Sample Category Title

US GDP Update Came in Slightly Softer Than Expected

European and US markets nosedived yesterday on the back of ‘good news is bad news’ and the futures hint at a bearish start to Thursday’s session.

First, Spain, France and Germany revealed better-than-expected growth numbers in Q3. Germany even eked out an unexpectedly positive figure, which certainly helped – I wouldn’t say ‘to improve’ the mood but – to prevent sentiment from getting worse in the midst of a jungle of bad economic news, there. VW posted its least profitable quarter since the pandemic but said that they could avoid factory closures IF the workers accepted a 10% decrease to their salaries and the German unemployment change came in almost double the expectations, but seeing the German economy eke out that 0.2% advance in Q3 was a good surprise.

Now, the encouraging GDP figures came in with a cost: inflation in Spain and Germany came in higher than expected. Inflation in Germany crossed past the European Central Bank’s (ECB) 2% target and reached 2.4% in October.

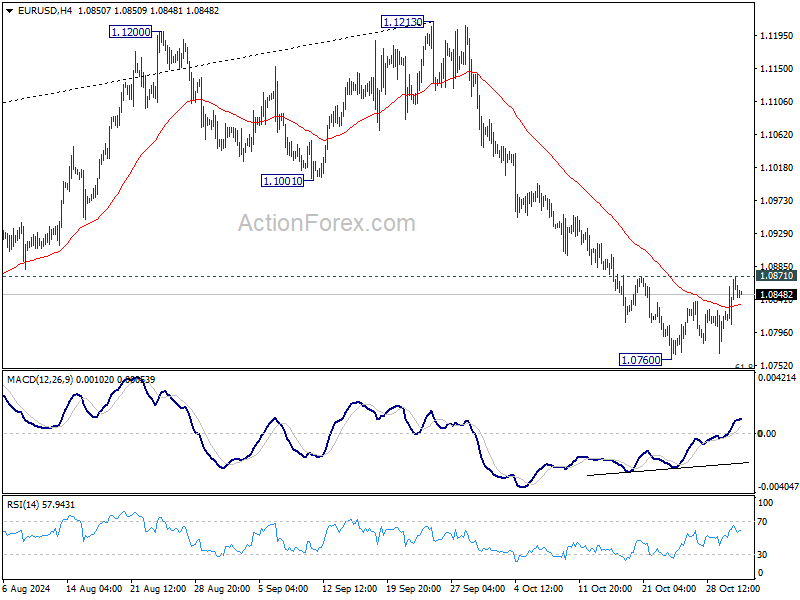

The aggregate CPI update for Eurozone, due this morning, is expected to brush up against the 2% target. The combination of better-than-expected growth and higher-than-expected inflation weighs on accelerated rate cut expectations from the ECB. And the latter is positive for the euro. This is why the EURUSD tested the 1.0870 resistance, which matches the minor 23.6% Fibonacci retracement on the September to October selloff and the 200-DMA, but couldn’t clear it.

And the reason why it couldn’t clear it is because mixed data came in from the US. There, the GDP update came in slightly softer than expected, at 2.8% versus 3% printed previously, but consumer spending jumped from 2.8% to 3.7% defying the rising credit card debt and delinquencies, and more importantly, PCE prices fell to 1.5%, and core PCE prices fell less than expected but printed 2.20% - which now is very close to the Federal Reserve’s (Fed) 2% policy target. The September core PCE index is due today and is expected to show a further slowdown as well.

Soft landing: Achieved?

With the current data that we have in hand, some investors now argue that the Fed already achieved the soft landing that it was dreaming of. As such, the US dollar was weaker yesterday because the softening price pressures could allow the Fed to continue its rate cuts, but the downside remained limited because the data suggests that the cuts could be moderated. The ADP report showed yesterday that the US economy added 233K new private jobs last month, more than the double of 110K expected by analysts and was stronger than the number printed a month earlier. Of course, Friday’s official data will say the last word but Friday’s figures could also bring some positive surprises if the Boeing strike and hurricanes had a lighter than expected impact on the numbers. We will see.

For now, the US dollar remains bid despite yesterday’s weakness, the 2-year yield spiked higher – as the Fed doves scaled back their Fed cut bets. A 25bp cut at next week’s FOMC meeting remains on cards. The probability assessed to that is around 96%. But the Fed is not seen repeating the 50bp cut anytime soon.

Budget was ...ok

In the UK, the budget day couldn’t give the pound the energy it needed to clear the 1.30 offers. The announcement went as smoothly as it possibly could – given the amplitude of the bad news. Reeves said that the country will raise taxes by £40bn pounds to boost spending on public services. The UK also announced earlier that they would boost gilt sales by almost £20bn this fiscal year. But the spending would be less than expected by the market. That brilliant management of expectations helped traders keep their nerves together. The UK’s 10-year yield spiked to 4.40% but the selloff in sterling remained contained as the Bank of England’s (BoE) hopes of seeing further inflation easing in the UK went up in smoke as increased spending pressures are now knocking on the door.

China and Japan

China posted a small but unexpected expansion in its manufacturing sector in October, a piece of news that may have help crude oil extend yesterday’s recovery, and the Bank of Japan (BoJ) maintained its policy unchanged at today’s meeting, as expected, and Governor Ueda pointed out concerns regarding the increasingly uncertain global economic outlook. But the board ‘remains committed to further rate increases if economic and price data align with its forecasts’ and that line capped the upside in the USDJPY limited, and gave some strength to the yen.

Earnings update

Microsoft and Meta released their Q3 earnings yesterday, after the bell, and the results were good. Microsoft posted a better-than-expected quarterly revenue growth, fueled by its cloud computing business and Office – which integrates AI capabilities. But the company projected slower quarterly growth in cloud revenue, highlighting its challenge in bringing data centers online quickly enough to meet the rising demand for AI services. Shares dropped 3.7% in the afterhours trading.

Similar with Meta. The company posted strong quarterly results, improved ad revenue thanks to AI, but the weaker than expected user number in Q3, and the plans to spend more on AI didn’t please investors. The shares fell 3% in the afterhours trading.

Today, it’s Apple and Amazon’s turn to go to the earnings confessional. And they should not only meet and beat expectations but came in with a solid forecast to keep enthusiasm going.

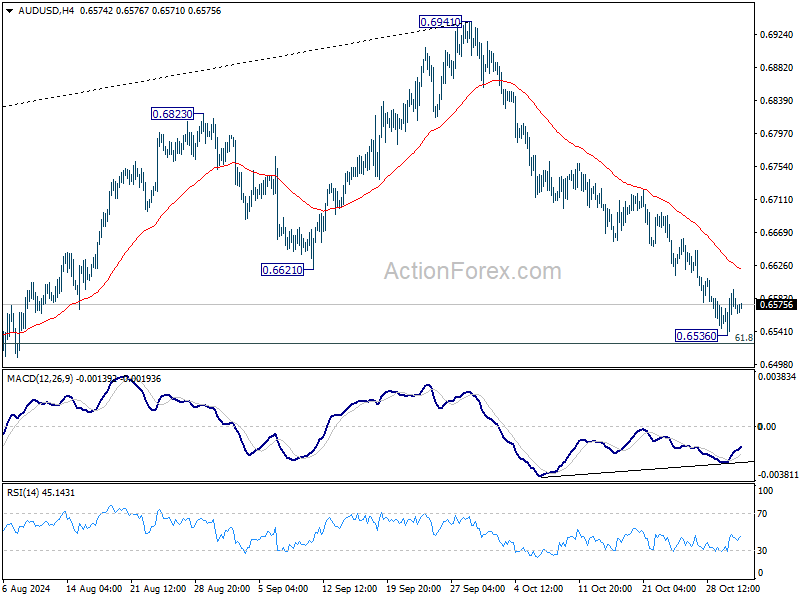

AUD/USD Daily Report

Daily Pivots: (S1) 0.6541; (P) 0.6568; (R1) 0.6600; More...

A temporary low was formed at 0.6536 with current recovery and intraday bias is turned neutral first. Further decline is expected as long as 55 D EMA (now at 0.6700) holds. On the downside, sustained break of 61.8% retracement of 0.6269 to 0.6941 at 0.6526 will target 0.6348 support next.

In the bigger picture, rise from 0.6269 (2023 low) should have completed with three waves up to 0.6941. Corrective pattern from 0.6169 (2022 low) is now extending with another falling leg. Deeper decline would be seen back to 0.6269 as sideway trading extends.

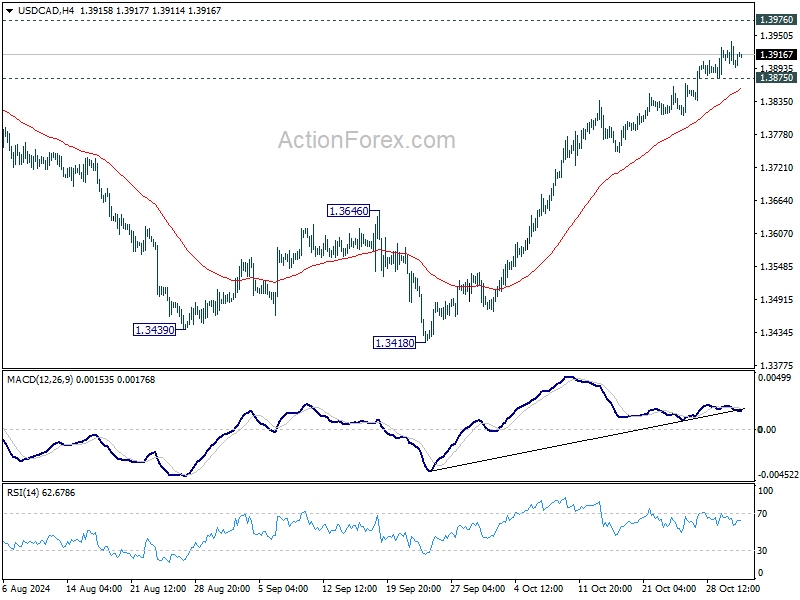

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3886; (P) 1.3913; (R1) 1.3932; More...

No change in USD/CAD's outlook and intraday bias stays on the upside for retesting 1.3946/76 resistance zone. Decisive break there will confirm larger up trend resumption. On the downside, below 1.3875 minor support will turn intraday bias and bring consolidations first.

In the bigger picture, sideway consolidation pattern from 1.3976 (2022 high) might still extend further. While another decline cannot be ruled out, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage. Decisive break of 1.3976 will target 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391.

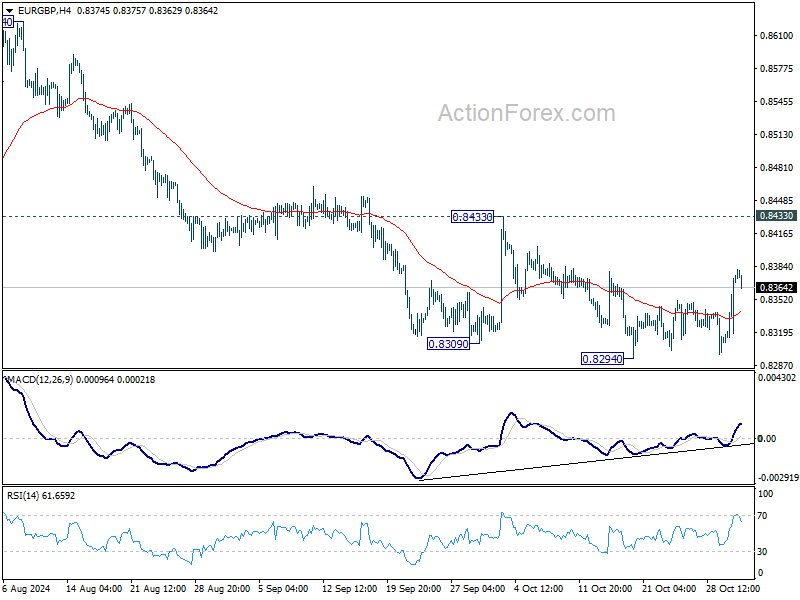

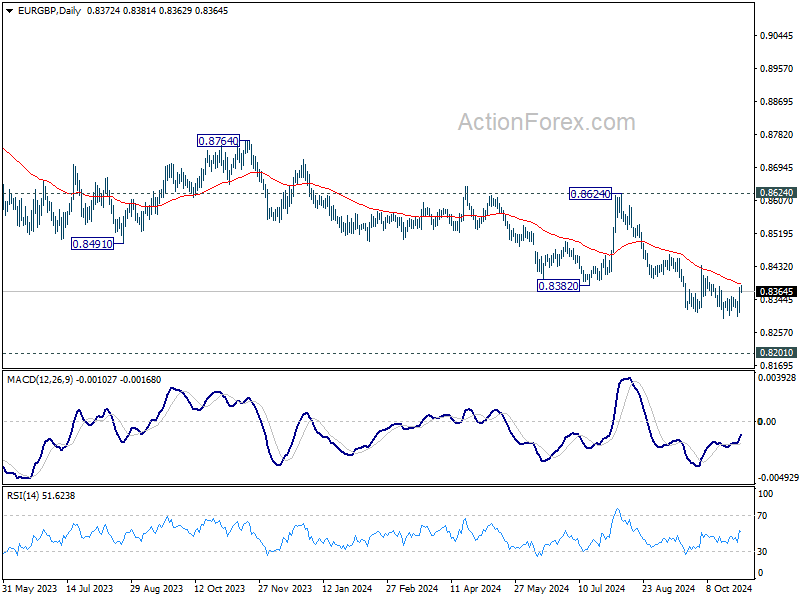

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8328; (P) 0.8353; (R1) 0.8400; More...

While EUR/GBP rebounded strongly, upside is still held below 0.8433 resistance. Intraday bias stays neutral and outlook remains bearish for now. On the downside, break of 0.8294 will resume larger down trend to 0.8201 key support next. Strong support could be seen from there to bring rebound.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

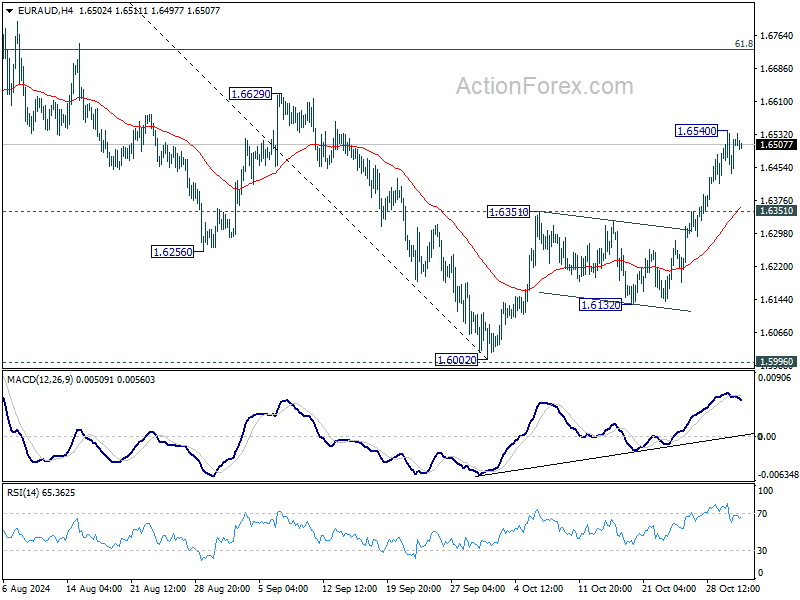

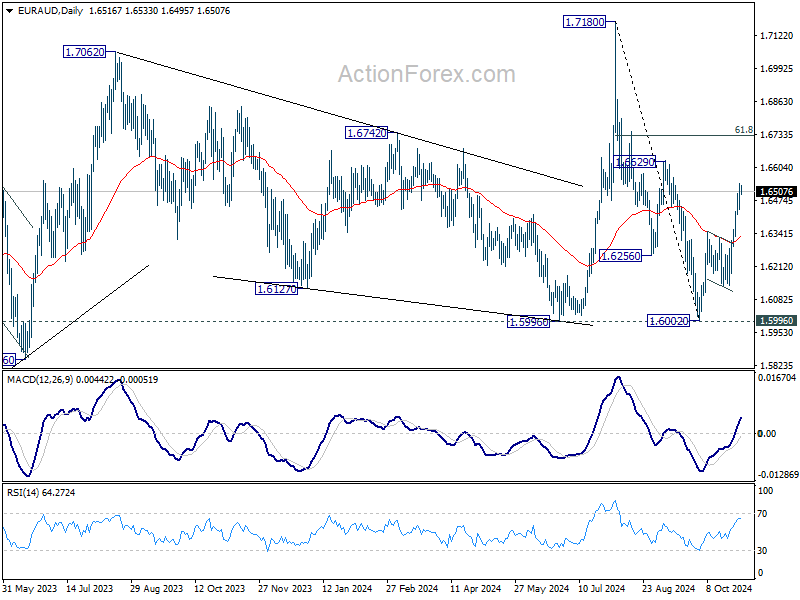

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6459; (P) 1.6501; (R1) 1.6561; More...

Intraday bias in EUR/AUD is turned neutral first with current retreat, and some consolidations would be seen. Further rally is expected as long as 1.6351 resistance turned support holds. Fall from 1.7180 should have completed with three waves down to 1.6002, after being supported by 1.5996. On the upside, above 1.6540 will target 61.8% retracement of 1.7180 to 1.6002 at 1.6730 next.

In the bigger picture, as long as 1.5996 cluster support holds (38.2% retracement of 1.4281 to 1.7062 (2023 high) at 1.6000), up trend from 1.4281 (2022 low) is still expected to resume at a later stage. However, decisive break of 1.5996 will argue that the medium term trend has reversed and turn outlook bearish.

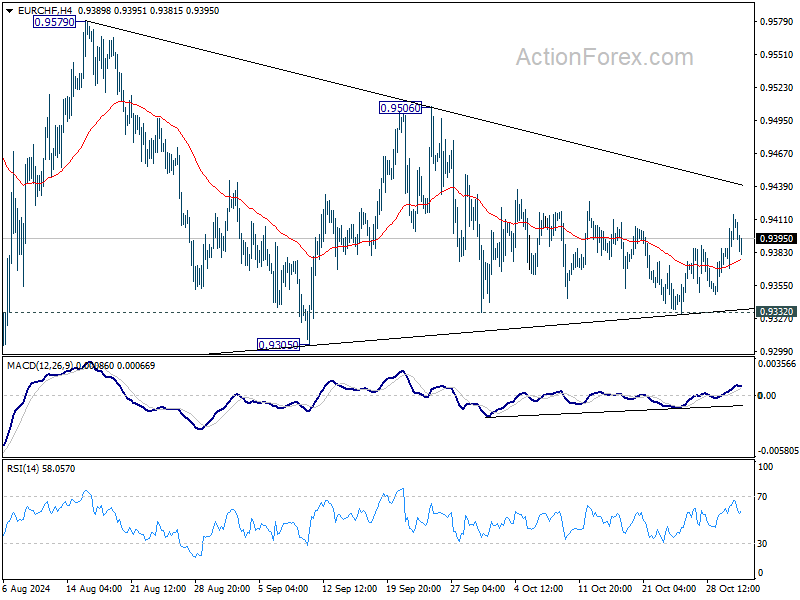

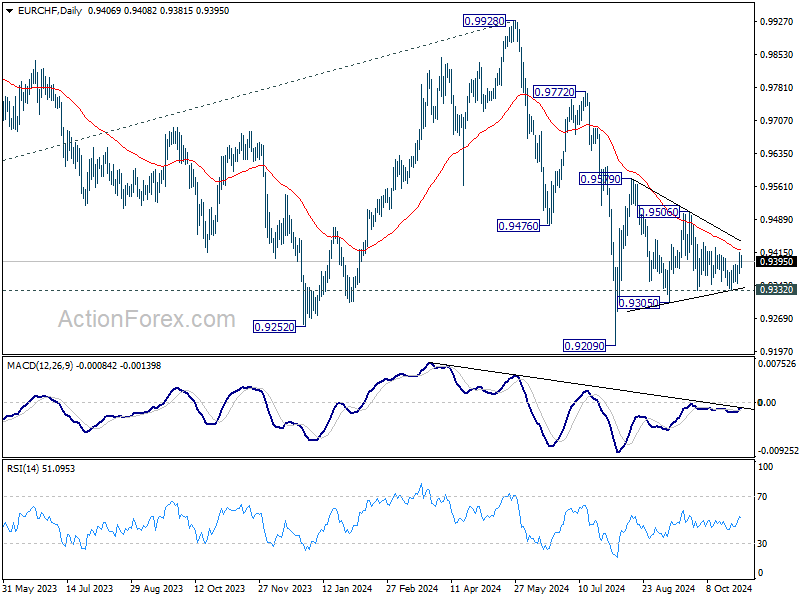

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9380; (P) 0.9399; (R1) 0.9426; More....

Intraday bias in EUR/CHF remains neutral as range trading continues. On the downside, break of 0.9332 will resume the fall from 0.9579 towards 0.9209 low. On the upside, break of 0.9506 will turn intraday bias to the upside for 0.9579 resistance and above.

In the bigger picture, fall from 0.9928 is seen as part of the long term down trend. Repeated rejection by 55 D EMA (now at 0.9427) keeps outlook bearish for breaking through 0.9209 low at a later stage. Nevertheless, sustained trading above 55 D EMA will confirm medium term bottoming and bring stronger rebound back towards 0.9928 key resistance.

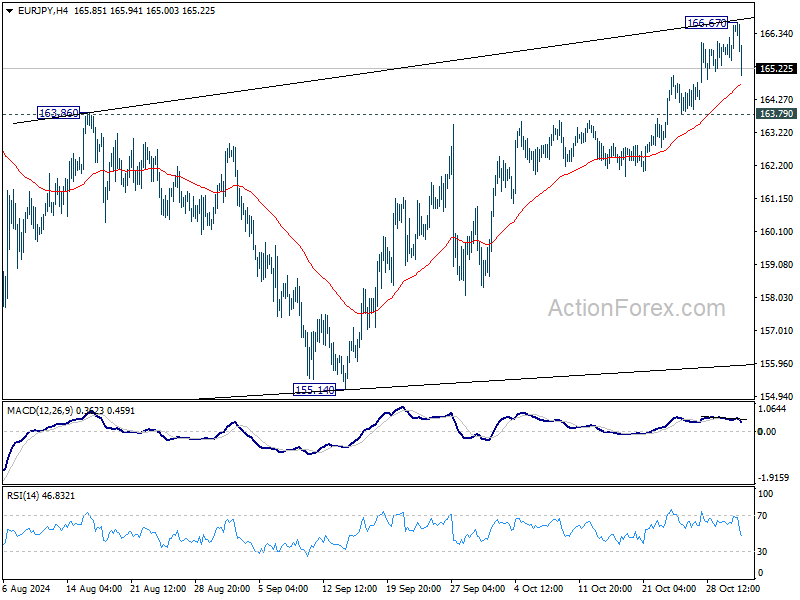

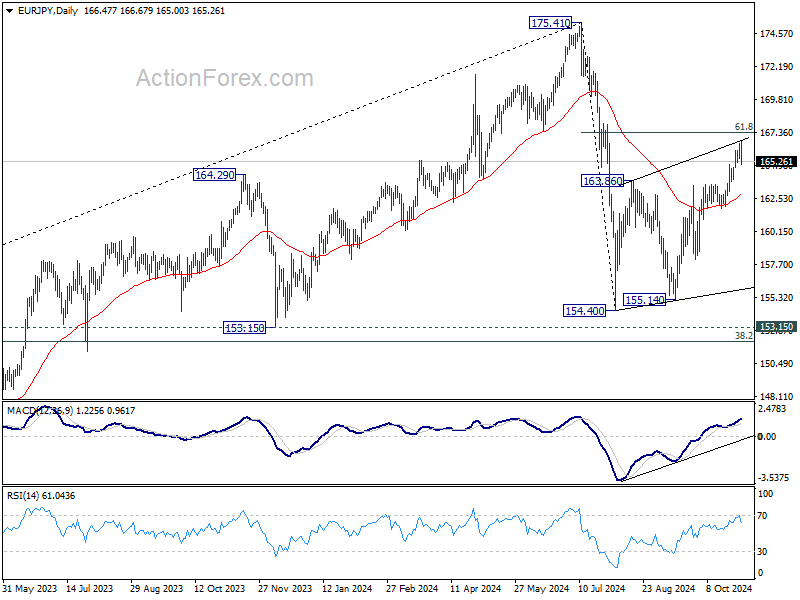

EUR/JPY Daily Outlook

Daily Pivots: (S1) 165.84; (P) 166.22; (R1) 166.93; More....

A temporary top was formed at 166.67 in EUR/JPY with current retreat. Intraday bias is turned neutral for consolidations first. Further rally is in favor as long as 55 D EMA (now at 162.85) holds. Sustained break of 61.8% retracement of 175.41 to 154.40 at 167.38 will pave the way to retest 175.41 high. However, firm break of 55 D EMA will argue that corrective rise from 154.40 has completed, and turn outlook bearish for this support again.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

All Eyes on Euro Area Inflation Today

In focus today

In the euro area, HICP inflation data for October is released. With inflation data out from Spain, Germany, and Belgium, we track euro area HICP at 2.0% y/y today, above consensus expectations (cons: 1.9%) driven by broadly higher inflation also in core inflation, which we see unchanged at 2.7% y/y (cons: 2.6%). Most importantly, we will see the monthly increase in seasonally adjusted services prices (prior: 0.14% m/m s.a.). For ECB this will help determine if weak momentum continued into October. We also receive the September unemployment rate, which will be interesting following easing labour market dynamics, while unemployment rate has remained record-low at 6.4%

In the US, the Employment Cost Index for Q3 is due for release this afternoon. This is a key measure of labour cost pressures for the Fed. September monthly PCE data will also be released.

The US Presidential election is coming closer, and we will host a conference call on 6 November to give our quick take on the potential market implications of the election: Conference call on the implications of the US election for Global and Scandi markets.

Economic and market news

What happened overnight

In Japan, the BoJ kept rates unchanged as expected this morning but stressed its intention to keep hiking borrowing costs if the economy sustains a moderate recovery. The BoJ will prefer a wait-and-see approach ahead of the US presidential election next week and until the political situation after the ruling coalition lost its majority is more certain. We expect another hike in December, particularly because the BoJ might see it as necessary to support the yen. With inflation on target and consumers' purchasing power heading slowly in the right direction, there is also an economically sound case for it, irrespective of the yen.

In China, October PMIs showed upbeat signs, with the composite PMI increasing to 50.8 driven by both manufacturing and non-manufacturing activities, which printed 50.1 (prior: 49.8) and 50.2 (prior: 50.0), respectively. This indicates that latest stimulus measures are helping pick up the economy.

What happened yesterday

In euro area, Q3 GDP rose 0.4% q/q beating expectations of a 0.2% q/q increase. The ECB estimated growth at 0.2% q/q in their latest projections, so the data comes as a pleasant surprise. Growth was driven by Spain which recorded a record 0.8% q/q expansion (cons: 0.6%, prior: 0.8%), France that got a boost from the Olympics with 0.4% q/q, and Germany that recorded rising activity of 0.2% q/q due to a downward revision of growth in Q2. However, growth outlook remains fragile as the manufacturing sector continues to struggle with declining activity and the service sector is moderating. The outlook for 2025 is dependent on consumption picking up as real income rises and an improvement in the industry. Currently, we are not seeing this, leaving downside risks to the outlook.

The higher-than-expected data on inflation and growth supports the case and our call for a 25bp cut by the ECB in December against a "jumbo" cut."

In the US, Q3 GDP figure is mostly in line with expectations at 2.8% q/q SAAR (cons: 2.9%). The increase particularly reflected solid growth in private spending, showing that consumers remain resilient ahead of the US presidential election. ADP employment for October exceeded expectations with +233k (cons: +111k). September is revised slightly higher from +143k to +159k. ADP has usually been a mixed predictor for NFP, so a modest reaction might be reasonable.

In Sweden, we changed our call for the Riksbank meeting next week and we now expect a 50bp cut down to 2.75% (previously 25bp cut). This change follows the release of disappointing growth data earlier this week. The GDP indicator for Q3 reported a decrease of -0.1% q/q. Additionally, both the Riksbank's company survey and the NIER survey have shown diminished expectations in the business sector. For a full preview ahead of next week's Riksbank decision.

In the UK, the Labour government released their first budget. In line with our expectation, the budget provided some expansionary measures with funding sourced from large tax increases worth GBP 40bn and the change in debt measure estimated to provide around GBP 50bn. However, and importantly, borrowing is set to rise substantially averaging GBP 36bn each year over the next five years. We have long argued that a more expansionary budget could trim markets expectation for a December cut, which today's events have provided support for. We continue to expect a 25bp cut in November and an unchanged decision in December.

Equities: Global equities were lower yesterday, driven by disappointing earnings and likely some de-risking ahead of the US election. In our opinion, macro data should not be blamed for the weak development yesterday, as most macro figures were strong, even in Europe where equities underperformed the most. Please also consider bond yields, which were marginally higher, as well as sector and style rotations; cyclicals performed well, quality underperformed, and minimum volatility was flat. This does not suggest a classic negative environment based on growth fears. Apologies for repeating ourselves here; this is expected given the massive number of factors currently at play, plus US election being less than one week away. In the US yesterday, Dow -0.2%, S&P 500 -0.3%, Nasdaq -0.6%, and Russell 2000 -0.2%. Asian markets are lower this morning, with Chinese stocks standing out on the positive side. European and US futures are also lower, led by the tech and growth segments of the indices.

FI: In a choppy session, driven by a heavy string of data releases, we saw yields selling off from the front end in a bearish flattening of the curves. The upside surprise to German inflation data took out 4bp of the jumbo rate cut discussion for December and thus now 'only' points to 31bp of ECB rate cuts in December. This combined with higher European growth (and above ECB projected Q3 development), means that a slower and more gradual approach was assessed as the most likely scenario by markets.

FX: EUR/USD trended toward the upper end of the 1.08-1.09 range on the back of euro area data that was better than feared. USD/JPY declined slightly, still hovering around 153 after the Bank of Japan's anticipated decision to hold the policy rate at 0.25% this morning. EUR/GBP experienced a rollercoaster day in an eventful session for UK markets with the release of the Labour government's first budget. NOK/SEK continues to move higher, driven largely by relative rate spreads as NOK-SEK spreads reach new wides. EUR/NOK drifted up to 11.90, while EUR/SEK neared 11.60.

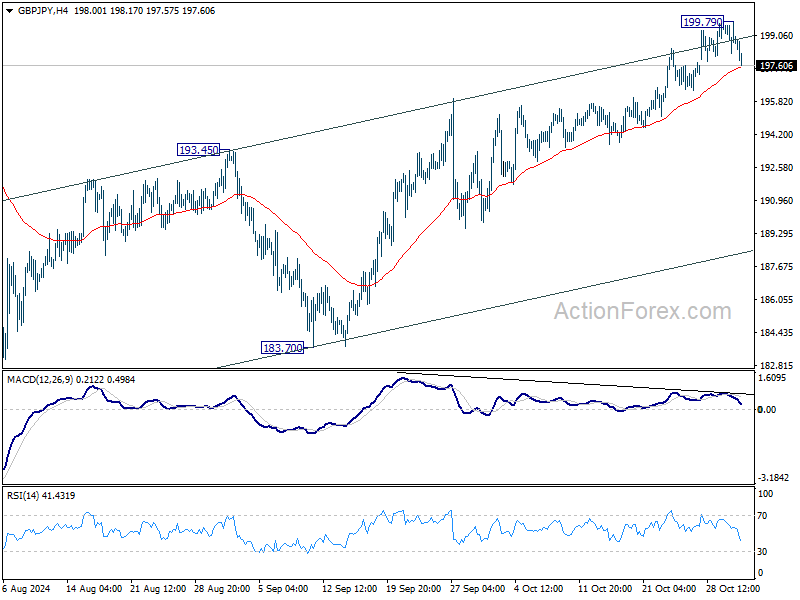

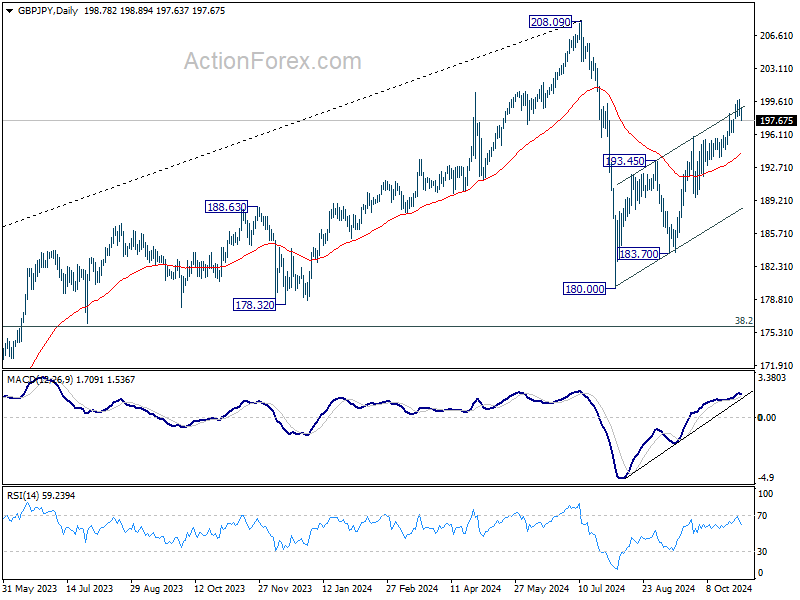

GBP/JPY Daily Outlook

Daily Pivots: (S1) 198.10; (P) 198.96; (R1) 199.70; More...

A temporary top is formed at 199.79 in GBP/JPY with current retreat. Intraday bias is turned neutral for consolidations first. Further rally would remain in favor as long as 55 D EMA (now at 194.20) holds. Above 199.79 will resume the rebound from 180.00 to retest 208.09 high. However, sustained break of 55 D EMA will argue that the corrective rise has completed already, and turn near term outlook bearish for 180.00/183.70 support zone.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

Yen Recovers as BoJ Holds Rates; Euro Strengthens Ahead of Inflation Data

Yen recovers broadly today after BoJ left interest rates unchanged, and largely maintained the economic projections unchanged too. The direction of monetary policy remains clear as the next move is a hike if the outlook is realized. Yet, BoJ dropped no clue on the timing. Data from Japan were mixed, with stronger industrial production and weak retail sales, they're not giving the markets any direction.

Overall, Euro is now the strongest one for the week so far, supported by yesterday's Eurozone GDP data, which lessen the need for aggressive policy easing from ECB. Focuses will turn to October CPI flash today. An up tick in headline inflation is expected while core inflation would continue the down trend.

Dollar and Swiss Franc are following as the next strongest. Focuses in the US would be on September PCE which would show slight decline in both headline and core inflation. But the main event for the week would be tomorrow's non-farm payroll which is the most important data for Fed's near term moves. Still, US presidential election stays as the biggest influence for the US economy and Fed for the medium term.

On the other hand, Aussie continues to sit at the bottom despite today's slight recovery. Yen is the next worst, followed by Canadian. Kiwi and Sterling are positioning in the middle.

Technically, an immediate focus today is whether EUR/USD could bounce through 1.0871 resistance. That would confirm short term bottoming an 1.0760, on bullish convergence condition in 4H MACD. This development would turn the fall from 1.1213 into consolidation mode first, before staging another decline at a later stage.

In Asia, Nikkei fell -0.50%. Hong Kong HSI is up 0.36%. China Shanghai SSE is up 0.63%. Singapore Strait Times is down -0.88%. Japan 10-year JGB yield is down -0.0055 at 0.947. Overnight, DOW fell -0.22%. S&P 500 fell -0.33%. NASDAQ fell -0.56%. 10-year yield fell -0.008 to 4.266.

ECB's Lagarde: Inflation target in sight but prudence warranted

In an interview with Le Monde, ECB President Christine Lagarde expressed cautious optimism about Eurozone's inflation path, noting that the target is "in sight" but stressing that inflation is not yet fully subdued. While headline CPI dipped to 1.7% in September, core inflation, excluding energy and food, remained elevated at 2.7%.

Lagarde acknowledged satisfaction with the recent drop in headline inflation but warned that “inflation is going to rise again in the coming months” due to base effects. Thus, she emphasized that "prudence is warranted."

She reiterated the importance of reaching the 2% target "on a sustained and durable basis," projecting that, barring any major shocks, the ECB expects this goal to be achieved by 2025.

BoJ maintains rate at 0.25% on unanimous vote

BoJ kept its uncollateralized overnight call rate steady at approximately 0.25% in a unanimous decision, aligning with market expectations. The central bank indicated that if the outlook for economic activity and prices materializes as anticipated, it will "accordingly continue to raise the policy interest rate and adjust the degree of monetary accommodation." This signals readiness to tighten monetary policy further, contingent on economic developments.

Nevertheless, BoJ emphasized the necessity of paying close attention to the "future course of overseas economies," particularly the US, along with developments in financial and capital markets due to their impact on Japan's economic activity and price outlook.

In its latest economic projections, the BoJ made the following adjustments:

Real GDP Growth:

- Fiscal 2024: Unchanged at 0.6%.

- Fiscal 2025: Revised upward from 1.0% to 1.1%.

- Fiscal 2026: Unchanged at 1.0%.

CPI Core (excluding fresh food):

- Fiscal 2024: Unchanged at 2.5%.

- Fiscal 2025: Revised downward from 2.1% to 1.9%.

- Fiscal 2026: Unchanged at 1.9%.

CPI Core-Core (excluding fresh food and energy):

- Fiscal 2024: Increased from 1.9% to 2.0%.

- Fiscal 2025: Unchanged at 1.9%.

- Fiscal 2026: Unchanged at 2.1%.

Japan’s industrial production rises 1.4% mom in Sep, continues to fluctuate indecisively

Japan’s industrial production increased by 1.4% mom in September, exceeding expectations of 0.8%. This recovery follows a sharp -3.3% mom drop in August when a typhoon disrupted operations across various sectors.

Out of the 15 industrial sectors surveyed, 10, including motor vehicles and chemical production, recorded growth. Five sectors, such as production machinery, saw declines.

Despite this recovery, the Ministry of Economy, Trade and Industry maintained its cautious view, describing industrial production as “fluctuating indecisively.”

Looking ahead, manufacturers polled by the ministry expect a robust 8.3% mom increase in output for October, followed by a -3.7% mom decline in November, indicating ongoing volatility in Japan’s production.

Meanwhile, Japan’s retail sales rose by a modest 0.5% yoy in September, falling significantly short of the anticipated 2.3% yoy growth.

China’s NBS PMI manufacturing rises to 50.1, first expansion in six months

China’s NBS Manufacturing PMI increased to 50.1 in October, meeting expectations and marking the first expansion since April. The improvement was led by large enterprises, which rose to 51.5 from 50.6, while medium-sized firms inched up to 49.4. Small enterprises, however, saw a further contraction, declining to 47.5 from 48.5.

Key subindices pointed to slight domestic improvement: production reached a six-month high of 52.0, and new orders returned to neutral at 50.0 after five months of contraction.

Though still below 50, subindices for employment (48.4), purchases (49.3), imports (47.0), and backlog of orders (45.4) showed smaller declines, suggesting a gradual stabilization.

However, new export orders continued to weaken, reaching an eight-month low at 47.3, underscoring soft external demand.

Non-Manufacturing PMI edged up from 50.0 to 50.2, just shy of the 50.5 forecast, with the employment subindex rising by 1.1 points to 45.8.

NZ ANZ business confidence hits 10-yr high , optimism grows on lower interest rates

New Zealand’s ANZ Business Confidence surged from 60.9 to 65.7 in October, marking its highest level in a decade and reflecting a wave of optimism among businesses.

This renewed confidence is supported by a range of positive indicators: the outlook for own activity increased slightly from 45.3 to 45.9, while export intentions jumped from 13.8 to 17.1, the highest since September 2018. Investment intentions also surged from 9.2, reaching 20.0, the highest level since June 2021, and employment intentions rose from 11.8 to 14.2, the highest since November 2021.

Several key metrics highlight this optimism. Cost expectations dropped from 66.8 to 64.2, indicating some relief in business expenses, while wage expectations edged up slightly from 76.4 to 77.0. Pricing intentions also rose, climbing from 42.8 to 44.2, suggesting businesses may feel confident in passing some costs to consumers. Profit expectations strengthened from 22.2 to 27.0, and inflation expectations continued their downward trend, dipping from 2.92% to 2.82%.

According to ANZ, "steady falls in interest rates" have provided a strong boost to business sentiment, encouraging growth across multiple sectors.

Australia’s retail sales show modest 0.1% mom growth in Sep

Australia’s retail sales turnover increased by a modest 0.1% mom in September, reaching AUD 36.46B but falling short of the expected 0.4% mom rise. This follows a 0.7% gain in August and a flat outcome in July.

Commenting on the data, Robert Ewing, Head of Business Statistics at ABS, noted that “retail spending held firm in September” following a boost in August from warmer-than-usual weather.

The report also highlighted quarterly retail sales volumes, which grew by 0.5% in Q3, marking a recovery after back-to-back declines of -0.4% in both Q2 and Q1.

Ewing added that this increase in volumes reflects “some of the lost ground in discretionary spending this year,” marking only the second quarterly rise in retail volumes over the past two years.

Looking ahead

Eurozone CPI flash is the main focus in European session while unemployment rate will also released. Germany import prices and retail sales will also be published.

Later in the day, US PCE inflation will be the main focus. Jobless claims and Chicago PMI will also be released. Canada will publish monthly GDP.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 198.10; (P) 198.96; (R1) 199.70; More...

A temporary top is formed at 199.79 in GBP/JPY with current retreat. Intraday bias is turned neutral for consolidations first. Further rally would remain in favor as long as 55 D EMA (now at 194.20) holds. Above 199.79 will resume the rebound from 180.00 to retest 208.09 high. However, sustained break of 55 D EMA will argue that the corrective rise has completed already, and turn near term outlook bearish for 180.00/183.70 support zone.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.