Sample Category Title

AUD/USD: Aussie Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the AUD declined 0.09% against the USD and closed at 0.7620 on Friday.

LME Copper prices declined 0.1% or $8.0/MT to $5782.5/MT. Aluminium prices rose 0.2% or $4.5/MT to $1917.5/MT.

In the Asian session, at GMT0300, the pair is trading at 0.7625, with the AUD trading 0.07% higher against the USD from Friday’s close.

The pair is expected to find support at 0.7605, and a fall through could take it to the next support level of 0.7586. The pair is expected to find its first resistance at 0.7640, and a rise through could take it to the next resistance level of 0.7656.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

EUR/USD: Euro-Zone’s Manufacturing And Services PMI Surprisingly Jumped To A Nearly 7-Year High Level In March

For the 24 hours to 23:00 GMT, the EUR rose 0.09% against the USD and closed at 1.0790 on Friday, lifted by the release of upbeat manufacturing and services PMIs across the Euro-zone that pointed towards strong economic activity across the bloc.

The Euro-zone's preliminary Markit manufacturing PMI unexpectedly advanced to a nearly seven-year high level of 56.2 in March, defying market expectations for a fall to a level of 55.3 and compared to a level of 55.4 in the prior month. Additionally, the region's flash Markit services PMI surprisingly climbed to a level of 56.5 in March, notching its highest level in 71 months. The PMI had recorded a reading of 55.5 in the previous month, while markets were expecting for a fall to a level of 55.3.

Separately, activity in Germany's manufacturing sector accelerated at its fastest pace in nearly seven-years, after the PMI unexpectedly jumped to a level of 58.3 in March, thus painting a robust growth picture of the nation's manufacturing sector. Meanwhile, investors had envisaged the PMI to drop to a level of 56.5, compared to a level of 56.8 in the prior month. Moreover, growth in the nation's services sector advanced more-than-expected to a level of 55.6 in March, expanding at its quickest pace in fifteen months and compared to market consensus for a rise to a level of 54.5. In the prior month, the PMI had recorded a level of 54.4.

Macroeconomic data indicated that the US flash Markit manufacturing PMI unexpectedly declined to a five-month low level of 53.4 in March, suggesting a slowdown in the nation's economic activity. The PMI had recorded a reading of 54.2 in the previous month, compared to market expectations of a rise to a level of 54.8. Further, the nation's services sector surprisingly eased to a level of 52.9 in March, growing at its slowest pace in six months and confounding market consensus for a rise to a level of 54.0. the PMI had registered a reading of 53.8 in the preceding month.

On the other hand, the nation's preliminary durable goods orders increased 1.7% in February, buoyed by greater demand for commercial aircraft and surpassing market expectations for a gain of 1.4%. Durable goods orders had advanced 2.0% in the previous month.

Meanwhile, the US House Republican, on Friday, pulled their health-care bill, thus adding to doubts over the Trump administration's ability to push through its pro-growth economic agenda.

In the Asian session, at GMT0300, the pair is trading at 1.0843, with the EUR trading 0.49% higher against the USD from Friday's close.

The pair is expected to find support at 1.0785, and a fall through could take it to the next support level of 1.0727. The pair is expected to find its first resistance at 1.0875, and a rise through could take it to the next resistance level of 1.0907.

Going ahead, investors will focus on Germany's Ifo expectations and business climate indices for March, slated to release in a few hours. Moreover, speeches by the Federal Reserve (Fed) Bank of Chicago President, Charles Evans and Dallas Fed President, Robert Kaplan, both due later in the day, will be eyed by traders.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

GBP/USD: UK’s Mortgage Approvals At 3-Month Low Level In February

For the 24 hours to 23:00 GMT, the GBP declined 0.24% against the USD and closed at 1.2486 on Friday, after UK's BBA mortgage approvals registered an unexpected drop to a level 42.6K in February, hitting its lowest level since November 2016 and defying market expectations for a rise to a level of 44.9K. In the previous month, BBA mortgage approvals had recorded a revised reading of 44.1K.

In the Asian session, at GMT0300, the pair is trading at 1.2519, with the GBP trading 0.26% higher against the USD from Friday's close.

The pair is expected to find support at 1.2482, and a fall through could take it to the next support level of 1.2446. The pair is expected to find its first resistance at 1.2539, and a rise through could take it to the next resistance level of 1.2560.

With no economic releases in the UK today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

USD/JPY: Monetary Policy Will Remain Easy For Some Time: BoJ Summary Of Opinions

For the 24 hours to 23:00 GMT, the USD rose 0.15% against the JPY and closed at 111.19 on Friday.

In the Asian session, at GMT0300, the pair is trading at 110.35, with the USD trading 0.76% lower against the JPY from Friday’s close.

The Bank of Japan (BoJ), in its summary of opinions report from its March meeting, indicated that easy monetary policy will be in place for some time as consumer price growth is still distant from the central bank’s 2% inflation target.

The pair is expected to find support at 109.89, and a fall through could take it to the next support level of 109.44. The pair is expected to find its first resistance at 111.14, and a rise through could take it to the next resistance level of 111.94.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

USD/CHF: Swiss Franc Trading Higher In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.21% against the CHF and closed at 0.9911 on Friday.

In the Asian session, at GMT0300, the pair is trading at 0.9878, with the USD trading 0.33% lower against the CHF from Friday’s close.

The pair is expected to find support at 0.9848, and a fall through could take it to the next support level of 0.9817. The pair is expected to find its first resistance at 0.9934, and a rise through could take it to the next resistance level of 0.9989.

Amid a lack of economic releases in Switzerland today, trading trend in the CHF is expected to be determined by global macroeconomic events.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

USD/CAD: Canadian Annual Inflation Softer Than Anticipated In February

For the 24 hours to 23:00 GMT, the USD rose 0.17% against the CAD and closed at 1.3377 on Friday.

The Canadian Dollar lost ground, after Canada's consumer price index (CPI) rose less-than-anticipated by 2.0% on an annual basis in February, compared to market expectations for an advance of 2.1%. The CPI had climbed 2.1% in the prior month. Meanwhile, on a monthly basis, the CPI rose 0.2% in

February, meeting market expectations and after recording a gain of 0.9% in the previous month.

In the Asian session, at GMT0300, the pair is trading at 1.3331, with the USD trading 0.34% lower against the CAD from Friday's close.

The pair is expected to find support at 1.3307, and a fall through could take it to the next support level of 1.3282. The pair is expected to find its first resistance at 1.3370, and a rise through could take it to the next resistance level of 1.3408.

Moving ahead, market participants will focus on the Bank of Canada's business outlook survey report, slated to release later in the day.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

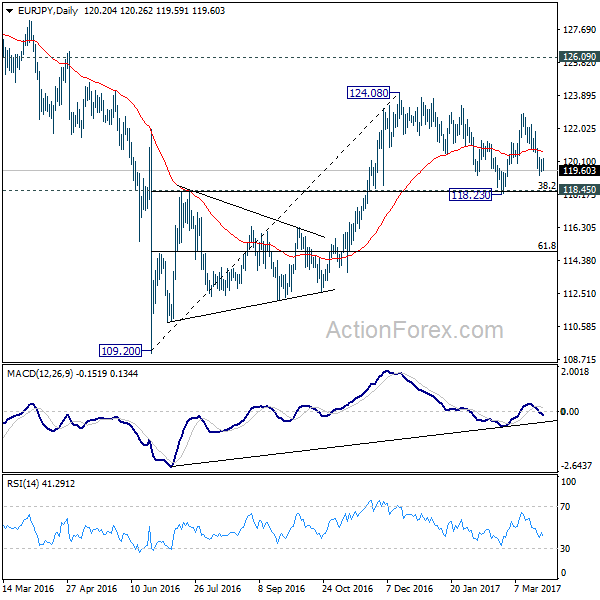

EUR/JPY Daily Outlook

Daily Pivots: (S1) 119.72; (P) 119.98; (R1) 120.45; More...

Intraday bias in EUR/JPY is remains neutral at this point. On the downside, break of 119.31 will bring deeper fall towards 118.23 low. But we'd expect strong support from 118.45 key cluster support level (38.2% retracement of 109.20 to 124.08 at 118.39) to contain downside and bring rebound. On the upside, above 120.81 minor resistance will turn bias back to the upside for 124.08 high. Overall, price actions from 124.08 are developing into a consolidative pattern and upside breakout is expected later.

In the bigger picture, we're holding on to the view that medium term rise from 109.20 is still in progress. Focus is on 126.09 key resistance level. Sustained break will confirm completion of the whole decline from 149.76. And rise from 109.20 is of the same degree as the fall from 149.76. In such case, further rally would be seen to 104.04 resistance and possibly above before topping. Meanwhile, rejection from 126.09, or firm break of 118.45 cluster support, will likely extend the fall from 149.76 through 109.20 low.

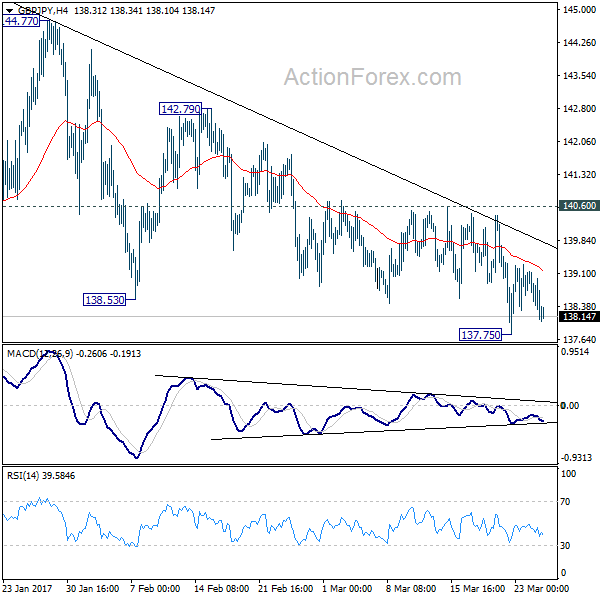

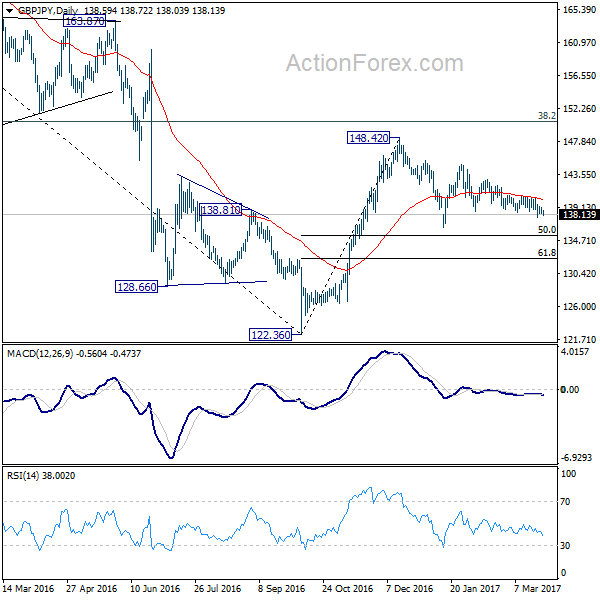

GBP/JPY Daily Outlook

Daily Pivots: (S1) 138.34; (P) 138.75; (R1) 139.21; More...

Intraday bias in GBP/JPY stays neutral first. Current development argues that choppy fall from 144.77 is still in progress. Further decline is mildly in favor as long as 140.60 resistance holds. Below 137.75 will target 136.44 support and below. But we'd expect support from 50% retracement of 122.36 to 148.42 at 135.39 to contain downside and bring rebound. On the upside, break of 140.60 resistance will turn bias to the upside and send GBP/JPY through 144.77 resistance. Overall, price actions from 148.42 are forming a consolidation pattern.

In the bigger picture, price actions from 122.36 medium term bottom are still seen as a corrective pattern. Main focus is on 38.2% retracement of 195.86 to 122.36 at 150.42. Rejection from there will turn the cross into medium term sideway pattern. Or, sustained break of 50% retracement of 122.36 to 148.42 at 135.39 will turn outlook bearish for a test on 122.36 low. Though, sustained break of 150.42 will extend the rebound towards 61.8% retracement of 195.86 to 122.36 at 167.78.

Asian Equity Markets Are Falling In Line With US Markets

Market movers today

The main event this week is set to be the UK's triggering of Article 50 on Wednesday. The first part of the negotiations will be centred on the ‘divorce bill' for the UK. The EU has made it clear that substantial progress on this issue will have been delivered before starting negotiations on a new trade deal.

On the date front today, in the euro area we are due to get the February figures for loan growth and M3 money supply growth. Loan growth increased for three consecutive months, from 1.8% yearly growth in October 2016 to 2.2% in January 2017. We estimate it increased further to 2.4% in February.

German Ifo expectations are also due to be released Today. Ifo expectations saw a fall in January to 103.2 from 105.5 in December 2016, but increased to 104.0 again in February. We believe it will have increased a bit further to 104.3 in March. Other survey indicators still indicate optimism in the business economy but German consumer confidence has started to trend lower and in coming months, we expect the same correction in the strong business sentiment seen recently.

German retail sales for February are also due for release. In January, we saw a monthly decline of 1.0% but we estimate a bounce back in February to 0.6%, as consumer confidence remains at a high level and low unemployment supports consumption. Note also that German unemployment figures are scheduled for release on Friday.

We also have two speeches from ECB executive board members. Peter Praet is set to speak on Monday, with Benoit Coeuré due to speak on Friday. The speeches are of special interest to market participants, as speculation about whether the ECB could hike rates before the termination of the QE programme has started to be priced in.

Selected market news

The dollar and US equity futures are this morning building on Friday's declines and gold is climbing further with bonds. This move comes after the failure of the US Congress on Friday night to pass the bill to replace Obamacare. As a result, the market is increasingly questioning whether the Trump administration will be able to pass any significant tax reforms and infrastructure bill, which is far more important for the economy than Obamacare. In our view, changes to US economic policy are likely to come later and be smaller than previously expected due to the chaos within the Republican Party. Asian equity markets are falling in line with US markets this morning. Emerging market currencies are on the other hand gaining against the USD, as a delay to expansionary fiscal policy in the US reduces the risk of more frequent Fed hikes than currently priced in by the markets.

In Europe, the EU leaders (excluding the UK government) showed unity in Rome, where they met to celebrate the 60th anniversary for the Rome Treaty this weekend. Prior to the meeting, there had been some fear that certain member states, such as Poland and Greece, would hijack the meeting to show their frustration against current EU policies, but this did not happen. At the meeting, German chancellor Angela Merkel said that the EU could move forward at different speeds.

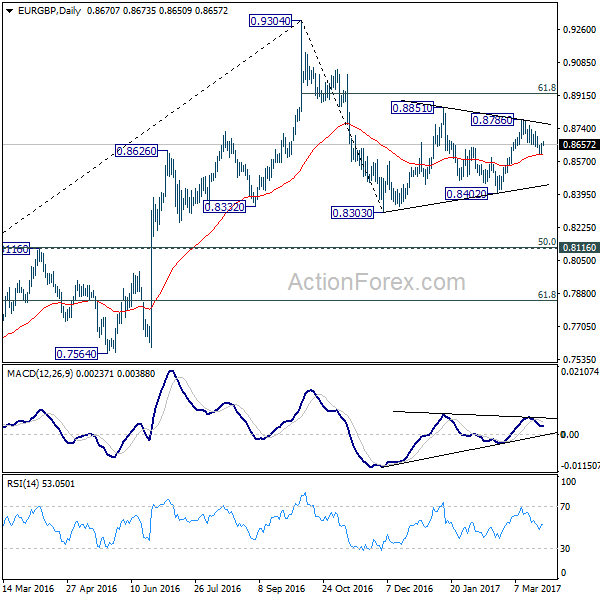

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8622; (P) 0.8642; (R1) 0.8674; More...

Intraday bias in EUR/GBP remains neutral for the moment. With 0.8699 minor resistance intact, deeper decline is mildly in favor. Below 0.8604 will target 61.8% of 0.8402 to 0.8786 at 0.8549 and possibly below. In that case, we'll look for support above to 0.8402 to bring another rebound before completing that correction from 0.8303. On the upside, above 0.8699 will turn bias back to the upside for 0.8786. Break will target 61.8% retracement of 0.9304 to 0.8303 at 0.8922 to finish the pattern from 0.8303. Overall, price actions from 0.8303 are forming a corrective pattern, as the second leg of the correction from 0.9304.

In the bigger picture, price actions from 0.9304 are viewed as a medium term corrective pattern. Deeper fall cannot be ruled out yet. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside. Overall, the corrective pattern would take some time to complete before long term up trend resumes at a later stage. Break of 0.9304 will pave the way to 0.9799 (2008 high).