Sample Category Title

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2412; (P) 1.2490; (R1) 1.2534; More...

GBP/USD is still bounded in range of 1.2346/2705. Intraday bias remains neutral first and outlook is unchanged. Price actions from 1.1946 are viewed as a consolidation pattern, with rise from 1.1986 as the third leg. In case of another rise, we'd expect upside to be limited by 1.2774 to bring larger down trend resumption. On the downside, below 1.2346 will revive the case that such consolidation is completed at 1.2705 already. In that case, intraday bias will turn back to the downside for retesting 1.1946 low.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

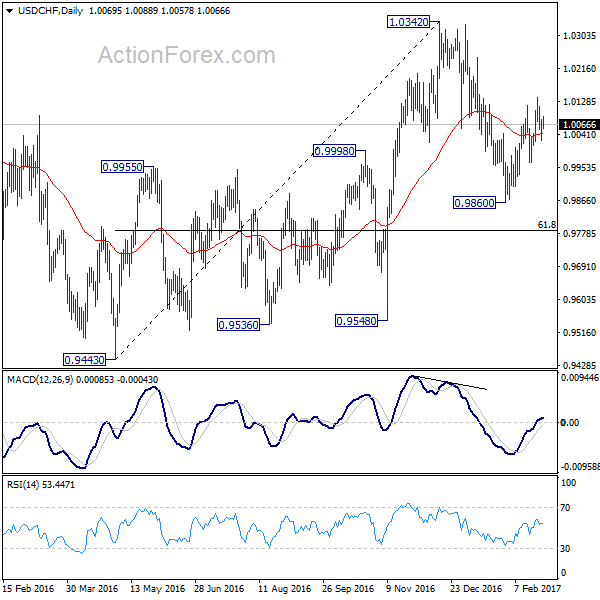

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 1.0038; (P) 1.0077; (R1) 1.0101; More.....

USD/CHF continues to consolidation below 1.0140 temporary top. Intraday bias remains neutral at this point. With 0.9966 support intact, further rise is in favor. Above 1.0140 will turn bias to the upside and target a test on 1.0342 resistance. Based on neutral medium term outlook, we'd be cautious on topping at around 1.0342. Meanwhile, break of 0.9966 will indicate completion of the rebound from 0.9860. And intraday bias will be turned back to the downside for 0.9860.

In the bigger picture, prior rejection from 1.0327 resistance argues that USD/CHF is staying in a medium term sideway pattern. In any case, decisive break of 1.0342 resistance is needed to confirm underlying strength. Otherwise, we'll stay neutral in the pair first. In case of another fall, we'd expect strong support from 0.9443/9548 support zone. Meanwhile firm break of 1.0342 will target 38.2% retracement of 1.8305 to 0.7065 at 1.1359.

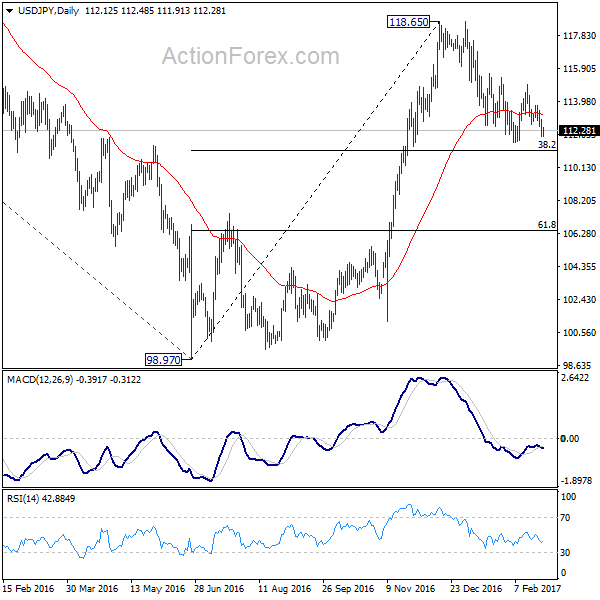

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.70; (P) 112.33; (R1) 112.72; More...

USD/JPY continues to stay in range of 111.58/114.94 and intraday bias remains neutral first. The corrective fall from 1118.65 could extend lower. But we'd still expect strong support from 38.2% retracement of 98.97 to 118.65 at 111.13 to contain downside and bring rebound. On the upside, above 114.94 resistance should confirm completion of pull back from 118.65. In such case, intraday bias will be turned back to the upside for retesting 118.65.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Rejection from 125.85 and below will extend the consolidation with another falling leg before up trend resumption.

Dollar Mixed as Markets Look Past Durable Orders

Dollar continues to trade mixed after weaker than expected data. Durable goods orders grew 1.8% in January, below expectation of 1.9%. Ex-transport orders dropped -0.2% versus expectation of 0.5% growth. Traders are staying cautious ahead of the highly anticipated address to Congress by US president Donald Trump tomorrow. Trump would likely provide details on dismantling the Affordable Care Act, or so-called Obamacare. However, market's attention will be on other economic related issues. That include the long-awaited tax reform that boosted stocks to new records highs. Traders started to reposition late last week as seen in the divergence in major indices. Also the greenback pull backed back following sharp fall in yields. The greenback could be vulnerable to selloff if Trump fails to live up to expectations again.

Separately, Fed Chair Janet Yellen and Vice Chair Stanley Fischer will be speaking on Friday on the economic outlook. The market has priced in higher chance of a rate hike in March with the OIS implied probabilities rising to 47.8% from 46.3% previously, following comments from Philadelphia Fed's Patrick Harker and Dallas Fed's Robert Kaplan, both appeared to support a March hike. Comments from Yellen and Fischer later this week should give more hints on Fed's normalization schedule.

Euro mildly higher as Macron closes gap with Le Pen

Euro strengthens mildly today on news that centrist French presidential candidate Emmanuel Macron opened up his lead over Republican Francois Fillon. Macron also managed to narrow the gap with rightist anti-Euro Marine Le Pen. Two polls published over the weekend showed that Macron has 25% support from French electorate going into April's election, just two points behind Le Pen. Overall, analysts maintained their view that no candidate can get majority vote in first round of election. And Macron is favorite to beat Le Pen in and one-on-one run-off in second round. However, as Le Pen's win would increase the risk of Frexit, Euro will remain sensitive to political news from France.

Eurozone confidence improved in January

Eurozone business climate rose to 0.82 in February, above expectation of 0.79. Economic confidence improved to 108.0 but missed expectation of 108.1. Industrial confidence rose to 1.3, above expectation of 1.0. Services confidence also rose to 13.8, above expectation of 13.3. Consumer confidence was finalized at -6.2. M3 money supply rose 4.9% yoy in January, slowed from 5.0% yoy. Lending to house holds grew 2.2% yoy, up from 2.0% yoy. Loans to businesses rose 2.3% yoy.

Sterling lower as Scotland worries resurface

Sterling is under broad based selling pressure today. Selloff in the Pound is seen as a reaction to news that Prime Minister May is preparing for Scotland to call for another independence referendum. And that would come as May triggers the Article 50 for Brexit negotiation with EU by the end of March. It's reported that May could agree to the vote on condition that it happens after completing the Brexit process.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 111.70; (P) 112.33; (R1) 112.72; More...

USD/JPY continues to stay in range of 111.58/114.94 and intraday bias remains neutral first. The corrective fall from 1118.65 could extend lower. But we'd still expect strong support from 38.2% retracement of 98.97 to 118.65 at 111.13 to contain downside and bring rebound. On the upside, above 114.94 resistance should confirm completion of pull back from 118.65. In such case, intraday bias will be turned back to the upside for retesting 118.65.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Rejection from 125.85 and below will extend the consolidation with another falling leg before up trend resumption.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Company Operating Profit Q/Q Q4 | 20.10% | 8.00% | 1.00% | 1.50% |

| 09:00 | EUR | Eurozone M3 Y/Y Jan | 4.90% | 4.80% | 5.00% | |

| 10:00 | EUR | Eurozone Business Climate Indicator Feb | 0.82 | 0.79 | 0.77 | 0.76 |

| 10:00 | EUR | Eurozone Economic Confidence Feb | 108 | 108.1 | 107.9 | |

| 10:00 | EUR | Eurozone Industrial Confidence Feb | 1.3 | 1 | 0.8 | |

| 10:00 | EUR | Eurozone Services Confidence Feb | 13.8 | 13.3 | 12.9 | 12.8 |

| 10:00 | EUR | Eurozone Consumer Confidence Feb F | -6.2 | -6.2 | -6.2 | |

| 13:30 | USD | Durable Goods Orders Jan P | 1.80% | 1.90% | -0.50% | -0.80% |

| 13:30 | USD | Durables Ex Transportation Jan P | -0.20% | 0.50% | 0.50% | -0.90% |

| 15:00 | USD | Pending Home Sales M/M Jan | 0.90% | 1.60% |

Canadian Dollar Unchanged as US Durables Mixed

USD/CAD is almost unchanged in the Monday session. Currently, the pair is trading slightly above the 1.31 line. On the release front, there are no Canadian releases. On the economic front, US Core Durable Goods Orders declined 0.2%, short of the estimate of +0.5%. However, Durable Goods Orders jumped 1.8%, beating the forecast of 1.6%. Later in the day, the US releases Pending Home Sales. On Tuesday, the US publishes Preliminary GDP and CB Consumer Confidence. As well, President Trump will address a joint session of Congress.

Canadian inflation levels jumped in January, led by CPI, which climbed 0.9%, well above the forecast of 0.3%. Higher gasoline prices and stronger crude prices boosted inflation. Still, the unexpected rise in inflation is unlikely to sway any opinions at the Bank of Canada, which is expected to hold rates at 0.50% at its policy meeting on Wednesday. Last year, the BoC adopted three new indicators to measure inflation, and these averaged 1.6% in January, below the central bank's inflation target of 2.0%. On Tuesday, Canada releases RMPI, which gauges inflation in the manufacturing sector.

US data was soft on Friday. Revised UoM Consumer Sentiment dropped to 96.3 in February, compared to 98.5 a month earlier. Still, this figure edged above the forecast of 96.1. On the housing sector, New Home Sales improved to 555 thousand in January, but this was well short of the forecast of 575 thousand. This follows Existing Home Sales, which jumped to 5.69 million, above the estimate of 5.55 million. On Monday, we'll get a look at Pending Home Sales, which is expected to dip to 1.1%.

President Trump's administration has a rough first month, beset by constant friction with the media and trouble filling in key cabinet positions. Trump will address Congress on Tuesday and the nation will be listening closely. Will we see the combative, outspoken Trump, or will he opt for a more conciliatory approach? In order to pass key legislation, Trump will have to make nice with lawmakers from both sides of the fence, and this speech would be an ideal time to offer a hand of cooperation rather than combat. The markets will be looking for some details about the administration's economic plan – if this is lacking, market sentiment could sour, dragging down the US dollar.

Yen Steady Ahead of Japanese Industrial Production, Retail Sales

USD/JPY has started the week with limited movement. Currently, USD/JPY is trading at 112.30. On the economic front, the US releases durable goods orders reports and Pending Home Sales. Japan will release Preliminary Industrial Production and Retail Sales. On Tuesday, the US releases Preliminary GDP and CB Consumer Confidence. As well, President Trump will address a joint session of Congress.

US data was soft on Friday. Revised UoM Consumer Sentiment dropped to 96.3 in February, compared to 98.5 a month earlier. Still, this figure edged above the forecast of 96.1. On the housing sector, New Home Sales improved to 555 thousand in January, but this was well short of the forecast of 575 thousand. This follows Existing Home Sales, which jumped to 5.69 million, above the estimate of 5.55 million. On Monday, we'll get a look at Pending Home Sales, which is expected to dip to 1.1%.

President Trump's administration has a rough first month, beset by constant friction with the media and trouble filling in key cabinet positions. Trump will address Congress on Tuesday and the nation will be listening closely. Will we see the combative, outspoken Trump, or will he opt for a more conciliatory approach? In order to pass key legislation, Trump will have to make nice with lawmakers from both sides of the fence, and this speech would be an ideal time to offer a hand of cooperation rather than combat. The markets will be looking for some details about the administration's economic plan – if this is lacking, market sentiment could sour, dragging down the US dollar.

With the Japanese yen hovering at low levels, imports have become pricier for Japanese consumers. Predictably, the response has been a drop in consumer spending. In its monthly economic report, the government lowered its assessment of consumer spending, the first downgrade in 11 months. Conversely, the weak yen has been a boom for exports, prompting the government to raise its assessment of exports for the first time in four months. The report did not change the overall assessment that the economy is recovering at a moderate clip. Japanese policymakers are concerned about the protectionist stance under President Donald Trump. Japanese Prime Minister Shinzu Abe met recently with Trump in Washington and defused a currency policy crisis. Still, Trump is unhappy with the trade balance between the two countries, so some turbulence could lie ahead in US-Japanese relations.

Dollar Crippled by Trumps Inaction

Monday February 27: Five things the markets are talking about

It's a nervy time for investors.

There are many factors that should be supporting riskier assets - improving economic outlooks in the U.S, Europe and China; U.S. corporate earnings and a gradual approach by the Fed to raise short-term interest rates and continued bond buying by the ECB and BoJ.

However, a lack of clarity on the timing and scope of promised pro-growth policies from Trumponomics, combined with uncertainty over whether the Fed will tighten rates at next months FOMC meeting has global equities losing momentum.

While in Europe, the Dutch parliamentary election on March 15 and the French first round presidential election on April 23 are also weighing on investor sentiment.

In the U.K, whispers of a second Scottish Referendum in the works in the weeks around Prime Minister Theresa May's triggering of the Brexit-inducing article 50 is battering GBP.

Note: The U.K. government is setting aside time for a Parliamentary battle to overturn changes May fears could be made to her draft Brexit law when it's debated in the House of Lords this week.

In the U.S, fixed income is parting ways with the stock market; the divergence is a warning signal that the Trump "reflation" trade is in trouble.

Despite all the markets negative undertones, all of this could change this week with President Trump's address to Congress Tuesday.

His speech will be scanned for guidance and insights on his proposed tax cuts and tax reform program, regulation, trade policy, and immigration.

1. Global equities see red

The rally in global equities that helped push their value above +$70T is losing momentum as investors grabble with political uncertainty and the Fed tightening timing.

In Japan, the Nikkei share average fell to 2-1/2 week low overnight as the yen strengthened (¥112.24) and as financial stocks dropped on lower U.S yields.

In China, blue chips posted their biggest single-day loss in two-months after the securities regulator vowed to step up their campaign against speculation and hinted about loosening its grip on new IPO's. The CSI300 index fell -0.8%, its sharpest drop since Dec. 23, while the Shanghai Composite Index also weakened -0.8%.

In Hong Kong, stocks fell for the third consecutive session, as the market's strong months-long rally showed signs of fatigue. The Hang Seng index dropped -0.2%, while the HK China Enterprises Index lost -0.8%.

In Europe, equity indices are trading mixed as the market await Trump's address to Congress on spending and tax plans tomorrow. Insurers are weighing down the FTSE 100 after the Chancellor amended the discount rate for Personal Insurance claims resulting in financial impacts on 2016 profits. However, the major banking stocks are providing support across the indices, while energy stocks are trading notably higher.

U.S equities are expected to open unchanged.

Indices: Stoxx50 +0.2% at 3,313, FTSE +0.2% at 7,260, DAX +0.1% at 11,819, CAC-40 -0.1% at 4,842, IBEX-35 +0.1% at 9,458, FTSE MIB +0.8% at 18,737, SMI -0.2% at 8,508, S&P 500 Futures flat

2. Oil prices confined to a tight range, gold up

Ahead of the U.S open, oil prices remain better bid, as the global supply glut appears to be easing, however, rising U.S production is expected to limit gains.

Brent crude oil has climbed +0.8% to +$56.44 per barrel, while U.S West Texas Intermediate (WTI) added +0.7% to +$54.35 a barrel.

Note: Oil prices tumbled on Friday after data from the EIA showed U.S. crude inventories rose for a seventh straight week. Domestic stocks rose +564k barrels to +518.7m last week.

The market has been supported within a tight +$4 - $5 range since November, when OPEC agreed to cut production. Currently, the IEA puts OPEC's average compliance at a record +90% in January for the six-month deal.

Gold prices are holding firm this Monday, trading atop of its four-month highs hit in the previous session (+$1,260.10) as investors await more clarity on President Trump's economic policy. The metal jumped +1.8% last week for its fourth straight weekly advanced.

Note: Hedge funds have raised their net 'long' position in COMEX gold to the highest in nearly three-months during the week to Feb. 21 - by +14,482 to 82,464 lots.

3. FI trading diverged from equities

Last week's February FOMC minutes appeared to pull forward hopes for the next rate hike, but the market is not yet behind a rate move in March.

Current futures prices seems to suggest that most believe the best bet could be May or more likely June rate hike - when the Fed is currently scheduled to hold a post-meeting press conference.

On Friday, U.S Treasury yields were further pressured by a decline in German bunds. Political concerns and talk of an ECB-induced short squeeze sent the German 2-year yield towards -1%, while the U.S benchmark 10-Year yield, which peaked at +2.43%, slid to a week close out of + 2.32%.

In France, 10-year bond yields hit a one-month low this morning (-2.5 bps to +0.90%), pushing other euro zone sovereign yields lower (Spanish, Italian and Portuguese yields all fell between -3 and -5 bps) as polls show centrist Macron would easily beat far-right candidate Le Pen in May's presidential election runoff.

In Germany, the Treasury department set a 0% coupon on the new March 2019 Schatz - all recent Schatz series carry a similar coupon to reflect the low yield environment. The 10-year bund trades atop its historic lows (-0.19%).

4. Dollar in consolidation mood

Ahead of the U.S open, the 'mighty' USD is consolidating its recent losses before President Trump's first major policy address to Congress on Tuesday. Trump is expected to include some details of his infrastructure spending and tax plans, but any lack of fresh direction would disappoint capital markets and weigh again on the USD.

The pound (£1.2412) is again starting the week on the back foot, pressured by reports that the Scottish government could possibly be seeking another independence referendum next year. Europe's single unit, the EUR (higher by +0.3% to trade at €1.0590), despite regionalist "populist" threats (Netherland and France) remains confined to its recent tight trading range.

Elsewhere, USD/JPY has moved off its two-week lows from Asia (¥111.98) and is trading atop minor resistance ¥112.25 just ahead of the N.Y open.

5. Eurozone confidence in line with expectations

Data this morning showed that Eurozone economic sentiment was in line with expectations in February. The headline print edged up to 108.0 from 107.9 and printed its highest level since March 2011.

Analysts note, that since consumer sentiment was "in-line" with the flash estimate, would suggest that business confidence rose significantly. This is consistent with the results of other recent surveys, which suggest the eurozone economy has gained some fresh momentum in Q1, despite heightened uncertainty about future policies ahead of a series of key elections across the currency region.

However, consumer inflation expectations were unchanged, despite the January jump in inflation, which supports ECB caution in the face of an otherwise encouraging data flow.

DAX – Under Pressure as Trump Speech Looms

The DAX Index has posted small losses in the Monday session. Currently, the DAX is trading at 11,909.50 points. On the release front, Eurozone Private Loans increased by 2.2%, above the estimate of 2.1%. M3 Money Supply edged lower to 4.9%, matching the forecast. On Tuesday, the US releases Preliminary GDP, with an estimate of 2.1%. As well, President Trump will address a joint session of Congress.

There was good news for the eurozone on Monday, as bank lending to eurozone households improved for a third straight month, rising to 2.2% in January. Lending has been moving upwards since 2015, but has only recently shown strong gains. This could be a sign that the ECB's stimulus program is finally bearing results. The central bank recently extended the QE program until December and is unlikely to end it earlier. Meanwhile, M3 Money Supply, which measures growth in the amount of money circulating in the eurozone, slowed to 4.8%, down from 5.0% a month earlier. This indicator is closely watched, as it often predicts economic activity.

In tandem with other stock markets, the DAX shrugged off the Federal Reserve's January minutes. There were no dramatic hints as to the timing of the next move by the Fed. The most important comment was that policymakers believe that a rate hike "fairly soon" could be appropriate in order to head off an overheated economy. The minutes indicated that Fed policymakers remain confident that the central bank will raise rates gradually, given the strong performance of the US economy. At the same time, the minutes noted uncertainty about President Trump's fiscal stimulus plan but little concern over the risk of inflation. So the million dollar question of when the Fed will press the rate trigger remains unanswered. Although pressure is slowly building towards a move by the Fed, there does not appear a sense of urgency to raise rates at the next meeting in March. According to the CME Group, the odds of a March hike are only at 17%, while the likelihood of a hike in either May or June stands above 40%.

President Trump's administration has endured a rough first month, beset by constant friction with the media and trouble filling in key cabinet positions. Trump will address Congress on Tuesday and the nation will be listening closely. Will we see the combative, outspoken Trump, or will he opt for a more conciliatory approach? In order to pass key legislation, Trump will have to make nice with lawmakers from both sides of the fence, and this speech would be an ideal time to offer a hand of cooperation rather than combat. The markets will be looking for some details about the administration's economic plan - if this is lacking, market sentiment could sour, dragging down the US dollar.

Key Week For Donald Trump And Risk Rally

News and Events:

Ahead of key week for Donald Trump

Donald Trump is about to give the most important speech - at least for financial markets - since taking office. Indeed, investors are impatiently waiting for the President to finally explain his plan regarding fiscal spending and tax cuts. Equities across the globe have been rallying strong during the past few weeks, with US indices breaking record levels day after day. The next couple of days will therefore prove a veritable landmine for investors. On one hand, the market’s expectations are very high, however also high is the probability that Trump will strongly disappoint. On the other hand, investors will not hesitate to reload long positions should Trump delivers some bold measures.

Equities are going both ways at the start of the week as investors do not know which way the wind is going to blow. Asian regional markets were broadly trading in negative territory with the Nikkei down 0.91% while in mainland China the CSI 300 was down 0.89%. Across the Atlantic, European equities started the week on a firmer footing with the Euro Stoxx 50 rising 0.30%. Despite this reassuring picture, volatility is on the rise since Friday, suggesting that investors are getting nervous. In the FX markets, most currency pairs were trading sideways this morning.

Divergence in political risk

As Europe hurdles towards the Dutch elections on 15th March, the significance of politics to Eurozone outlook is materialising. EUR has failed to positively react to news of the French political alliance, which suggests a reduction in the probability of a presidential win for Le Pen, despite a narrowing of French vs. German sovereign yields. Lack of volatility indicates that risk aversion has increased as traders brace for a barrage of destabilizing events. We continue to search for opportunity to short the European political landscape and view short EURGBP as the clearest trade. We suspect that European political uncertainty is not merely comprised of singular events, but rather rolling negative sentiment which sees Europe paralysed by breakup fears. This fact will weigh on EUR even should results predict a positive outcome. In the US, the market has become more sensitive to positive economic surprises. Recent Q4 data has indicated strong momentum, despite weakness in consumption and fixed investment, while inflationary pressures continue to build. Manufacturing PMI is expected to increase to 56.4 from 55.9 while Service sentiment will also improve to 55.3 from 54.5. This week, the Notification Withdrawal Bill is expected to be delivered to the committee stage, potentially reducing uncertainty. EURGBP recovery bounce to 0.8535 (capped by 50d MA) should provide opportunity to reload short targeting of 0.8402 support (then 0.8305).

SNB’s intervention accelerates

Upside pressures on the Franc are very important. One euro can be exchanged for around 1.06 franc and the trend shows the euro keeps on weakening. This morning the total sights deposits showed a CHF 4.7 billion increase for last week to CHF 548.2 billion. The pace of the deposits’ growth has rarely been so high.

It is clear for us that the SNB is intervening. The European political uncertainties along with the European mixed economy are pushing the franc higher. One thing needs to be said, the Swiss economy resists well to those pressures. This Wednesday, the Manufacturing PMI is set to increase and on Thursday, the GDP will be released. Financial markets expects a growth increase of 0.4% q/q for the last quarter of 2016.

Those figures are showing that current levels of the Franc are nor hurting that much the Swiss economy. There is nonetheless once concern, the SNB FX reserves are now invested in foreign assets and in particular into US equities. The US rally is providing some unrealized gains to the SNB but the correlation towards the US economy may be dangerous at some point. Equity markets have been told to be undervalued.

The Risk Today:

EURUSD is trading sideways within a fifty-pip range below 1.0600. Hourly resistance is given at 1.0679 (16/02/2017 high) while hourly support can be found at 1.0521 (15/02/2017 low). The technical structure suggests deeper consolidation. In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

GBPUSD is trading sideways within a fifty-pip range below 1.0600. Hourly resistance is given at 1.0679 (16/02/2017 high) while hourly support can be found at 1.0521 (15/02/2017 low). The technical structure suggests deeper consolidation. In the longer term, the death cross late October indicated a further bearish bias. The pair has broken key support given at 1.0458 (16/03/2015 low). Key resistance holds at 1.1714 (24/08/2015 high). Expected to head towards parity.

USD/JPY's demand is fading after its increase from support given at 111.36 (28/11/2016 low). Bearish pressures arise around hourly resistance given at 115.62 (19/01/2016 high). The technical structure suggests further weakness around former resistance given at 112.57 (17/01/2017 low). We favor a long-term bearish bias. Support is now given at 96.57 (10/08/2013 low). A gradual rise towards the major resistance at 135.15 (01/02/2002 high) seems absolutely unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

USD/CHF's short-term momentum is definitely bullish. The pair lies within an uptrend channel. Hourly resistance is implied by upper bound of the uptrend channel. Key resistance is given at a distance at 1.0344 (15/12/2016 high). Expected to see further strengthening. In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

| EURUSD | GBPUSD | USDCHF | USDJPY |

| 1.1300 | 1.3445 | 1.1731 | 121.69 |

| 1.0954 | 1.3121 | 1.0652 | 118.66 |

| 1.0874 | 1.2771 | 1.0344 | 115.62 |

| 1.0590 | 1.2536 | 1.0052 | 112.48 |

| 1.0454 | 1.2254 | 0.9967 | 111.36 |

| 1.0341 | 1.1986 | 0.9862 | 106.04 |

| 1.0000 | 1.1841 | 0.9550 | 101.20 |

EUR/USD – Euro Edges Higher, Markets Eyes US Durables

EUR/USD has posted slight gains in the Monday session. Currently, the pair is trading at 1.0580. On the release front, Private Loans increased by 2.2%, above the estimate of 2.1%. M3 Money Supply edged lower to 4.9%, matching the forecast. The US starts off the week with durable goods orders reports and Pending Home Sales. On Tuesday, the US releases Preliminary GDP and CB Consumer Confidence. As well, President Trump will address a joint session of Congress.

There was good news for the eurozone on Monday, as bank lending to eurozone households improved for a third straight month, rising to 2.2% in January. Lending has been moving upwards since 2015, but has only recently shown strong gains. This could be a sign that the ECB’s stimulus program is finally bearing results. The central bank recently extended the QE program until December and is unlikely to end it earlier. Meanwhile, M3 Money Supply, which measures growth in the amount of money circulating in the eurozone, slowed to 4.8%, down from 5.0% a month earlier. This indicator is closely watched, as it often predicts economic activity.

US data was soft on Friday. Revised UoM Consumer Sentiment dropped to 96.3 in February, compared to 98.5 a month earlier. Still, this figure edged above the forecast of 96.1. On the housing sector, New Home Sales improved to 555 thousand in January, but this was well short of the forecast of 575 thousand. This follows Existing Home Sales, which jumped to 5.69 million, above the estimate of 5.55 million. On Monday, we’ll get a look at Pending Home Sales, which is expected to dip to 1.1%.

President Trump’s administration has a rough first month, beset by constant friction with the media and trouble filling in key cabinet positions. Trump will address Congress on Tuesday and the nation will be listening closely. Will we see the combative, outspoken Trump, or will he opt for a more conciliatory approach? In order to pass key legislation, Trump will have to make nice with lawmakers from both sides of the fence, and this speech would be an ideal time to offer a hand of cooperation rather than combat. The markets will be looking for some details about the administration’s economic plan – if this is lacking, market sentiment could sour, dragging down the US dollar.