Sample Category Title

Trade Idea : GBP/USD – Buy at 1.2490

GBP/USD - 1.2568

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2545

Kijun-Sen level : 1.2525

Ichimoku cloud top : 1.2497

Ichimoku cloud bottom : 1.2478

New strategy :

Buy at 1.2490, Target: 1.2600, Stop: 1.2455

Position : -

Target : -

Stop : -

As cable has surged again today, adding credence to our bullish view that recent upmove from 1.2109 is still in progress and upside bias remains for this move to extend further gain to 1.2600, then towards 1.2635-40, however, loss of upward momentum should prevent sharp move beyond 1.2670-80 and price should falter below previous resistance at 1.2706, risk from there is seen for a retreat later.

In view of this, would not chase this rise here and would be prudent to buy cable on subsequent retreat. Only below support at 1.2469 (Friday’s low) would abort and signal top is formed, bring retracement of recent upmove towards previous support at 1.2424 which is likely to hold from here.

Trade Idea : EUR/USD – Buy at 1.0800

EUR/USD - 1.0866

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.0856

Kijun-Sen level : 1.0823

Ichimoku cloud top : 1.0793

Ichimoku cloud bottom : 1.0778

Original strategy :

Buy at 1.0720, Target: 1.0820, Stop: 1.0685

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.0800, Target: 1.0900, Stop: 1.0765

Position : -

Target : -

Stop : -

The single currency also opened higher today on dollar’s broad-based weakness and the the subsequent rally signals recent upmove is still in progress, hence bullishness remains for further gain to 1.0900 and possibly 1.0930-35 (61.8% Fibonacci retracement of 1.1300-1.0340), however, loss of near term upward momentum should prevent sharp move beyond 1.0955-60 and price should falter below 1.0990-00, risk from there has increased for a retreat to take place later.

In view of this, would not chase this rise here and we are looking to buy euro on subsequent pullback as 1.0800-10 should limit downside. Only below support at 1.0760 would abort and signal top is formed, bring retracement of recent upmove to 1.0730 but 1.0719 support should remain intact.

E-mini S&P500: Be Aware Of A 3-Wave Rally

We see dollar index to hit new lows of the year as EUR/USD breaks above 1.0800, while stocks sold-off as Trump's health-care bill fails. E-mini S&P500 has extended its weakness from last week down to 2320 area which was our projected zone for a fifth wave of decline, highlighted last week. Question is, what is next. Well, if you are familiar with the Elliott Wave principle, then you know that market can be ready for a bounce this week if we consider that after every five waves trend will make a change in three legs minimum, no matter what is the structure on a higher time-frame charts. So from a technical perspective, and also from a psychological point of view, when others are turning aggressively bearish on stocks, we suspect that three wave of retracement may show up on stocks, but it may be just another temporary recovery. Divergence on the RSI also indicates a potential turn. We see first support zone here near 2320 while next one stands near 2310.

S&P, 1H

Trade Idea : USD/JPY – Sell at 111.00

USD/JPY - 110.26

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 110.36

Kijun-Sen level : 110.74

Ichimoku cloud top : 111.18

Ichimoku cloud bottom : 111.11

Original strategy :

Sell at 112.20, Target: 110.80, Stop: 112.55

Position : -

Target : -

Stop : -

New strategy :

Sell at 111.00, Target: 110.00, Stop: 111.35

Position : -

Target : -

Stop : -

The greenback opened lower earlier today and has dropped again, adding credence to our bearish view that recent selloff is still in progress and may extend weakness to 110.00, however, loss of downward momentum should prevent sharp fall below 109.70-75 and reckon 109.50 would hold from here, risk from there has increased for a rebound to take place later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as 111.00 should limit upside. Above 111.30-35 would risk test of resistance at 111.48 but break there is needed to signal low is formed instead, bring retracement of recent decline to 111.75-80 first.

USD Slips as Trump Fails to Reform Health Care

The US dollar opened with a negative gap against its major counterparts today, after the House vote regarding Trump's healthcare bill was canceled on Friday. The Republican leaders decided to withdraw the bill altogether rather than suffer a defeat in the voting process, as they lacked the necessary votes to pass it. Even though President Trump and the Republican leadership quickly reassured investors that they will now concentrate on introducing big tax cuts, the inability of the new administration to deliver on health care may have raised concerns that tax reform is likely to encounter similar obstacles. What's more, reforming health care was one of the conditions for making the tax numbers Trump pledged feasible. As such, heightened doubts over Trump's ability to deliver on his tax promises could keep sentiment among investors somewhat subdued and thereby, weigh further on the greenback. Asian and European equity indices felt the heat as well, opening with bearish gaps. This negative sentiment may roll over into the US markets, where we expect stock indices to open in a similar fashion.

USD/JPY gapped down and continued to drift lower during the Asian morning Monday, falling below the support (now turned into resistance) barrier of 110.70 (R1). Following the dip below 111.60 (R2), the lower bound of the sideways range that contained the price action from the 11th of January until last Wednesday, we believe that the outlook has turned negative. Therefore, we expect the pair to continue trading south and perhaps challenge the round figure of 110.00 (S1) sometime soon. If the bears prove strong enough to overcome that psychological zone, then we may experience extensions towards our next support obstacle of 108.80 (S2), defined by the low of the 17th of November.

Eurozone's PMIs surge and lift the euro

Eurozone's economic growth hit a six-year high in March, according to the bloc's preliminary composite PMI survey that was released on Friday. The index beat its forecast for a marginal decline and instead rose further. The survey was upbeat on all economic fronts, indicating the best employment growth for almost a decade and perhaps even more importantly for ECB policymakers, that selling prices during the first quarter of 2017 rose at the steepest rates since 2011. The euro started strengthening ahead of the report, boosted by the German and French indices released a few minutes earlier, and continued drifting north in the aftermath of the bloc's prints. Considering the strength of these forward-looking data, we could see the common currency enjoy increased demand in the next days or weeks on speculation that the ECB could start to reduce its stimulus dose perhaps as early as next year. In our view, if incoming data continue to show mounting inflationary pressures combined with robust economic growth, then the ECB may begin to sound gradually more hawkish at its upcoming meetings, thereby preparing market participants for an eventual tightening. However, something like that is conditional upon the bloc's core CPI rate establishing an uptrend in coming months, as President Draghi made it clear that the Bank is unlikely to change its stimulus program without notable progress in underlying inflationary pressures.

EUR/USD opened with a positive gap on Monday, after the defeat of President Trump's healthcare package on Friday. After clearing the 1.0800 (S2) key resistance (now turned into support) territory, the pair broke above the 1.0825 (S1) barrier and during the early European morning Monday, it looks ready to challenge the longer-term downtrend line taken from the peak of the 3rd of May and the resistance hurdle of 1.0875 (R1), marked by the high of the 8th of December. A decisive break above that key crossroad could solidify the completion of an inverted head and shoulders, signaled upon the breach of the 1.0800 (S2) territory, and is possible to confirm a medium-term trend reversal.

Today's highlights: During the European day, we get Germany's Ifo survey for March. The forecast is for the expectations index to have risen somewhat, while the current conditions figure is expected to have ticked down. We see the risks surrounding the current conditions forecast as skewed to the upside, perhaps for an increase instead of a marginal fall. We base our view on the ZEW and PMI surveys for the month, both of which showed increased optimism in the German economy. In case of a positive surprise, the euro could extend its recent gains, as this would be another set of numbers entering the basket of data that support a gradual end to the ECB's stimulus program.

As for the rest of the week, on Tuesday, the economic calendar is light. The only event that is likely to attract some market attention is a speech by Fed Chair Yellen.

On Wednesday, the main event will be in the UK, where PM May is expected to trigger Article 50 of the Lisbon Treaty and commence the formal process for leaving the EU. We do not expect the actual triggering to be a particularly big market mover for sterling, as the move and timing have been signaled repeatedly over the past months and weeks.

On Thursday, we get Germany's preliminary CPI figures for March and from the US, the final estimate of Q4 GDP.

On Friday, during the Asian morning, Japan's CPI data for February are due to be released. In Eurozone, preliminary CPI data for March are coming out and in the UK, the final estimate of Q4 GDP will be in focus. From the US, we get personal income and spending data for February, as well as the core PCE price index for February.

USD/JPY

Support: 110.00 (S1), 108.80 (S2), 107.70 (S3)

Resistance: 110.70 (R1), 111.60 (R2), 111.90 (R3)

EUR/USD

Support: 1.0825 (S1), 1.0800 (S2), 1.0760 (S3)

Resistance: 1.0875 (R1), 1.0920 (R2), 1.0950 (R3)

Orders For US-Manufactured Durable Goods Rise 1.7% In February

'I think it's fair to say that many of my colleagues and I note a much more optimistic frame of mind among many, many businesses in recent months.' - Janet Yellen, Federal Reserve

Orders for US-manufactured long-lasting goods rose more than expected last month, official figures revealed on Friday. The US Department of Commerce reported that orders for durable goods advanced 1.7% in February, following the preceding month's upwardly revised gain of 2.3% and surpassing analysts' expectations for a 1.1% increase. Excluding transportation equipment, orders for US-manufactured durable goods climbed 0.4%, compared to the previous month's reading of 0.0%. In the meantime, market analysts anticipated a bigger gain of 0.5% during the reported period. However, the following rise marked the sixth straight monthly increase in orders for core durable goods. Analysts suggest that businesses will improve even more if US lawmakers succeed in lowering corporate taxes and reducing regulations. Non-defence capital goods orders excluding aircraft dropped 0.1%, following January's revised climb of 0.1% and falling behind expectations for a 0.5% increase. Shipments of non-defence capital goods excluding aircraft, used in calculating GDP, advanced 1.0% last month. Data also showed that orders for civilian aircraft rose 47.6%, compared to a 83.3% surge in the prior month. Boeing reported it received 43 orders for aircraft in February, up from the previous month's 26.

Canadian Inflation Rises In Line With Market Forecasts In February

'They've still got this very stable inflation backdrop as an ace up their sleeve, which suggests there's no rush for the bank to move.' - Doug Porter, BMO Capital Markets

Canadian inflation rose for the second consecutive month in February, matching market forecasts. Statistics Canada reported that the Consumer Price Index advanced 0.2% in February, following the preceding month's 0.9% surge and meeting analysts' expectations. Back in 2015, the Bank of Canada cut its key interest rates twice amid low oil prices that hurt badly the Canadian economy. However, analysts suggest that stronger economic growth, rising inflation and higher oil prices will probably force the Bank to raise rates in the Q2 of 2018, when the economy fully recovers. Food prices and telephone services prices dropped 2.3% and 2.2%, respectively, compared to the same month a year ago. Meanwhile, the price of gasoline jumped 23.1% from a year earlier. Excluding gasoline, year-over-year inflation was just 1.3%. Earlier this month, the BoC said that higher inflation was more affected by temporary factors, such as changes in petrol prices, adding that underlying inflation remained subdued. Data also showed that the Common CPI, the Central bank's preferred inflation measure, came in at 1.3%, solidly below the BoC's inflationary target of 2%. In the meantime, the Median CPI, another measure of the underlying inflation trend, remained at 1.9%.

EUR/USD Already Trades Above 1.0850 Mark

'One thing we can be sure of is that the economy in the euro area is picking up momentum and growth is becoming broader based.' – Ken Wattret, TS Lombard (based on Bloomberg)

Pair's Outlook

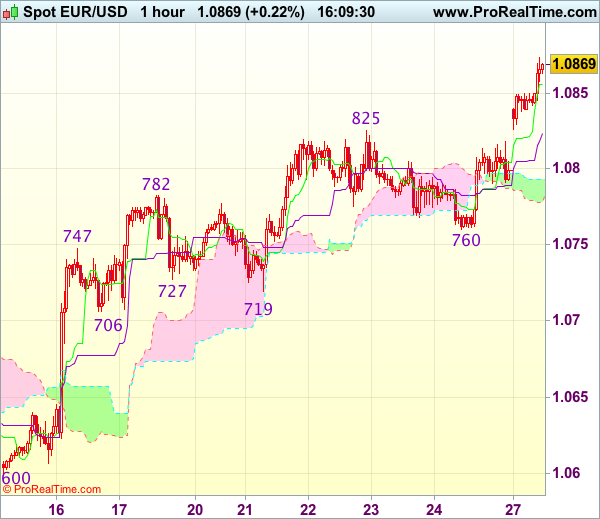

On Monday morning the Euro started the day's trading session against the Greenback much higher that it could be expected, as the rate started the day at 1.0835. Moreover, during the early morning hours the currency pair has jumped above the 1.0860 level, and it is clearly heading for the 1.0880 level. At that level the rate is set to pause, as the 200-day SMA at 1.0881 and the weekly R2 at 1.0886 are providing resistance to the currency exchange rate's surge. However, if those levels are broken, it is highly possible that the rate would jump to the 1.0950 mark in the upcoming trading sessions.

Traders' Sentiment

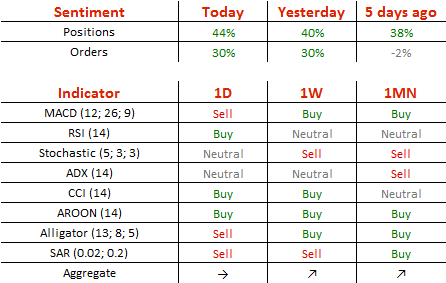

SWFX traders remain bearish, as 64% of open positions are short. In addition, 56% of trader set up orders are to sell the Euro.

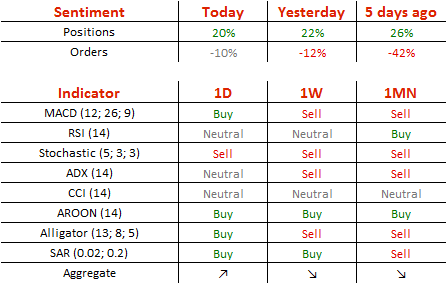

Pound Takes Advantage Of Weak Dollar

'There isn't much going for the dollar right now and the market will be bracing for its further decline.' – Barclays (based on Reuters)

Pair's Outlook

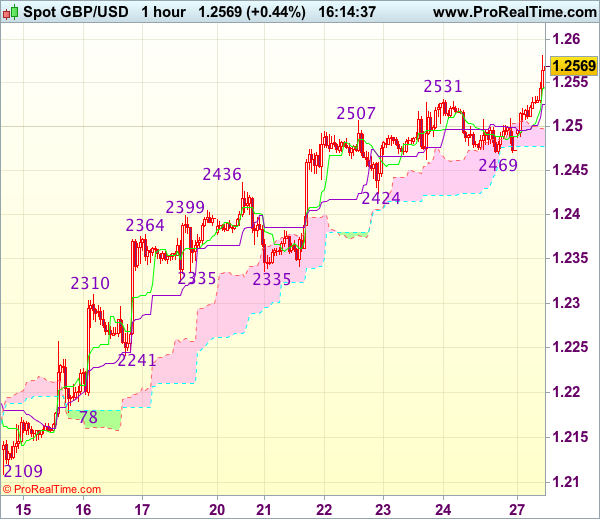

Even though the GBP/USD pair edged lower on Friday, once again crossing the 1.25 major level to the downside, this decline was just a mere setback in the pair's bullish trend. Broad USD weakness due to Trump's failure to bring down Obamacare is allowing the Sterling to continue climbing higher. Today's intraday high is expected to be the 1.26 handle, with the monthly R1 preventing any attempts to pass beyond this mark. Furthermore, the weekly R1 and the upper Bollinger band around 1.2570 form a relatively strong resistance area as well, which is likely to contribute to limiting the Cable's rally today. Meanwhile, technical studies are in favour of the positive outcome.

Traders' Sentiment

Today 60% of traders hold long positions, barely changed since Friday (61%). The portion of sell orders inched down from 56 to 55%.

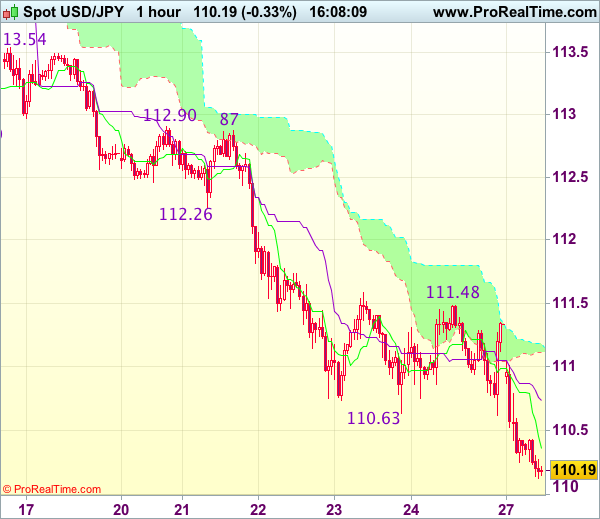

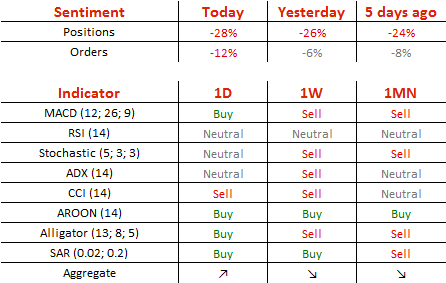

USD/JPY: 110.00 Eyed

'The Trump reflation trade could still reverse course in a more meaningful way, resulting in dollar weakness.' – MUFG (based on Business Recorder)

Pair's Outlook

The Buck succeeded in reversing polarity, but only for a day, as the bearish momentum returned over the weekend. Trade opened with the USD/JPY pair erasing all Friday's gains, with the 111.00 major level getting a full-blown downside breach. The Greenback now risks dropping towards the 110.00 level, with the only support on the pair's path being the lower Bollinger band and the weekly S1 around 110.35. In case the Buck falls under 110.00, the monthly S2 at 109.74 could still save it from further weakness, but a failure would open the door for a plunge to 108.00, being that no political or economical driver triggers a rebound earlier.

Traders' Sentiment

Market sentiment suggests that the US Dollar might be overbought, as 72% of all open positions are currently long.