade Idea Update: GBP/USD – Stand aside

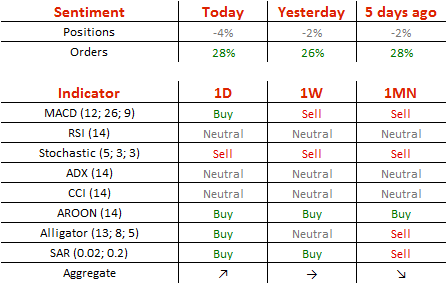

GBP/USD - 1.2444

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although cable has retreated after yesterday’s rise to 1.2524 in part due to cross-trading in sterling and consolidation below said resistance would be seen, break of 1.2400 is needed to revive bearishness and signal the rebound from 1.2377 has ended at 1.2524, bring retest of 1.2377 (this week’s low) first, otherwise, further choppy trading would take place and risk of another rebound remains.

In view of this, would not chase this fall here and would be prudent to stand aside in the meantime. Above 1.2500 would bring another test of 1.2524, break there would bring test of previous support at 1.2539, however, break there is needed to signal the fall from 1.2616 has ended, bring further rise to 1.2555-60 later.

Trade Idea Update: EUR/USD – Sell at 1.0745

EUR/USD - 1.0677

Original strategy :

Sell at 1.0745, Target: 1.0645, Stop: 1.0780

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0745, Target: 1.0645, Stop: 1.0780

Position : -

Target : -

Stop : -

As this week’s selloff has kept euro under pressure, adding credence to our bearish view that top has been formed at 1.0906 and bearishness remains for the decline from there to extend further weakness to 1.0660, then 1.0640, however, near term oversold condition would limit downside and reckon previous strong support at 1.0600 would hold from here, bring rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 1.0740-50 should limit upside. Only above resistance at 1.0773 would suggest low is formed instead, bring a stronger rebound to 1.0800 but resistance at 1.0827 should remain intact.

Trade Idea Update: USD/JPY – Buy at 111.50

USD/JPY - 111.90

Original strategy :

Buy at 111.25, Target: 112.25, Stop: 110.90

Position : -

Target : -

Stop : -

New strategy :

Buy at 111.50, Target: 112.50, Stop: 111.15

Position : -

Target : -

Stop : -

As the greenback has eased after intra-day initial rise too 112.20, suggesting minor consolidation below this level would be seen and test of the Kijun-Sen (now at 111.60) is likely, however, reckon previous resistance at 111.32 would contain downside and bring another rise later, above indicated resistance at 112.20-26 would extend the upmove from 110.11 low to 112.50-55 but price should falter below previous resistance at 112.87-90, bring retreat.

In view of this, would not chase this rise here and would be prudent to buy dollar on pullback as 111.50 should limit downside. Below the upper Kumo (now at 111.13) would defer and risk test of 110.90-95, break there would abort and signal top is formed instead, bring weakness to support at 110.72, break there would suggest the rebound from 110.11 (this week’s low) has ended, then further fall to 110.45-50 would follow.

Sterling Continues to Strengthen

Day two of the Brexit negotiations period and it's all kicking off. Threats and warnings abound, while the Scottish First Minister opts for guerrilla tactics in trying to ambush the British Prime Minister over another 'once in a lifetime' independence vote. "Keep calm and carry on" is the best policy for Theresa May, as the 27 remaining members of the EU discuss Britain's departure today.

In spite of all the furore, Sterling held up well on Thursday and even gained ground in some areas. We end the week with UK Q4 Gross Domestic Product (GDP) figures, which have the capacity to improve slightly on the previous estimates. That would boost the Pound. We'll also get the current account balance, which we think will have narrowed marginally and we'll have a speech from Andy Haldane, who holds the snappy title of "Chief Economist and Executive Director of Monetary Analysis and Statistics" at the Bank of England. (Massive business cards…huge!) If he hints that the Bank of England (BoE) might be edging closer to a rate hike, that will also be positive for Sterling.

The Euro is having a more troubled time. Perhaps it has dawned on traders that Brexit could be bad for the Eurozone and for the EU generally. The Euro is weaker against Sterling, the USD and others. Eurozone inflation is due for release this morning and that is expected to be a tad lower than last month's 2.0% figure. Less pressure on the ECB to look at interest rate hikes, then, and it would therefore leave further room for Euro weakness.

The US and Chinese Presidents meet next week and their approaches have been very different. President Xi said the meeting can be a new starting point for the US and China to become "great partners". President Trump tweeted that the meeting will be "a very difficult one". In the meantime, we will get US income and expenditure data this afternoon and that is likely to be mildly positive for the USD.

It is the last day of the month and the quarter and it is the last day of the financial year for a lot of UK companies. There is a significant risk of volatility today and, particularly over late trade into the US close. This is another opportunity for those with any sort of requirement to place automated orders to do your bidding as the markets shuffle ahead of the trading day. Have a word with your Halo Financial currency consultant to see how that could work for you.

NZ business confidence declined again in March, as shown by overnight data from the ANZ Business Outlook. A net 11% of the companies that were surveyed are optimistic about the general outlook for the economy. That is much lower than last month's 16.6% percent in February. The NZ Dollar weakened a little on the news.

This afternoon's data also brings Canada's GDP growth data. A small slowdown is expected and the Canadian Dollar may well weaken a tad on that news, if the forecasters have got it right of course…

It is Kindness Day in the UK, so I will spare you any corny jokes. (Kindness personified, that's me!)

And it is April Fool's day tomorrow, so trust no one and believe nothing you see or hear. Kind of the antidote to kindness, isn't it.

See you in April.

Some suggested honest product tag lines

Monopoly - Destroyer of family harmony

Lego - Foot pain for the unwary

Bic - You probably didn't buy it

Netflix - 90% searching 10% watching

iPhone - you bought the hype, sucker!

Google - We know more about you than anything else

Southern Rail - We occasionally run trains

Lush - Scent induced high street headaches

Argos - You can only see it when you've paid

Daily Technical Analysis

EURUSD

The EURUSD continued its bearish momentum yesterday bottomed at 1.0671. The bias remains bearish in nearest term testing 1.0600 region. That said, we have a CCI bullish divergence as you can see on my H1 chart below suggests a potential bullish correction especially if price able to make a clear break above 1.0700 testing 1.0750 – 1.0785 region but as long as stay below the EMA 200 I still prefer a bearish scenario at this phase and any upside pullback should be seen as a good opportunity to sell. Overall I remain neutral.

GBPUSD

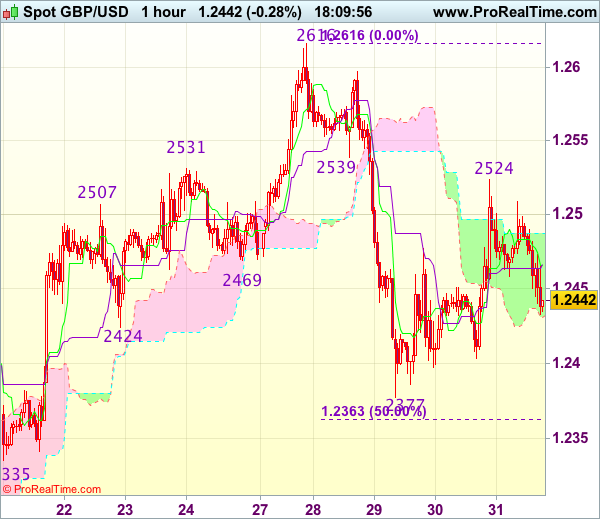

The GBPUSD attempted to push higher yesterday topped at 1.2524 but closed lower at 1.2467. Overall price is still in a bearish phase since fell below the bullish channel as you can see on my H1 chart below but still unable to stay consistently below the H1 EMA 200 and moving inside a minor bullish channel. The bias is neutral in nearest term probably with a little bullish bias testing 1.2530 – 1.2550 region. Immediate support is seen around 1.2450. A clear break below that area could trigger further bearish pressure testing 1.2375 key support which need to be clearly broken to the downside to continue the bearish scenario. Overall I remain neutral.

USDJPY

The USDJPY had a bullish momentum yesterday topped at 111.94 and hit 112.08 earlier today in Asian session. The bias is bullish in nearest term testing 112.85 as a part of the “hammer” formation bullish scenario as you can see on my daily chart below. Immediate support is seen around 111.70. A clear break below that area could lead price to neutral zone in nearest term but only a clear break back below 111.30 would be a serious threat to the bullish reversal scenario.

USDCHF

The USDCHF continued its bullish momentum yesterday topped at 1.0013. The bearish scenario after fell below the bullish channel as you can see on my H4 chart below is in a serious threat. The bias is bullish in nearest term testing 1.0060 region. A clear break and daily/weekly close above that area would activate my bullish short-term mode. Immediate support is seen around 0.9990. A clear break below that area could lead price to neutral zone in nearest term testing 0.9950 or lower. Overall I remain neutral.

US Data And French Election In Focus

News and Events:

Markets to refocus on hard data and monetary policy

It has been a quiet week so far as volatility in the FX market remains desperately low, despite lingering political uncertainty. Over the last few days, the USD has been particularly resilient, especially after Trump's health-care reform setback. The single currency completely erased last week’s gains dipping below the 1.07 threshold amid building political pressure in Europe, mostly due to Brexit and the upcoming French elections. However, we have the feeling that the Trump trade is coming to an end and the market now needs a new driver. Equity gains have begun to stall recently, while the greenback has been unable to reach higher ground. We believe that the market will slowly start focusing again on monetary policy and economic data.

US price data is due for release later today. The Fed’s favourite measure of inflation, the core PCE, is expected to have held steady at 1.7%y/y in February, while the headline measure, which includes the most volatile components, is expected to have risen from 1.9% to 2.1%. Personal income and spending are also anticipated to have stabilised at 0.4%m/m and 0.2%m/m respectively. Next week will be a busy one in the US as a fresh batch of key data is due for publication, with notably the March job report, FOMC minutes, factory and durable goods orders and ISM. The market is still positioned for two rate hikes from the Fed this year, suggesting that risk is mostly on the downside as we are approach the release of the FOMC minutes.

Japan shows signs of steady improvement

Economic data released for Japan continues to support steady improvements. Japan's CPI for February posted a 0.3% y/y gain as expected, while industrial product surged 2.0% m/m - well above the expected figure of 1.2%. However, housing starts fell 2.6% y/y following a 12.8% rise prior, posting the first decline in eight months. Next week will bring the BoJ Tankan report into focus. Weaker JPY and strong global trade growth should allow sentiment, specifically in manufacturing to improve. Given the inflation backdrop, we anticipate further strengthening in corporate inflation expectations which should influence the BoJ's monetary policy strategy. Despite BoJ commitment to ultra-extreme accommodating measures, improvement in the economics suggests tightening in 2018. Given the lack of responsiveness from US yields, we remain short USDJPY heading into next week. USDJPY 21d MA at 112.83 should provide resistance for a corrective decline to 108.80. Watch EURJPY for a deeper bearish move towards 118.55.

French Elections: Macron clear favourite in race for French presidency

Both in polls and the financial markets, Macron seems to be the clear favourite for the Élysée Palace with markets currently pricing a probability in excess of 67%. However, for now, the euro still remains weak against the dollar with further possibility for upside. Drawing comparisons with the US elections, we would do well to recall that Clinton had an estimated win of over 80%. However, we are extremely sceptical of these polls and believe that the Le Pen vote should not be underestimated, especially when we factor in the clear bias regarding this candidate.

Zooming in on markets, the 10-year French yield has risen above 0.90%, yet rates are still holding around a one-month low, while the 10-year spread France vs Germany is back above 60 basis points.

Markets are demonstrably confident that Macron will win and French rates are clearly trending lower. This is partly due to the nature of the elections. Many socialists from the government (including former Prime Minister, Manuel Valls) are now supporting Macron. This is why we believe that what is called the “Republican Front” i.e. an alliance of all forces against the National Front represents the best possible strategy for French leftists. Macron is now racing towards the presidency and the markets are reflecting this. Of course, this perception could create epic turmoil in the event of a Le Pen victory. Yet, as we have seen in the past, political turmoil can be very temporary and central banks would quickly return to being the main drivers of asset pricing.

Today's Key Issues (time in GMT):

- 4Q F GDP SA QoQ, last 0,20% DKK / 07:00

- 4Q F GDP SA YoY, last 1,90% DKK / 07:00

- Feb Unemployment Rate Gross Rate, exp 4,20%, last 4,20% DKK / 07:00

- Feb Unemployment Rate SA, last 3,30% DKK / 07:00

- Feb Trade Balance, exp -3.70b, last -4.31b, rev -4.33b TRY / 07:00

- Feb Retail Sales YoY, last -0,10% EUR / 07:00

- Feb Retail Sales SA YoY, exp 0,90%, last 0,10% EUR / 07:00

- 4Q GDP YoY, exp 1,90%, last -1,80%, rev -1,30% TRY / 07:00

- Mar Unemployment Change (000's), exp -10k, last -14k, rev -15k EUR / 07:55

- Mar Unemployment Claims Rate SA, exp 5,90%, last 5,90% EUR / 07:55

- Jan Current Account Balance, last 3.4b, rev 3.6b EUR / 08:00

- Apr Norges Bank Daily FX Purchases, exp -850m, last -850m NOK / 08:00

- mars.24 Money Supply Narrow Def, last 8.93t RUB / 08:00

- Mar Unemployment Rate, exp 3,00%, last 3,10% NOK / 08:00

- Bank of Italy Annual Shareholder Meeting EUR / 08:00

- 4Q Current Account Balance, exp -16.0b, last -25.5b, rev -25.7b GBP / 08:30

- 4Q F GDP QoQ, exp 0,70%, last 0,70% GBP / 08:30

- 4Q F GDP YoY, exp 2,00%, last 2,00% GBP / 08:30

- Jan Index of Services MoM, exp 0,20%, last 0,20% GBP / 08:30

- Jan Index of Services 3M/3M, exp 0,70%, last 0,80% GBP / 08:30

- 4Q F Total Business Investment QoQ, exp -1,00%, last -1,00% GBP / 08:30

- 4Q F Total Business Investment YoY, exp -0,90%, last -0,90% GBP / 08:30

- ECB's Benoit Coeure Speaks in Brussels EUR / 09:00

- Mar P CPI NIC incl. tobacco MoM, exp 0,10%, last 0,30%, rev 0,40% EUR / 09:00

- Mar P CPI NIC incl. tobacco YoY, exp 1,50%, last 1,50%, rev 1,60% EUR / 09:00

- Mar P CPI EU Harmonized MoM, exp 2,10%, last 0,20% EUR / 09:00

- Mar P CPI EU Harmonized YoY, exp 1,60%, last 1,60% EUR / 09:00

- Mar CPI Estimate YoY, exp 1,80%, last 2,00% EUR / 09:00

- Mar A CPI Core YoY, exp 0,80%, last 0,90% EUR / 09:00

- ECB's Ignazio Angeloni Speaks in Bologna, Italy EUR / 09:50

- Feb PPI MoM, last 1,10% EUR / 10:00

- Feb PPI YoY, last 2,80% EUR / 10:00

- Feb Fiscal Deficit INR Crore, last 62942 INR / 11:00

- Jan Economic Activity MoM, exp -0,20%, last -0,26% BRL / 11:30

- Jan Economic Activity YoY, exp -0,50%, last -1,82% BRL / 11:30

- Feb Trade Balance Rand, exp 1.6b, last -10.8b ZAR / 12:00

- Feb National Unemployment Rate, exp 13,10%, last 12,60% BRL / 12:00

- Jan GDP MoM, exp 0,30%, last 0,30% CAD / 12:30

- Feb Personal Income, exp 0,40%, last 0,40% USD / 12:30

- Jan GDP YoY, exp 1,90%, last 2,00% CAD / 12:30

- Feb Personal Spending, exp 0,20%, last 0,20% USD / 12:30

- Feb Real Personal Spending, exp 0,10%, last -0,30% USD / 12:30

- Feb PCE Deflator MoM, exp 0,10%, last 0,40% USD / 12:30

- Feb PCE Deflator YoY, exp 2,10%, last 1,90% USD / 12:30

- Feb PCE Core MoM, exp 0,20%, last 0,30% USD / 12:30

- Feb PCE Core YoY, exp 1,70%, last 1,70% USD / 12:30

- 4Q F Current Account Balance, last 7800m RUB / 13:00

- Fed's Dudley Speaks to Mike McKee in Bloomberg TV Interview USD / 13:00

- Feb Primary Budget Balance, exp -21.2b, last 36.7b BRL / 13:30

- Feb Nominal Budget Balance, exp -55.8b, last 0.3b BRL / 13:30

- Feb Net Debt % GDP, exp 47,10%, last 46,40% BRL / 13:30

- Mar Chicago Purchasing Manager, exp 56,9, last 57,4 USD / 13:45

- Fed's Kashkari Answers Questions at Banking Conference USD / 14:00

- Mar F U. of Mich. Sentiment, exp 97,6, last 97,6 USD / 14:00

- Mar F U. of Mich. Current Conditions, last 114,5 USD / 14:00

- Mar F U. of Mich. Expectations, last 86,7 USD / 14:00

- Mar F U. of Mich. 1 Yr Inflation, last 2,40% USD / 14:00

- Mar F U. of Mich. 5-10 Yr Inflation, last 2,20% USD / 14:00

- Fed's Bullard Speaking in New York USD / 14:30

- BOE's Andy Haldane speaks in San Francisco GBP / 21:00

The Risk Today:

EUR/USD is getting lower. The pair is heading lower since the pair failed to hold above former resistance given at 1.0874 (08/12/2017 high). Hourly support given at 1.0719 (21/03/2017 low) has been broken. Stronger support can be found at 1.0493 (22/02/2017 low). The short-term technical structure indicates further weakness.. In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD's bullish pressures increase again after the pair exited short-term uptrend channel. Hourly resistance is located at 1.2615 (27/03/2017 high). Hourly support is given at 1.2324 (03/17/2017 low). Expected to show strengthening towards resistance at 1.2771 (05/10/2016 high). The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY's bearish pressures are fading. Hourly resistance can be located at 113.57 (16/03/2017 high) while support is given at 110.11 (27/03/2017 low). We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

USD/CHF is strengthening. Hourly support is given at 0.9814 (27/03/2017 low). Key resistance can be found at a distance at 1.0344 (15/12/2016 high). Expected to show further consolidating below parity. In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

| EURUSD | GBPUSD | USDCHF | USDJPY |

| 1.1300 | 1.3445 | 1.0652 | 121.69 |

| 1.0954 | 1.3121 | 1.0344 | 118.66 |

| 1.0906 | 1.2771 | 1.0171 | 115.62 |

| 1.0695 | 1.2445 | 1.0001 | 111.85 |

| 1.0494 | 1.1986 | 0.9550 | 106.57 |

| 1.0341 | 1.1841 | 0.9444 | 106.04 |

| 1.0000 | 1.0520 | 0.9259 | 101.20 |

EUR/USD Trades Below 1.07 Mark

'The dollar climbed to a two-week high against the euro after U.S. data showed gains in personal consumption and corporate profits.' – Lananh Nguyen and Vincent Cignarella, Bloomberg

Pair's Outlook

During the early hours of Friday's trading session the common European currency found support against the Greenback in a combined support level, which is made up of the weekly S2 and 55-day SMA. Both of the support levels are located exactly at the 1.0675 mark. The pair fell sharply during Thursday's trading session, as the Buck surged all across the financial markets. If the fall continues, the rate is set to retreat to a much stronger support cluster, which begins with the 23.60% Fibonacci retracement level at 1.0639. On the other hand a rebound up to the 20-day SMA at 1.0708 might occur.

Traders' Sentiment

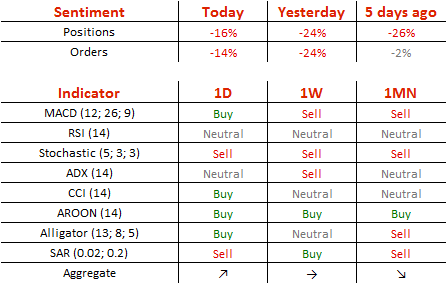

SWFX traders have decreased their bearish outlook, as 58% of open positions are short, compared to 62% previously. Meanwhile, 57% of set up orders are to sell the Euro.

GBP/USD Stuck Between 1.24 And 1.26

'Given the positioning, our bias would still be toward a stronger pound over the coming weeks.' – MUFG (based on Business Recorder)

Pair's Outlook

The British Pound found support in front of the 55 and 100-day SMAs yesterday, but was unable to fully breach the immediate resistance cluster. Although technical studies keep suggesting the GBP/USD pair is to edge higher and the 55-day SMA is on the verge of crossing the 100-day one to the upside, the potential bullish development is unlikely to exceed the 1.2550 mark. The weekly R1 at 1.2558 is to prevent the Cable from rising further in case bulls do prevail today, but downside risks are still present, with political factors continuing to weigh on the Sterling.

Traders' Sentiment

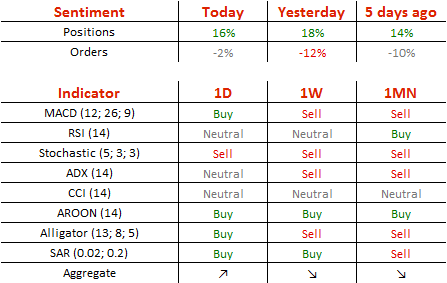

There are 58% of traders holding long positions today (previously 59%), whereas 51% of all pending orders are to sell the Pound, compared to 56% on Thursday.

USD/JPY Struggles To Breach 112.00 Handle

'It is too early to expect a sustained recovery even though on the converse, the odds for a break below 110.00 have diminished considerably.' – UOB (based on FXStreet)

Pair's Outlook

The US Dollar successfully outperformed the Yen on Thursday, receiving a boost from a better-than-expected US GDP reading. As a result, the given pair breached two immediate resistances, encountering resistance only in front of the 112.00 level. After such a relatively strong rally a bearish correction is expected. The weekly PP, which is now the nearest support, is unlikely to limit the losses if bears do push the Buck lower. Technical indicators are in favour of the negative outcome, but we should not rule out the possibility of another rally, with fundamental data providing the Greenback with more impetus.

Traders' Sentiment

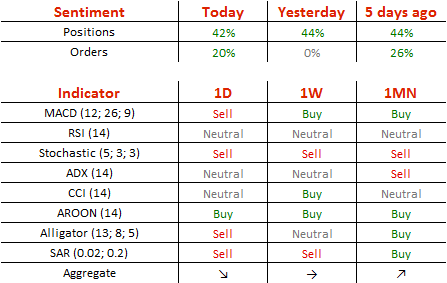

Today 71% of traders are long the Buck (previously 72%), while 60% of all pending orders are to acquire the US Dollar, up from 50% yesterday.

Gold Retreats To 1,240 Level

'In the short term, factors including a strengthening dollar could pull prices down to around the $1,230 an ounce range.' – Yuichi Ikemizu, Standard Bank (based on Reuters)

Pair's Outlook

On Friday the yellow metal began the day's trading session just above the 1,240 level. The reason for that is the strength of the US Dollar, which pushed the price lower in the second part of Thursday's trading session. However, the metal seems to have found support in the weekly PP, which is located at the 1,240.87 mark, which indicates that a short period of consolidation is set to occur. Although, the further short term path of the metal is most likely going to be dictated by the US Dollar fundamentals and political risk events around the world.

Traders' Sentiment

Traders have increased their bearish outlook on the bullion, as 52% of open positions are short, compared to 51% the past three consecutive trading sessions. Meanwhile, 64% of set up orders are to buy.