Sample Category Title

Week Ahead Dollar Drops After Rate Hike

Fed speakers could stop USD slide

The USD is weaker against major currencies across the board after the Fed hiked rates for the third time since the financial crisis but lacked upgrades to the economic projections. A proactive but patient Fed, with other central banks standing pat, meant the forward looking FX market came away with a less hawkish view on future US interest rates and sold the USD despite a 25 basis points hike to the benchmark rate. Fed member speeches during the week will give the central bank the chance to add more clarity into the FOMC statement and Chair Yellen's press conference.

The Office for National Statistics in the UK will release the monthly inflation data on Tuesday, March 21 at 5:30 am EDT (9:30 GMT). After the Bank of England (BoE) held interest rates at 0.25 percent the minutes from the policy meeting showed members discussed raising rates if inflation accelerated. The lone dissenter in the BoE Kristen Forbes voted for a rate hike as she felt inflation was rising quickly and would remain above the BoE's target for at least 3 years. A higher inflation indicator on Tuesday would appreciate the pound as higher UK rates could happen sooner rather than later. UK retail sales data will be released on Thursday, March 23 at 5:30 am EDT (9:30 GMT) with a forecasted gain of 0.4 percent that could restore confidence after a drop last month.

The Reserve Bank of New Zealand (RBNZ) will publish its rate decision on Wednesday, March 22 at 4pm EDT (8pm GMT). Analysts expect the rate to remain unchanged at 1.75 percent after a disappointing fourth quarter GDP has reduced the probabilities of a rate hike in the short term.

The EUR/USD gained 1.201 percent in weekly trading. The single pair is trading at 1.0750 after the Fed hiked interest rates by 25 basis points for the first time in 2017. The market had already priced in the central bank move after heavy handed signalling from Fed members. Investors had become used to ignoring Fed comments and forecasts as for the past two years there was the promise of multiple rate hikes and in reality only 1 hike per year was delivered. The Fed had to change its communication strategy to avoid catching the market off guard as the CME FedWatch tool showed very low probabilities of a rate hike March as late as mid February.

The hype created by Fed officials was made into reality on March 15, but without further guidance and with a statement laced with less hawkish undertones investors sold the US dollar. The greenback is down against all majors ahead of a quiet week for US economic indicator releases. Fed Chair Janet Yellen will speak at a research conference in Washington on Thursday, March 23 at 8:45 am EDT (12:45 pm GMT) giving her another turn to comment on the central bank forecasts for US growth. Fed members Charles Evans, William Dudley, Neel Kashkari and Robert Kaplan are all scheduled to speak this week and could use the opportunity to clarify their stance on the central bank's rate path that triggered a drop in the USD after the March monetary policy meeting.

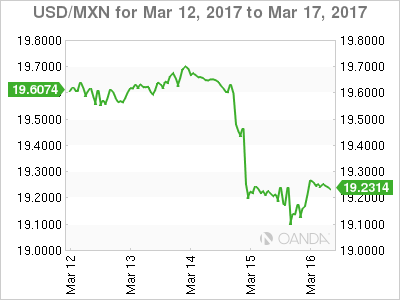

The USD/MXN lost 2.791 percent in the last five days. The currency pair is trading at 19.0852 after a new round of peso positive comments came from the Trump administration. Top trade advisor Peter Navarro said that a new trade agreement replacing NAFTA should make the Canada, Mexico and the United States collective a global manufacturing powerhouse. This follows comments from Secretary of State Rex W. Tillerson and John F. Kelly Secretary of Homeland Security during their joint visit to Mexico at the end of February. While being careful not to openly contradict the statements from President Trump, there has been a clear softening in the language used with regard to Mexico-US trade and immigration.

The MXN has appreciated versus the USD since the inauguration of President Donald Trump on January 20. The worst case scenarios for the peso have not materialized despite the rhetoric putting pressure on the Latin American currency during the lengthy election process and the eventual victory of Trump. The current US administration has focused on trade and immigration, but has not delivered details on what was seen as the biggest factor of the USD rally: pro-growth policies such as tax stimulus and infrastructure spending. The peso is trading near pre-election levels but risks remain as the US Federal Reserve appears willing to hike interest rates higher multiple times in 2017 and Secretary of Treasury Steven Mnuchin has reassured markets those pro-growth polices are coming.

XAU/USD gained 2.29 percent in the last week. The price of gold is trading at $1,229.42 as the USD retreated and political risk with a potential trigger of Article 50 in the coming week making the metal an attractive safe haven. The fact that the elections in the Netherlands did not signal an advance for eurosceptics did little to stem the anxiety regarding upcoming Brexit and the looming French elections where Marine LePen has a higher chance than the Dutch far-right candidate Geert Wilders did.

A rise in gold prices in the same week that the Fed announces a rate hike is not that common but the way the central bank communicated the impending March rate hike had investors changing expectations. The Fed might have oversold their hand as it only delivered a rate hike of 25 basis points, but kept forecasts unchanged which was taken as less hawkish than anticipated taking into account the Fedspeak that saw the market switch from 20 percent probability of a rate hike to 93 percent in three weeks.

Market events to watch this week:

Monday, March 20

- 8:30pm AUD Monetary Policy Meeting Minutes

Tuesday, March 21

- 5:30am GBP CPI y/y

- 8:30am CAD Core Retail Sales m/m

Wednesday, March 22

- 10:30am USD Crude Oil Inventories

- 4:00pm NZD Official Cash Rate

- 4:00pm NZD RBNZ Rate Statement

Thursday, March 23

- 5:30am GBP Retail Sales m/m

- 8:00am USD Fed Chair Yellen Speaks

- 8:30am USD Unemployment Claims

Friday, March 24

- 8:30am CAD CPI m/m

- 8:30am USD Core Durable Goods Orders m/m

*All times EST

Trade Idea Wrap-up: USD/CHF – Sell at 1.0020

USD/CHF - 0.9968

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9967

Kijun-Sen level : 0.9979

Ichimoku cloud top : 1.0046

Ichimoku cloud bottom : 1.0019

Original strategy :

Sell at 1.0020, Target: 0.9920, Stop: 1.0055

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.0020, Target: 0.9920, Stop: 1.0055

Position : -

Target : -

Stop : -

As the greenback has remained under pressure, suggesting recent decline from 1.0171 is still in progress and may extend further weakness to 0.9920-25, however, loss of near term downward momentum should prevent sharp fall below 0.9900 and reckon 0.9870-75 would hold from here, risk from there has increased for a strong rebound later.

In view of this, would not chase this fall here and would be prudent to sell dollar on recovery as the lower Kumo (now at 1.0019) should limit upside and bring another decline. Only above previous support at 1.0060 (now resistance) would abort and signal low is formed instead, risk rebound to 1.0090-95 first.

Trade Idea Wrap-up: GBP/USD – Buy at 1.2310

GBP/USD - 1.0755

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.2349

Kijun-Sen level : 1.2309

Ichimoku cloud top : 1.2258

Ichimoku cloud bottom : 1.2210

Original strategy :

Buy at 1.2290, Target: 1.2400, Stop: 1.2255

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.2290, Target: 1.2400, Stop: 1.2255

Position : -

Target : -

Stop : -

As cable has eased after rising to 1.2399, suggesting consolidation below this level would be seen and pullback to 1.2320-25 cannot be ruled out, however, reckon downside would be limited o 1.2290-00 and bring another rise later, above said resistance at 1.2399 would extend recent rise from 1.2109 low to 1.2410-15 but reckon 1.2440-50 would hold, price should falter well below resistance at 1.2471, bring retreat later.

In view of this, would not chase this move from here and we are looking to buy cable on pullback as 1.2290-00 should limit downside and bring another rise. Below 1.2265-70 would suggest top is possibly formed, risk test of said support at 1.2241 which is likely to hold on first testing.

Weekly Market Outlook: Fed/ECB Policy Collision

Fed / ECB Policy Collision

At the start of the year the dominate thinking in FX markets was USD would outperform in the G10. With the Fed the only G10 central banks raising policy rates in 2017, yields differential would favor rotation in the greenback. However, with economic data in Europe rapidly improving, political risk dissipating and ECB members comments sounding hawkish the probability of ECB tightening has increase meaningfully. As stated in our Yearly Market Outlook the likelihood Fed and ECB policy converging in September forcing investors to shift their rate rotation strategy remains resilient.

Last weeks FOMC 25bp hike to 75-100bp indicates a reaction to rising inflation, strong confidence levels and robust optimism in financial markets. Yet lack of real improvement in data including core inflation and failure of real wages to improve forced a "dovish hike" statement (despite arguments to the contrary). The Fed fund rate median "dots "remained unchanged at three hikes in 2017 followed by three more in 2018. Yellens statement "we have plenty of time to see what happens" suggest a comfort level and not panic policy setting many had suggested. The sharp reaction in asset with US 10 year yields dropping 10bp, S&P jumping 1%, USD falling and rush into all things EM indicates scant worries of a steeper tightening cycle.

Barring any political upheaval (which is clearly a big "If") , by September, conditions should be correct for the ECB to begin indicating the removal of emergency support framework. At the ECB press conference Draghi indicated that risks of deflation had "largely disappeared" and stated that the ECB "no longer had a sense of urgency" is taking further action, clearly hawkish tone.

While in an interview with Handelsblatt ECB council member Nowotny suggested that process of policy normalization could see increase in the deposit rate ahead of ending bond purchases and prime rate. This is counter to the general expectations for ending QE before raising interest rate. It also opens the prospect of advance tightening. With a shallow Fed policy path and the ECB shifting toward less accommodation it's hard to forecast sustained EURUSD weakness below 1.05. In addition, convergent tighter monetary policy around September should have impact of unbridled equity optimism.

Brexit: When Will Article 50 Be Triggered?

What a contradiction! The expected economic nightmare triggered by the Brexit vote has not materialised. Indeed, unemployment rate has reached its lowest level in 42 years at just 4.7%. It seems that at least for now, the UK economy is not the worse off from its decision to exit of the European Union. Nonetheless, it is worth noting that pressure on wages are almost non-existent. One explanation, the lack of job security (for example with the zero-hour contract) is showing the structural change of the labour market not only in the UK but globally in the western world. This definitely pushes unemployment rate to go lower.

Earlier last week, the Bank of England decided to keep its interest rates unchanged at 0.25%. It is clear that Brexit fears are helping the central bank as the pound remains weak. On top of that, we see European uncertainties growing in the medium term, in particular given the impact the French Elections outcome may have.

When looking more specifically at data, inflation is on the rise and we should see the BoE hinting to further tightening in the medium-term. The triggering of the article 50 looms and negotiations are likely to last longer than expected as trade agreements are paramount for the future UK competitiveness.

As Brexit proceedings drag on and fears of a hard Brexit continue to loom large, the pound continues to paint a very vivid picture of market worries. At present, UK Parliament remains split on PM May's EU exit plans. The outcome however will be of little relevance as May will likely plough on and trigger Article 50 as planned. The question on everyone's lips right now of course is whether the PM will cut the cord with no actual deal in place.

The pound has been feeling the heat from both the single currency and the greenback over the past couple of weeks on the back of renewed hard Brexit fears. We believe that there is a strong opportunity to reload bullish pound positions. The dragging out of these proceedings will be more damaging than the actual exit itself. Brexit will clearly not be the promised apocalyptic nightmare and will allow the UK breathing space to regain its competitive stance, free from constraint from Brussels.

Negative Real Wage Growth Threatens US Recovery

The US dollar had a tough week amid lacklustre economic data and a rather dovish Federal Reserve. The US economy created 235k private jobs in February, widely beating the median forecast of 200k, while the previous month's reading was upwardly revised to 238k. All employment measures improved in February as the unemployment rate eased to 4.7% as participation climbed to 63%. The U-6 measure, commonly known as the underemployment rate, fell to 9.2% from 9.4% a month previous. So, after such a bullish report how come the Fed sound that dovish?

Well, there are a few explanations for this. Firstly, wage growth clearly failed to impress despite the solid pace of job creation. Average hourly earnings grew 0.2%m/m versus 0.3% expected. In addition, inflation pressures have intensified over the last few months as crude oil prices recovered - the consumer price index rose 2.7%y/y in February. Taken together, these developments pushed real wage growth in negative territory during the first two months of the year - average weekly earnings contracted -0.5%y/y and -0.3%y/y in January and February respectively - which will ultimately translates into weaker purchasing power for the common American in the longer run. This is the first time since December 2013 that the gauge has dipped below the neutral threshold. In fact, since the fourth quarter of 2015 real wage growth has started to decelerate. This negative trend could explain why the Fed was not in such a hurry to raise rates last year.

Over the coming months the Fed will find itself on the hot seat as core inflation pressure remains subdued and US consumer are suffering from weaker purchasing power. As a quick reminder consumer spending accounts for roughly 70% of the US GDP. Moreover, less disposable money for consumers means less price pressure, which translates into falling consumer prices, which ultimately means that the Fed will have to increase rates slowly if not taking a break during the process altogether.

It is not without reason that Janet Yellen stressed, during the press conference, that the Fed remains data-dependent and not interested in aggressive tightening. So far the Fed appears relatively confident, meaning that it is betting heavily on Trump's economic programme.

All in all, in the short-term the market will stay focused on the political risk in Europe, which would help the dollar to hold ground against the single currency. The dollar's medium-term outlook is heavily dependent on the results of the EU political elections; however, should the political chessboard stay unchanged in Europe, the USD will start to reverse gains.

BioTech Revolution

The pharmaceutical industry is going through a minor revolution. Biotechnology has a broad mandate, covering a wide range of processes for transforming living organisms for human purposes. However, this theme focuses on a new breed of companies that have joined the race to use modern technology to create healthcare products. These companies harness cellular and bio-molecular processes to develop technologies and products to fight disease. Exploding R&D costs have forced traditional pharma companies to look to smaller, more agile, technology-driven firms as the primary pipeline for innovation. With public and private investors and big pharma all expecting the next big breakthrough to come from this dynamic sector, valuations are on the rise.

We built this theme by filtering on firms with a market capitalization of over $1 billion and positive sales growth over the past two years, ensuring that they have sufficient cash flow to fund the next blockbuster.

BioTech Revolution theme can now be trading in an easy to execute Strategic Certificate.

RBNZ Policy Decision, Key Economic Data in Focus

Next week's market movers

- In New Zealand, the RBNZ is likely to remain on hold and maintain its dovish bias amid lackluster economic data and elevated uncertainty around global trade.

- In the UK, CPI figures for February could impact market expectations with regards to near-term policy tightening by the BoE.

- We also get key economic data from Eurozone, the US, and Canada.

On Monday, we have a relatively light day, with no major events or indicators due to be released.

On Tuesday, the UK will release its CPI data for February. The forecast is for both the headline and the core rates to have risen, something supported by the UK services PMI for the month, which showed that rapidly rising input costs led to the largest increase in prices charged by service providers for eight-and-a-half years. At the latest BoE gathering, some members noted that they would consider reducing stimulus should there be any further upside news on the prospects for growth or inflation, while Kristyn Forbes actually voted for an immediate hike. This suggests that in case the CPIs accelerate further as expected, then the next big market theme could well be whether the BoE will reduce its asset purchases, or even hike rates at some point in the foreseeable future. At the very least, accelerating inflation is likely to lead to more hawkish dissents in coming months, assuming that economic growth remains robust. Having said all these though, we are skeptical as to whether we will actually see a BoE rate hike in the near-term, mainly because the Bank is unlikely to rush into monetary tightening before the Brexit negotiating landscape becomes clearer.

On Wednesday, late during the day, the RBNZ rate decision will be in the spotlight. At its latest gathering, the Bank retained its easing bias despite improving domestic economic data. Policymakers indicated that numerous uncertainties persist, particularly in the global outlook, and policy may need to adjust accordingly. As was later explained by Governor Wheeler, this was a reference to the risks surrounding exports and the prospect of increased global protectionism. What's more, the officials reiterated that a decline in the Kiwi's exchange rate is needed, something that became reality following their dovish policy signals. Since that meeting, economic data have been lackluster. Although the nation's terms of trade improved in Q4, GDP growth slowed notably in the quarter, much more than the RBNZ's own forecasts. To make matters worse, economic growth for Q3 was revised lower. Bearing also in mind that the aforementioned global risks remain elevated, we see no material reason for the Bank to shift to a more upbeat tone, especially since something like that could trigger a surge in NZD. Despite the fact that we expect the Bank to maintain a dovish bias though, we do not expect the officials to actually take action in the foreseeable future, barring some unforeseen shock. This view is amplified by the fact that the nation's 2-year inflation expectations have rebounded notably in recent quarters, alleviating some pressure from the Bank to take further steps in order to boost inflation.

On Thursday, the only major indicator we get is UK retail sales for February, but no forecast is presently available. Consumer sentiment indicators were mixed during the month. The TR/IPSOS figure declined, and while the Gfk index ticked up, it remained negative. The combination of these prints does not paint a clear picture about consumer optimism in the month. The fact that the BRC retail sales rate rose somewhat, but also remained negative, does not make the situation any clearer. Our own view is that both the headline and core rates are likely to have remained unchanged within the negative territory, with risks skewed to the upside. We base that on the hypothesis that if consumer demand was to continue deteriorating, it would be more clearly visible on the aforementioned sentiment indicators, we think.

On Friday, we get the preliminary manufacturing and services PMIs for March from several European nations and the Eurozone as a whole. Most of these indices are expected to have ticked down, but to still remain at elevated levels. Considering that all of these surveys are expected to show that Eurozone's economy continues to perform well, we believe that they are likely to be another set of pleasant news for ECB policymakers, who at their latest meeting shifted to a more optimistic tone. Although President Draghi reiterated that there is no convincing upward trend in the core CPI yet and as such the Bank will keep its stimulus program unchanged, he made it clear that there is diminished willingness among the Governing Council for any more extraordinary easing measures. If incoming data continue to show that economic growth and inflationary pressures are gradually picking up, then we would expect the ECB to drop more dovish aspects of its forward guidance in coming meetings. We think that the Bank's next step is to remove the word "lower" from the reference regarding rates remaining at current, or lower levels in the foreseeable future.

From the US, we get durable goods orders for February. Expectations are for the headline rate to have risen for the second consecutive month, while no forecast is available for the core figure. Our own view is that the core figure likely rose as well, after a minor slide in January. We base our expectations on the nation's ISM manufacturing PMI for the month, where the New Orders sub-index rose notably, indicating a rising pace of increase in new orders. What's more, US civilian aircraft orders were decent during the month, which further supports the forecast for another increase in the headline rate.

From Canada, we get CPI figures for February. In the absence of a forecast, we see the case for the core rate to have ticked up, but we are mindful on whether the headline rate followed suit. Our view for the core rate is based on Canada's Markit manufacturing PMI survey for February, which indicated that as a result of increased cost pressures, there was a solid increase in the prices of finished products. However, February's yearly change in oil prices suggests that the headline rate could stay unchanged, or even tick down, as energy-related effects start to filter out of the yearly CPI calculation. Although a potential acceleration in core inflation is likely to be an encouraging development for BoC policymakers, we do not expect this to lead to a material shift in their dovish tone. At its latest meeting, they did not appear particularly worried about inflation, but they did maintain a cautious tone with regards to exports, which continue to face competitiveness challenges as they noted. This was a hint that the strength of the Canadian dollar is muting the outlook for exports and as such, we expect BoC officials to maintain a relatively dovish tone in the foreseeable future, despite any modest progress in economic data.

Solid Improvement in Manufacturing Production

Don't sweat the flat reading for industrial production. The second-warmest February on record resulted in a second consecutive drop in utilities, but manufacturing output increased for a sixth straight month.

Continued Firming in Manufacturing

Going into today's report, there was some justification for anticipating an increase in manufacturing. The ISM's index for manufacturing business activity rose in February to its highest level since 2011. We already knew from the jobs report that manufacturers added 28,000 new employees to their payrolls in February—matching the biggest monthly increase in three and a half years. Despite the increased number of workers, the average weekly hours for the manufacturing sector held steady at 40.8, which matches the highest figure in the past year.

Manufacturing output, which comprises more than three quarters of all industrial output, increased 0.5 percent in February. This extends the winning streak to six months and lifts the three-month annualized growth rate for manufacturing production to its fastest clip since 2014. Given the momentum for production activity and employment in the sector, we remain confident that gradual improvement in manufacturing will continue.

February: Not a Month You Typically Say "Open the Windows" Utilities output fell 5.7 percent in February. According to the National Weather Service, it was the second-warmest February on record. In fact, the NOAA maintains a residential energy demand temperature index to gauge household utility needs. That measure fell to zero in February; that is the only time it has been zero during February in the 123-periods of record. With two consecutive monthly declines of more than 5 percent and much cooler weather so far in March, we would not be surprised to see a surge in utilities output next month.

Mining activity was up 2.7 percent in February. This adds to the 2.2 percent increase in January and was sufficient to lift the three-month annualized growth rate to its fastest pace since before the bottom fell out from underneath energy prices in the middle of 2014. The price of a barrel of crude oil rose above $54 for the first time since 2015 during the month and the rig count has jumped along with it. The CRB index, a price basket of commodities, rose to its highest level since 2014 in February. Prices have been up and down so far in March, but continued firming would be supportive of the recovery in the mining sector.

Little Inflationary Pressure from Manufacturing

The Federal Reserve raised its benchmark lending rate earlier this week, citing a firm labor market and an inflation environment that is consistent with its 2.0 percent target. Despite recent improvements in manufacturing, there is still a fair amount of slack in this sector. Capacity utilization at 75.4 percent in February remains well-below its longer-run average of 79 percent.

Elliott Wave Analysis: AUDUSD Intraday View

On the AUDUSD count we see price currently undergoing an intraday rally, which we see it as unfolding sub-wave b as part of a three wave correction in wave 4. Well, if that is the case, then more weakness will follow from around the 0.77250 region and down into wave c of 4. But if price keeps going higher, then we could be already trading in wave 5.

AUDUSD, 1H

Trade Idea: EUR/GBP – Buy at 0.8620

EUR/GBP - 0.8697

Recent wave: Major double three (A)-(B)-(C)-(X)-(A)-(B)-(C) is unfolding and 2nd (A) has possibly ended at 0.6936.

Trend: Near term down

Original strategy :

Buy at 0.8620, Target: 0.8750, Stop: 0.8580

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.8620, Target: 0.8750, Stop: 0.8580

Position : -

Target : -

Stop : -

Euro’s near term choppy trading is likely to continue and initial downside risk remains for pullback to 0.8645-48 (38.2% Fibonacci retracement of 0.8422-0.8788), however, reckon downside would be limited to 0.8615-20 and bring another rise later, break of 0.8760 would suggest the pullback from 0.8788 has ended, bring retest of this level, above there would extend the rise from 0.8403 low to 0.8800 but loss of near term upward momentum should prevent sharp move beyond 0.8825-30 and price should falter well below 0.8850.

In view of this, we are looking to buy euro on subsequent pullback as 0.8615-20 should limit downside. Below 0.8605 (50% Fibonacci retracement of 0.8422-0.8788) would defer and suggest top is possibly formed, risk test of 0.8560-65 (61.8% Fibonacci retracement) but support at 0.8547 should remain intact.

Our preferred count is that, after forming a major top at 0.9805 (wave V), (A)-(B)-(C) correction is unfolding with (A) leg ended at 0.8400 (A: 0.8637, B: 0.9491 and 5-waver C ended at 0.8400. Wave (B) has ended at 0.9413 and impulsive wave (C) has either ended at 0.8067 or may extend one more fall to 0.8000 before prospect of another rally. Current breach of indicated resistance at 0.9043 confirms our view that the (C) leg has ended and bring stronger rebound towards 0.9150/54, then towards 0.9240/50.

US Crude Oil Running Out of Steam

Yesterday's close in red signaled that recovery from $47.08 low might be running out of steam ahead of psychological / daily cloud base barrier at $50.00.

However, oil managed to close above 200SMA that marks solid support ($48.70) for the second day keeping in play hopes of fresh attempts higher.

Stronger direction signals could be expected on break of either pivot (48/70 or 50.00), while the price may spent some time in extended consolidation within this range.

Near-term studies are neutral, while bearish tone prevails on dailies and keep risk shifted lower.

Firm break below 200SMA would signal upside rejection and fresh weakness that may return to $47.08 low.

Conversely, violation of base of thick daily cloud ($50.00) would trigger stronger correction of $53.78/$47.08 fall.

Res: 49.10; 49.61; 50.00; 50.43

Sup: 48.70; 48.44; 47.90; 47.08

Trade Idea: USD/CAD – Stand aside

USD/CAD - 1.3330

Recent wave: Only wave v of c has ended at 0.9407 and wave C of major A-B-C correction is underway for headway to 1.4700

Trend: Near term up

New strategy :

Stand aside

Position: -

Target: -

Stop:-

Although the greenback has recovered from 1.3276, this week’s selloff suggests top has been formed at 1.3535 earlier and upside should be limited to 1.3380-90 and price should falter below previous support at 1.3421 (now resistance), bring another decline later, below said support at 1.3276 would add credence to our bearishness and extend the fall from 1.3535 for retracement of recent upmove to 1.3235-40 (61.8% Fibonacci retracement of 1.3056-1.3535) but reckon previous resistance at 1.3210 would hold due to near term oversold condition.

In view of this, would be prudent to stand aside in the meantime. Above previous support at 1.3421 (now resistance) would suggest low is formed, bring a stronger rebound to 1.3450 and possibly test of resistance at 1.3479, however, only break of 1.3495 resistance would indicate the pullback from 1.3535 has ended and bring retest of this level later.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.