Sample Category Title

GBP/JPY Long: Same Level, Take 2

A couple of weeks ago, we were looking for a possible GBP/JPY counter-trend long. The Beast was sitting at a horizontal support/resistance zone and if it had have held then we were looking for that first intraday pullback to get long off of. But alas the level didn’t hold and price dropped lower through it.

Three weeks later and price is back at the zone again and the setup has some real promise.

GBP/JPY 4 Hourly:

That looks like a textbook trend line breakout which if you keep reading, would mean a possible entry short on a re-test. But how often do we see the textbook setups like this fail miserably. Nothing in forex trading is textbook! If it is written in a textbook then the smart money will so often do the opposite otherwise everyone would make money.

Ah this trading game is a strange one, I know!

GBP/JPY 15 Minute:

So now zooming into an intraday chart, with that 4 hour horizontal support/resistance zone looking like it’s holding for now, the play might actually be to look to get long.

Your options are to aggressively get long on this current pullback if you think that the support zone has held, or you can wait and see if it properly breaks higher and then buy the first true pullback once you have that confirmation.

Markets Subdued as Momentum against Trump’s Immigration Ban Grows

Following last week when the Dow Jones, NASDAQ and S&P 500 all reached record highs, with this positivity having a similar impact on both the Asian and European markets; there is now an air of caution throughout the financial markets as the new trading week gets underway. It is very possible that the reason for this caution, and the European markets slipping lower is due to investors digesting those record moves seen in the US last week. There is also no denying that the turmoil caused by the Trump administration banning certain nationals from entering the United States, which has caused anger worldwide, could be linked to the subdued atmosphere.

While investors were very quick to price in the expected impact that deregulation, infrastructure spending and job growth could have on the US economy, I find it very difficult to believe that after pricing in heavy premiums based on fiscal promises, that investors are not now reconsidering what damage Trump might do by implementing other promises that supplemented an incoherent and ranting political campaign. Whether it is building a wall, banning certain nationalities, starting a trade war or pretty much anything else President Trump may do to upset people, it does risk both creating and deepening a negative perception of the US.

What if someone now reacts by banning US products, or even worse US nationals from entering their nations? What if investors now decide to take money out of US funds? Over one million Britons have already reacted by signing a petition to stop an upcoming visit from Trump to the United Kingdom, something that will put even more pressure on Theresa May as she has not only just concluded a meeting with the new President but is already under pressure to meet her own deadline to invoke Article 50 within the next two months. Although it is expected and understood that the UK will be aiming to strengthen relationships around the world following the result of the EU Referendum, I am unsure how people will react to Theresa May strengthening a relationship with the United States that appears on track to isolate itself from globalisation.

GBPUSD at risk to falling below 1.25

The GBPUSD is at risk to declining for the third successive day as investors continue to take profit after the pair reached a 6-week high marginally below 1.27 last week. Investors are still reluctant to consider longer-term buying positions on the British Pound with the continuous uncertainty around Article 50 being invoked around the corner. It will likely require another round of unwinding on USD positions or for the date to be delayed for the invoking of Article 50 to send the Pound back to the higher 1.20's.

EURUSD continues to meet sellers

The Eurodollar is continuing to face near-term downside pressure, with the currency pair dipping back to 1.06 after opening and climbing above 1.07 as investors digested the news around the United States over the weekend. Generally speaking the USD is still trading higher against most of its major trading partners including the British Pound, Euro, Swiss Franc, Australia and New Zealand Dollar, as well as the Canadian Dollar. As long as the Dollar does not fall victim to a round of selling, the near-term pressure on the Euro should persist as the Eurodollar gradually reverses after from its gains since earlier in January.

Dollar slipping against emerging currencies

Despite the Dollar trading higher against most of the G-8 currencies, the USD has slipped lower against a host of emerging market currencies. The Turkish Lira, Mexican Peso, Thai Baht, Indian Rupee, Indonesian Rupiah and Philippine Peso have all strengthened at the start of the week. This is likely not due to the protests taking place throughout the United States, but instead linked to the overwhelming consensus that US interest rates will be left unchanged later this week. With that being said the news headlines are being completely dominated by politics.

Turkish Lira rebounds by 1.4%

This is likely just a small recovering following what has been a brutal couple of months for the Turkish Lira, but the currency has is the major market mover today with the USDTRY declining by over 1.4%. Despite what looks on headline as a significant move, Turkey is still plagued by a multitude of different social/economic and even political problems that makes it difficult to believe that the Lira will be able to recover much lost ground.

U.S. Consumer Did Not Disappoint in December

Personal income rose 0.3% in December, in line with consensus. Removing inflation and taxes, real disposable income rose 0.1% on the month.

Americans were clearly in a spending mood to end 2016, with consumption up 0.5%, also as expected. That marked an acceleration from the previous two months.

In real terms spending rose a decent 0.3%, following a 0.1% gain in November. Spending gains were concentrated on durable goods, which jumped 1,.4% on the month. Services spending was solid at 0.3% for the second consecutive month.

The combination of higher spending and more modest income gains saw the savings rate decline further to 5.4%. The personal saving rate trended down over the course of 2016, after creeping up through 2015.

Inflation, as measured by the year-on-year change in the personal consumption deflator, ticked up to 1.6%, from 1.4% in November. Core PCE inflation (ex food & energy) held steady at 1.7%, roughly where it has been for most of 2016.

Key Implications

Today's solid report provides a nice handoff for consumer spending growth heading into 2017. U.S. consumers drove growth in the fourth quarter, and we expect that momentum to be sustained in in the first quarter of 2017.

Consumers have been working down their savings buffers accumulated since the fall in energy prices, but the saving rate is not unduly low. We expect income growth to pick up in the months ahead reflecting robust wage and employment gains, providing a solid foundation for consumer spending.

Later this week we will hear from the FOMC. While the Fed does expect that a hotter economy will lift core price pressures in the coming months, so far in 2016 core inflation has remained fairly steady. That should enable the Fed to wait patiently on the sidelines until the second quarter, before taking rates another step higher.

US Consumer Spending up in December

- US nominal personal consumer expenditures (PCE) rose an expected 0.5% in December following a 0.2% increase in November and 0.4% October gain. Spending was up 0.3% on a volumes basis.

As-expected, overall December spending was boosted by a 2.8% increase in motor vehicle sales (consistent with the earlier-reported 3% increase in December unit vehicle sales) that contributed to a 1.4% gain in spending on durable goods. Spending on services also posted a solid 0.4% gain, although driven by a weather-related 12.2% monthly rebound in spending on electricity & gas that retraced most of a 13.5% decline over the previous three months (temperatures were closer to normal in December after a warmer-than-usual start to the winter, on balance). Spending on nondurable goods inched up 0.2%, though solely the result of higher prices with the volume of spending on non-durables unchanged.

Personal incomes continued to grow, rising 0.3% in December following a 0.1% gain in November and 0.5% jump in October. With monthly spending nonetheless outpacing monthly income growth, the saving rate inched lower to 5.4% from 5.6% in November and 6.1% a year ago.

Annual growth in the PCE deflator moved up to 1.6% from 1.4% in November as energy prices moved higher. The core PCE deflator held steady at 1.7% year-over-year, unchanged from November.

Our Take:

Today's consumer spending numbers provide the monthly pattern behind the solid 2.5% increase in real spending in the advance Q4/16 GDP report. The strong finish to the end of the quarter (real spending in December was an annualized 1.1% above its Q4 average) bodes well for another strong gain in Q1/17. We expect household spending will remain a support to economic activity going forward reflecting strong labour markets, rising consumer confidence, and low interest rates. Although still early, data-to-date (including strong household spending, a pickup in business equipment shipments, and a bounce-back in December exports) point to solid underlying momentum in the economy. We expect overall GDP to increase at an above-trend 2.3% rate in Q1/17 to build on a 1.9% Q4 gain and 3.5% jump in Q3. Although much uncertainty remains about the future of U.S. government policy under the new Trump administration, we expect underlying economic improvement is strong enough to warrant higher interest rates and look for the Fed to implement two additional 25 basis point hikes to the fed funds target range this year.

Canadian Dollar Edges Lower, US Housing Report Next

USD/CAD has edged higher at the start of the trading week. In the Monday session, the pair is trading at 1.3150. On the release front, there are no Canadian events on the schedule. In the US, the key event of the day is Pending Home Sales, which is expected to rebound with a gain of 1.6%. On Tuesday, Canada will release GDP, with an estimate of 0.3%. The US will publish CB Consumer Confidence, with the markets expecting a strong reading of 112.6 points.

Canada will release the November GDP report on Tuesday. In October, GDP was unexpectedly low, missing the estimate of a 0.1% gain. This marked the first decline since May and has raised concerns that economic growth in the fourth quarter will be weak. If GDP again misses expectations, we could see the Canadian dollar lose ground, and the BoC will be under increased pressure to lower interest rates. Last week, Earlier in January, the bank held rates at 0.50% but expressed concerns of economic turbulence due to Donald Trump's protectionist stance, which could have significant repercussions for the Canadian economy.

The markets had predicted that US economic growth would soften in the fourth quarter, and Advance GDP fell short of the estimate. The economy expanded 1.9%, shy of the estimate of 2.1%. Business investment and consumer spending remains solid and should continue into 2017. However, Trump's protectionist rhetoric and action, which saw tensions escalate with Mexico last week, could cloud the bright picture for the US economy.

Donald Trump has barely warmed the president's chair in the Oval House, but has already signed a host of controversial executive orders which have been condemned both domestically and abroad. Trump has withdrawn from the Trans-Pacific Partnership and declared he will reopen the NAFTA trade agreement with Canada and Mexico. He has also ordered work to begin on a wall with Mexico and banned immigrants from seven Moslem countries. Trump's unconventional and disjointed approach to international politics and trade could have major ramifications on global trade and could lead to financial instability in global markets, triggering volatility in the currency markets. Just a few days before being sworn in as president, Trump stated that the US dollar was "too strong", blaming a weak Chinese currency. Predictably, the greenback lost ground after Trump's remarks. It's a safe bet that Trump's offhand tweets and comments will continue to fuel market movement.

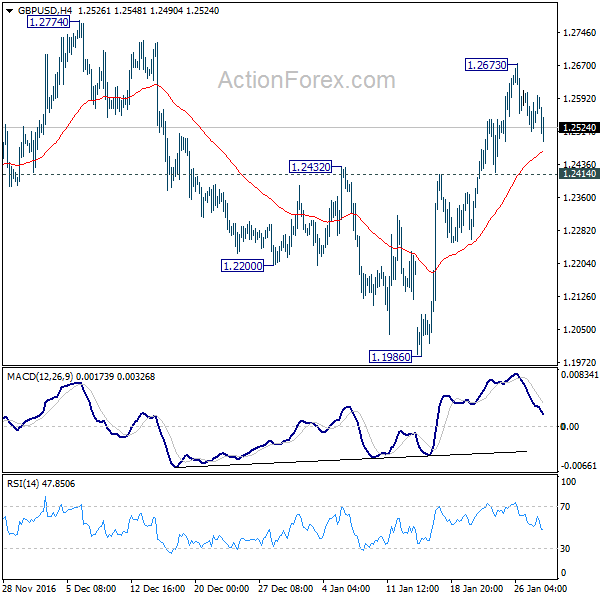

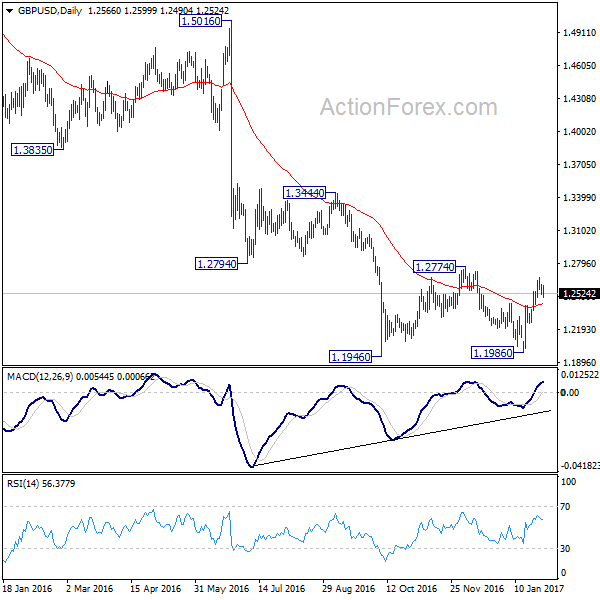

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2506; (P) 1.2555; (R1) 1.2596; More...

GBP/USD's fall from 1.2673 extends but it stays above 1.2414 minor support so far. Intraday bias remains neutral first. Rise from 1.1986 is seen as the third leg of the consolidation pattern from 1.1946. Break of 1.2414 minor support will argue that it's completed and turn bias to the downside for 1.1946 low. In case of another rise, we'd expect strong resistance at 1.2774 to limit upside and bring down trend resumption eventually.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Subscribe to our daily and mid-day newsletter to get this report delivered to your mail box

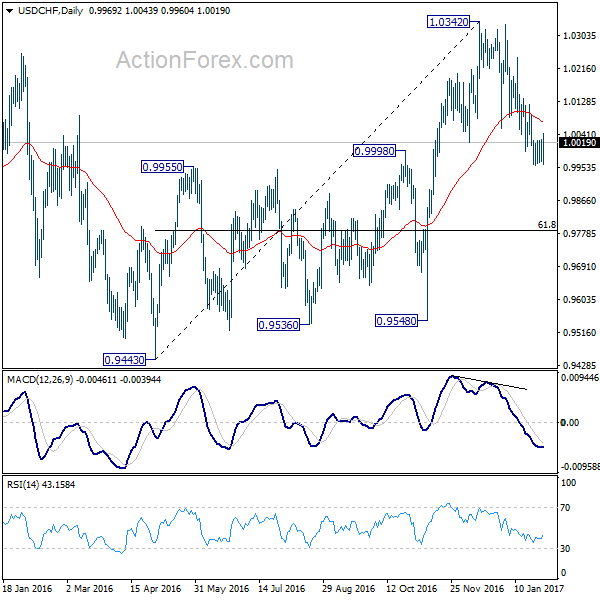

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9963; (P) 0.9995; (R1) 1.0021; More.....

USD/CHF recovers today but stays in tight range above 0.9958. With 1.0121 minor resistance intact, deeper fall is still in favor. Decline from 1.0342 is seen as the third leg of the pattern from 1.0327. Below 0.9958 will target 61.8% retracement of 0.9443 to 1.0342 at 0.9786 and below. Nonetheless, break of 1.0121 will indicate near term reversal and turn focus back to 1.0342.

In the bigger picture, rejection from 1.0327 resistance suggests that consolidation pattern from there is still in progress. Fall from 1.0342 is seen as the third leg and retest of 0.9443/9548 support zone could be seen. But we'd expect strong support from there to contain downside. At this point, we're still expecting the larger rally to resume later to 38.2% retracement of 1.8305 to 0.7065 at 1.1359.

Subscribe to our daily and mid-day newsletter to get this report delivered to your mail box

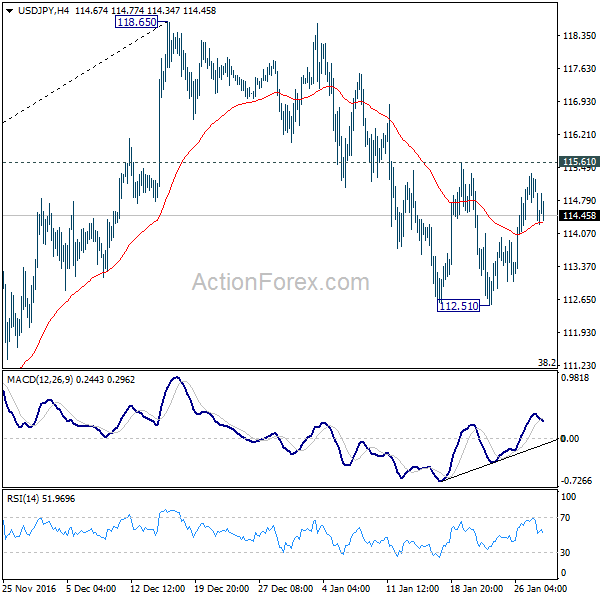

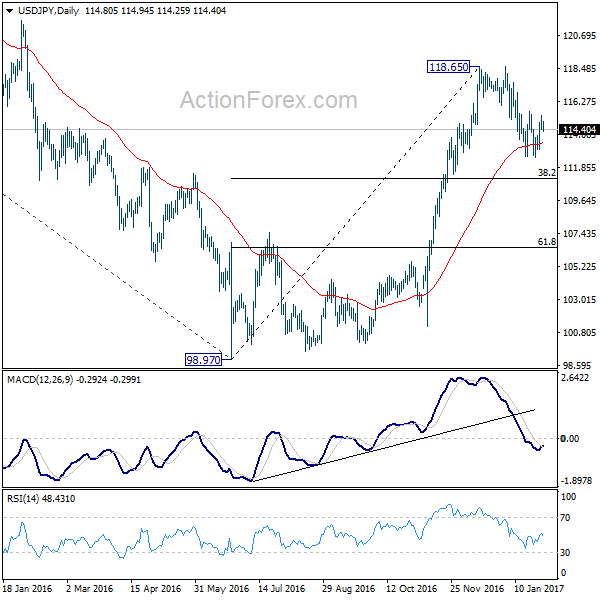

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 114.50; (P) 114.94; (R1) 115.48; More...

USD/JPY is still bounded in range of 112.51/115.61 and intraday bias remains neutral. The choppy decline from 118.65 is seen as a correction. Break of 115.61 resistance will suggest that the correction is finished and turn bias to the upside for 118.65. Break will resume whole rise from 98.97 and target 125.85 key resistance. On the downside, below 112.51 will extend such decline but downside should be contained by 38.2% retracement of 98.97 to 118.65 at 111.13 and bring rebound.

In the bigger picture, price actions from 125.85 high are seen as a corrective pattern. The impulsive structure of the rise from 98.97 suggests that the correction is completed and larger up trend is resuming. Decisive break of 125.85 will confirm and target 61.8% projection of 75.56 to 125.85 from 98.97 at 130.04 and then 135.20 long term resistance. Rejection from 125.85 and below will extend the consolidation with another falling leg before up trend resumption.

Subscribe to our daily and mid-day newsletter to get this report delivered to your mail box

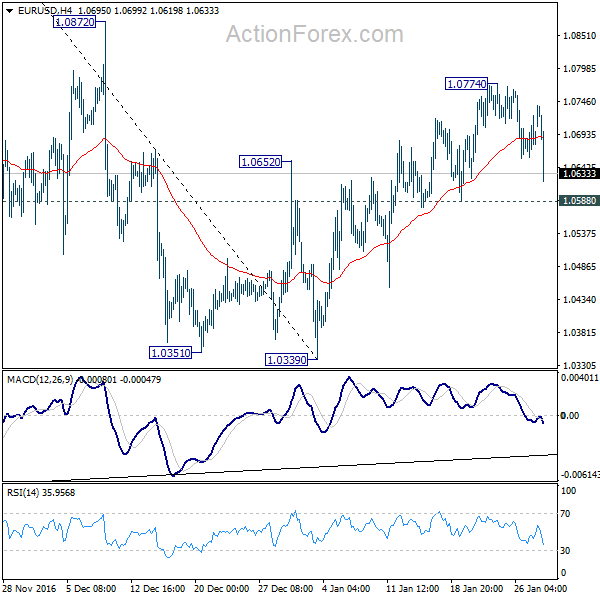

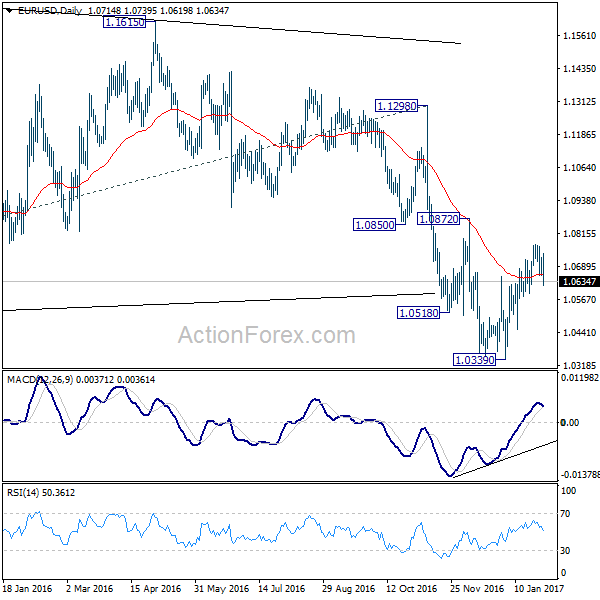

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0660; (P) 1.0693 (R1) 1.0727; More.....

EUR/USD dips notably in early US session but stays above 1.0588 minor support so far. Intraday bias remains neutral at this point. Price actions from 1.0339 are seen as a corrective move. Break of 1.0588 will indicate that such rise is completed and turn bias to the downside for retesting 1.0339 low. In case of extension, upside should be limited by 1.0872 resistance.

In the bigger picture, whole down trend from 1.6039 (2008 high) is in progress. Such down trend is expected to extend to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. On the upside, break of 1.1298 resistance is needed to confirm medium term bottoming. Otherwise, outlook will stay bearish in case of rebound.

Subscribe to our daily and mid-day newsletter to get this report delivered to your mail box

Dollar Reversed Earlier Loss, BoJ Watched in Upcoming Asian Session

Dollar reversed earlier loss and trades higher in early US session. Traders are turning their eyes from the unrests and protests regarding US president Donald Trump's immigration ban executive orders. Instead the focuses are back on economic data and the anticipate of FOMC announcement later in the week. Released from US, personal income rose 0.3% in December while spending rose 0.5%. Headline PCE rose 0.2% mom, 1.6% yoy. Core PCE rose 0.1% mom, 1.7% yoy. In particular, the upward movement in core PCE should affirm the case for Fed to continue policy accommodation later this year.

ECB governing council member Ewald Nowotny said together that the central bank will have "better information" for making a decision about the end of the asset purchase program "in summer". There has been talk of stimulus exit recently. In particular, executive board member Sabine Lautenschlaeger said last week that she was "optimistic that we can soon turn to the question of an exit" and ECB must "get ready for better times."

Released from Eurozone, business climate dropped to 0.77 in January. Economic confidence rose to 108.2. Industrial confidence rose to 0.8. Services confidence rose to 13.5. Consumer confidence was finalized at -4.7. German CPI dropped -0.6% mom, rose 1.9% yoy in January, below expectation of -0.5% mom, 2.0% yoy. Also from Europe, Swiss KOF leading indicator dropped to 101.7 in January.

BoJ rate decision will be the main focus in upcoming Asian session. The central bank is expected to keep interest rate unchanged. It announced to increase purchases of 5-10 years bonds to JPY 450b, from JPY 410b previously, last week, under the yield curve control framework. Released earlier today, Japan retail sales rose 0.6% yoy in December, below expectation of 1.6% yoy. New Zealand trade deficit narrowed to NZD -41m in December.

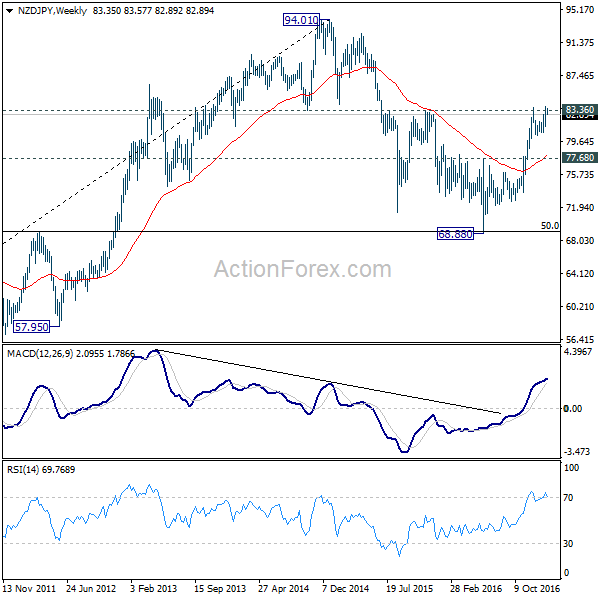

NZD/JPY faced some resistance from 83.36 in December in pulled back. The correction was held well above medium term support level at 77.68 and thus maintaining bullishness. The cross is indeed back pressing 83.36 resistance now. Overall, the correction from 94.01 (2014 high) was completed last year at 68.88. Rise from here is a medium term move at the same degree as the fall fro 94.01. Thus, sustained trading above 83.36 will target 94.01 high. We'll stay medium term bullish in the cross as long as 77.68 holds.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0660; (P) 1.0693 (R1) 1.0727; More.....

EUR/USD dips notably in early US session but stays above 1.0588 minor support so far. Intraday bias remains neutral at this point. Price actions from 1.0339 are seen as a corrective move. Break of 1.0588 will indicate that such rise is completed and turn bias to the downside for retesting 1.0339 low. In case of extension, upside should be limited by 1.0872 resistance.

In the bigger picture, whole down trend from 1.6039 (2008 high) is in progress. Such down trend is expected to extend to 61.8% projection of 1.3993 to 1.0461 from 1.1298 at 0.9115. On the upside, break of 1.1298 resistance is needed to confirm medium term bottoming. Otherwise, outlook will stay bearish in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Consensus | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Dec | -41M | -95M | -705M | -746M |

| 23:50 | JPY | Retail Trade Y/Y Dec | 0.60% | 1.60% | 1.70% | |

| 8:00 | CHF | KOF Leading Indicator Jan | 102.9 | 102.2 | ||

| 10:00 | EUR | Eurozone Business Climate Indicator Jan | 0.8 | 0.79 | ||

| 10:00 | EUR | Eurozone Economic Confidence Jan | 107.8 | 107.8 | ||

| 10:00 | EUR | Eurozone Industrial Confidence Jan | 0.2 | 0.1 | ||

| 10:00 | EUR | Eurozone Services Confidence Jan | 12.7 | 12.9 | ||

| 10:00 | EUR | Eurozone Consumer Confidence Jan F | -4.9 | -4.9 | ||

| 13:00 | EUR | German CPI M/M Jan P | -0.50% | 0.70% | ||

| 13:00 | EUR | German CPI Y/Y Jan P | 2.00% | 1.70% | ||

| 13:30 | USD | Personal Income Dec | 0.40% | 0.00% | ||

| 13:30 | USD | Personal Spending Dec | 0.50% | 0.20% | ||

| 13:30 | USD | PCE Deflator M/M Dec | 0.20% | 0.00% | ||

| 13:30 | USD | PCE Deflator Y/Y Dec | 1.70% | 1.40% | ||

| 13:30 | USD | PCE Core M/M Dec | 0.10% | 0.00% | ||

| 13:30 | USD | PCE Core Y/Y Dec | 1.70% | 1.60% | ||

| 15:00 | USD | Pending Home Sales M/M Dec | 1.10% | -2.50% |

Subscribe to our daily and mid-day newsletter to get this report delivered to your mail box