Sample Category Title

European Market Update: Markets Await Trump’s 1st Major Policy Speech On Tuesday

Markets await Trump's 1st major policy speech on Tuesday

Notes/Observations

Overnight:

Asia:

China FX regulator SAFE: To strengthen supervision of FX market in 2017

China State Information Center (SIO) forecasted Q1 GDP at 6.6%

Europe:

UK PM May could agree to new Scottish independence vote on condition it was held after UK leaves EU

BOE's Saunders (MPC member): Brexit to have long-term "modest adverse" impact on UK GDP. Lack of credit freeze after Brexit vote likely the main factor behind economic resilience

UK govt said to announce curbs on new EU migrants on the same date PM May triggers Article 50 EU exit process on March 15th

ECB's Weidmann (Germany) reiterated that it still viewed the QE program "very critically"; ECB would not put a sudden end to its asset purchases

German Deputy Fin Min Spahn: Reiterates govt view that Greece must not be granted a "bail in" where creditors take a loss on their loans

Senior Merkel Ally Kauder:Europe should impose tariffs on US goods if Trump puts tariffs on imports from Europe

France Socialist Candidate Hamon failed to form possible alliance with far-left rival Jean-Luc Melenchon; Melenchon confirmed he will be a candidate

German Emnid Poll: Merkel's conservatives and the centre-left Social Democrats (SPD) are neck-and-neck at 32% (Note: elections in Sept)

Recent polls on France Presidential election (results in-line with priors). Odoxa Poll: 1st Round: Le Pen 27%, Macron 25%, Fillon 19%; 2nd Round: Macron 61%, Le Pen 39%

Italy Democratic Party scheduled party primaries for April 30th (Seen as precursor to calling an election)

Italy Eco Min Padoan refuted press speculation that he threatened to resign if effective reforms and planned privatizations are not carried out

ESM's Regling reiterates optimism that positions on Greece were growing closer. Reiterated view that could not make further payments to Greece without IMF involvement as would not be in line with what Govts had agreed

(DE) Moody's affirmed German sovereign rating at AAA; stable outlook

(GR) Fitch affirmed Greece sovereign rating at CCC

Americas:

US Treasury Sec Mnuchin: President Trump's first budget would not include any cuts to social welfare programs such as Social Security and Medicare. NY Times reported that Trump would not seek cuts to social welfare programs; Expected to seek sharp increases in defense spending and major cuts to other agencies, including the EPA. Trump administration could submit budget proposals as early as today

Economic date

(FI) Finland Feb Consumer Confidence: 20.8 v 21.0 prior; Business Confidence: 1 v 2 prior

(TR) Turkey Feb Economic Confidence: 91.5 v 85.7 prior

(ES) Spain Feb Preliminary CPI M/M: -0.3% v -0.2%e; Y/Y: 3.0% v 3.2%e

(ES) Spain Feb Preliminary CPI EU Harmonized M/M: -0.3% v -0.3%e; Y/Y: 3.0% v 3.1%e

(HU) Hungary Jan Unemployment Rate: 4.3% v 4.4% prior

(HK) Hong Kong Jan Trade Balance (HKD): -12.3B v -20.8Be, Exports Y/Y: -1.2% v +8.4%e; Imports Y/Y: -2.7% v +8.8%e

(SE) Sweden Jan Household Lending Y/Y: 7.2% v 7.1%e

(EU) Euro Zone Jan M3 Money Supply Y/Y: 4.9% v 4.8%e

(PT) Portugal Feb Consumer Confidence: -4.4 v -6.2 prior; Economic Climate Indicator: 1.3 v 1.2 prior

(EU) Euro Zone Feb Business Climate Indicator: ### v 0.79e; Consumer Confidence (Final): ## v -6.2e

Fixed Income Issuance:

(DK) Denmark sold total DKK4.04B in 3-month and 6-month Bills

(NO) Norway sold NOK4.0B vs. NOK4.0B indicated in 6-month Bills;Avg Yield: 0.50% v 0.52% prior; Bid-to-cover: 2.15x v 2.85x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Index snapshot (as of 10:00 GMT)

Indices [Stoxx50 +0.2% at 3,313, FTSE +0.2% at 7,260, DAX +0.1% at 11,819, CAC-40 -0.1% at 4,842, IBEX-35 +0.1% at 9,458, FTSE MIB +0.8% at 18,737, SMI -0.2% at 8,508, S&P 500 Futures flat]

Market Focal Points/Key Themes: European equity indices are trading mixed in the morning session after an overall negative end to the Asian session overnight; Markets jittery as participants await Trump's address to Congress on spending and tax plans tomorrow; FTSE 100 weighed by insurers Direct Line and Admiral after the Chancellor amended the discount rate for PI claims to -0.75% resulting in financial impacts on FY16 profits; shares of the LSE also trading lower after the board announced that it is highly unlikely that a sale of MTS could be satisfactorily achieved, therefore the proposed merger with Deutsche Boerse would unlikely to be approved by the European Commission; the major banking stocks providing support across the indices; Energy stocks trading notably higher as WTI and Brent trade higher intraday.

Upcoming scheduled US earnings (pre-market) include AES Corp, Amtrust Financial Services, American Tower, American Woodmark, Armstrong World Industries, Sotheby's Holdings, Crawford & Co, FEMSA, Horizon Pharma, Installed Building Products, JinkoSolar, Kosmos Energy, National General Holdings, Senior Housing, TEGNA, and TransCanada.

Equities (as of 09:50 GMT)

Consumer Discretionary: [Associated British Foods ABF.UK -0.9% (trading update), Bunzl BNZL.UK +1.8% (FY16 results), Persimmon PSN.UK -0.4% (FY16 results, strategic update), Sopra Steria SOP.FR +4.5% (FY16 results), SHW SW1.DE -1.4% (FY16 results), Volex VLX.UK +7.6% (trading statement)]

Financials: [Admiral Group ADM.UK -4.4% (net financial impact on profits of £70-100M from reduction in discount rate), Deutsche Boerse DB1.DE -4.4% (LSE said its proposed merger was unlikely to be approved by the European Commission), Direct Line Insurance DLG.UK -7.6% (impact of Lord Chancellor's announcement), eSure ESUR.UK +2.8% (trading update), Hiscox HSX.UK +0.8% (FY16 results), London Stock Exchange LSE.UK -3.2% (Board believes that it is highly unlikely that a sale of MTS could be satisfactorily achieved), Senior PLC SNR.UK -1.8% (FY16 results)]

Healthcare: [Almirall ALM.ES -3.6% (FY16 results), arGEN-X ARGX.BE +1.0% (Shire alliance extension)]

Industrials: [Dassault Aviation AM.FR +0.8% (prelim FY16 sales), PostNL PNL.NL -6.4% (Q4 results), Rotork ROR.UK +3.7% (FY16 results), Volkswagen VOW3.DE -0.9% (prelim FY16 results)]

Materials: [Recticel REC.BE +5.8% (FY16 results)]

Speakers

Japan 2017 Budget Bill said to pass lower house

China PBOC official reiterated govt view that China's monetary policy should be more neutral; should keep liquidity basically stable

Currencies

USD consolidated its recent losses ahead of President Trump's first major policy address to Congress on Tuesday. President expected to include some details of his infrastructure spending and tax plans, but some market participants worry that a lack of fresh direction could disappoint investors and weigh on the USD

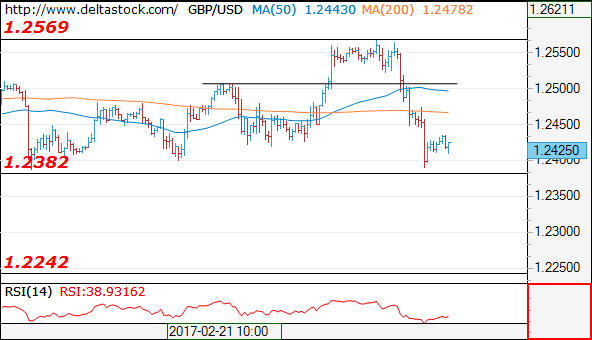

GBP was softer in both Asia and European sessions on reports that about the Scottish government was possibly seeking another independence referendum next year. Such news has circulated in recent weeks but remained a headwind for the pound sterling. GBP/USD was at 1.2425 area after testing a low of 1.2383

EUR/USD was higher by 0.3% to trade at 1.0590.

USD/JPY moved off its 2-week lows from Asia and stayed above the key 111 support level. The pair was holding steady at 112.25 just ahead of the NY morning.

Fixed Income:

Bund futures trade at 166.03 down 17 ticks trading in the lower portion of today's range, fading some of the move higher seen last week. Further downside momentum targets 165.60 initially followed by 165.31. A resumption higher targets 166.40 followed by 166.61.

Gilt futures trade at 128.13 up 8 ticks with volatility likely to increase due to futures rolling to the June contract this week. Resistance moves to 128.32 Friday high then 128.50. Support moves to 127.85 followed by 127.25 then 126.70.

Monday liquidity report showed Friday's excess liquidity rose to €1.314T up €13B from €1.301T prior. Use of the marginal lending facility fell to €103M from €188M prior.

Corporate issuance saw $13.9B come to market last week via 21 tranches, which slightly missed analyst estimates of between $15-20B.

In Euro denominated issuance €33.2B came to market largely comprised of SSA deals with the EFSF, UK and Spain accounting for over €15B of the weeks issuance. Tuesday saw the bulk of the volume with over €10B priced.

Looking Ahead

(CH) Swiss Parliament holds Spring Session in Bern

(UK) House of Lords holds detailed review of Article 50 Bill (through Mar 3rd)

(BE) Belgium Feb CPI M/M: No est v 0.7% prior; Y/Y: No est v 2.7% prior

(CL) Chile Jan PPI M/M: No est v 2.0% prior - 07:30 (CH) SNB's Zurbruegg speaks in Basel

08:00 (ES) Spain Debt Agency (Tesoro) announces size of upcoming auctions in week

08:15 (UK) Baltic Dry Bulk Index

08:30 (US) Jan Preliminary Durable Goods Orders: +1.7%e v -0.5% prior; Durables Ex Transportation: 0.5%e v 0.5% prior; Capital Goods Orders (Non-defense ex aircraft): 0.5%e v 0.7% prior, Capital Goods Shipments (Non-defense/ex- aircraft): 0.2%e v 1.0% prior; Durables Ex-defense: No est v 1.7% prior

08:50 (FR) France Debt Agency (AFT) to sell €5.4-6.6B in 3-month, 6-month and 12-month Bills

09:00 (MX) Mexico Jan Unemployment Rate (Seasonally Adjusted): 3.7%e v 3.7% prior; Unemployment Rate (Unadj): 3.8%e v 3.4% prior

09:00 (MX) Mexico Jan Trade Balance: -$2.6Be v $0.0B prior

09:00 (IL) Israel Central Bank (BOI) Interest Rate Decision: Expected to leave Base Rate unchanged at 0.10%

09:30 (EU) ECB announces Covered-Bond Purchases

09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

10:00 (US) Jan Pending Home Sales M/M: 1.0%e v 1.6% prior; Y/Y: No est v -2.0% prior

10:30 (US) Feb Dallas Fed Manufacturing Activity: 19.4e v 22.1 prior

11:30 (US) Treasury to sell 3-Month and 6-Month Bills

Forex Technical Analysis

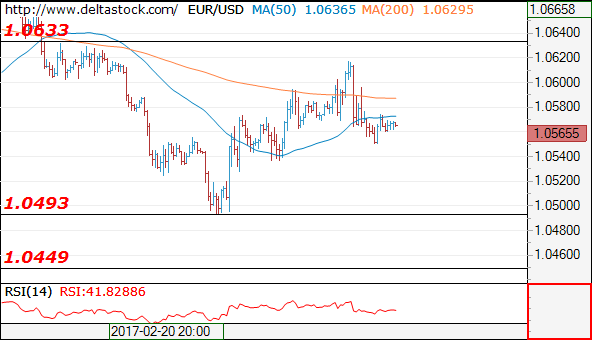

EUR/USD

Current level - 10565

My outlook is already bearish after the reversal at 1.0618, for a break through 1.0535 low, towards 1.0450 area.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.0600 | 1.0705 | 1.0535 | 1.0500 |

| 1.0630 | 1.0870 | 1.0450 | 1.0350 |

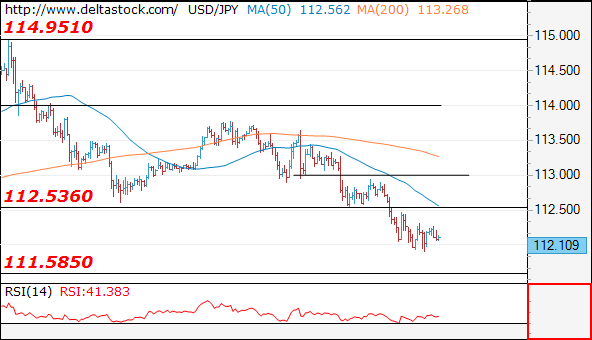

USD/JPY

Current level - 112.10

The downtrend remains intact, for a tight test of 111.60 support area. The latter should provide a reliable bas for an upswing towards 114.95 zone. Initial intraday resistance lies at 112.53.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 112.53 | 118.65 | 111.60 | 111.40 |

| 114.95 | 120.00 | 111.60 | 109.80 |

GBP/USD

Current level - 1.2425

My outlook here is bearish, for a break through 1.2380 support, towards 1.2240 area. Key resistance lies at 1.2505.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2505 | 1.2780 | 1.2380 | 1.2230 |

| 1.2570 | 1.2780 | 1.2240 | 1.1984 |

AUDUSD Remains Directionless, Rising 20SMA Supports For Now

The Aussie remains within short-term congestion, shaped in three consecutive weekly long-legged Dojis, unable so far to clearly break higher, despite repeated probes above pivotal 0.7700 barrier. However, overall bullish structure remains intact, with price action being supported by rising 20SMA (currently at 0.7659) that keep alive hopes of renewed attack at recent highs at 0.7730/39 and possible stretch toward target at 0.7776 (08 Nov high). The pair is awaiting Wednesday's release of Australian Q4 GDP data, which could boost the pair on release at/above forecasts. Meantime, extended consolidation is expected to hold above 20SMA and prevent deeper dips that would expose next strong support at 0.7600 higher base.

Res: 0.7687, 0.7700, 0.7739, 0.7758

Sup: 0.7659, 0.7624, 0.7600, 0.7575

USDJPY – Bears Tested Daily Cloud Base, 2017 Low In Focus

Strong bearish acceleration from 113.76 (21 Feb lower top) extended to 111.90 today and hit the base of rising daily cloud.

Strong bearish setup of daily studies pressures the pair for final push towards key short-term supports at 111.60 (06/09 Feb base/2017 lows) and 111.36 (weekly cloud top) in extension.

Near –term price action may show hesitation before firm break below daily cloud base (reinforced by rising 100SMA), with recovery attempts expected to remain below falling hourly cloud (spanned between 112.86 and 113.08).

Res: 112.59, 112.86, 113.08, 113.42

Sup: 111.90, 111.60, 111.36, 111.00

GBPUSD – Fresh Weakness Pressures 55/100SMA / Daily Cloud Top Pivots At 1.2400/1.2379

Pound extended last Friday's fall in Asian session today and cracked strong support at 1.2400 (converged 55/100SMA's), after Thursday's strong rally was capped by Fibo 61.8% barrier at 1.2567.

Fresh weakness came on renewed talks about Scotland's independence referendum, with investors also focusing on Tuesday's speech of US President Donald Trump for more clues about expected tax reform.

Near-term focus has turned lower again, with daily cloud top (1.2379) being under pressure.

Daily technical studies are returning to bearish setup that increases risk of further weakness.

Close below 55/100 SMA is seen as initial trigger for fresh extension lower, with break below next set of pivotal supports at 1.2379 (daily cloud top) and 1.2345 (weekly Tenkan-sen), needed to confirm bearish scenario.

Meantime, consolidation above 1.2400 handle should stay capped by daily Tenkan-sen at 1.2475, to keep negative sentiment in play.

Alternative scenario requires break and close above 1.2475 barrier for renewed attempts at upper breakpoints at 1.2567/80.

Res: 1.2433, 1.2457, 1.2475, 1.2500

Sup: 1.2400, 1.2379, 1.2345, 1.2300

EURUSD – Negative Tone To Persist While 55SMA Caps

The Euro is at the back foot in early Monday's trading and is holding around daily cloud base at 1.0557, following strong bearish acceleration and close below converged 10/55SMA's after last Friday's strong upside rejection.

Daily 55SMA (currently at 1.0587) marks strong barrier (10/55SMA bear cross is forming here) and capped the action in past five days.

Firm break below daily cloud base would generate stronger bearish signal, with completion of H&S pattern that is forming on hourly chart (neckline lies at 1.0545), needed to confirm resumption of fresh weakness from 1.0617 upside rejection (Friday's high) and look for return to 1.0492 (22 Feb low).

Bearishly aligned daily studies support scenario.

Conversely, break and close above 10/55SMA's would signal fresh strength and focus 20 SMA barrier at 1.0649.

Res: 1.0587, 1.0649, 1.0678, 1.0694

Sup: 1.0557, 1.0545, 1.0522, 1.0492

Sterling Tumbles on Brexit-Related Reports

The British pound tumbled during the Asian morning Monday, following media reports over the weekend regarding Brexit and immigration control, as well as the prospect of a second Scottish independence referendum. Firstly, according to the Telegraph, PM May is expected to announce that EU citizens who travel to Britain after the triggering of Article 50 in March will no longer have the automatic right to stay in the UK permanently. This is a significant development because prior to this, the UK was expected to keep the free movement of people principle intact until it exited the EU in roughly two years. In our view, the fact that PM May wants to take full control of Britain's borders as soon as when the exit negotiations begin, confirms that the government's top priority is immigration and not access to the single market, and enhances our view that we may be headed for a "hard Brexit". The other story over the weekend that may have weighed further on sterling was that the Scottish National Party raised the issue of a second Scottish independence referendum at a private meeting with May's administration last week. Although this prospect is not new, the report added that according to government sources May could agree to a new Scottish vote, but on condition it is held after the UK departs from the EU.

Coming on top of Q4 GDP data showing falling business investment and a BoE that appears to be in absolutely no rush to raise rates, these fresh signals of a "hard Brexit" and the risk of another Scottish referendum amplify our view that the broader outlook for GBP remains negative. What's more, given the uncertainty surrounding fiscal policy in the US, we would avoid exploiting GBP weakness through Cable. Instead, our favorite proxy for any potential sterling softness in the foreseeable future is still GBP/JPY, considering that the looming political risks in Eurozone could strengthen the yen due to its safe haven status.

GBP/JPY traded lower on Friday to break below the support (now turned into resistance) territory of 140.00 (R1) and the upside support line drawn from the low of the 16th of January. The rate slid further during the Asian morning Monday, before finding fresh buy orders marginally above the 138.90 (S1) area and subsequently rebounding somewhat. The fact that the rate has exited a triangle formation to the downside confirms that the short-term outlook of the pair is negative. As such, even though the latest rebound may continue for a while and perhaps test the 140.00 level (R1) as a resistance, we would expect the bears to take control again at some point and push the price lower for another test at 138.90 (S1). A clear break below that zone could set the stage for further declines towards the 138.50 (S2) territory.

Today's highlights

During the European day, the data calendar is very light. The only noteworthy indicator we get is Eurozone's final consumer confidence index for February.

In the US, durable goods orders for January are due to be released. The forecast is for the headline rate to have rebounded from previously, while the core figure is expected to have risen for the 5th consecutive month, indicating that despite some softness in civilian aircraft orders, the underlying trend in durable goods continues to be to the upside. The case for solid durable goods orders is supported by the nation's ISM manufacturing PMI for the month, where the new orders sub-index, already at an elevated level, rose for the 5th straight month. Something like that could bring USD under renewed buying interest.

EUR/USD traded lower on Friday, falling below the support (now turned into resistance) barrier of 1.0600 (R1). Given that the pair has resumed its downfall after testing as a resistance a short-term downtrend line taken from the highs of the 6th of February, we believe that the short-term bias remains negative. Strong US durable goods orders today could be the catalyst for further declines, perhaps for an initial test of our 1.0530 (S1) support level. Nevertheless, with not much else on the economic calendar today and with investors focus being on Trump's address (see below), we would expect any declines to stay more or less limited near the 1.0500 (S2) psychological barrier.

We have only one speaker scheduled for today: Dallas Fed President Robert Kaplan.

As for the rest of the week

On Tuesday, the highlight of the day will be US President Trump's address to a joint session of Congress. Following Trump's recent pledge that he is going to announce a "phenomenal" plan on tax reform within the next weeks, market participants will be on the edge of their seats for any details regarding the new administration's fiscal plans. As for the US data, we get the 2nd estimate of Q4 GDP.

On Wednesday the Bank of Canada rate decision will take center stage. The forecast is for the Bank to remain on hold. In such a case, market focus will quickly turn to the statement accompanying the decision for any forward guidance, as there is no press conference by Governor Poloz. Given the progress in economic data since the latest BoC meeting, the tone of the statement could remain neutral overall. As for the economic data, we get Australia's GDP for Q4, Germany's preliminary CPI for February, and the UK's manufacturing PMI for the same month. What's more, we get personal income and spending data for January from the US, as well as the core PCE price index for that month.

On Thursday, Eurozone's preliminary CPI for February and Canada's GDP data for Q4 are coming out.

On Friday, during the Asian morning, we get Japan's CPI figures for January. During the rest of the day, we get the UK services PMI for February, and from the US, the ISM non-manufacturing PMI for the same month.

EUR/USD Begins Week Below 1.06 Level

'At 1.06 versus the U.S. dollar, the euro is undervalued.' - Mark Haefele, UBS Wealth Management (based on Bloomberg)

Pair's Outlook

The common European currency started the week higher against the US Dollar than the Friday's closing price. With a new week the new levels of significance have been calculated, and the weekly PP at 1.0562 began to provide support to the currency exchange rate. As a result of the before mentioned facts, the currency pair began a surge. The Euro is set to surge up to the closest notable resistance level at 1.0591, which is represented by the 55-day SMA. The simple moving average is likely to hinder the pair's surge, if not even reverse it.

Traders' Sentiment

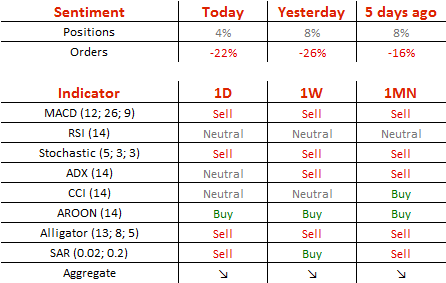

SWFX traders have decreased their bullish sentiment, as 52% of open positions are long on Monday, compared to 54% on Friday. Meanwhile, 61% of trader set up orders are set to sell the Euro.

GBP/USD Remains On The Back Foot

'The GBP slides this morning against all major currencies after the Times reports that UK Prime Minister Theresa May is preparing for Scotland to potentially call an independence referendum in March to coincide with triggering of Article 50. The referendum may be allowed but only after the UK leaves the EU.' – Nordea Markets (based on PoundSterlingLive)

Pair's Outlook

Friday ended with the Cable erased most of that week's gains, with the bearish momentum persisting through the weekend. The main gauge of such bearish developments were concerns over another possible Scottish independence referendum; Brexit turmoil keeps weighing on the Pound. The GBP/USD pair still faces a tough demand cluster around 1.24, which is expected to limit the losses as it has done through all of February so far. A close below 1.2380 could lead to the Sterling slumping back to 1.20, with political factors driving this weakness. However, a close above still brings hope for a potential recovery towards at least 1.27.

Traders' Sentiment

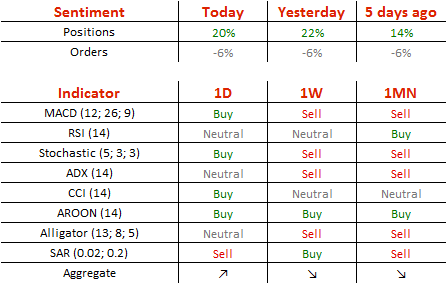

There are 60% of traders holding long positions today, while 53% of all pending orders are to sell the British Pound.

USD/JPY In Limbo Ahead Of Durable Goods Orders Data

'Our basic stance is that the correction in the USD/JPY will halt at ¥110-115, but we should be paying closer attention to downside risk at least for the short term.' – Deutsche Bank (based on FXStreet)

Pair's Outlook

The less favourable for the US Dollar scenario prevailed on Friday, causing the pair to edge lower once again. Nevertheless, the USD/JPY pair managed to retain its position above the 112.00 handle, which in turn is supported by the 100-day SMA, the lower Bollinger band and the weekly S1, while the 111.75 mark also acts as a tough psychological support. Consequently, another bearish development is unlikely, despite technical indicators suggesting so. The Greenback could easily reach the 113.00 level today, should the fundamentals provide a sufficient boost later during the day; however, disappointing data could still cause a downside reaction.

Traders' Sentiment

Market sentiment remains bullish, now at 61% (previously 54%). Meanwhile, the portion of buy orders edged down from 67 to 59%.