Sample Category Title

Canadian Dollar Steady as Manufacturing Sales Posts Gain

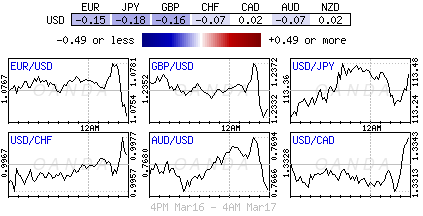

USD/CAD is unchanged in the Friday session. In North American trade, the pair is trading slightly above the 1.33 line. On the release front, Canadian Manufacturing Sales gained 0.6% in January, marking a third straight gain. In the US, today's highlight is US Preliminary UoM Consumer Sentiment, which is expected to improve to 97.1 points.

As widely expected, the Federal Reserve raised rates by a quarter-point on Wednesday. The rate hike, the second in just three months, raised the benchmark lending rate to a 0.75%-1% range. The dollar reacted negatively, declining broadly against its major rivals. This was largely due to disappointment with the Fed, which sent a more dovish message than the markets wanted to hear. Leading up the rate announcement, there had been speculation that a red-hot US economy would propel the Fed to accelerate its pace of monetary tightening, with possibly four rate hikes this year. Instead, Fed Chair Janet Yellen reiterated that further rate hikes would be "gradual" and left its "dot plot" unchanged, with a projection for three rate hikes in 2017. As well, the US dollar may have lost ground due to traders and investors acting on "buy on rumor, sell on fact". This large-scale selling of US dollars after the Fed hike has sent the US dollar broadly lower, and the Canadian dollar has taken advantage, gaining 1.1 percent this week.

Oil remains under pressure, and weak crude prices could weigh on the Canadian dollar. West Texas crude plunged 8.7 percent last week and dipped below the $47 level this week. US Crude Oil Inventories finally reversed directions, posting a drawdown of 0.2 million barrels, compared to an estimate of 3.3 million. This decline comes after the indicator posted 11 surpluses in the past 12 weeks, reflective of increasing US shale production. OPEC cobbled together a deal to cut production which began on January 1, but the expected jump in oil prices has failed to materialize, as the increase in US production has more than offset the OPEC cutbacks.

Markets are Mellow ahead of G20 Meeting

The "dovish hike" powered stock market rally slightly cooled off during Friday's trading session with investors turning cautious ahead of the anticipated G20 meeting. Asian shares were mostly mixed as participants weighed on the prospects of fewer US interest rates increases this year. In Europe, the defensive trading mood slightly pressured equities and the bearish contagion could limit gains on Wall Street this evening. An explosively volatile trading week is slowly coming to an end with investors turning their attention towards the G20 finance meeting which could offer some insights on how world leaders feel about key topics such as protectionism and global growth. With some discussions of currencies also being a possibility, the Greenback could turn volatile if leaders start to discuss the impacts of its resurgence since Trump's presidential victory.

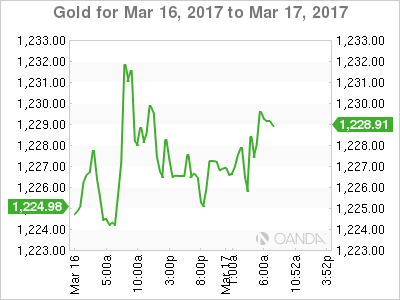

Gold elevated by Feds caution

Gold has staged a sharp rebound this week with prices springing above $1230 after the Federal Reserve signaled a more gradual pace of monetary tightening in 2017 then what markets anticipated. The "dovish hike" and caution displayed by the Fed simply disappointed many hawks consequently exposing the Dollar to downside shocks. Although bulls have exploited Dollar's weakness to elevate Gold, gains could be limited in the longer term if the Fed readopts an aggressive stance. With sentiment towards the U.S economy firmly bullish, the Greenback remains supported consequently capping gains on Gold in the medium to longer term. From a technical standpoint, although prices are turning bullish on the daily charts, the $1240 regions could act as a checkpoint for bears to attack prices lower.

Currency spotlight - Dollar

The Greenback was under intense selling pressure this week after the Federal Reserve's cautious attitude to future rate hikes left the hawks empty handed. Although the depreciation this week has sent the Dollar Index towards 100.20, prices may remain buoyed in the longer term amid the bullish sentiment towards the U.S economy. Much attention may be directed to how the Dollar Index reacts around the 100.00 psychological support which could be a real game changer for the bulls or bears.

Commodity spotlight - WTI

The rapidly diminishing optimism over the OPEC production cut deal has heavily dented buying sentiment towards Oil with the commodity struggling below $49.50 as of writing. Although U.S Crude stockpiles have eased from record levels last week, concerns still remain elevated over the high global inventories. With concerns lingering over the compliance of some OPEC and non-OPEC members to cutting production, the upside on oil seems limited. While some remain cautiously optimistic towards OPEC renewing their six-month supply cut to sustain the recovery in oil prices, the resurgence of U.S shale and lingering fears of members not following compliance could obstruct the extension. From a technical standpoint, WTI is heavily bearish on the daily charts. Bears remain in firm control below $50.

FTSE Pressured by Fresh Strength of Pound

FTSE opened lower on Friday, pressured by fresh strength of pound, after BoE's policy voting on Thursday hinted possible earlier rate hike.

The index dipped to 7329 (near 61.8% of 7254/7444 09/16 Mar upleg) after posting fresh all-time high at 7444 on Thursday.

Near-term studies weakened on today's fall and see increased risk of deeper pullback, as pound continues to rally.

While today's gap remains unfilled, immediate risk is expected to stay shifted lower, with close below Fibo support at 7326, seen as another bearish signal.

Rising daily Kijun-sen marks next good support at 7306, loss of which would increase risk of return to 7254 (09 Mar correction low).

Conversely, filling today's gap would generate positive signal and keep near-term focus at the upside.

Res: 7368; 7389; 7424; 7444

Sup: 7329; 7306; 7298; 7254

One-Minute Round Up: A ‘Less Hawkish’ Fed Has the Market Rethinking Strategy

There is a lot to absorb after this week's market sensitive events.

It's been a busy week on the central bank front. Aside from the Fed and the PBoC, many have stood pat (Norges, BoE, BoJ), but their tone and statements have changed a tad, which is supporting their own currencies.

The defeat in this week's Dutch elections of anti-immigration candidate Geert Wilders is being seen as a blow to populist political leaders, easing concerns ahead of next months French Presidential election – the French/Bund spread has narrowed to its lowest level in sometime.

On Wednesday, the Fed hiked as expected, but the dollar has taken a beating, and is poised for its first monthly loss in a month, as investors re-price three rate hikes for 2017, rather that last weeks four.

The ECB's Nowotny (Austria) has suggested that their strategy for tightening policy would be different from the Feds. The EUR (€1.0770) has seen a significant move higher, supported by the possibility that the ECB could start to raise rates before its QE program is complete.

Sterling (£1.2382) is consolidating its post-BoE Thursday spike as the decision mentioned 'price pressures.' This morning, the BoE's sole dissenter, Kristin Forbes, has clarified his surprise call for a hike, noting a change to growth and inflation data suggest that rates should rise. Futures indicate that the next rate move is higher not lower, and are pricing in a +50% probability of a +25 bps rate increase in 2018. Before yesterday's announcement, this figure stood at +30%.

The PBoC China's central bank also raised borrowing costs this week, while the BoJ left its monetary policy setting unchanged. The PBoC's +10bp increase in reverse repo and MLF (medium term lending facility) rates is part of policymakers deleveraging efforts in key sectors of the economy (steel, coal, non-ferrous metals, and real estate) and not a policy shift.

Global stocks are on course for the best week since January after the Fed hiked without accelerating their timetable for future hikes.

Commodities have found support from a weaker dollar. Yesterday, gold futures notched their biggest daily gain in 10-months, as dealers bet the Fed risks letting inflation perk up beyond its +2% desired target.

Crude oil has a record OPEC compliance cut and an IEA statement that H1 supplies would be depleted to support higher prices.

The U.S yield curve has flattened now that the U.S 10-year yield has plummeted to +2.53% away from the markets psychological 'bear bond market' swing point north of +2.60%.

On this Friday morning, despite market volatility retreating somewhat, investors are also weighing if the White House can make good on its fiscal stimulus plan of a new tax regime, business deregulation and infrastructure spending.

There is also the G20 Finance Minister meet in Germany today and tomorrow. Participants are expected to focus on avoiding protectionism and FX devaluations, is that possible? Could make for an interesting open to Australasian markets on Sunday.

USD/CAD Trapped In A Range Bound Price Action

After a strong drop below 1.3385 level caused by USD profit taking and Fed being less hawkish than expected, the USD/CAD is stabilizing in a range bound market condition where the price is trapped between 2 POC zones. POC for possible buying is 1.3265-85 (L4, historical buyers, ATR pivot) while sellers should appear at upper POC 1.3375-90 (Ema89,ATR top, H5, weekly L4). At this point the price is in no man's land but Friday profit taking should give boost to volatility and zones should be reached.

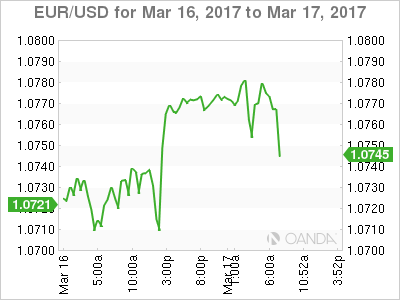

EUR/USD – Euro Rally Pauses, US Consumer Confidence Next

EUR/USD is unchanged in the Friday session, as the pair trades at 1.0770. On the release front, it’s a quiet end to the week. Eurozone Trade Balance slipped to EUR 15.7 billion, well short of the estimate of EUR 22.3 billion. In the US, today’s highlight is US Preliminary UoM Consumer Sentiment, which is expected to improve to 97.1 points.

There were no raised eyebrows when the Federal Reserve raised rates by a quarter-point on Wednesday, as the markets had priced a rate hike at over 90%. The rate hike, the second in just three months, raised the raised the benchmark lending rate to a 0.75%-1% range. What was not expected, however, was the sharp drop of the dollar against its major rivals. This was largely due to disappointment with the Fed, which sent a more dovish message than the markets wanted to hear. Leading up the rate announcement, there had been speculation that a red-hot US economy would propel the Fed to accelerate its pace of monetary tightening, with possibly four rate hikes this year. Instead, Fed Chair Janet Yellen reiterated that further rate hikes would be 'gradual' and left its 'dot plot' unchanged, with a projection for three rate hikes in 2017. As well, the US dollar may have lost ground due to traders and investors acting on 'buy on rumor, sell on fact'. This large-scale selling of US dollars after the Fed hike has sent the US dollar broadly lower, and gold has taken advantage with impressive gains of 2.5 percent since the Fed announcement.

European governments can breathe a sigh of relief following the results of the election in the Netherlands. The centre-right coalition of Prime Minister Mark Rutte won the most votes, handily defeating the anti-EU Freedom Party, headed by Geert Wilders. The election was closely watched across Europe, as it was viewed as a bellwether of populist sentiment on the continent. Leaders in France and Germany, who are also facing tight races due to rising anti-EU sentiment, are hopeful that they can copy Rutte’s recipe for electoral success. The election results have helped push the euro to its highest level February 5.

Gold Consolidating, Silver Bearish Consolidation, Crude Oil Ready For Another Leg Lower.

Gold Consolidating.

Gold's weakness has paused as the precious metal surged yesterday out of the Fed rate hike. Strong support is given at 1177 (11/01/2017 low). The short-term momentum seems strong and it would not be abnormal to see an increase again towards resistance at 1263 (27/02/2017 high).

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

Silver Bearish consolidation.

Silver's selling pressures have stopped below 17.00. Strong support is given at 16.63 (27/01/2016 low). Hourly resistance is now given at 17.52 (intraday high). Ongoing bearish pressures are due to some profit taking.

In the long-term, the death cross indicates that further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

Crude oil Ready for another leg lower.

Crude oil's bearish pressures continues despite ongoing consolidation due to some shortsqueeze. The commodity had been unable to mount a serious challenge to 55.24 (03/01/2017 high) resistance. Strong support given at 49.61 (08/12/2016) has been broken. Expected to see deeper selling pressures.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 24.82 (13/11/2002) while resistance can now be found at 55.24 (03/01/2017 high).

EUR/CHF Moving Sideways Between 1.0700 And 1.0750, EUR/JPY Setting Higher Lows, EUR/GBP Selling Pressures Are Lively.

EUR/CHF Moving sideways between 1.0700 and 1.0750.

EUR/CHF's renewed bearish pressures continues to increase. The medium-term pattern suggests us to see continued bearish pressures towards key support that can be found at 1.0623 (24/06/2016 low). Temporary surges seem the new normal for the CHF.

In the longer term, the technical structure is mixed. Resistance can be found at 1.1200 (04/02/2015 high). Yet,the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

EUR/JPY Setting higher lows.

EUR/JPY's momentum is definitely bullish despite ongoing momentum. Hourly support lies at 121.13 (intraday low). Strong resistance is given at a distance at 123.31 (27/01/2017 high).

In the longer term, the technical structure validates a medium-term succession of lower highs and lower lows. As a result, the resistance at 149.78 (08/12/2014 high) has likely marked the end of the rise that started in July 2012. Strong support at 94.12 (24/07/2012 low) looks nonetheless far away.

EUR/GBP Selling pressures are lively.

EUR/GBP is trading lower despite ongoing volatility Selling pressures increase around 0.8800. Key resistance is given at 0.8854 (15/01/2017 high). The road is wide-open for further weakness as there is no close support.

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 psychological level.

USD/CHF Pushing Slightly Lower, USD/CAD Bullish Pressures Have Faded, AUD/USD Consolidating.

USD/CHF Pushing slightly lower

USD/CHF keeps on weakening since the pair has exited uptrend channel. Hourly support is given at 0.9862 (31/01/2017 low) has been broken. Key resistance can be found at a distance at 1.0344 (15/12/2016 high). Expected to consolidate.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/CAD Bullish pressures have faded.

USD/CAD's bullish pressures have ended abruptly. The road seems wide-open for larger decline. Key support is given at 1.2969 (31/01/2017 low).

In the longer term, there is a golden cross with the 50 dma crossing the 200 dma indicating further upside pressures. Strong resistance is given at 1.4690 (22/01/2016 high). Long-term support can be found at 1.2461 (16/03/2015 low).

AUD/USD Consolidating.

AUD/USD's technical structure has changed. Support is given at 0.7494 (19/01/2017 low). Expected to target key resistance can be found at 0.7778 (08/11/2016 high).

In the long-term, we are waiting for further signs that the current downtrend is ending. Key supports stand at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8295 (15/01/2015 high) is needed to invalidate our long-term bearish view.

EUR/USD Strengthening, GBP/USD Bouncing Higher Within Downtrend Channel, USD/JPY Trading Mixed.

EUR/USD Strengthening.

EUR/USD keeps on strengthening. The pair is lying in an uptrend channel. Key resistance is still given at a distance 1.0874 (08/12/2017 high). Strong support can be found at 1.0493 (22/02/2017 low). The technical structure suggests deeper increase towards resistance at 1.0874.

In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBP/USD Bouncing higher within downtrend channel.

GBP/USD is moving up but the pair remains around support given at 1.2254 (19/01/2017 low). The road is still wide-open for further decline. Hourly resistance is given at 1.2300 (05/03/2017 high).

The long-term technical pattern is even more negative since the Brexit vote has paved the way for further decline. Long-term support given at 1.0520 (01/03/85) represents a decent target. Long-term resistance is given at 1.5018 (24/06/2015) and would indicate a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

USD/JPY Trading mixed.

USD/JPY has failed to break key resistance given at 115.62 (19/01/2016 high). Hourly support given at 113.56 (06/03/2017 low) has been broken. Yet the pair is moving sideways.

We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).