Sample Category Title

Eurozone PMI Temporarily Helps the Euro but Is Unlikely to Change the Trend

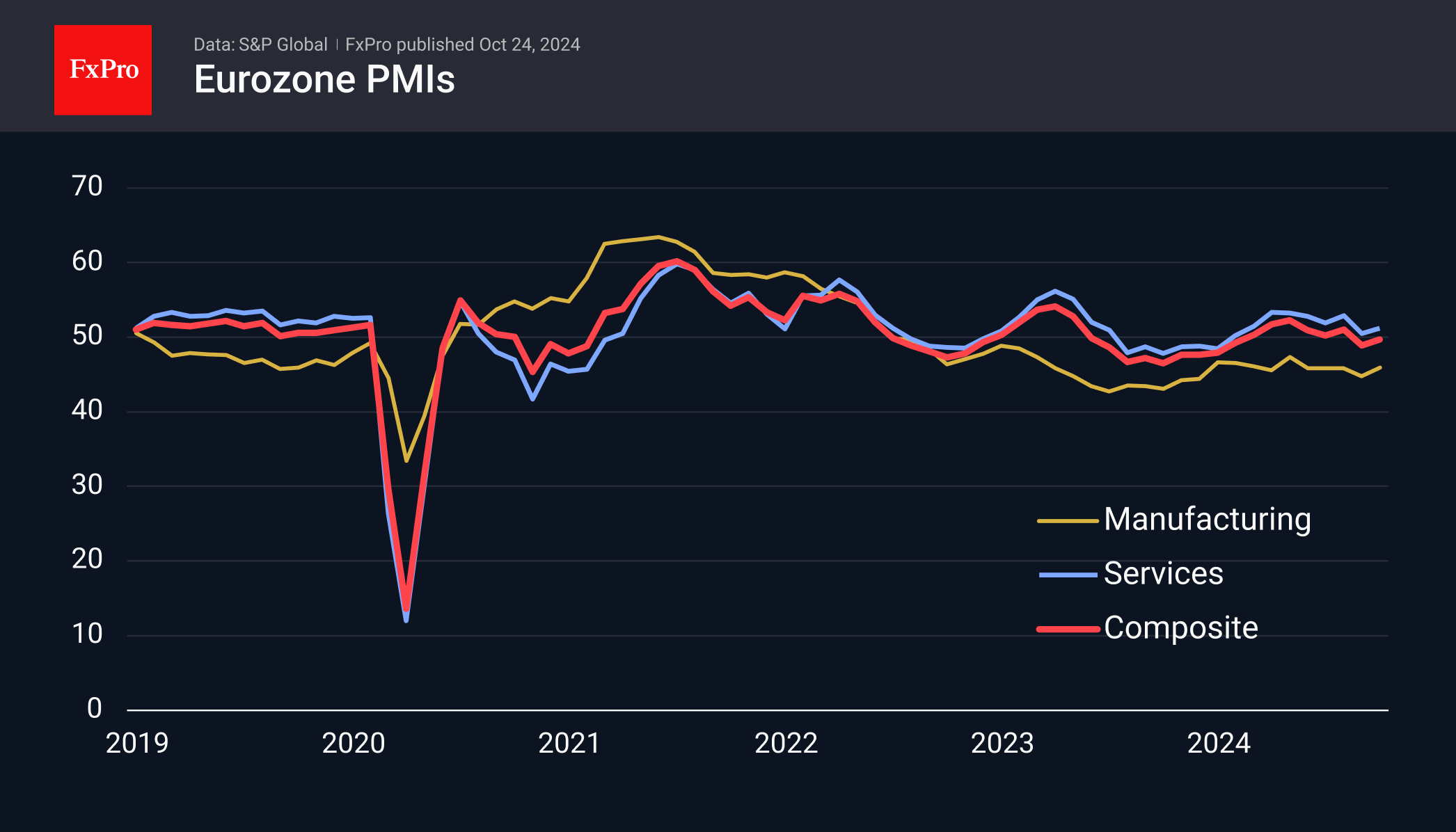

On Thursday, S&P Global released flash estimates for the October PMIs across major regions. The significance of this data increases over time, and in Europe, it often influences market trends.

The European data was mixed, but the currency market focused on stronger-than-expected numbers from Germany.

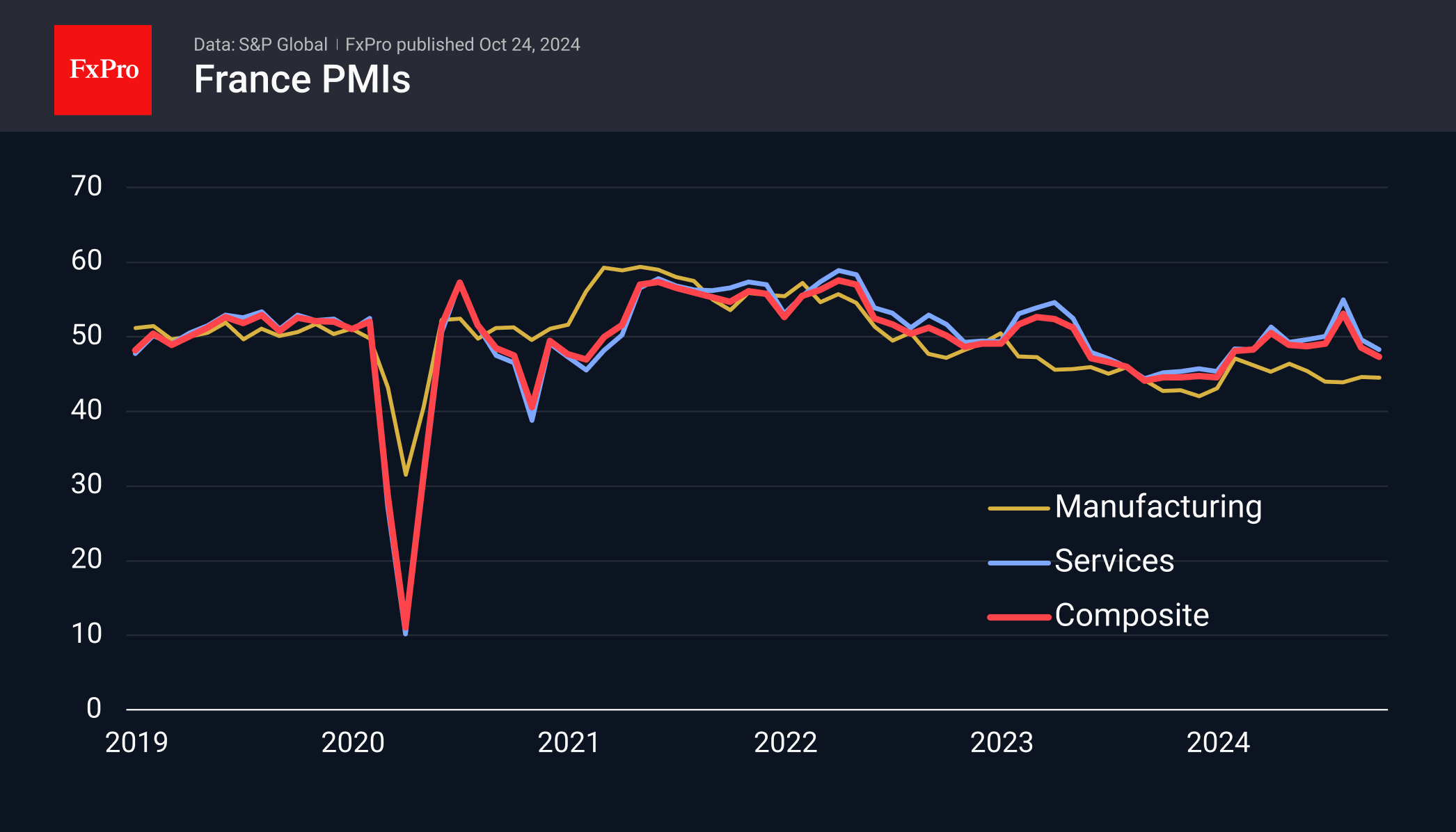

In France, the services sector is experiencing a deeper decline following a boost from the Olympics. The services index dropped from 49.6 to 48.3, marking its lowest point since the end of last year. Meanwhile, the manufacturing PMI remains in contraction territory at 44.5, staying below 50 for the second consecutive month. The composite index also fell to a nine-month low of 47.3.

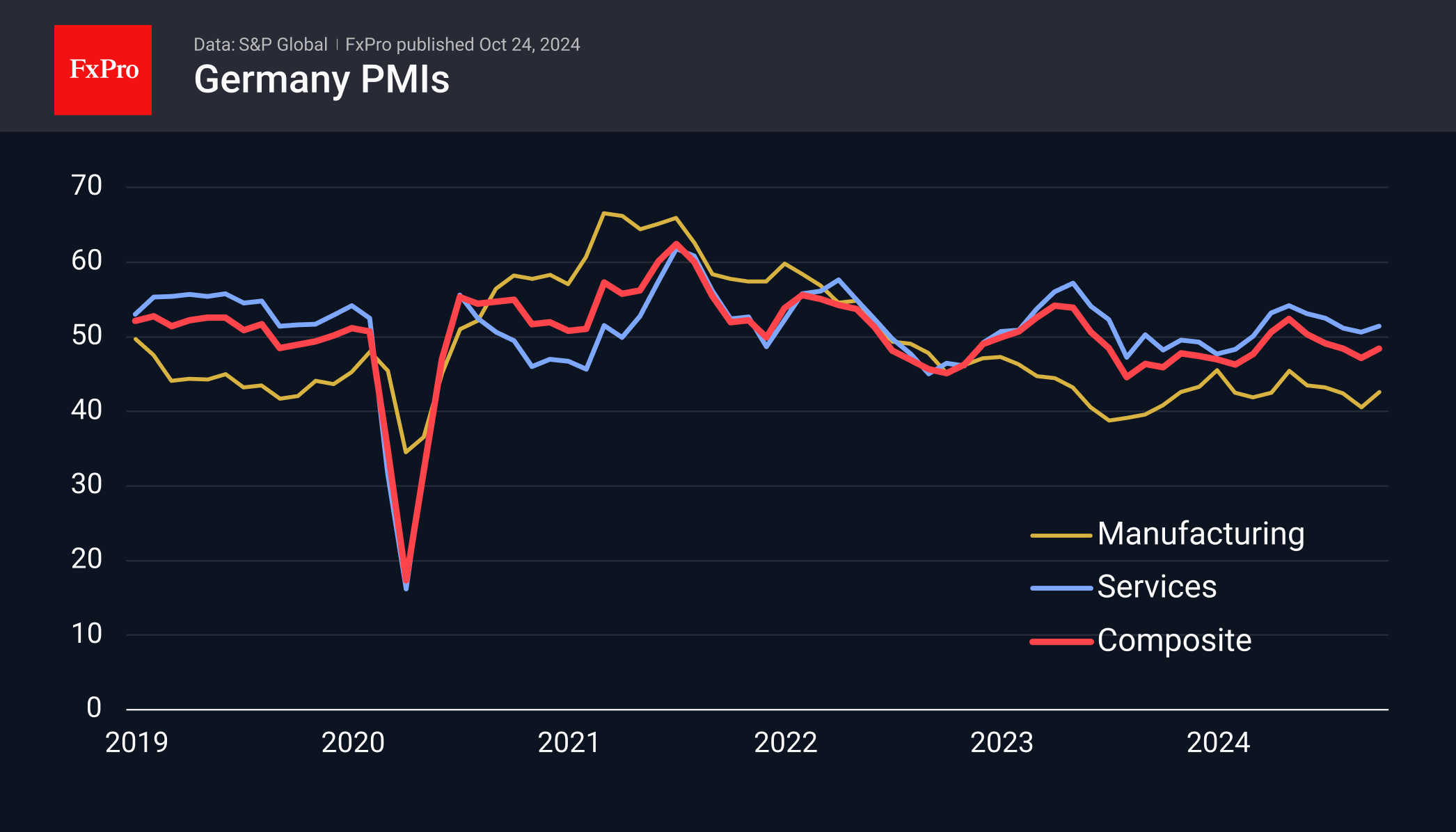

Index estimates for Germany shifted the euro’s trajectory, beating forecasts by a wide margin. The services index rose to 51.4 after four months of decline. The manufacturing PMI rose from 40.6 to 42.6, although 40.7 was expected. This rebound offers some reassurance, as German manufacturing, as measured by the PMI, has been in contraction territory since July 2022. As a result, the composite index stands at 48.4 in October, remaining below the 50 mark for the past four months.

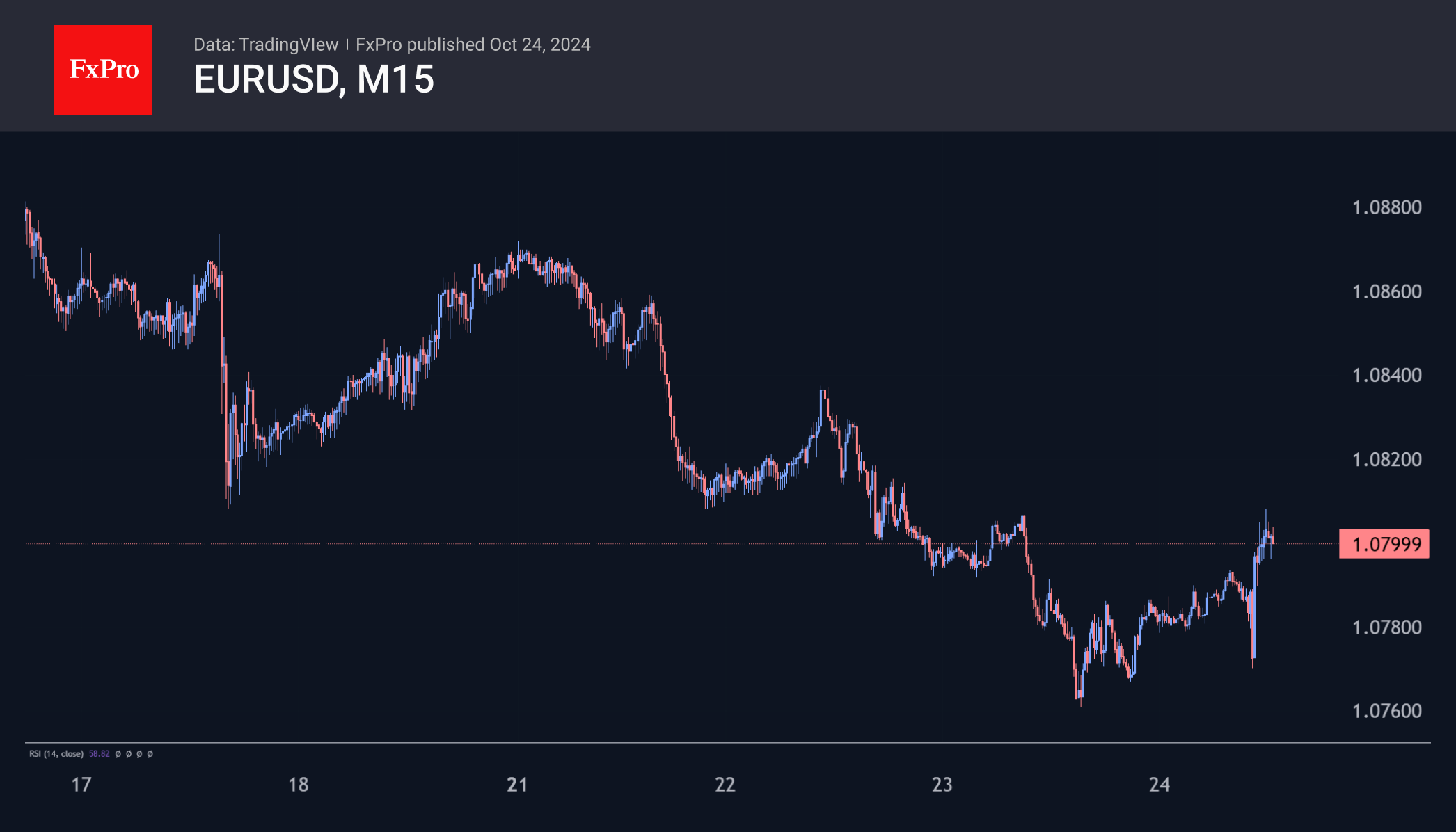

Investors and traders clearly saw the light at the end of the tunnel, as they noted the slight reversal of the German PMIs towards growth, prompting a 0.35% jump in the EUR/USD immediately after the release. However, in the short term, the single currency struggled to break above the 1.08 level, which appears to act as local resistance.

The PMI data for the entire Eurozone exceeded expectations for the manufacturing sector, with the index reaching a five-month high of 45.9. Meanwhile, growth in the services sector picked up slightly, as the composite index increased from 48.9 to 49.7, remaining in contraction territory.

Better-than-expected German data helped the euro pause its decline. Against this backdrop, EURUSD may be able to start a corrective bounce after its almost continuous failure since the end of September. However, the improvement is too modest to affect the ECB’s dovish tone on interest rates in the coming weeks. The central bank is still expected to cut rates actively.

WTI Crude Oil Meets Downtrend Line Again

- WTI crude oil surpasses 20- and 50-day SMAs

- Technical oscillators are mixed

WTI crude oil futures are experiencing a new bullish wave, meeting the medium-term descending trend line again near the 73.00 level after the significant rebound off the 68.90 support level.

Technically, the MACD oscillator is moving horizontally still beneath its trigger and zero lines; however, the stochastic oscillator is climbing above the 80 level, confirming the upside momentum in the market. Moreover, the price is standing above the 20- and 50-day simple moving averages (SMAs).

If there is a steeper bullish move, the commodity may retest the 76.65 resistance and the significant 200-day SMA at 77.85 that failed to surpass it in the preceding days. A successful climb above it could endorse the positive scenario, hitting the next levels of 78.75 and 80.50.

On the flip side, a retreat below the downtrend line could take the bears near the previous trough of 68.90 and the 67.00 round number. More downside pressure could open the way for the 17-month low of 65.70.

In summary, WTI crude oil is battling against the downward trend line and exhibiting indications of improvement in the medium-term outlook.

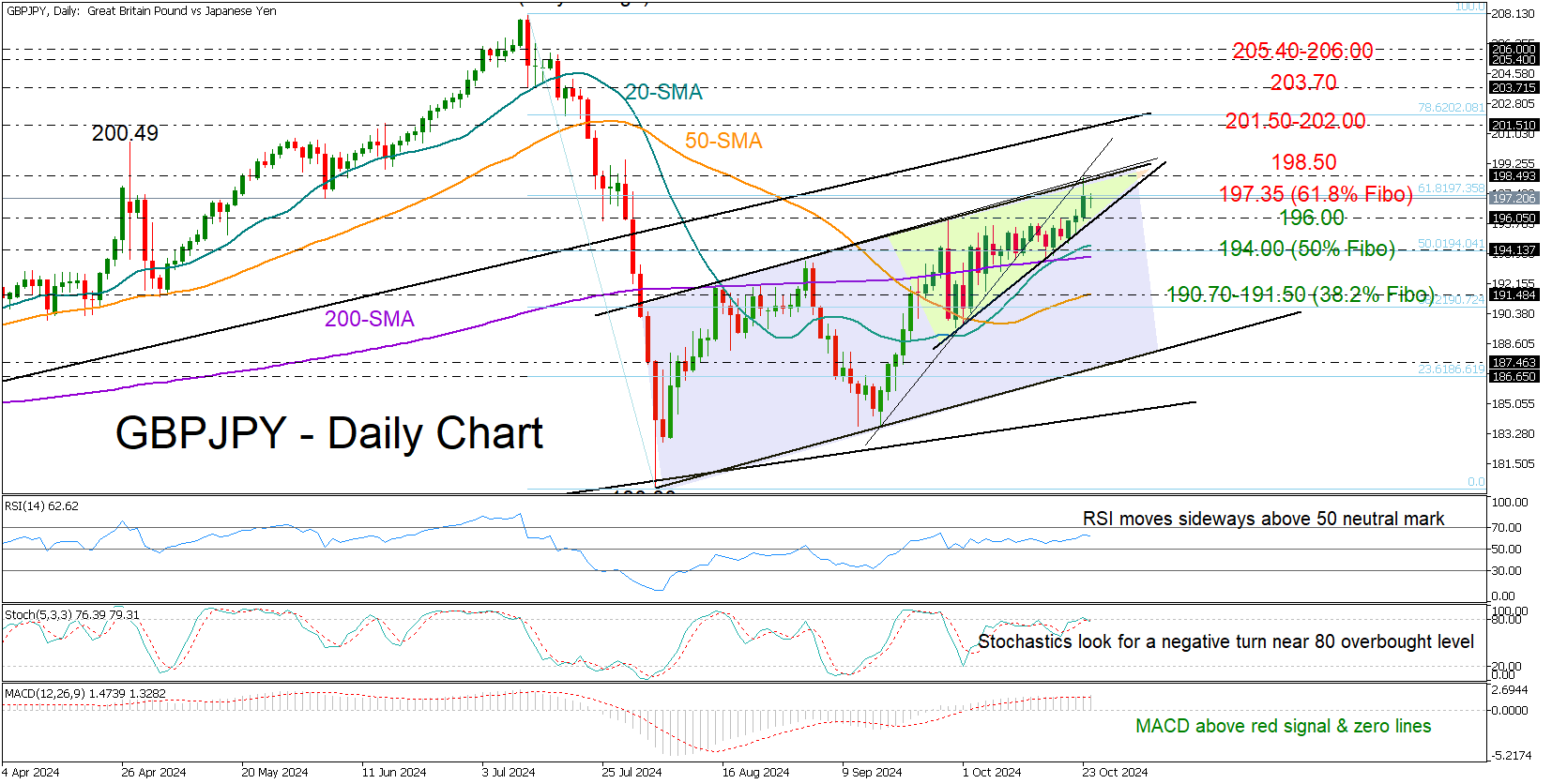

GBPJPY at 3-Month High

- GBPJPY marks new higher high; remains restricted

- Resistance near 198.50; support seen around 196.00

GBPJPY charted a three-month high of 198.42 at the top of a bullish channel, increasing speculation that a new bearish wave could soon start, especially after the close below the 61.8% Fibonacci retracement at 197.35.

Technical indicators are showing mixed signals: the stochastic oscillator is poised for a decline, while the RSI and MACD remain in bullish territory. The 20-day SMA crossing above the 50- and 200-day SMAs suggests potential trend continuation, but a bearish rising wedge is currently creating uncertainty.

If the price breaks above 198.50, the next resistance could occur between 201.50 and 202.00. Continued buying may then push the pair to 203.70 and then towards the 205.40-206.00 zone.

Alternatively, a slide below the 196.00 number could find initial support around the 194.00 area, where the 20- and 200-day SMAs as well as the 50% Fibonacci level are positioned. Further losses could retest the 50-day SMA and the 38.2% Fibonacci of 190.70, a break of which could cause a dramatic downfall towards the channel’s lower band currently seen at 187.20.

In short, GBPJPY is in a cautious area, with decisive movements above 198.50 or below 196.00 likely guiding future price action.

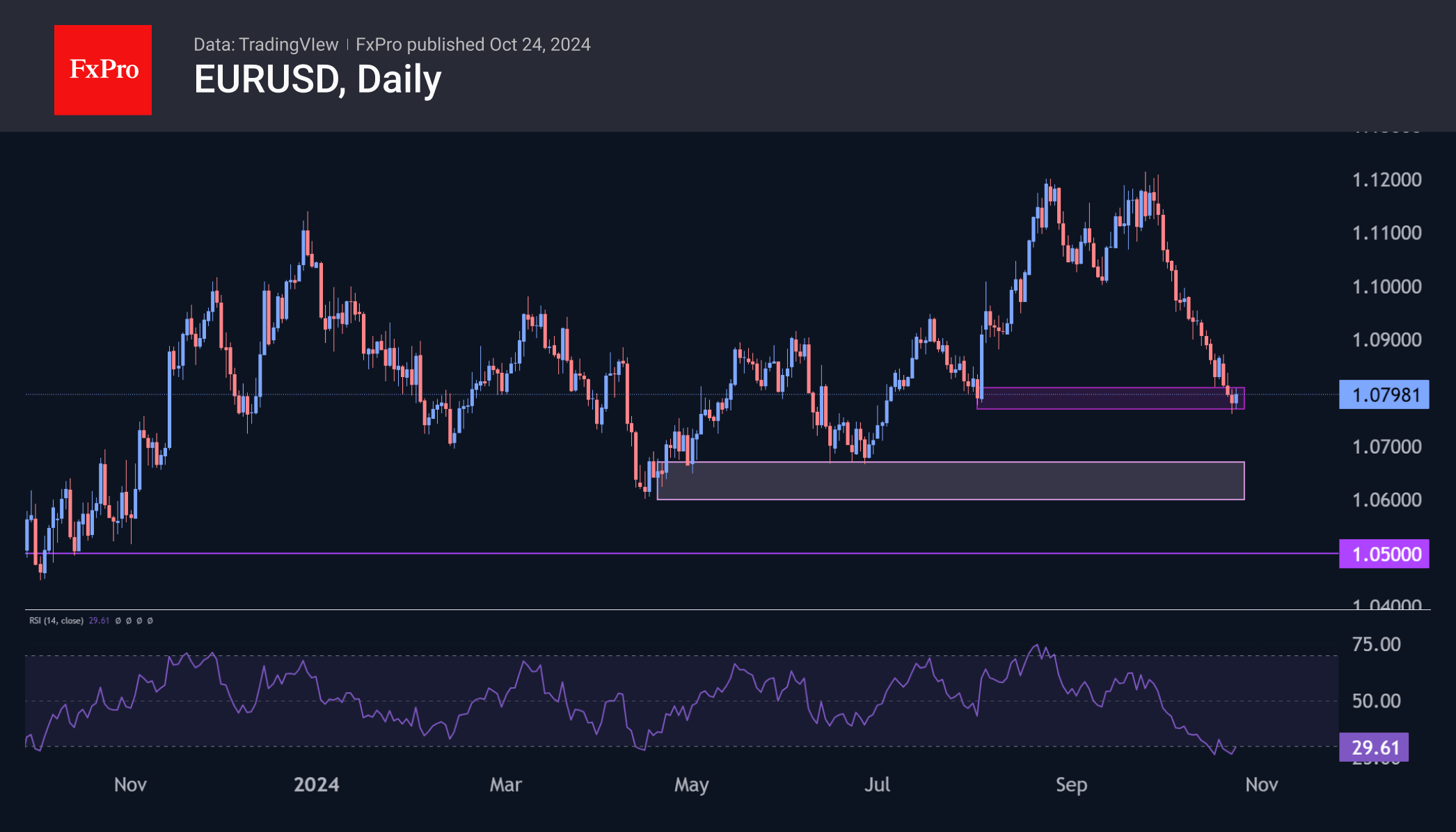

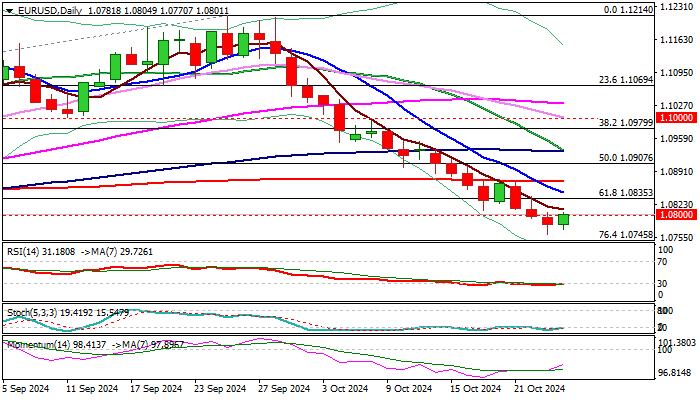

EUR/USD Outlook: Overall Negative PMI Data and Dovish ECB to Weigh on Current Recovery Attempts

EURUSD edges higher on Thursday morning as oversold daily studies prompted partial profit taking.

Recovery is unlikely to be significant as the pair is in a larger downtrend, driven by negative technical and fundamentals.

Release of PMI data from EU, Germany and France showed that French business activity contracted more in October, while results from Germany were slightly better and numbers from the EU bloc fell below expectations.

According to the latest releases, manufacturing sector continues to suffer with no firm signs of significant recovery in the horizon, while services sector performs better as PMI numbers remain above 50 threshold which divides contraction from growth (Germany, EU) but overall picture shows that business activity is still contacting.

Adding to euro’s negative outlook were the latest dovish comments from ECB officials which suggest that the central bank should keep cutting interest rates until monetary policy enters the territory that stimulates economic growth.

Fresh recovery attempts probe through broken 1.0800 level and eyeing resistances at 1.0835/48 (broken Fibo 61.8% / falling 10DMA) with 200DMA (1.0869) marking solid barrier which should cap upticks.

Res: 1.0835; 1.0848; 1.0869; 1.0907.

Sup: 1.0761; 1.0745; 1.0700; 1.0666.

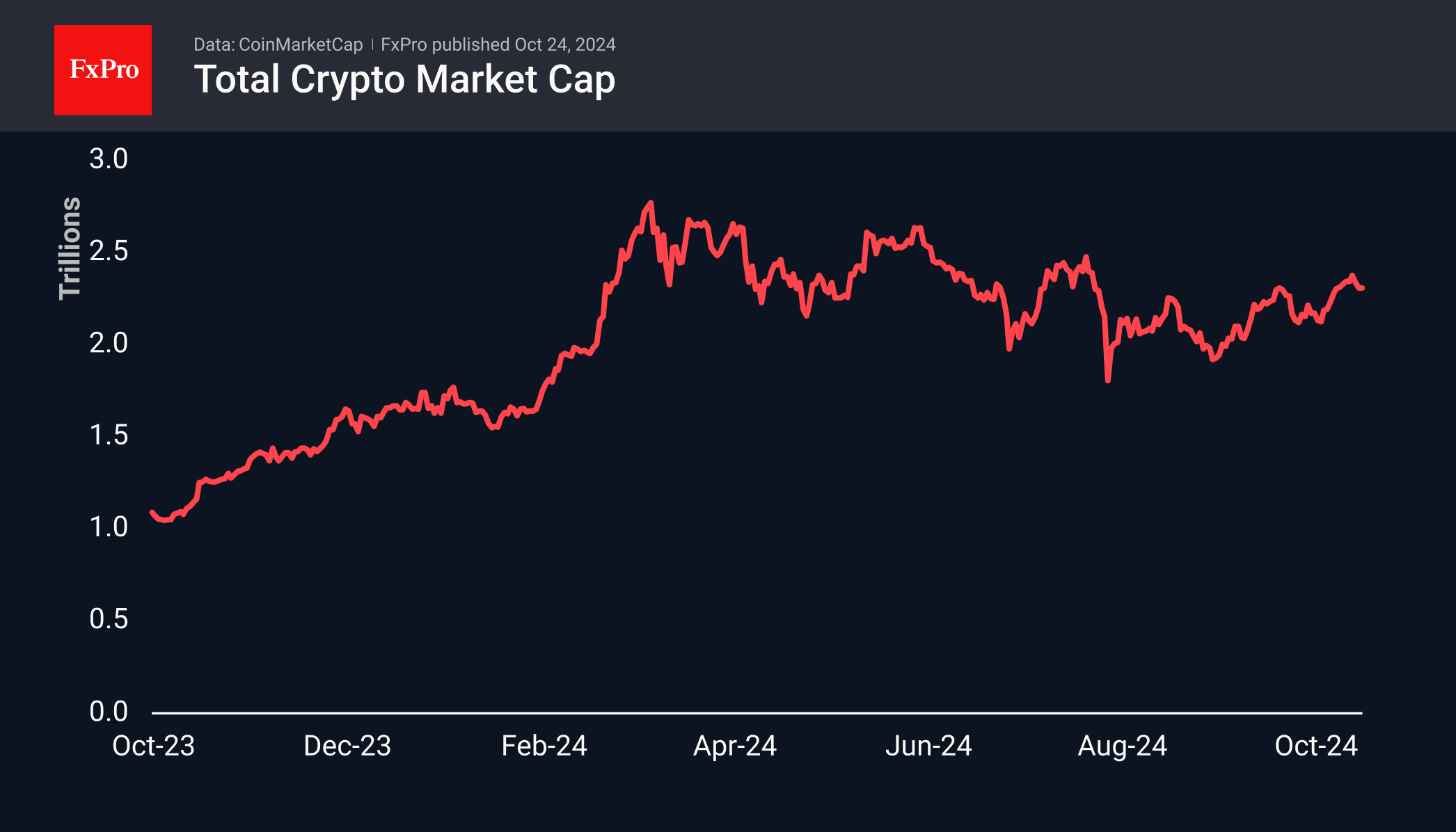

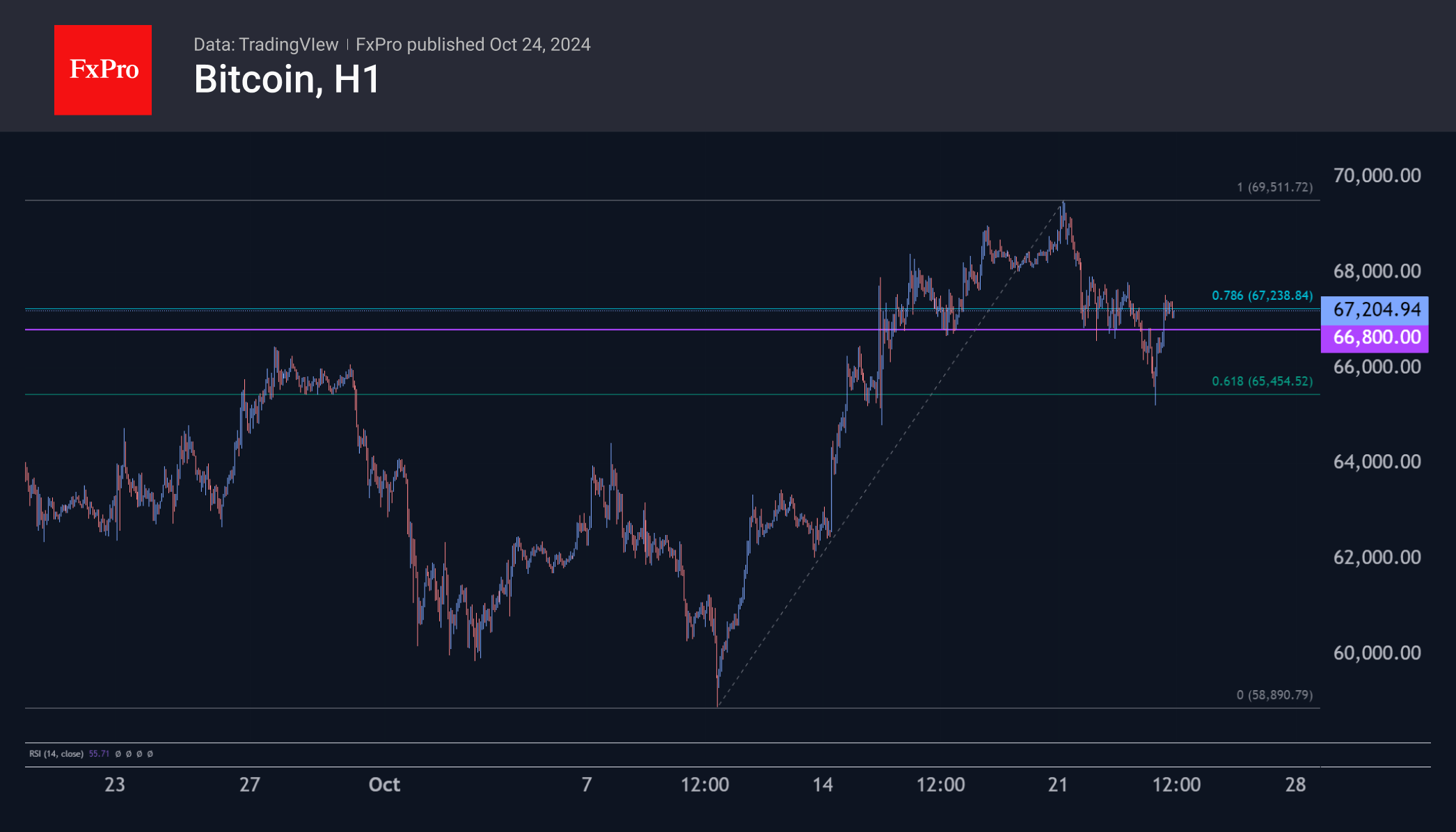

Has Bitcoin Completed a Correction?

Market Picture

The cryptocurrency market has been rising since the start of the day on Thursday, recovering strongly from Wednesday’s late afternoon sell-off in the wake of global financial markets. At its lowest point, the market capitalisation was down to $2.23 trillion, and at the time of writing, it had risen to $2.32 trillion (+0.1% in 24 hours). The market’s intraday movements will reveal whether this marks the bears’ last stand or if the current rebound is just a bull trap.

Bitcoin’s intraday dynamics are bullish. Wednesday’s end-of-day lows saw a flash drop below $65.5K, completing a 61.8% Fibonacci retracement of the 10-21 October rally. A quick exit to the recent highs at $69.5K would make the main scenario an extension of the upside with the potential to strengthen to $76K before further consolidation.

News Background

According to CryptoQuant, 94% of the Bitcoin supply is ‘long’, with the median purchase price hovering around $55K. Such high levels of unrealised profits have historically served as a precursor to significant BTC corrections.

Retail demand for Bitcoin returned to pre-ATH levels in March. This contrasts with the first quarter when large players largely drove demand.

Bernstein reiterated its prediction of a $200K price for the first cryptocurrency by the end of next year, calling it ‘conservative’. BTC’s investment appeal is increasing against the backdrop of rising US government debt and the threat of inflation.

DAX 40 Loses Upward Momentum

Today, Germany's PMI data was released, according to Forex Factory:

→ German Flash Manufacturing PMI: actual = 42.6, expected = 40.7, previous = 40.6;

→ German Flash Services PMI: actual = 51.4, expected = 50.6, previous = 50.6.

The DAX 40 index (Germany 40 mini on FXOpen) showed a slight intraday increase, which could be viewed positively, especially given that last week, the index reached a yearly high.

However, the chart for the DAX 40 (Germany 40 mini on FXOpen) shows signs of the upward momentum slowing:

→ The RSI indicator is showing bearish divergence;

→ Price fluctuations are forming a triangle that could turn into a bearish reversal pattern known as a Bearish Rising Wedge (marked by black lines).

If a bearish break below the lower black line occurs, it might indicate that the bulls failed to maintain the momentum above the blue channel, within which the DAX 40 index had fluctuated for most of 2024.

Thus, a potential pullback towards the psychological level of 19,000 should not be ruled out.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

UK PMI composite hits 11-month low as business confidence wavers

UK business activity weakened in October, with both the manufacturing and services sectors showing signs of slowing momentum. PMI Manufacturing index dropped from 51.5 to 50.3, marking a 6-month low, while PMI Services index fell from 52.4 to 51.8, an 11-month low. Consequently, Composite PMI also declined to an 11-month low, slipping from 52.6 to 51.7.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, attributed this slump to "gloomy government rhetoric" and rising uncertainty ahead of the Budget. He added that external risks, such as conflicts in the Middle East, the ongoing war in Ukraine, and the upcoming US elections, have further dampened economic confidence.

The early PMI data suggests that the UK economy grew at a meagre 0.1% quarterly rate in October. However, Williamson noted that further cooling of input cost inflation, now at its lowest level in four years, could allow BoE to take a "more aggressive stance" toward rate cuts if the economic slowdown persists.

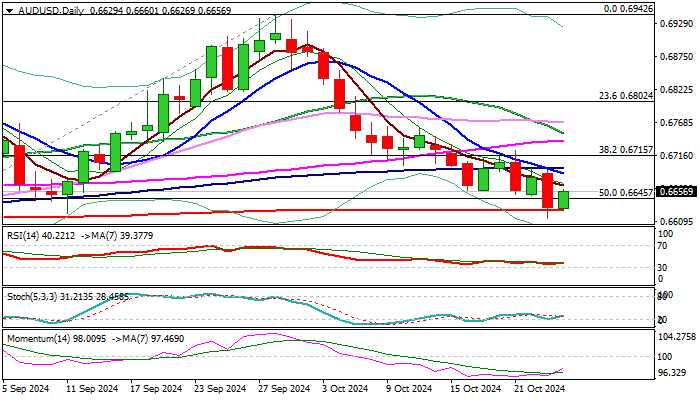

AUD/USD Outlook: Bears Take a Breather

AUDUSD edges higher on Thursday morning after bears repeatedly failed to clear 200DMA support (0.6627).

Recovery is in its early stage and needs more work at the upside to generate firmer positive signal, although near-term action to remain constructive while above 200DMA.

Repeated daily close above here to boost hopes of stronger recovery and Friday’s close above 200DMA to complete a bear-trap on weekly chart and open more prospects for stronger bounce however, 100DMA (0.6794) and daily Ichimoku cloud top (0.6707) mark strong barriers where potential recovery rally may face strong headwinds.

Daily studies remain bearishly aligned (MA’s in predominantly bearish setup and north heading 14-d momentum is still deeply in negative territory) which contributes to scenario of limited correction before larger bears regain control.

Look for firmer direction signals on break of either boundary of daily Ichimoku cloud (base at 0.6593 and top at 0.6707).

Res: 0.6670; 0.6694; 0.6707; 0.6739.

Sup: 0.6627; 0.6593; 0.6575; 0.6563.

Eurozone PMIs: Persistent price pressures lean ECB toward 25bps Dec cut, not 50bps

Eurozone's economic activity showed mixed signals in October, with PMI Manufacturing rising slightly from 45.0 to 45.9, while PMI Services fell marginally from 51.4 to 51.2. As a result, Composite PMI ticked up slightly to 49.7 from 49.6, but remained below the 50-point mark, indicating ongoing economic contraction.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, described the Eurozone as "stuck in a bit of a rut," noting that the economy contracted for the second consecutive month. While the manufacturing sector continues to slump, its negative impact is being balanced out by minor gains in services. De la Rubia added, "For now, it is not clear whether we will see a further deterioration or an improvement in the near future."

According to de la Rubia, for ECB, the data present an "unwelcome surprise," particularly in the services sector. Inflationary pressures appear to be lingering, driven by wage growth, which has been pushing up costs and selling prices for service providers.

This persistent inflation suggests that the ECB may lean towards a 25bps rate cut in December, as opposed to the larger 50bps cut some had speculated.

Germany’s PMI offers slight relief, but structural weaknesses persist

Germany's economic outlook improved slightly in October, as PMI Manufacturing index rose to 42.6 from 40.6, while PMI Services climbed to 51.4 from 50.6. This led to a rise in Composite PMI to 48.4 from 47.5, offering some hope for the start of Q4.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, highlighted that the start to Q4 is "better than expected." With manufacturing shrinking at a slower rate and services expanding more quickly, he noted that growth in Q3 is a "distinctive possibility."

However, despite these improvements, Germany's GDP is still forecast to remain flat for the year, following a 0.3% contraction in 2023, as projected by the International Monetary Fund.

De la Rubia also pointed to the "structural weaknesses" weighing down the German economy. Key issues such as high energy costs, rising competition from China, and ongoing labor market shortages are continuing to strain the manufacturing sector.