Sample Category Title

Summary 10/28 – 11/1

Monday, Oct 28, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 14:30 | USD | Dallas Fed Manufacturing Business Index Oct | -9 | |

| 17:30 | CAD | BoC's Governor Macklem speech | ||

| 23:30 | JPY | Unemployment Rate Sep | 2.50% | 2.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 14:30 | USD | Dallas Fed Manufacturing Business Index Oct | |

| Forecast: | Previous: -9 | ||

| 17:30 | CAD | BoC's Governor Macklem speech | |

| Forecast: | Previous: | ||

| 23:30 | JPY | Unemployment Rate Sep | |

| Forecast: 2.50% | Previous: 2.50% | ||

Tuesday, Oct 29, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 07:00 | EUR | Germany GfK Consumer Sentiment Nov | -20.5 | -21.2 |

| 09:30 | GBP | Mortgage Approvals Sep | 64K | 65K |

| 09:30 | GBP | M4 Money Supply M/M Sep | 0.10% | -0.10% |

| 12:30 | USD | Goods Trade Balance (USD) Sep P | -96.1B | -94.3B |

| 12:30 | USD | Wholesale Inventories Sep P | 0.20% | 0.10% |

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Aug | 6.00% | 5.90% |

| 13:00 | USD | Housing Price Index M/M Aug | 0.20% | 0.10% |

| 14:00 | USD | Consumer Confidence Oct | 98.9 | 98.7 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 07:00 | EUR | Germany GfK Consumer Sentiment Nov | |

| Forecast: -20.5 | Previous: -21.2 | ||

| 09:30 | GBP | Mortgage Approvals Sep | |

| Forecast: 64K | Previous: 65K | ||

| 09:30 | GBP | M4 Money Supply M/M Sep | |

| Forecast: 0.10% | Previous: -0.10% | ||

| 12:30 | USD | Goods Trade Balance (USD) Sep P | |

| Forecast: -96.1B | Previous: -94.3B | ||

| 12:30 | USD | Wholesale Inventories Sep P | |

| Forecast: 0.20% | Previous: 0.10% | ||

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y Aug | |

| Forecast: 6.00% | Previous: 5.90% | ||

| 13:00 | USD | Housing Price Index M/M Aug | |

| Forecast: 0.20% | Previous: 0.10% | ||

| 14:00 | USD | Consumer Confidence Oct | |

| Forecast: 98.9 | Previous: 98.7 | ||

Wednesday, Oct 30 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Sep | 2.50% | 2.70% |

| 00:30 | AUD | CPI Q/Q Q3 | 0.30% | 1.00% |

| 00:30 | AUD | CPI Y/Y Q3 | 2.90% | 3.80% |

| 00:30 | AUD | RBA Trimmed Mean CPI Q/Q Q3 | 0.70% | 0.80% |

| 00:30 | AUD | RBA Trimmed Mean CPI Y/Y Q3 | 3.50% | 3.90% |

| 05:00 | JPY | Consumer Confidence Oct | 36.8 | 36.9 |

| 06:30 | EUR | France Consumer Spending M/M Sep | 0.30% | 0.20% |

| 08:00 | CHF | KOF Economic Barometer Oct | 105.0 | 105.5 |

| 08:55 | EUR | Germany Unemployment Change Oct | 18K | 17K |

| 08:55 | EUR | Germany Unemployment Rate Oct | 6.10% | 6.00% |

| 09:00 | CHF | UBS Economic Expectations Oct | -8.8 | |

| 09:00 | EUR | Italy GDP Q/Q Q3 P | 0.20% | 0.20% |

| 09:00 | EUR | Germany GDP Q/Q Q3 P | -0.10% | -0.10% |

| 10:00 | EUR | Eurozone GDP Q/Q Q3 P | 0.20% | 0.20% |

| 10:00 | EUR | Eurozone Economic Sentiment Oct | 96.4 | 96.2 |

| 10:00 | EUR | Eurozone Industrial Confidence Oct | -10.5 | -10.9 |

| 10:00 | EUR | Eurozone Services Sentiment Oct | 6.7 | |

| 10:00 | EUR | Eurozone Consumer Confidence Oct F | -12.5 | -12.5 |

| 12:15 | USD | ADP Employment Change Oct | 110K | 143K |

| 12:30 | USD | GDP Annualized Q3 P | 3.00% | 3.00% |

| 12:30 | USD | GDP Price Index Q3 P | 2.70% | 2.50% |

| 13:00 | EUR | Germany CPI M/M Oct P | 0.20% | 0.00% |

| 13:00 | EUR | Germany CPI Y/Y Oct P | 1.80% | 1.60% |

| 14:00 | USD | Pending Home Sales M/M Sep | 0.60% | |

| 14:30 | USD | Crude Oil Inventories | 5.5M | |

| 23:50 | JPY | Industrial Production M/M Sep P | 0.80% | -3.30% |

| 23:50 | JPY | Retail Trade Y/Y Sep | 2.30% | 2.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Monthly CPI Y/Y Sep | |

| Forecast: 2.50% | Previous: 2.70% | ||

| 00:30 | AUD | CPI Q/Q Q3 | |

| Forecast: 0.30% | Previous: 1.00% | ||

| 00:30 | AUD | CPI Y/Y Q3 | |

| Forecast: 2.90% | Previous: 3.80% | ||

| 00:30 | AUD | RBA Trimmed Mean CPI Q/Q Q3 | |

| Forecast: 0.70% | Previous: 0.80% | ||

| 00:30 | AUD | RBA Trimmed Mean CPI Y/Y Q3 | |

| Forecast: 3.50% | Previous: 3.90% | ||

| 05:00 | JPY | Consumer Confidence Oct | |

| Forecast: 36.8 | Previous: 36.9 | ||

| 06:30 | EUR | France Consumer Spending M/M Sep | |

| Forecast: 0.30% | Previous: 0.20% | ||

| 08:00 | CHF | KOF Economic Barometer Oct | |

| Forecast: 105.0 | Previous: 105.5 | ||

| 08:55 | EUR | Germany Unemployment Change Oct | |

| Forecast: 18K | Previous: 17K | ||

| 08:55 | EUR | Germany Unemployment Rate Oct | |

| Forecast: 6.10% | Previous: 6.00% | ||

| 09:00 | CHF | UBS Economic Expectations Oct | |

| Forecast: | Previous: -8.8 | ||

| 09:00 | EUR | Italy GDP Q/Q Q3 P | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 09:00 | EUR | Germany GDP Q/Q Q3 P | |

| Forecast: -0.10% | Previous: -0.10% | ||

| 10:00 | EUR | Eurozone GDP Q/Q Q3 P | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 10:00 | EUR | Eurozone Economic Sentiment Oct | |

| Forecast: 96.4 | Previous: 96.2 | ||

| 10:00 | EUR | Eurozone Industrial Confidence Oct | |

| Forecast: -10.5 | Previous: -10.9 | ||

| 10:00 | EUR | Eurozone Services Sentiment Oct | |

| Forecast: | Previous: 6.7 | ||

| 10:00 | EUR | Eurozone Consumer Confidence Oct F | |

| Forecast: -12.5 | Previous: -12.5 | ||

| 12:15 | USD | ADP Employment Change Oct | |

| Forecast: 110K | Previous: 143K | ||

| 12:30 | USD | GDP Annualized Q3 P | |

| Forecast: 3.00% | Previous: 3.00% | ||

| 12:30 | USD | GDP Price Index Q3 P | |

| Forecast: 2.70% | Previous: 2.50% | ||

| 13:00 | EUR | Germany CPI M/M Oct P | |

| Forecast: 0.20% | Previous: 0.00% | ||

| 13:00 | EUR | Germany CPI Y/Y Oct P | |

| Forecast: 1.80% | Previous: 1.60% | ||

| 14:00 | USD | Pending Home Sales M/M Sep | |

| Forecast: | Previous: 0.60% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: 5.5M | ||

| 23:50 | JPY | Industrial Production M/M Sep P | |

| Forecast: 0.80% | Previous: -3.30% | ||

| 23:50 | JPY | Retail Trade Y/Y Sep | |

| Forecast: 2.30% | Previous: 2.80% | ||

Thursday, Oct 31, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| JPY | BoJ Interest Rate Decision | 0.25% | ||

| 00:00 | NZD | ANZ Business Confidence Oct | 60.9 | |

| 00:30 | AUD | Retail Sales M/M Sep | 0.40% | 0.70% |

| 00:30 | AUD | Private Sector Credit M/M Sep | 0.50% | 0.50% |

| 00:30 | AUD | Import Price Index Q/Q Q3 | 1% | |

| 00:30 | AUD | Building Permits M/M Sep | 2.20% | -6.10% |

| 01:30 | CNY | NBS Manufacturing PMI Oct | 50.1 | 49.8 |

| 01:30 | CNY | NBS Non-Manufacturing PMI Oct | 50.5 | 50 |

| 05:00 | JPY | Housing Starts Y/Y Sep | -4.10% | -5.10% |

| 07:00 | EUR | Germany Import Price Index M/M Sep | -0.40% | -0.40% |

| 07:00 | EUR | Germany Retail Sales M/M Sep | -0.50% | 1.60% |

| 09:00 | EUR | ECB Economic Bulletin | ||

| 10:00 | EUR | Eurozone Unemployment Rate Sep | 6.40% | 6.40% |

| 10:00 | EUR | Eurozone CPI Y/Y Oct P | 1.90% | 1.70% |

| 10:00 | EUR | Eurozone CPI Core Y/Y Oct P | 2.60% | 2.70% |

| 11:30 | USD | Challenger Job Cuts Y/Y Oct | 53.40% | |

| 12:30 | CAD | GDP M/M Aug | 0.10% | 0.20% |

| 12:30 | USD | Initial Jobless Claims (Oct 25) | 231K | 227K |

| 12:30 | USD | Personal Income M/M Sep | 0.40% | 0.20% |

| 12:30 | USD | Personal Spending Sep | 0.40% | 0.20% |

| 12:30 | USD | PCE Price Index M/M Sep | 0.10% | |

| 12:30 | USD | PCE Price Index Y/Y Sep | 2.20% | |

| 12:30 | USD | Core PCE Price Index M/M Sep | 0.30% | 0.10% |

| 12:30 | USD | Core PCE Price Index Y/Y Sep | 2.70% | |

| 12:30 | USD | Employment Cost Index Q3 | 0.90% | 0.90% |

| 13:45 | USD | Chicago PMI Oct | 48.2 | 46.6 |

| 14:30 | USD | Natural Gas Storage | 80B | |

| 21:45 | NZD | Building Permits M/M Sep | -5.30% |

| GMT | Ccy | Events | |

|---|---|---|---|

| JPY | BoJ Interest Rate Decision | ||

| Forecast: | Previous: 0.25% | ||

| 00:00 | NZD | ANZ Business Confidence Oct | |

| Forecast: | Previous: 60.9 | ||

| 00:30 | AUD | Retail Sales M/M Sep | |

| Forecast: 0.40% | Previous: 0.70% | ||

| 00:30 | AUD | Private Sector Credit M/M Sep | |

| Forecast: 0.50% | Previous: 0.50% | ||

| 00:30 | AUD | Import Price Index Q/Q Q3 | |

| Forecast: | Previous: 1% | ||

| 00:30 | AUD | Building Permits M/M Sep | |

| Forecast: 2.20% | Previous: -6.10% | ||

| 01:30 | CNY | NBS Manufacturing PMI Oct | |

| Forecast: 50.1 | Previous: 49.8 | ||

| 01:30 | CNY | NBS Non-Manufacturing PMI Oct | |

| Forecast: 50.5 | Previous: 50 | ||

| 05:00 | JPY | Housing Starts Y/Y Sep | |

| Forecast: -4.10% | Previous: -5.10% | ||

| 07:00 | EUR | Germany Import Price Index M/M Sep | |

| Forecast: -0.40% | Previous: -0.40% | ||

| 07:00 | EUR | Germany Retail Sales M/M Sep | |

| Forecast: -0.50% | Previous: 1.60% | ||

| 09:00 | EUR | ECB Economic Bulletin | |

| Forecast: | Previous: | ||

| 10:00 | EUR | Eurozone Unemployment Rate Sep | |

| Forecast: 6.40% | Previous: 6.40% | ||

| 10:00 | EUR | Eurozone CPI Y/Y Oct P | |

| Forecast: 1.90% | Previous: 1.70% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Oct P | |

| Forecast: 2.60% | Previous: 2.70% | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Oct | |

| Forecast: | Previous: 53.40% | ||

| 12:30 | CAD | GDP M/M Aug | |

| Forecast: 0.10% | Previous: 0.20% | ||

| 12:30 | USD | Initial Jobless Claims (Oct 25) | |

| Forecast: 231K | Previous: 227K | ||

| 12:30 | USD | Personal Income M/M Sep | |

| Forecast: 0.40% | Previous: 0.20% | ||

| 12:30 | USD | Personal Spending Sep | |

| Forecast: 0.40% | Previous: 0.20% | ||

| 12:30 | USD | PCE Price Index M/M Sep | |

| Forecast: | Previous: 0.10% | ||

| 12:30 | USD | PCE Price Index Y/Y Sep | |

| Forecast: | Previous: 2.20% | ||

| 12:30 | USD | Core PCE Price Index M/M Sep | |

| Forecast: 0.30% | Previous: 0.10% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Sep | |

| Forecast: | Previous: 2.70% | ||

| 12:30 | USD | Employment Cost Index Q3 | |

| Forecast: 0.90% | Previous: 0.90% | ||

| 13:45 | USD | Chicago PMI Oct | |

| Forecast: 48.2 | Previous: 46.6 | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 80B | ||

| 21:45 | NZD | Building Permits M/M Sep | |

| Forecast: | Previous: -5.30% | ||

Friday, Nov 1, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | PPI Q/Q Q3 | 0.70% | 1.00% |

| 00:30 | AUD | PPI Y/Y Q3 | 4.80% | |

| 00:30 | JPY | Manufacturing PMI Oct F | 49.0 | 49.0 |

| 01:45 | CNY | Caixin Manufacturing PMI Oct | 49.5 | 49.3 |

| 07:30 | CHF | Real Retail Sales Y/Y Sep | 2.50% | 3.20% |

| 07:30 | CHF | CPI M/M Oct | 0.00% | -0.30% |

| 07:30 | CHF | CPI Y/Y Oct | 0.80% | |

| 08:30 | CHF | Manufacturing PMI Oct | 49.5 | 49.9 |

| 09:30 | GBP | Manufacturing PMI Oct F | 50.3 | 50.3 |

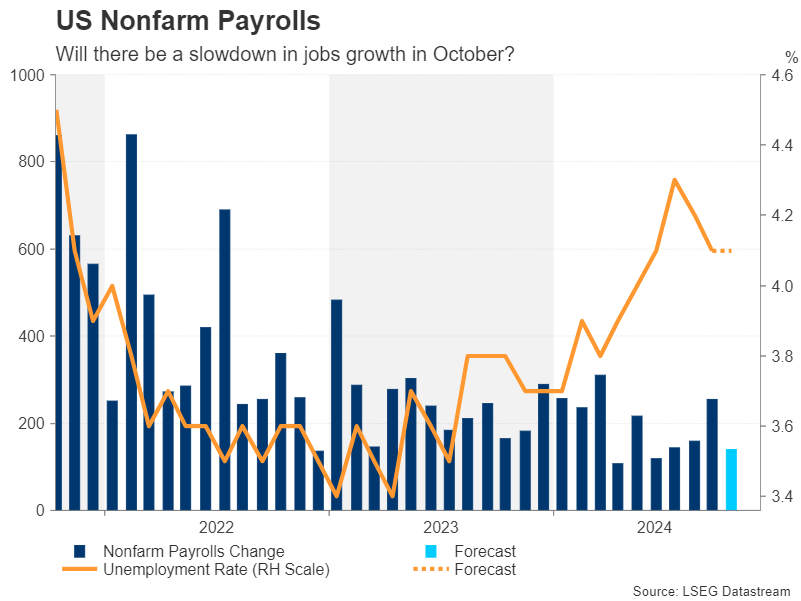

| 12:30 | USD | Nonfarm Payrolls Oct | 125K | 254K |

| 12:30 | USD | Unemployment Rate Oct | 4.10% | 4.10% |

| 12:30 | USD | Average Hourly Earnings M/M Oct | 0.30% | 0.40% |

| 13:30 | CAD | Manufacturing PMI Oct | 50.4 | |

| 13:45 | USD | Manufacturing PMI Oct F | 47.8 | 47.8 |

| 14:00 | USD | ISM Manufacturing PMI Oct | 47.6 | 47.2 |

| 14:00 | USD | ISM Manufacturing Prices Paid Oct | 48.3 | |

| 14:00 | USD | ISM Manufacturing Employment Index Oct | 43.9 | |

| 14:00 | USD | Construction Spending M/M Sep | 0.00% | -0.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | PPI Q/Q Q3 | |

| Forecast: 0.70% | Previous: 1.00% | ||

| 00:30 | AUD | PPI Y/Y Q3 | |

| Forecast: | Previous: 4.80% | ||

| 00:30 | JPY | Manufacturing PMI Oct F | |

| Forecast: 49.0 | Previous: 49.0 | ||

| 01:45 | CNY | Caixin Manufacturing PMI Oct | |

| Forecast: 49.5 | Previous: 49.3 | ||

| 07:30 | CHF | Real Retail Sales Y/Y Sep | |

| Forecast: 2.50% | Previous: 3.20% | ||

| 07:30 | CHF | CPI M/M Oct | |

| Forecast: 0.00% | Previous: -0.30% | ||

| 07:30 | CHF | CPI Y/Y Oct | |

| Forecast: | Previous: 0.80% | ||

| 08:30 | CHF | Manufacturing PMI Oct | |

| Forecast: 49.5 | Previous: 49.9 | ||

| 09:30 | GBP | Manufacturing PMI Oct F | |

| Forecast: 50.3 | Previous: 50.3 | ||

| 12:30 | USD | Nonfarm Payrolls Oct | |

| Forecast: 125K | Previous: 254K | ||

| 12:30 | USD | Unemployment Rate Oct | |

| Forecast: 4.10% | Previous: 4.10% | ||

| 12:30 | USD | Average Hourly Earnings M/M Oct | |

| Forecast: 0.30% | Previous: 0.40% | ||

| 13:30 | CAD | Manufacturing PMI Oct | |

| Forecast: | Previous: 50.4 | ||

| 13:45 | USD | Manufacturing PMI Oct F | |

| Forecast: 47.8 | Previous: 47.8 | ||

| 14:00 | USD | ISM Manufacturing PMI Oct | |

| Forecast: 47.6 | Previous: 47.2 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Oct | |

| Forecast: | Previous: 48.3 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Oct | |

| Forecast: | Previous: 43.9 | ||

| 14:00 | USD | Construction Spending M/M Sep | |

| Forecast: 0.00% | Previous: -0.10% | ||

Markets Weekly Outlook – ‘Magnificent 7’ Earnings, BoJ Meeting and US Jobs Data

- Markets are in a holding pattern as investors weigh risks and uncertainties ahead of a busy week filled with key events.

- The US election is drawing closer, and markets may react to the possibility of a Trump victory, which could lead to a rise in the US Dollar and inflation expectations.

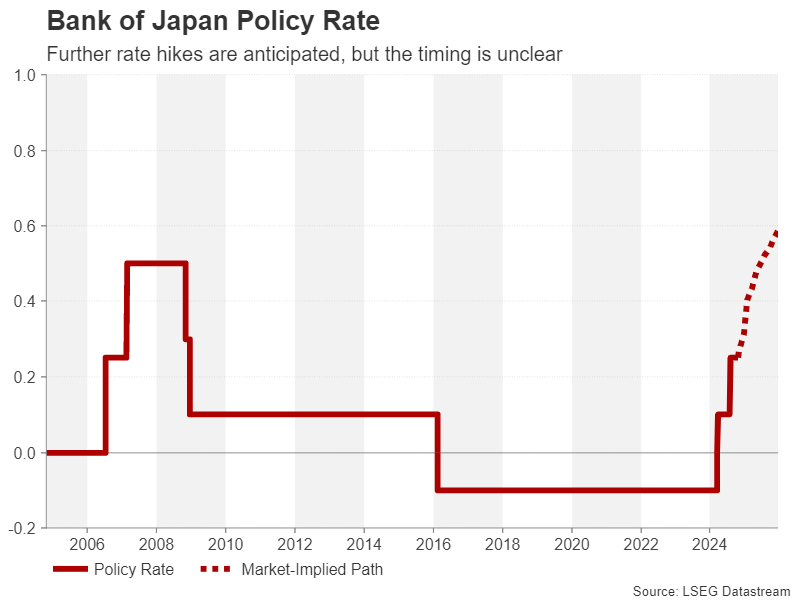

- The Bank of Japan (BoJ) meeting is a highlight in Asia, with market expectations leaning towards no rate hike.

- In the UK, the first budget by the Labor Party under Chancellor Rachel Reeves is highly anticipated.

Week in Review: Markets Appear to be in Holding Pattern as Uncertainties Pile Up

A mixed week comes to a close as markets appear to be balancing their risks ahead of a blockbuster week. Wall Street Indexes suffered early in the week before the Nasdaq and S&P 500 rallied late Thursday and into Friday on the back of a rise in Tesla stock. A good start with the rest of the ‘magnificent 7’ due to report next week.

The IMF conference in Washington will continue into the weekend with no significant developments coming thus far. A few speeches by Central Bank policymakers also throwing up nothing of note has left markets in a state of wait and see as risk and uncertainty begin to pile up.

Market attention will start to turn toward the US election which draws closer. If markets begin to price in a Trump victory the US Dollar could continue to rise. Markets may see a potential rise in inflation and thus less rate cuts should Trump emerge victorious.

There appears to be mixed polling thus far with betting markets pricing in a sizable Donald Trump lead, while a recent Reuters/IPSOS Poll saw a 3% lead in favor of Kamala Harris. The uncertainty is keeping markets on edge and could result in some wild swings as the election draws closer.

The UK saw some weakening PMI data and cooling price pressures this week which adds to the possibility of a BoE rate cut on November 7. However, the week ahead will focus on the first budget by the Labor Party and Chancellor Rachel Reeves. There have been mixed comments with the new Chancellor stating only yesterday that ‘debt will be redefined in the upcoming budget as a % of GDP’. There are also questions around tax hikes etc which makes this a key event for the UK economy.

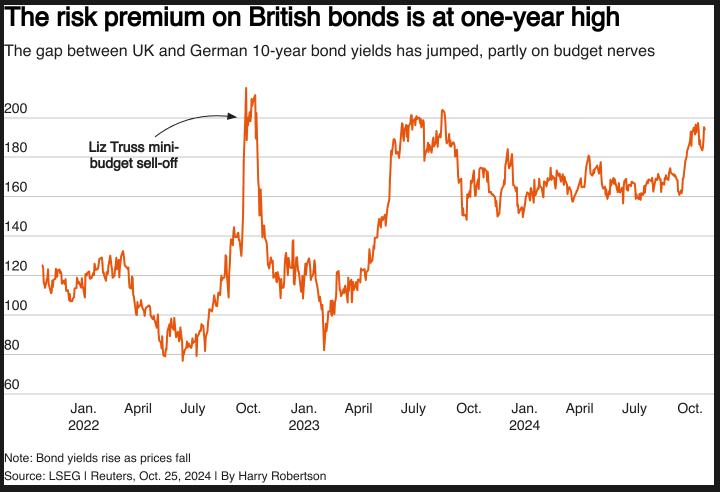

British government bond yields rose sharply with the GB10YT=RR on Thursday after finance minister Rachel Reeves said she would change the fiscal rules to allow her to borrow more to invest. This has left the risk premium on British bonds at a one-year high.

Source: LSEG

Tokyo inflation data released on Friday have complicated matters for the BoJ, just as market optimism had been growing for further rate hikes. Tokyo Core CPI, a leading indicator of inflation trends in Japan, fell to 1.8% y/y in October, down from 2% in September and just above the market estimate of 1.7%.

Commodity markets continue to rise with Gold and Silver in particular continuing their stellar performance. Gold continues to find support as global uncertainties continue to rise. Oil prices look set for modest gains despite a turbulent week that saw some swings in price. The uncertainty in the Middle East continues to keep oil supported.

As long Middle East tensions remain in play, Oil prices will remain supported. The risk premium may continue to flow back and forth which will affect both Oil and Gold moving forward.

The Week Ahead: Magnificent 7 Earnings, NFP Data, UK Budget

The week ahead kickstarts a two week frenzy of risk events and market uncertainties which could result in wild price swings and an upsurge in volatility. Highly awaited earnings from the ‘magnificent 7’ await with indices likely to see a surge in volatility. The S&P 500 and Nasdaq 100 are both within striking distance of their respective all-time highs.

US Jobs data could see rate cut expectations repriced once more and this could have a knock on effect on the US Dollar, US Yields and wall street indexes.

Asia Pacific Markets

In Asia, the Bank of Japan (BoJ) meeting is the highlight of the week. I think the Tokyo data this week has provided a reality check for market participants who had gotten ahead of themselves hoping for a rate hike next week.

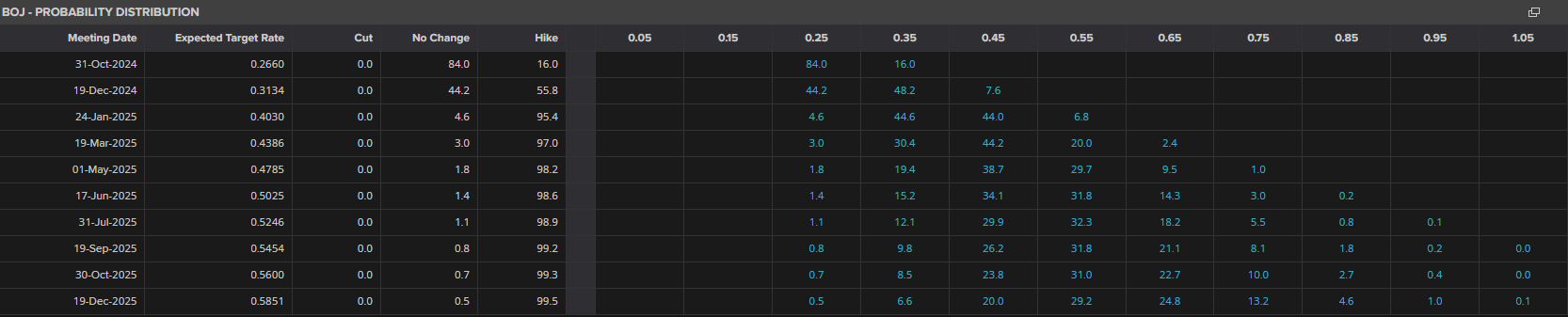

I am of the belief that we will not get a rate hike next week but rather expect the BoJ to repeat that if the economy grows as they expect, they will keep adjusting monetary policy back to normal. According to LSEG data, markets are pricing in an 84% probability that the Central Bank will keep rates on hold.

Source: LSEG Workspace

Everyone will be watching the BoJ quarterly report closely. There is a possibility that inflation for 2024 might be predicted to go higher, but no big changes are expected for next year. However, the GDP forecast for the fiscal year 2024 might be lowered because of recent drops in production in the car industry and natural disasters.

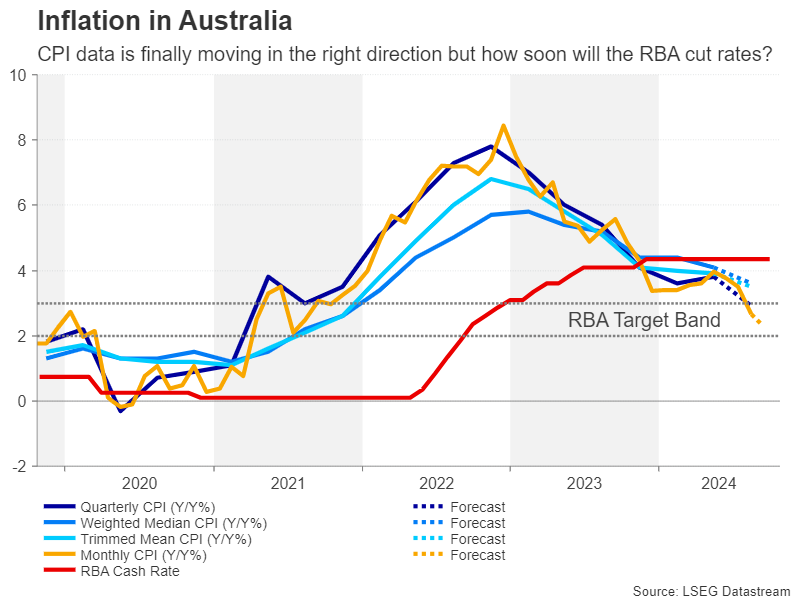

In Australia, inflation is getting closer to the target. Year-on-year inflation is expected to drop in the third quarter, reaching the 2-3% target range for the first time since mid-2021, mainly due to lower gasoline and electricity rebates. However, core inflation is likely to stay above 3% because of the tight job market, meaning the Reserve Bank of Australia probably won’t cut rates in their November meeting.

Europe + UK + US

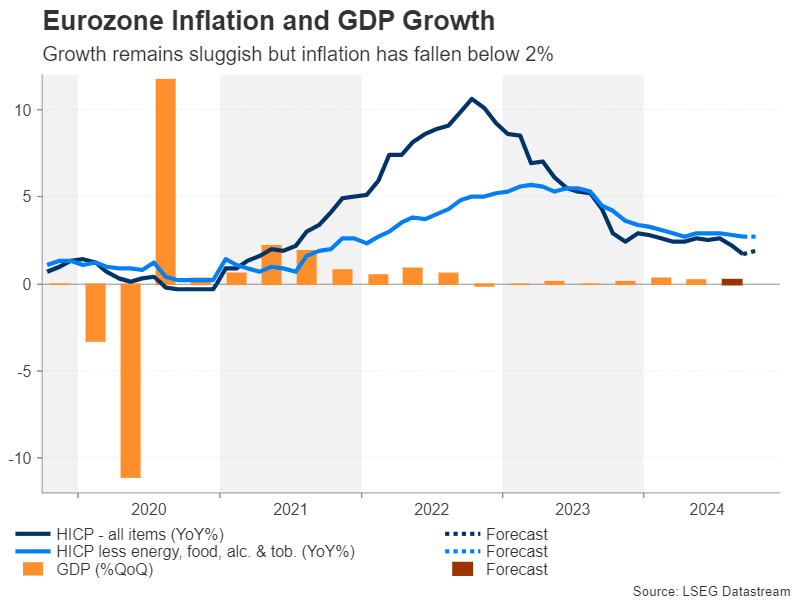

In developed markets, the Eurozone will get the Q3 preliminary GDP numbers which may provide a better picture into the health of the economy. The question for the Euro Area appears to be one of growth now rather than a focus on inflation, much like how the US focus has shifted to the job market. A poor GDP print might increase the rate cut probabilities for the ECB and this could weigh on the Euro.

The US has a pretty busy week with earnings expected from megacap technology firms including Alphabet GOOGL.O, Apple AAPL.O and Microsoft MSFT.O are also due, along with the nonfarm payrolls report for October.

Different earnings results in various sectors and ongoing uncertainty about the U.S. election have made investors careful. However, it would appear markets have begun to consider the possibility of Donald Trump being re-elected recently as reflected in betting data.

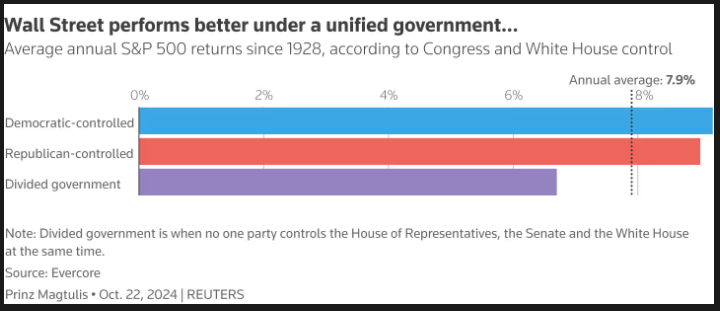

According to historical data, US stock markets perform better under a unified government as you can see from the chart below.

Source: LSEG, Evercore

In the UK markets wait with bated breath for the first budget of the Labor Government to be presented by Chancellor Rachel Reeves on Thursdays November 30. Chancellor Reeves will likely need to spend more on government departments each day, which means taxes might go up, especially for employers. While there will be more investment, it will probably be small because the Treasury wants to avoid borrowing too much and worrying the markets. All in all it is expected to be challenging for Reeves hence why this budget will be intriguing.

Chart of the Week

This week’s focus is on the GBP/USD which i have been monitoring for a while. There is a the possibility of a breakout in either direction and given the host of data affecting the US Dollar and the GBP, i think they could be the catalyst to facilitate a move.

Cable bounced out off a key confluence zone by recording its third touch of the ascending trendline before recording a bullish engulfing daily candle close. This saw a bounce on Friday but the pair continues to struggle to gain acceptance above the 1.3000 psychological level.

There is the possibility of a break below the trendline and retest of the 200-day MA resting lower at the 1.2800 handle. As much as the confluences support a narrative i would caution against being too biased on any setup next week. Given the fundamental risk at play we could see wild price swings which could influence potential setups.

GBP/USD Daily Chart – October 25, 2024

Source:TradingView.Com (click to enlarge)

Key Levels to Consider:

Support

- 1.2940

- 1.2800

- 1.2750

Resistance

- 1.3000

- 1.3100

- 1.3250

Weekly Economic & Financial Commentary: Beige Flags in the Beige Book

Summary

United States: Move On Up

- The housing sector was in focus this week. During September, existing homes sales remained in a slump and declined to a fresh cycle low, while new home sales bucked the trend and rose solidly. Although the move up in mortgage rates will pose some near-term challenges for housing, growth elsewhere appears sturdy.

- Next week: GDP (Wed.), Personal Income and Spending (Thu.), Employment (Fri.)

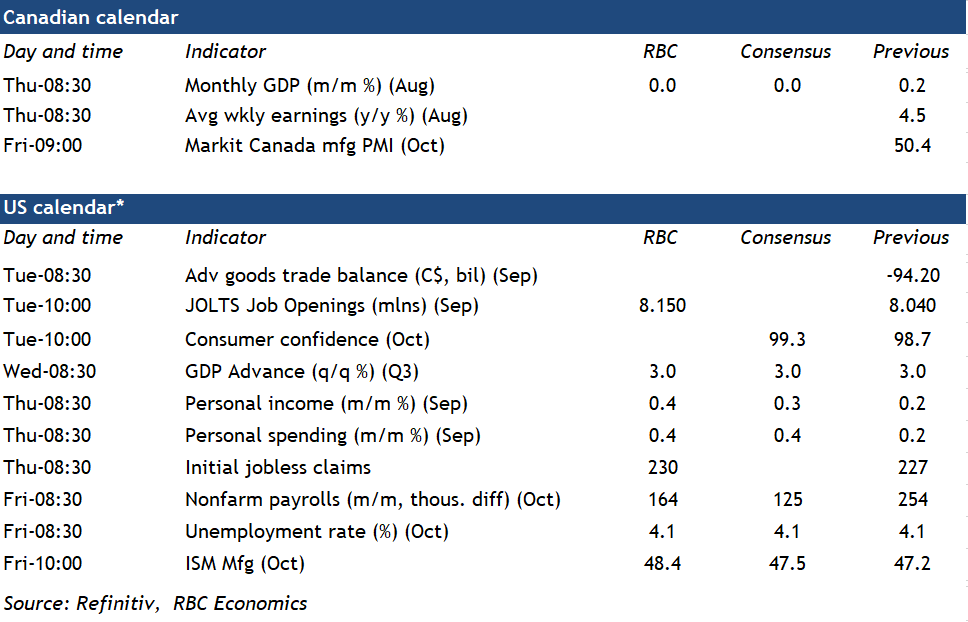

International: Bank of Canada Quickens Monetary Easing, Eurozone Economy Continues to Struggle

- It was a somewhat lighter week for international economic data and events, save for the Bank of Canada (BoC) rate decision and a mix of sentiment data from global economies. The Bank of Canada lowered its policy rate by 50 bps to 3.75% and offered generally dovish-leaning commentary. In the Eurozone, the October PMIs were somewhat mixed but overall not that encouraging.

- Next week: Eurozone CPI & GDP (Wed. & Thu.), China PMIs (Thu.), Bank of Japan Policy Rate (Thu.)

Credit Market Insights: Financial Condition Indices Hit Early 2022 Levels

- Monetary policymakers are keenly interested in quantifying financial conditions, because households and firms respond to changes in them, which in turn translates into changes in real economic activity. Somewhat surprisingly, two financial condition indices from the Federal Reserve currently indicate conditions are about as loose as they were on the eve of the Fed's hiking cycle.

Topic of the Week: Beige Flags in the Beige Book

- The latest Beige Book—which covers early September through mid-October—revealed a picture of softening economic growth. However, despite the bleak picture, contacts were overall optimistic about the longer-term outlook, though still exercised caution in their hiring and investment decisions.

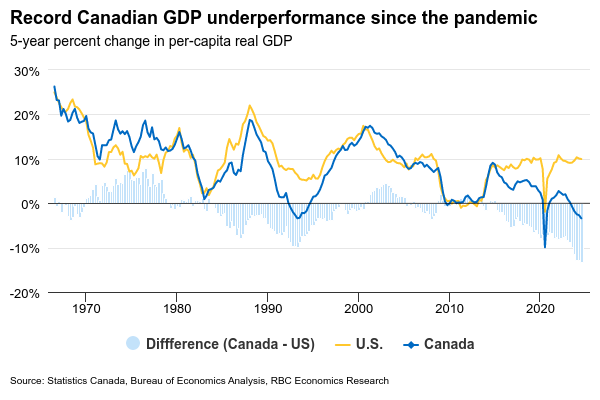

No Growth in Canadian GDP for August Extends Historic Per Capita Underperformance

The Canadian gross domestic product report for August on Thursday will likely reveal more softness in the economy with no growth in line with Statistics Canada’s preliminary estimate a month ago and down from 0.2% growth in July.

A slowdown will be seen in both goods and services. The manufacturing sector likely saw a decline in output, given that sales and volumes were down in August. But, that decline was partially offset by higher output in mining, oil and gas. Wholesale sale volumes declined by 0.7% in August and our tracking of credit card transactions is pointing to a pullback in hospitality services, but retail sales and home resales increased.

The early estimate for September GDP will also likely remain soft. Hours worked declined 0.4% in September—leaving GDP per capita tracking a sixth consecutive quarterly decline. That would extend a historically unprecedented underperformance on a per-capita basis versus the U.S. economy, where we expect Wednesday’s U.S. GDP for Q3 to show another solid 3% gain, faster than Q2. This is consistent with why we expect more interest rate cuts from the Bank of Canada than the U.S. Federal Reserve in the year ahead.

The Fed will be watching U.S. labour market data closely on Friday. U.S. unemployment has been inching higher, but the deterioration has been very gradual and more consistent with normalization in the job market from overheated conditions earlier in the recovery from the pandemic. Disruptions from strikes and hurricanes could significantly distort payroll employment estimates in October, but we look for the unemployment rate to hold at 4.1%. This should be a “cleaner” account of labour market conditions, because those temporarily off work due to bad weather will still be counted as employed for calculating the unemployment rate.

Week ahead data watch

We expect 164,000 jobs to be added to the U.S. labour market in October, slowing from 254,000 in September.

In U.S. Q3 GDP, residential investment is expected to show more weaknesses with housing starts and existing home sales both lower than in the previous quarter. For non-residential investment, equipment investment likely saw solid growth, mainly supported by the aircraft component. That will also offset the decline in structure investment. Lastly, exports likely expanded at a solid pace in Q3, outpacing import growth.

U.S. personal consumption likely grew by 0.4% given robust retail sales in September. We expect personal income to tick up 0.4% from 0.2% in July.

The August Survey of Employment, Payrolls and Hours on Thursday will be analyzed for further signs of easing in the Canadian labour market. Given slower hiring demand, we continue to look for lower job openings and slower wage growth moving forward.

The Weekly Bottom Line: Is 50 the New 25?

Canadian Highlights

- The Bank of Canada made a super-sized interest rate cut this week, taking the overnight rate to 3.75%. The Bank cited the significant decline in inflation as a key factor, but their inflation forecast was little changed from July.

- The Bank’s data dependence has made policy decisions backward looking. If they had focused on their inflation forecast rather than the data, they would have cut rates earlier in the year.

- This focus on the here and now, rather than the forecast may result in overdoing it and needing to recalibrate rates later. Resulting in a more stop-and-go path for interest rates.

U.S. Highlights

- U.S. Treasury yields continued to rise as the race for the White House tightened, leading to elevated uncertainty regarding the future path of fiscal policy.

- Federal Reserve speakers this week noted that further reductions in interest rates would be warranted, although incoming data supported a cautious approach.

- Existing home sales fell to a fourteen year low in September. Elevated interest rates, combined with expectations for lower rates moving forward, worked to keep demand subdued.

Canada – Is 50 the new 25?

No, I’m not talking about age, although I’d greatly benefit from that view! I knew I would eat crow on Wednesday’s Bank of Canada (BoC) call with the high market pricing for a 50 basis point (bp) cut. There’s no regret in having conviction that risks need to be managed when the Bank delivers a rate cut that historically aligns to emergency periods. It could condition Canadians to expect data misses to be met with large monetary responses. I was hoping this would be clearly addressed in the press conference. Unfortunately, it was not, and there was little indication on where the bar is set for another 50 bps in December.

Within the press release, oil was mentioned twice, which is not common fare. It’s been a contributor to a larger-than-expected decline in inflation, but all it would take is a supply disruption from geopolitical events to cause a spike. If so, would we assume all bets are off on future rate cuts? Of course not.

Next up were shelter prices, which were noted to be decelerating. Of course! This is highly forecastable and observable. The peak impact of the rapid escalation in mortgage rates is in the rear-view mirror. And, the act of cutting interest rates takes heat off mortgage interest costs, where there’s a “circular reference” into inflation metrics. Almost a fifth of shelter costs derives from this single input and models have correctly predicted this easing in the growth-impulse.

Next up was mention that the Bank’s preferred core measures were just under 2.5%. The memo that communicated 2.5% was a meaningful threshold, rather than the midpoint of the inflation range, must have gotten lost. The Bank also did not make significant changes to their outlook on the economy or core inflation metrics, except to mark-to-market in Q3.

Carolyn Rogers offered the clearest (and most transparent) explanation — with the benefit of time and more data, the 50 bps cut reflects greater confidence that inflation will hold near 2%. By extension, a faster normalization in rates is warranted. However, this logic automatically argues for at least one more 50 bps cut in December, absent a large miss to the upside on the Bank’s forecast. No surprise, markets have about two-thirds of that priced in.

Normalization means getting back to the BoC’s range for the neutral rate, which they estimate is between 2.25% and 3.25%. The midpoint is cited as the ideal target. Now, that range is not static. It’s regularly revised based on population and productivity trends. For instance, the government’s recently announced changes to immigration targets should result in a downshift in the range due to labour market impacts. In addition, Canada’s persistent poor productivity performance offers further rationale to lower the range. However, doing so would only mean that the BoC policy rate is even further away from neutral than originally believed, yet another argument for several 50 basis point rate cuts to achieve normalization. But as it currently stands, this requires returning to 2.75%, at a minimum. There was no discussion at the press conference on the appropriate pace, other than if the BoC’s forecast is met, interest rates will be cut again.

Let’s get back to fundamentals and pull the lens back on what’s really motivating outsized rate cuts. For decades, central banks drilled into the public mindset that the best approach in monetary policy was:

- Gradual (and transparent) adjustments

- Decisions reflect a forward-looking economic and risk landscape, generally within the 12-to-18-month range.

But that was the pre-pandemic world when central bankers had reasonable confidence in forecast models and historical relationships. Since then, the communication pivoted to focusing analysts on the here-and-now data. Confidence requires irrefutable proof, rather than being about 60% of the way there on the data trend.

Understandable given that the pandemic created a persistent inflation surge that models were not designed to predict. The shock occurred simultaneously along the demand and supply channels. Most macroeconomic models have greater sophistication in understanding the demand side of the equation, rather than the supply side. But here too there were big failures. For instance, the unemployment rate typically had a great track record in predicting household financial stress and consumer patterns. But it had no chance on accuracy during the pandemic cycle that displayed historic departures as the pause button was hit on loan repayments and household bank accounts were backfilled with massive government transfers.

Those days are long gone, and the learnings and sophistication of models has since broadened, as has the understanding of those who rely on them. With the absence of unusual or unique factors, there should be greater confidence in the predictive outcomes of models and judgement. Yet, the central bank keeps its eyes and communication trained on the immediate data to influence decisions. Effectively, decisions are based on data fluctuations largely informing one-quarter ahead rather than the medium term. This is not just a Bank of Canada phenomenon, but a global central bank trend.

What could this mean in the bigger picture? One outcome is an amplification of interest rate volatility. No longer are 50, 75 or 100 basis point moves reserved for the “oh shoot!” emergency moments where there’s high risk of a recession. Interest rate cycles have a later start, but then get compressed, creating larger jumps and tumbles, or volatility.

Is that a bad thing? Not in every aspect. As the BoC noted, they want to stick the landing. A larger interest-rate move isn’t a signal that they know something you don’t. It is an admission that they are behind the curve because that’s the natural state that occurs when the emphasis is on changes in the near-term data. By the time you see the data, observe persistence, you’ll naturally be behind the curve. The data, after all, are already backward looking. But at least once this condition is known, the adjustment is swift to try to prevent more economic weight. As the BoC Governor noted, we took a bigger step because inflation is back to the 2% target, and want to keep it there.

However, this can likewise train households to develop a “pile in” psychology. Canadians are not shy about taking on debt. And the housing market is indeed a sport, with a team fielded by population growth and insufficient supply within key segments, like the detached market. The Canadian history on housing is clear: It responds quickly to interest rate movements. And we’ve just come out of a lengthy pent-up demand cycle. In addition, the government is adding fuel to the market with recent policy changes that will stoke demand amongst first time buyers. That means there will be two big channels feeding through the housing market simultaneously, even as immigration flows get tapped down with the government’s recent announcement.

There will be those wanting to “beat the crowd” and secure “a deal” before the combination of government measures and even lower interest rates create a groundswell in demand that risks flipping various markets from balance back to a sellers’ market. But some will be forced to wait longer, in need of those new government measures. So for those with eyes trained on the here-and-now data, the next couple of months may produce housing data that might look like Canadians are not overly responding to interest rate cuts, but my money is on nature and nurture coming back into play. 2025 could display a stronger response in housing demand as monetary and government policy collide into a one-two punch to unleash pent-up demand.

If the Bank of Canada is going to prioritize the near-term data towards outsized rate cuts, we must consider that it would need to be equally responsive to risk-development. This can create an overcorrection on interest rates, going down too deep only to be fine tuned again on the upside as the household spending impulses kick in more suddenly relative to when interest rates follow more gradual cycles. Likewise, it can result in more stop-and-go monetary policy.

U.S. – Countdown to Election Day

One of the most anticipated global events of 2024 is now nearly a week away. As financial markets anxiously await the outcome of the U.S. presidential and congressional elections, we have seen U.S. Treasury yields and the U.S. dollar rise to three-month highs (Chart 1). The uptick which began earlier this month was initially incited by stronger-than-expected economic data, but recent movements have also likely been driven by the narrowing in the polls for the U.S. presidential election. Given that the election will determine the path of fiscal policy moving forward, and by extension monetary policy, uncertainty related to the outcome is likely to remain a weight on financial markets through to November 5th.

Elevated interest rates continued to dampen housing market activity in September, as existing home sales fell to their lowest level since 2010! Demand is also likely being restrained in part by consumer expectations for lower interest rates moving forward, with Federal Reserve Chair Powell indicating that rates would likely be trending lower through the coming year during his press conference last month. Existing home sales are likely to remain subdued in the near-term as mortgage rates moved back above 6½% in October. Nevertheless, the housing market is expected to thaw over the coming year as the Federal Reserve continues to reduce borrowing costs.

The Federal Reserve will be entering its pre-interest rate decision blackout period this weekend, with no further updates expected until Chair Powell’s post-meeting press conference on November 7th. The Fed officials we heard from this week stated that the strength of incoming economic data would warrant caution in future policy decisions, but all speakers noted that the trajectory of interest rates would continue to be downward. Market pricing has pulled back their expectations for rate cuts, but they are now realigned with the Federal Reserve’s median projection from the September Summary of Economic Projections (Chart 2).

Next week sees a bumper crop of data releases that will be key inputs to the Federal Reserve’s next interest rate decision. The advance estimate for real GDP growth in the third quarter is expected to show the economy continuing to grow at a strong pace of 3.0%. While employment growth remained solid in the third quarter, October’s employment report due out next Friday is expected to show a deceleration in job gains (125k vs. 254k in September). The Federal Reserve will also be monitoring the release of their preferred inflation metric next week, core PCE, which is expected to show a modest decline to 2.6% in September.

Assuming there are no surprises in the incoming data, the Federal Reserve is expected to continue to cut rates at a pace of 25 basis points per meeting through the end of the year. Chair Powell’s remarks on November 7th will be monitored closely for guidance, although they may be competing with the results of the 2024 election for the attention of financial markets. Suffice it to say, markets will not be left wanting for important developments in the coming weeks.

Week Ahead – A Decisive Week for USD with NFP and More; BoJ Meets

- A crucial week lies ahead with US jobs report, advance GDP and PCE inflation

- The Bank of Japan is expected to hold rates, but will it flag a year-end hike?

- Flash GDP and CPI data for the euro area are also hotly anticipated

- Australian quarterly CPI and UK budget on the agenda too

All eyes on US data as Fed turns hawkish again

The Federal Reserve’s surprise decision in September to cut rates by a larger-than-expected 50-basis-points seems like a distant memory now, as policymakers are once again sending out hawkish soundbites.

US economic indicators since the September meeting have been on the strong side, including the CPI report, with Fed officials cautioning that another 50-bps cut is unlikely in the near term. The sudden switch in the narrative from ‘hard landing’ to ‘soft landing’, or possibly even a ‘no landing’, has spurred a sharp reversal in Treasury yields, which in turn has pushed the US dollar higher.

With the Fed’s November policy decision fast approaching, next week’s data will serve as a timely update on the strength of the US economy as well as on inflation.

Slowdown, what slowdown?

Kicking things off are the October consumer confidence index and the JOLTS job openings for September on Tuesday. But the top-tier releases do not start until Wednesday when the first estimate of third quarter GDP is due.

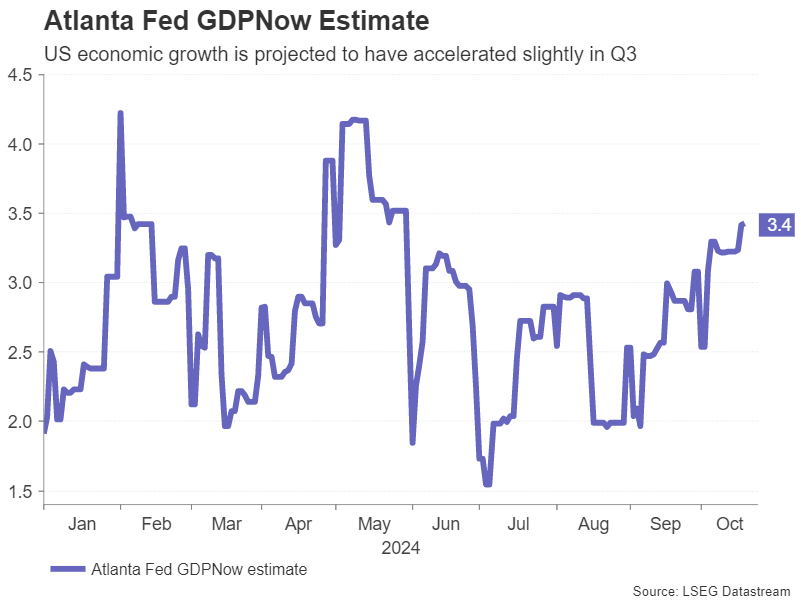

The US economy is expected to have expanded by an annualized rate of 3.0% in Q3, the same pace as in Q2. Not only is this above average growth but an upside surprise is more likely than a downside one as the Atlanta Fed’s GDPNow model puts the estimate at 3.4%.

Other data on Wednesday will include the ADP private employment report, which will provide an early glimpse into the labour market, and pending home sales.

Spotlight on PCE inflation after mixed CPI

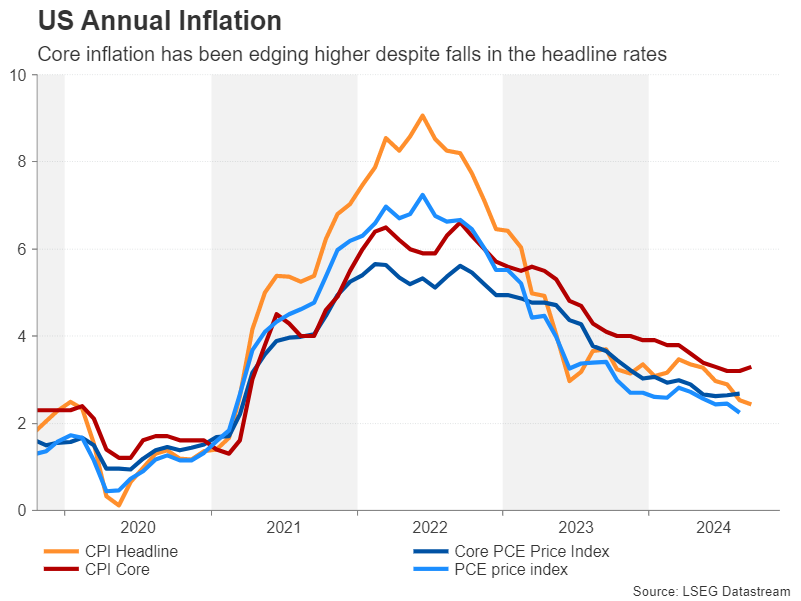

Both the CPI and PCE measures of inflation show a divergence between the headline and core readings. The core PCE price index, which the Fed puts the most weight on in its decision making, ticked up to 2.7% y/y in August even as headline PCE eased to 2.2%. It’s likely that both prints stayed unchanged in September or fell slightly. Hence, the inflation numbers may not be particularly helpful for the Fed or investors.

Still, the personal income and consumption figures due the same day will offer additional clues for policymakers, while October Challenger Layoffs and the quarterly employment cost will be watched too.

NFP report may hold the cards

Finally on Friday, the week’s highlight – the October nonfarm payrolls report – will come to the fore. After a solid 254k rise in September, it’s projected that the US labour market created 140k new jobs in October, signalling a marked slowdown. Nevertheless, the unemployment rate is expected to have held at 4.1%, while average hourly earnings are forecast to have moderated slightly from 0.4% to 0.3% m/m.

Also important will be the ISM manufacturing PMI, which is expected to improve from 47.2 to 47.6 in October. With the Fed now more worried about the jobs market than inflation, soft payrolls could set the tone back to a more dovish one.

Can the US dollar extend its rebound?

Moreover, any signs that the American economy is cooling is likely to push up market bets of back-to-back rate cuts for the next few meetings. However, if growth remains robust and more significantly, PCE inflation points to some stickiness, rate cut bets will probably suffer a further blow.

At the moment, only one additional 25-bps reduction is fully priced in for 2024. If a rate cut in November starts to come into doubt, the US dollar could climb to fresh highs but stocks on Wall Street would probably come under selling pressure.

For the latter, however, a busy earnings week might keep the positive momentum going if results from Microsoft, Apple and Amazon.com don’t disappoint.

Bank of Japan expected to stand pat

Twenty twenty-four was a turning point for the Bank of Japan’s decades-long fight against deflation. The BoJ abandoned its yield-curve control policy, halved its bond purchases, and raised borrowing costs twice, ending its policy of negative interest rates.

However, despite policymakers’ clear intention to continue the normalization of monetary policy and raise rates even higher, inflation appears to be settling around the BoJ’s 2.0% target, lessening the need for further tightening. The most recent commentary from Governor Ueda and other board members suggests a rate hike is not forthcoming on Thursday when the Bank announces its October decision.

But the updated outlook report with a fresh set of projections on inflation and growth should be quite insightful on the likelihood of a rate hike in December or during the first few months of 2025.

In the absence of any hints about a rate hike anytime soon, the yen will probably continue to struggle against the US dollar. Yet, a renewed weakness in the yen will only incentivize policymakers to hike sooner rather than later and this is a risk investors may be overlooking.

Also on the Japanese schedule are preliminary industrial output figures and retail sales figures for September, both due on Thursday.

Euro awaits flash GDP and CPI

The euro’s double top pattern against the greenback did not let down technical analysis enthusiasts and the pair recently brushed 16-week lows, falling below $1.08. Next week’s releases are unlikely to be of much help to the bulls.

The flash estimate of GDP out on Wednesday is expected to show that the Eurozone economy eked out growth of just 0.2% q/q in the third quarter. On Thursday, attention will turn to the flash CPI readings. The headline rate probably edged up from 1.7% to 1.9% y/y in October, but the ECB is already forecasting a pickup in the coming months.

Nevertheless, stronger-than-expected data could provide the euro with some short-term relief following four consecutive weeks of losses. Alternatively, if the numbers disappoint, investors are sure to ramp up their bets of a 50-bps cut by the ECB in December.

Pound looking shaky ahead of UK budget

It hasn’t been the best of times for sterling either lately, despite the Bank of England being one of the more hawkish central banks at the moment. The pound has lost grip of the $1.30 handle, and there could be more downside on Wednesday when the UK Chancellor of the Exchequer Rachel Reeves announces the new Labour government’s first budget.

The UK press has gone into overdrive with its coverage of the budget and all indications are that Reeves will unveil tax increases of £40 billion, raising the tax burden to the highest since 1948. Whilst this may not be good news for taxpayers, BoE policymakers might welcome it, as tighter fiscal policy will dampen demand in the economy, paving the way for faster rate reductions.

The pound is at risk of slipping further from a deficit-reducing budget. Even if there are some growth boosting policies included, they are likely to be longer-term measures and not get in the way of the BoE cutting rates. Yet, there might be some support for sterling if investors take note of the fact that the UK government is focusing on long term investments and keeping the deficit in check rather than on short-term sweeteners for voters that push up borrowing.

Australian CPI eyed as RBA decision looms

Finally, traders will be watching CPI stats out of Australia on Wednesday as the Reserve Bank of Australia maintains a neutral stance on rates. After edging up earlier in the year, inflation in Australia finally started moving in the right direction over the summer. The monthly print fell to 2.6% y/y in August, hitting the RBA’s 2-3% target band for the first time since 2021.

The quarterly data, which is deemed more accurate, is bound to form the basis of discussion for the November 5 meeting. However, even if there is more good progress in bringing inflation down, particularly in the trimmed and weighted mean measures, the RBA is likely to remain cautious for now and at best, begin the debate of when to start cutting rates.

But for the Australian dollar, a hawkish RBA may only go so far in coming to the aussie’s aid if broader market risk sentiment remains fragile and the US dollar stays strong. In addition to domestic data, aussie traders will also be monitoring China’s October PMIs out on Thursday and Friday.

Weekly Focus – Stagnant Euro Area Economy Supports Gradual Easing

The dollar continued its October rally, and yields edged higher this week. The moves reversed somewhat by the end of the week, as investors maybe questioning the sustainability of the recent sharp rise in US rates. Oil prices retraced some of the decline from recent weeks which weighs on energy-importing currencies such as euro and yen. The latter has been the big loser in October in general amid the moderation in the Fed pricing as US recession fears have been placed on the back burner.

The modest growth trajectory in the euro area continues with the October composite PMI at 49.7 on the back of a weaker-than-expected service sector and a stronger-than-expected manufacturing sector. Interestingly, German and French employment indices are now below 50 in the service sector for the first time in four years. That said, the two dominating economies are also the weak links in the euro area. The French service sector in particular pulled activity lower, but since we compare to a September with Paralympics in Paris, the world's third largest sporting event, we think markets should have been less surprised by the weak service print. German data was better than expected with a reaccelerating service sector and manufacturing increasing from very low levels. Ifo data also confirmed the encouraging German signs with both the current assessment and expectations moving higher, although from very low levels.

Largely the data aims with gradual ECB easing as we see it. That said, it does not keep investors from pricing in a growing probability of a jumbo cut in December and even a hawk such as Dutch governing council member Klaas Knot would not rule it out when speaking this week.

The coming week will be eventful. In the euro area, we will look out for inflation and Q3 GDP. In the former, gauging service price momentum will be key following a marked slowdown in September. We suspect it was mainly a blip and expect service price momentum to pick up again. We expect 0.2% Q3 GDP-growth supported by Southern Europe and the Olympic Games in France.

We also get a fan of key data releases from the US. On the labour market, we will look out for the number of job openings in the JOLTS report, which is an important measure of labour demand for the Fed. We think nonfarm payrolls growth slowed down to 130k (Sep: 254k) both due to weather-related distortions and less favourable seasonal adjustment. We expect Q3 GDP-growth of 2.5% on annualized Q/Q basis (Q2: 3.0%).

In Japan, we will keep an eye on the general election on Sunday. Polls have indicated the ruling coalition is in danger of losing its Lower House majority. This could compromise the backing for further rate hikes from the Bank of Japan (BoJ). That said, the largest opposition party, which has refused to enter the coalition, has a more hawkish stance on monetary policies, so the consequences for potential rate hikes down the line are not clear. We still look for another rate hike in December or January, but we expect the BoJ to stay on hold on Thursday.

Sunset Market Commentary

Markets

German Bunds underperformed US Treasuries today. Yields added between up to 2.2 bps, the front end of the curve taking the lead. Yesterday’s PMI’s didn’t deliver a similar September-shocker and even offered a glimpse of hope for the battered German economy. That led some of the more hawkish ECB policymakers to come out of the shadows and push back against building market expectations for a 50 bps cut in December. Kazaks (“markets shouldn’t run ahead of themselves”), Muller (“best policy choice is measured rate cuts”), Wunsch (“don’t need a discussion on 50 bps at this stage”) and Simkus (“don’t see case for 50 bps cut”) all hit the wires. US yields ease a few basis points but remain on track for weekly gains from 6 (30-yr) to 12 bps (3, 5-yr). The euro ekes out a tiny gain on improving interest rate differentials in technically insignificant trading (EUR/USD 1.084). The trade-weighted dollar index eases few ticks and is testing the 104 big figure. EUR/GBP steadies around 0.834. The eco calendar contained US September durable goods data. The headline figure eased -0.8%, less than the expected -1% but came after the August number was revised down from flat to -0.8%. Core gauges beat estimates but a key one, shipments, missed the bar by unexpectedly dropping 0.3% m/m. The latter is a proxy for investments in GDP and is probably the reason why we’ve seen some intraday (yield) jitters: markets are headed towards an important eco calendar next week with the US, amongst others, publishing the first estimate of third-quarter GDP growth on Wednesday. Estimates are for a solid 3% q/q (annualized), matching the previous quarter’s pace. Other critical US data include PCE inflation (Thursday), October payrolls (for which the bar is pretty low because of an expected hurricane impact) and the manufacturing ISM (both on Friday). Next week are heydays for European number crunchers too. GDP growth on Wednesday may be better than the dire Q3 PMI readings suggest (0.2% vs flat) as hard data lately often deviated from soft indicators. European inflation numbers for October are scheduled on Thursday. Base effects should make clear that the current 2% undershoot is temporary at least through the end of the year. Investors are also keeping a close eye on the UK Chancellor presenting the Budget on Wednesday. Reeves already disclosed she’s altering the fiscal rules in order to create additional budgetary headroom of as much as £50bn over the coming years. Markets are on high alert. The Bank of Japan meets on Thursday. It won’t hike rates from the current 0.25% but it may hint at one in December. The Japanese yen sure won’t complain, having lost more than 10 big figures in just one month. The earnings season meanwhile also gains traction: Apple, Amazon, Intel, Microsoft, Meta Platforms, Alphabet and many others report.

News & Views

The ECB consumer expectations survey of September, inflation perceptions over the previous 12 months, for the next 12 months and for three years ahead all declined to respectively 3.4% (from 3.9% in August), 2.4% (from 2.7% and now the lowest since September 2021) and 2.1% (from 2.3%, the lowest since the Russia invaded Ukraine in February 2022). Expectations for nominal income growth rose slightly from 1.2% to 1.3% while those for spending growth over the next year remained unchanged at 3.2%. Stable expectations for spending and at the same time a lower inflation trajectory suggests a positive turning point for real spending, according to the comment in the survey. Consumers still see economic growth unchanged at -0.9% in the next 12 months with the unemployment rate rising to 10.6% from 10.4%.

The business survey of the National Bank of Belgium showed a small recovery in October. After successive declines since June the indicator rose slightly to -12.8 from -13.3. Business confidence improved in the building industry, trade and business-related service, but confidence in the manufacturing industry worsened. The improvement in the building industry was mainly due to an improvement in demand expectations and increased order books. The trade sector also expressed greater optimism on expected demand and intends to place more orders with suppliers. In business-related services respondents assess the current activity much more negatively but expect it to improve in the next three months. They also believe that general market demand will rise. The slight fall in manufacturing is mainly due to a more unfavourable assessment of total order books. The sector anticipates a slight drop in demand but is more optimistic about stock levels and expectations for employment.

Canada: Retail Sales Grow for the Second Consecutive Month, Supported by Auto Sales.

Retail sales rose by 0.4% month-on-month (m/m) in August, coming in worse than Statistics Canada's advance estimate for a 0.5% m/m increase. July's print was unchanged at 0.9% m/m reported in the advance estimate.

Adjusting for inflation, the volume of retail sales was 0.4% higher on the month.

Sales at motor vehicle and parts dealers rose by 3.5% m/m – the second consecutive month of growth. Ex-autos, sales were down 0.7% m/m, below the consensus expectation for growth of 0.4% m/m.

Receipts at gas stations and fuel vendors fell 2.7% m/m in nominal terms, as gas prices declined thanks to lower oil prices. Still, in volume terms, receipts were down 2.2% m/m in August.

Excluding auto sales and receipts at gas stations, core retail sales were down by 0.4% m/m in August.

- The loss in core sales was led by food and beverage stores (-1.5% m/m) and furniture & electronics stores (-2.6% m/m).

- A few categories reported gains, but they weren’t strong enough to offset the contraction reported by biggest category declines.

E-commerce sales declined by 2.5% m/m, erasing gains of the previous month.

Statistics Canada's advanced estimate for September points to an increase of 0.4% m/m.

Key Implications

Strong auto sales continued to drive retail growth in August. However, ex-autos, sales were the weakest in three months. Our internal credit and debit card spending data, which primarily reflects non-durable and durable goods, indicates a softening trend through September. Together, these signals align with our forecast, where a rebound in durable goods is expected to be the largest contributor to Q3 growth in total personal consumption expenditures - projected to rise at a below-trend rate of 1.0-1.5% quarter-on-quarter (annualized).

Alongside the weakness in core sales, the downward trend in retail spending per capita remains intact, marking a major area of concern for the Bank of Canada, which moved to cut rates by 50 basis points this week. By accelerating its easing cycle, the Bank wants to see consumption growth strengthen, but it risks sparking more demand for housing instead. Financial markets are currently pricing in a coin-flip chance of another jumbo cut in December.

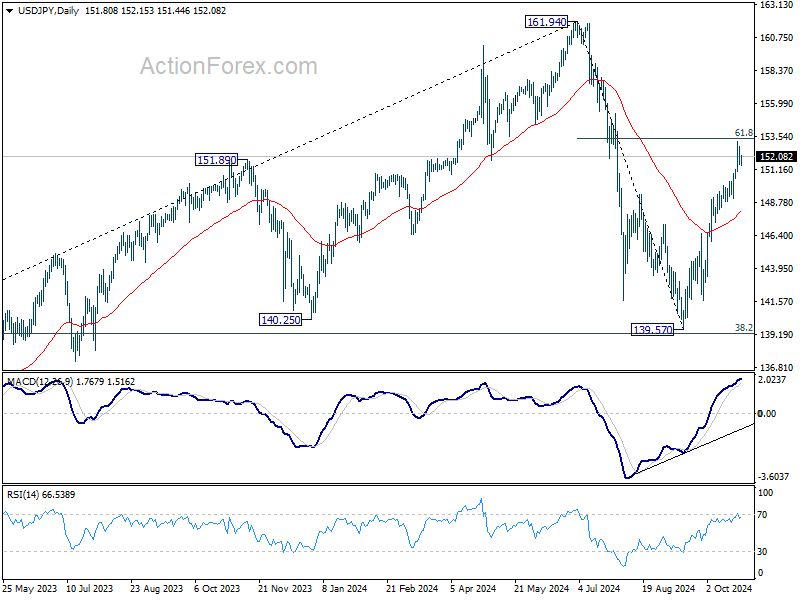

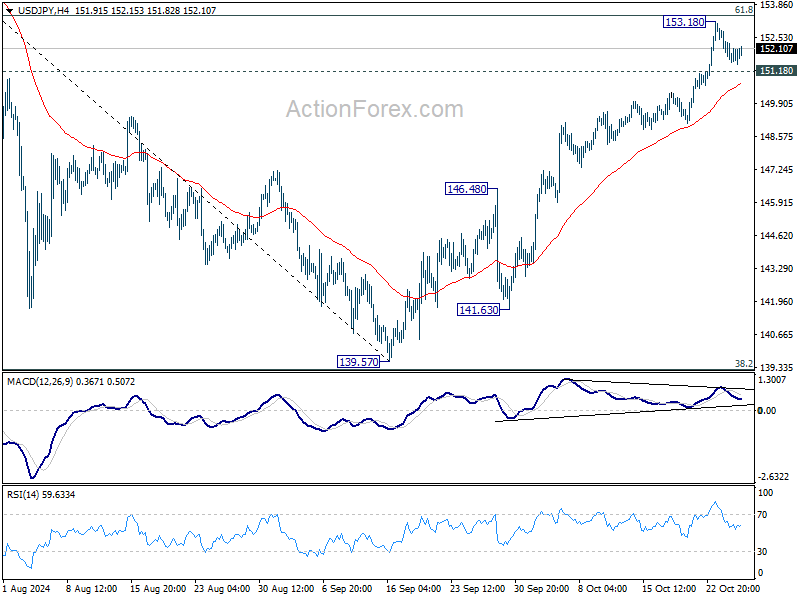

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.30; (P) 152.07; (R1) 152.58; More...

Intraday bias in USD/JPY remains neutral for consolidations below 153.18 temporary top. Further rise is in favor as long as 151.18 minor support holds. Decisive break of 61.8% retracement of 161.94 to 139.57 at 153.39 will extend the rally from 139.57 to retest 161.94 high. However, considering bearish divergence condition in 4H MACD, break of 151.18 will indicate short term topping, and turn bias to the downside for 55 D EMA (now at 148.01).

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.