Sample Category Title

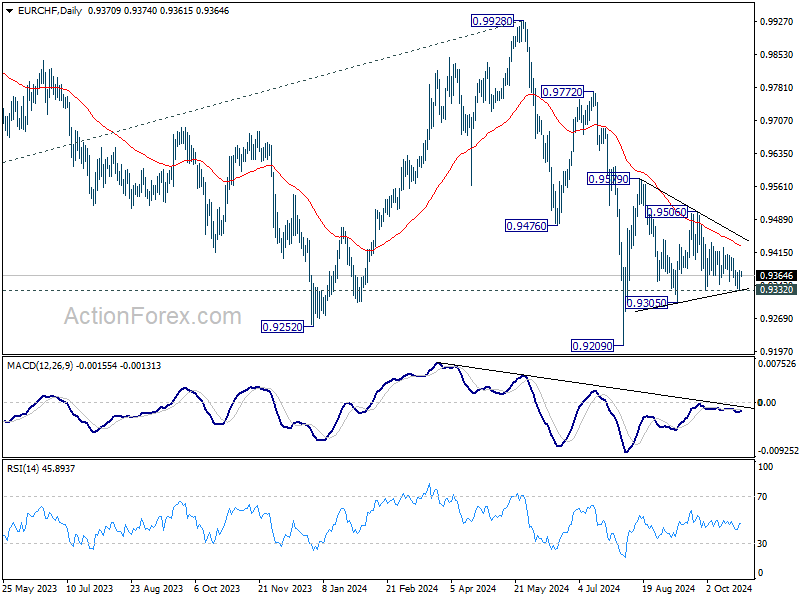

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9346; (P) 0.9362; (R1) 0.9390; More....

EUR/CHF recovered after drawing support from 0.9332 and intraday bias remains neutral. On the downside, firm break of 0.9332 resume the fall from 0.9579 towards 0.9209, and argue that larger down trend might be ready to resume too. On the upside, though, break of 0.9506 will turn intraday bias to the upside for 0.9579 resistance and above.

In the bigger picture, fall from 0.9928 is seen as part of the long term down trend. Repeated rejection by 55 D EMA (now at 0.9427) keeps outlook bearish for breaking through 0.9209 low at a later stage. Nevertheless, sustained trading above 55 D EMA will confirm medium term bottoming and bring stronger rebound back towards 0.9928 key resistance.

EUR/USD 1.0778 Lives to Fight Another Day

Markets

EUR/USD 1.0778 lives to fight another day. The technical support level survived October PMI surveys. Disappointing French numbers forced a test early on European dealings, but a better German reading and a close to consensus EMU gauge (2nd consecutive month below neutral 50-level though) balanced things out. Investors took it as a first sign to stop adding to ECB policy rate cut bets for now. The market implied probability of an acceleration to a 50 bps rate cut in December stands at 33% with the deposit rate expected to dip below the 2% neutral level in H2 2025. We continue to find this path too aggressive. The ECB’s monthly consumer survey offers a second piece of information today via inflation expectations (1y & 3y forward). Both remain stuck above the central bank’s 2% inflation target, respectively at 2.7% and 2.3%, but are gradually grinding lower. We doubt they’ll be gamechangers though. Next week will be more interesting with Q3 GDP data and October inflation figures. Over summer, there’s been a discrepancy between very bad EMU sentiment data and less bad hard numbers. The PMI-based nowcast hints at flat GDP growth in Q3, but the actual number could reach 0.2% Q/Q or even 0.3% Q/Q. Such reality check could also slow or even partly reverse trends set in motion in the wake of last week’s policy rate cut. Inflation is equally set to undo September’s dip below the 2% inflation target as base effects will push CPI higher going into year-end. When the spotlight turns away from euro weakness, it will take dollar strength to pull EUR/USD below 1.0778. The greenback had a stellar run since the start of the month, both driven by US data outperformance and by Trump’s solid polling going into presidential elections. Yesterday’s good eco figures (declining jobless claims and solid (services) PMI couldn’t inspire dollar bulls though in a sign that the greenback could shift into lower gear as we approach the combination of payrolls (Nov 1), elections (Nov 5) and Fed meeting (Nov 7). US durable goods orders are today’s only highlight on the US agenda.

News & Views

Inflation in Japan’s capital city Tokyo eased from 2.1% to 1.8% in October. Energy was the main driving force behind the deceleration. Government subsidies for energy costs shaved about half a percentage point from the overall index. This also caused a slowdown in the gauge excluding fresh food from 2% to 1.8%. An even narrower gauge (ex. fresh food and energy) actually unexpectedly accelerated from 1.6% to 1.8%. The monthly 0.6% pace was the quickest in over a year. Services inflation edged up from 0.6% to 0.8%, led by price rises in public services. Price developments in the public sector are seen as more rigid than in the private sector, suggesting the wage-price spiral is materializing in that part of the economy too. The Tokyo indicator points at continued underlying inflationary momentum and is considered a good indicator of where the national trend is headed. That should trigger further hikes by the Bank of Japan, though not at next week’s October 31 meeting. Its governor Ueda in the sidelines of the IMF and World bank annual meetings yesterday said the central bank has time to consider its next steps. That makes December the earliest candidate for a third rate hike (by 25 bps this time?) this cycle. The Japanese yen trades a tad stronger this morning at USD/JPY 151.6 as it heads into Japanese general elections on Sunday. The ruling LDP risks losing its majority for the first time since 2009.

UK GfK consumer confidence eased to the lows seen earlier this year. The indicator fell from -20 to -21 in October with households becoming gloomier on the broader economic outlook despite seeing an improvement in their personal finances on dropping inflation. The back-to-back decline was an extension to last months’ steep 7 point drop which GfK attributed to speculation about the tax and spending plans in the Chancellor’s upcoming Budget statement (October 30). UK consumers’ saving intentions picked up from 23 to 27. The GfK’s major purchase gauge improved slightly but remains at a relatively low level nonetheless.

Divergence Between Euro and US Dollar Outlook

Major stock indices across Europe and US were up on Thursday, after a few good-looking earnings across both continents including Hermes, Barclays, Unilever and Renault in Europe and Tesla and UPS in the US, gave a smile to investors after three cloudy sessions. The S&P500 gained 0.21% while Nasdaq 100 rebounded 0.83%. Tesla jumped almost 22% - its best session in 11 years. The DAX advanced 0.34% and the Stoxx 600 index closed near flat. Even Kering’s shares – the troubled company that owns Gucci – saw its shares jump 1.42% yesterday despite the fact that the company warned that its profit this year will fall to the lowest levels since 2016 due to the weak Chinese demand. Elsewhere, the Korean SK Hynix released satisfactory results for its investors and added to the optimism that the AI demand remains robust and Roundhill’s Magnificent 7 ETF gained more than 3%.

Overall, the earnings season is going well in the US, less well in Europe. The latter also matches the macroeconomic news where data is strong in the US, and much less in Europe. In this context, yesterday’s PMI figures showed that contraction in mainland Europe continued, even though the deterioration in Germany was less severe than expected in October, while France saw its manufacturing and services sector contract faster. The latest PMI numbers, combined with weakness in earnings and dovish remarks from the European Central Bank (ECB) members, brought some investors to start betting that the ECB would accelerate the size of its rate cuts in the foreseeable future. There is now a small but a rising possibility of a 50bp cut from the ECB in its December meeting. And the EZ’s below 2% headline inflation could convince many ECB members that it’s time to take a risk.

As such, the euro should remain under pressure. The EURUSD rebounded yesterday on the back of a broad-based US dollar weakness that, by the way, came to play despite stronger-than-expected housing and PMI data, and softer-than-expected jobless claims hinting that the dollar’s move yesterday was certainly a consolidation and correction and isn’t backed by fundamentals.

The divergence between the euro and US dollar outlook, the view that Trump’s potential return to the US White House could worsen the trade relations between the two continents and the sustained gap between the German and French 10-year yields (due to worries about France’s ability to strengthen its finances amid political turmoil) remain supportive of a further decline in the EURUSD. The pair should see resistance into 1.0870, the minor 23.6% Fibonacci retracement on the latest selloff. Key resistance to the actual bearish trend sits at 1.0935 – the major 38.2% Fibonacci retracement.

The single currency is however better bid against the British pound that’s also under pressure these days, as the Bank of England (BoE) Governor Bailey sounds unusually dovish regarding the policy of his bank, and overly confident that inflation will be slowing faster than the policymakers once thought. As such, Cable will likely close the week below the 1.30 mark, very close to the major 38.2% Fibonacci retracement on April to September rally, and walk into next week’s Budget in the bearish consolidation zone. As per the budget, there will certainly be difficult-to-digest announcements for UK companies and wealthy individuals next week. And the tighter the budget, the more supportive the BoE should be... if inflation allows.

In Japan, the yen is better bid but the USDJPY consolidates gains above the 150 level and the risks remain tilted to the upside into the election weekend, which could see the country’s ruling party lose its majority in the lower parliament for the first time since 2009. The latter would be bad for both the yen and the Japanese stocks. Moreover, the Bank of Japan (BoJ) Governor Ueda aligned with the expectations that the bank would not hike rates at its next week’s policy meeting. Therefore, the yen risks remain tilted to the downside, dipbuyers in the USDJPY are waiting in ambush near the 150 level and a direct FX intervention may not be on the menu before the 160s range.

Finally in energy, US crude made an attempt to clear the 50-DMA – a touch lower than the $72pb level – yesterday but the 5.5-mio barrel build in US inventories last week capped the upside potential near this important technical level. While oil bulls may not be in peak form lately, risks tend to lean to the upside heading into weekends due to the potential for an escalation in the Middle East conflict. Therefore, selling oil below the $70pb level doesn’t look safe.

Weak PMIs Keep ECB Jumbo Cut Speculation Alive

In focus today and over the weekend

Today, focus turns to the German Ifo growth indicator for October. The Ifo survey is more extensive than the PMIs and it will be very interesting to see if it mirrors the recent uptick observed in the PMIs yesterday.

In the euro area, September data on credit growth and money supply is published today. Credit growth has started to rebound, and the latest ECB bank lending survey showed increased demand for lending as well as unchanged credit conditions in Q3.

In Japan, all eyes are on Sunday's general election. Polls have indicated the ruling coalition is in danger of losing its Lower House majority, after a slush fund scandal forced the previous prime minister out. Changes in the political scene could impact the backing for further BoJ rate hikes. We still look for another rate hike in December or January.

Economic and market news

What happened overnight

In Japan, CPI Tokyo Ex-Fresh Food declined to 1.8% (cons: 1.7%, prior: 2.0%), undershooting the BoJ's 2% target for the first time since May.

What happened yesterday

In the euro area, October flash PMIs came in at: Composite at 49.7 (cons: 49.7, prior: 49.6), services at 51.2 (cons: 51.5, prior: 51.4) and manufacturing at 45.9 (cons: 45.1, prior: 45.0). Overall, the data shows that the growth momentum in the euro area remains fragile at the start of Q4 with PMIs suggesting stagnation. Looking ahead, we expect growth to remain weak in the final quarter of the year, but we still expect positive support by services activity amid a decent labour market, rising real incomes and diminishing headwinds from falling interest rates.

For the first time in four years, employment numbers in the service sector have decreased for Germany and France. Signs of labour market softening and subdued economic growth, pave the way for lower interest rates. Currently, the ECB is set to lower interest rates in December with traders pricing in a 43% chance of a 50bp rate cut. For that to happen, we anticipate a significant deterioration in key metrics to be required. Before the next rate meeting data on inflation, wages and another round of PMIs could change the economic outlook.

ECB policymakers Martins Kazaks (hawk) and Bostjan Vasle (hawk) advocated for a step-by-step approach to cutting rates, as weakness in the euro zone is 'single biggest concern' despite domestic price pressures continuing to remain 'sticky', US election worries and energy price risks. ECB's Nagel (hawk) followed by saying that the ECB should not be hasty but cautious about lowering interest rates.

In the US, flash PMIs edged up beating expectations: Composite at 54.3 (cons: 53.8, prior: 54.0), services at 55.3 (cons: 55.0, prior: 55.2) and manufacturing at 47.8 (cons: 47.5, prior: 47.3). In total, the indicators point towards robust growth with manufacturing likely past the bottom.

Fed policymaker Beth Hammack (voting member) echoed the words of Fed Chairman Jerome Powell, acknowledging the impact of previous rate hikes on reducing inflation but noting that it has not yet fallen to the 2% target.

New home sales reached the highest level in 1.5 years of 738,000 (cons: 720,000, prior: 716,000), climbing 4.1% following the fall in mortgage rates last month as the Fed began cutting interest rates. In recent weeks mortgage rates have climbed as expectations for another 50bp cut from the Fed have diminished following solid US economic data.

In the UK, preliminary PMIs for October surprise to the downside: Composite at 51.7 (cons: 52.5, prior: 52.6), services at 51.8 (cons: 52.4, prior: 52.4) and manufacturing at 50.3 (cons: 51.5, prior: 51.5). Overall, the PMIs point to a more muted growth outlook for the rest of the year and should put the domestic demand worries at the BoE to a slight ease, ahead of the much-anticipated UK budget release.

FI: The October euro area PMIs came out in line with expectations, though markets interpreted the details as renewed signs of disinflation. Euro swap curves declined from the back with the 10Y tenor closing 5bp lower. Pricing of the ECB December meeting still stands at -35bp with another -35bp priced in January. The short end of the market remains highly responsive to any ECB commentary regarding the possibility of a significant rate cut in December. Yesterday, even typically hawkish members such as Kazaks and Wunsch seemed a bit hesitant to dismiss the potential for a 'jumbo' cut. Peripheral spreads tightened, while the Bund ASW-spread was close to unchanged at 16.7bp.

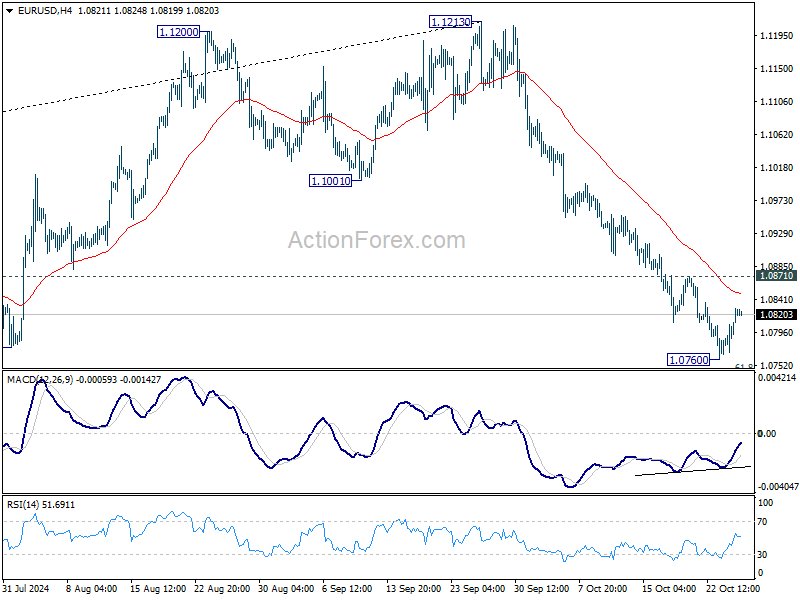

FX: The USD rally lost steam yesterday when NOK, JPY and EUR came out on top among G10 currencies. EUR/USD rose above 1.08 and USD/JPY fell below 152. EUR/NOK briefly dropped to 11.80-level.

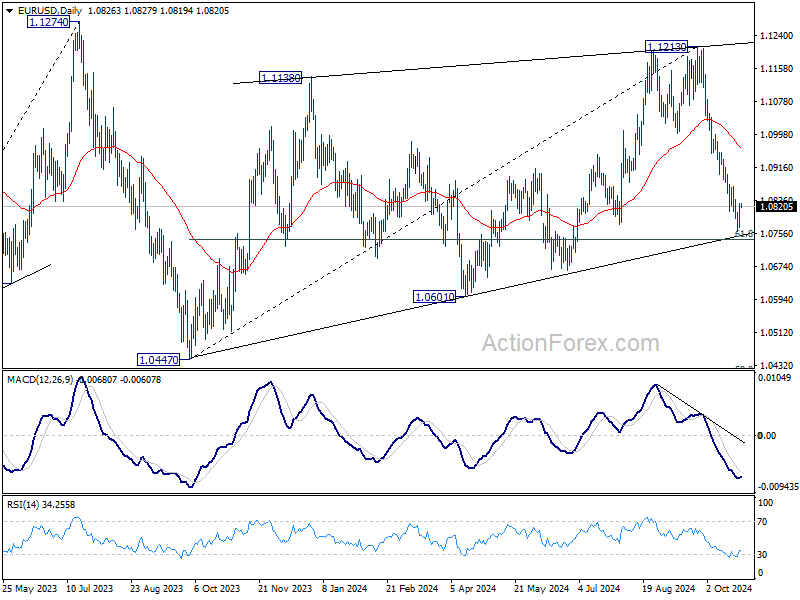

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0789; (P) 1.0810; (R1) 1.0848; More...

Intraday bias in EUR/USD is turned neutral with a temporary low formed at 1.0760. Further decline is expected as long as 1.0871 resistance holds. Below 1.0760 will resume the fall from 1.1213 to 1.0601 support next. However, considering bullish convergence condition in 4H MACD, break of 1.0871 will indicate short term bottoming, and turn bias back to the upside for 55 D EMA (now at 1.0963).

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

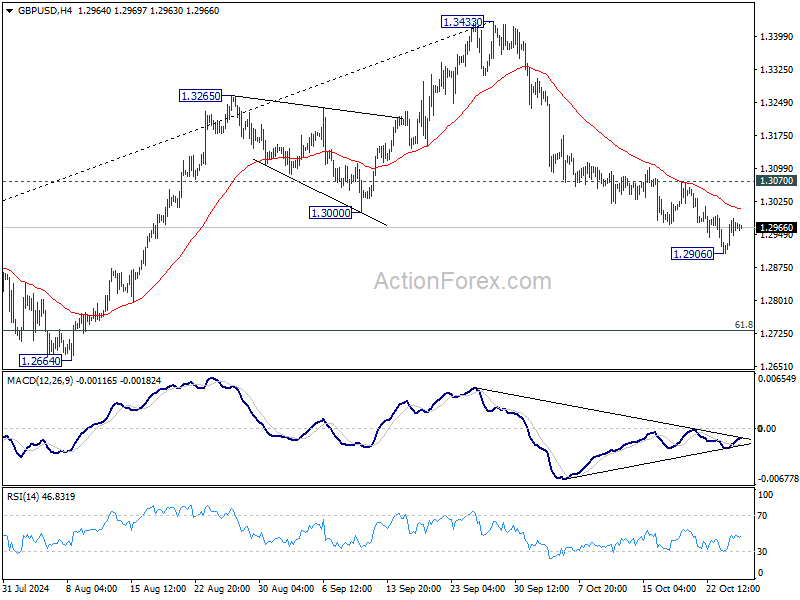

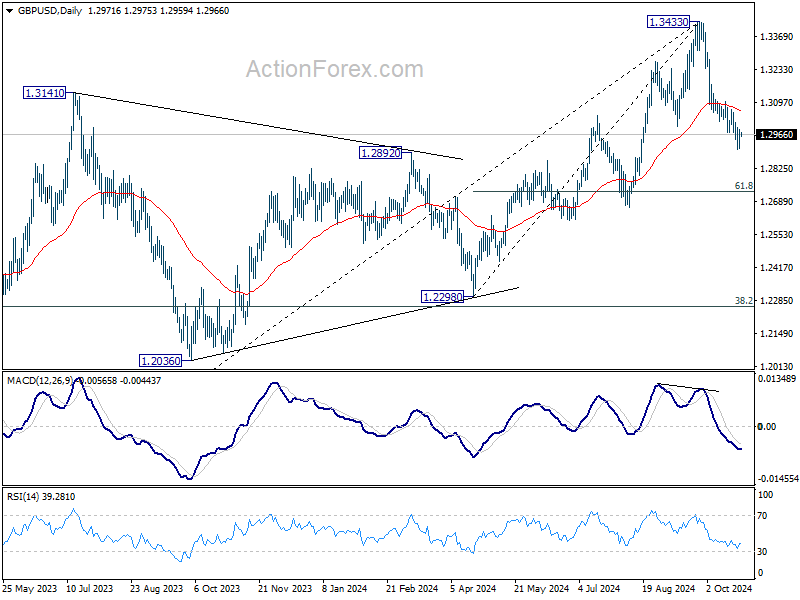

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2928; (P) 1.2958; (R1) 1.3007; More...

Intraday bias in GBP/USD is turned neutral with a temporary low formed at 1.2906. Further decline is expected as long as 1.3070 resistance holds. Below 1.2906 will resume the fall from 1.3433 to 61.8% retracement of 1.2298 to 1.3433 at 1.2732. However, considering bearish divergence condition in 4H MACD, firm break 1.3070 resistance will indicate short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, considering mildly bearish divergence condition in D MACD, a medium term top is likely in place at 1.3433 already. Price actions from there are seen as correction to whole up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

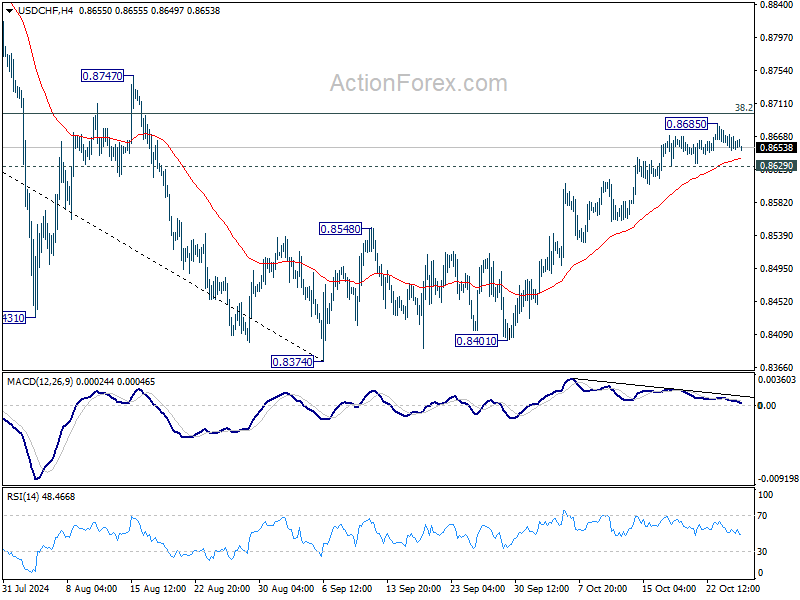

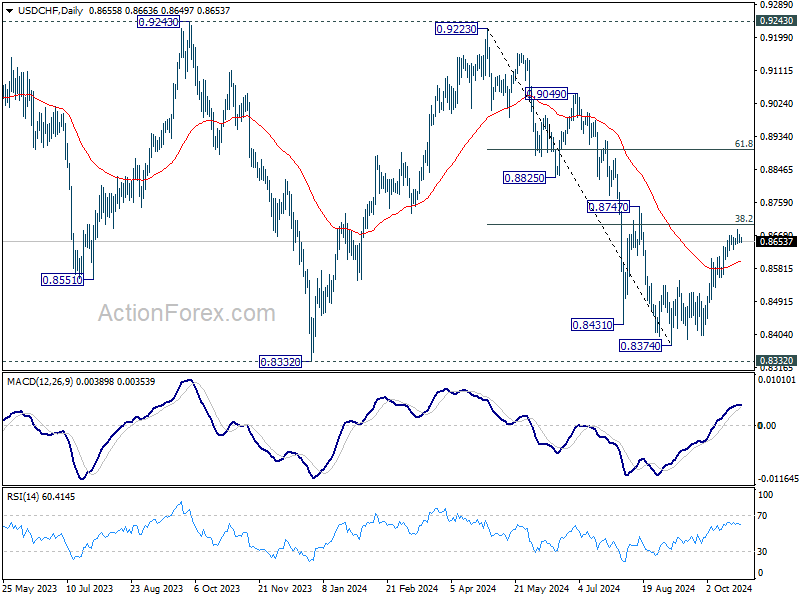

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8646; (P) 0.8662; (R1) 0.8674; More…

Intraday bias in USD/CHF is turned neutral as a temporary top is formed at 0.8685, ahead of 38.2% retracement of 0.9223 to 0.8374 at 0.8698. Considering bearish divergence condition in 4H MACD, firm break of 0.8629 support will indicate short term topping, and turn bias back to the downside for 55 D EMA (now at 0.8601). Nevertheless, sustained break of 0.8698 will argue that fall from 0.9223 has completed at 0.8374, after defending 0.8332 low. Further rally should then be seen to 61.8% retracement at 0.8899 next.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

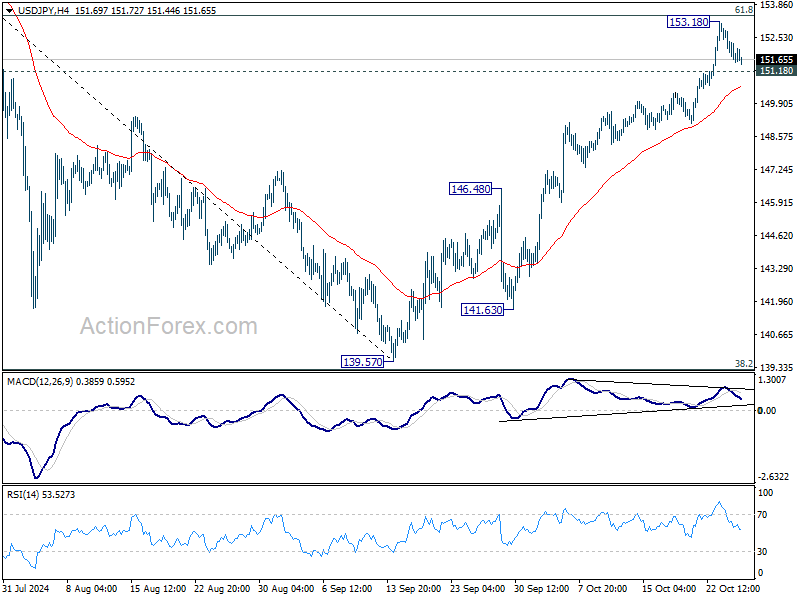

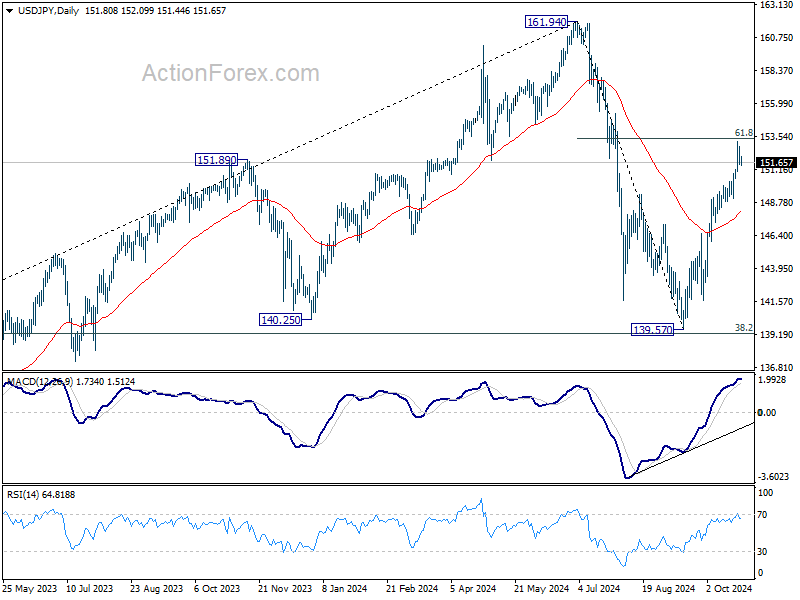

USD/JPY Daily Outlook

Daily Pivots: (S1) 151.30; (P) 152.07; (R1) 152.58; More...

Intraday bias in USD/JPY is turned neutral as a temporary top was formed at 153.17, ahead of 61.8% retracement of 161.94 to 139.57 at 153.39. Considering bearish divergence condition in 4H MACD, break of 151.18 will indicate short term topping, and turn bias to the downside for 55 D EMA (now at 148.01). Nevertheless, decisive break of 153.39 will extend the rally from 139.57 to retest 161.94 high.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

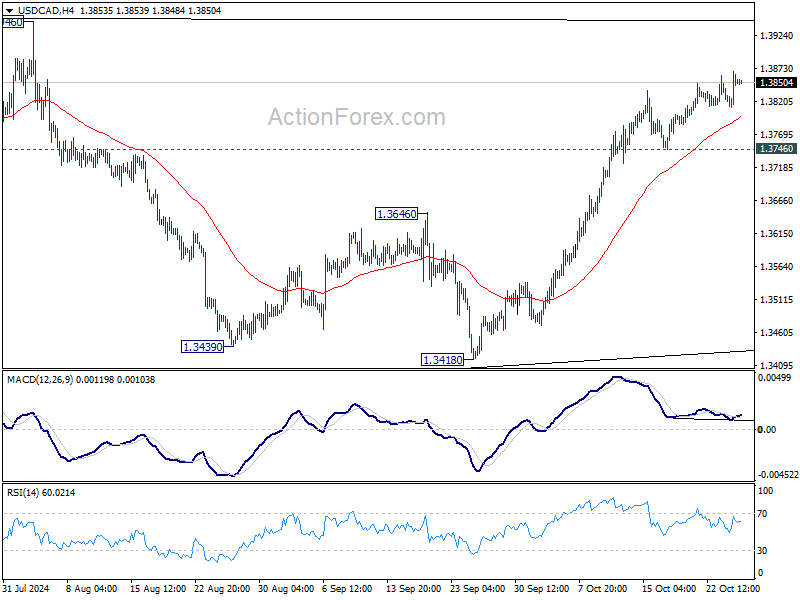

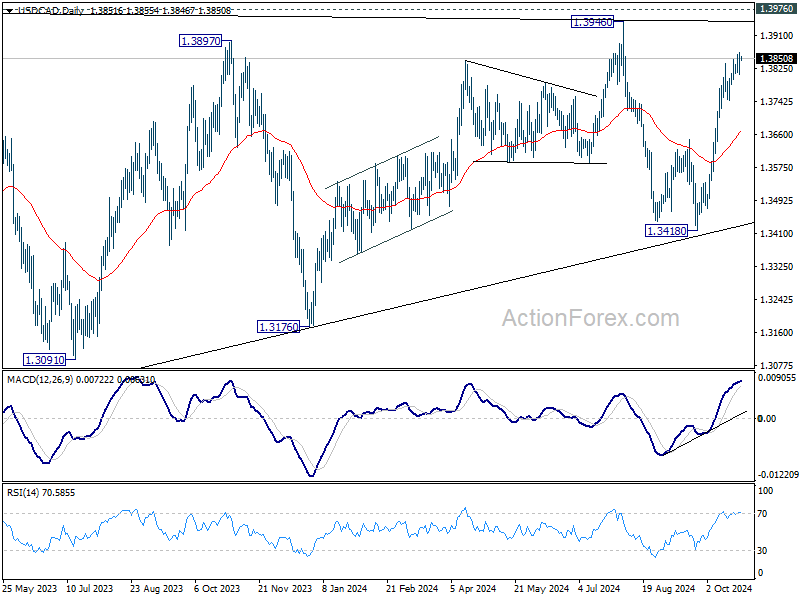

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3823; (P) 1.3846; (R1) 1.3879; More...

Intraday bias in USD/CAD stays on the upside at this point. Current rally from 1.3418 is in progress for retesting 1.3946/76 key resistance zone. Strong resistance might be seen there to limit upside. On the downside, break of 1.3746 support is needed to indicate short term topping, or another rise is in favor in case of retreat.

In the bigger picture, sideway consolidation pattern from 1.3976 (2022 high) might still extend further. While another decline cannot be ruled out, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage.

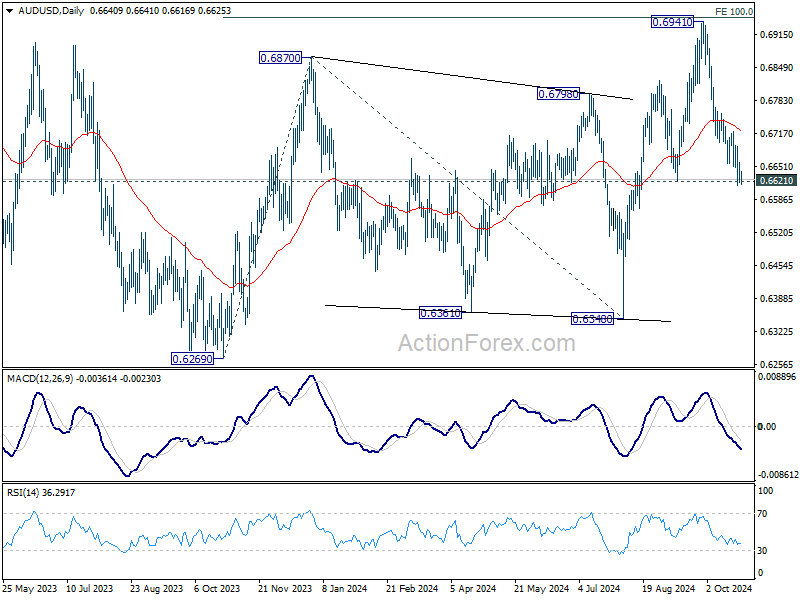

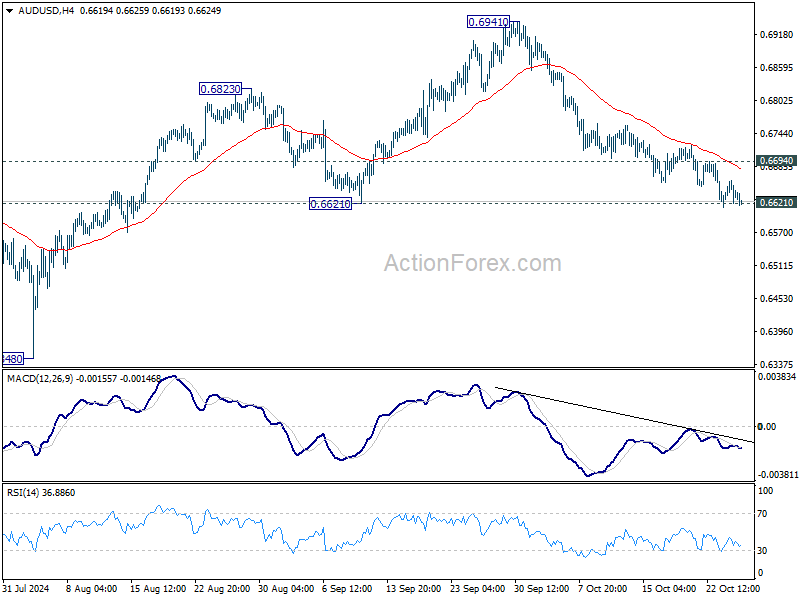

AUD/USD Daily Report

Daily Pivots: (S1) 0.6620; (P) 0.6641; (R1) 0.6660; More...

Intraday bias in AUD/USD remains on the downside for the moment. Firm break of 0.6621 support should confirm near term bearish reversal after topping at 0.6941. Deeper decline should then be seen to 0.6348 support next. On the upside, above 0.6694 minor resistance will turn intraday bias neutral first.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 100% projection of 0.6269 to 0.6870 from 0.6340 at 0.6941 will target 138.2% projection at 0.7179. However, sustained break of 0.6621 support will argue that rise from 0.6269 has completed and bring deeper fall back to 0.6269/6348 support zone.