Sample Category Title

USD/CHF Daily Outlook

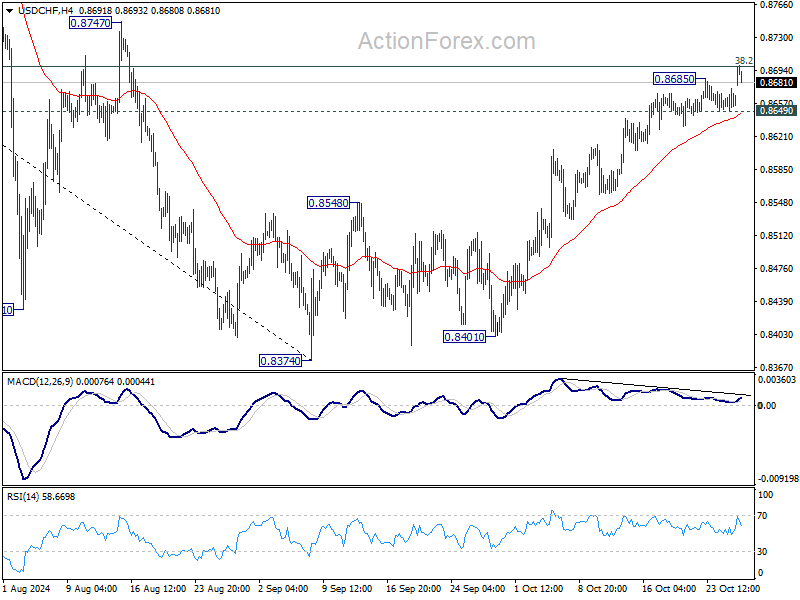

Daily Pivots: (S1) 0.8652; (P) 0.8664; (R1) 0.8679; More…

USD/CHF's rally from 0.8374 resumed after brief consolidations, and intraday bias is back on the upside. Decisive break of 38.2% retracement of 0.9223 to 0.8374 at 0.8698 will argue that fall from 0.9223 has completed after defending 0.8332 low. Further rally should then be seen to 61.8% retracement at 0.8899 next. On the downside, below 0.8649 minor support will turn intraday bias neutral again first.

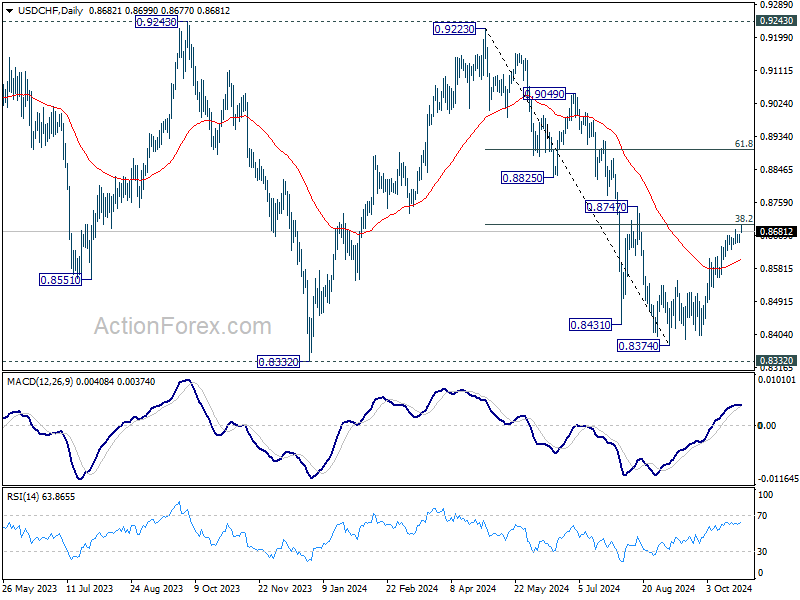

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

Yen Extends Losses This Morning

Markets

Core bond yields ended the week higher. German bond yields added between 1.2 (30-yr) and 4 bps (2-yr). Bunds initially underperformed US Treasuries before the latter suffered from a late-session swoon. US yields swapped earlier losses for gains varying between 2.6 and 3.2 bps across the curve. The US dollar held the upper hand against all G10 peers. EUR/USD tried but failed to extend Thursday’s gains. European PMI’s not delivering a September-like disappointment was a weak base to rally on anyway. The couple returned from intraday highs around 1.084 to back below 1.08. The trade-weighted dollar index finished north of 104 after all. A nervous JPY going into the Sunday elections prevented USD/JPY from dropping below the 200dMA around 151.45. The yen extends losses this morning after the ruling LDP and its much smaller coalition party lost their majority in what is considered a bigger blow than expected to premier Ishiba’s party. Ishiba and the LDP will be exploring their options, potentially teaming up with a party that’s pursuing expansionary fiscal policies - in coming weeks. Not that it needed one, but the extra layer of political uncertainty is an additional argument for the Bank of Japan to stand pat at Thursday’s policy meeting. That’s just one of the key events featuring the massive eco calendar this week though. Today starts off quiet, paving the way for a technical extension to the so-called Trump trade (higher USD, US rates) as the odds increasingly turn into the favour of the former president. The US publishes the first estimate of third-quarter GDP growth as well as quarterly PCE inflation numbers on Wednesday. Estimates are for a solid Q2-matching 3% q/q (annualized). Key US labour market data include JOLTS job numbers on Tuesday and (hurricane-affected) October payrolls on Friday. Spotlights are also on Europe with GDP growth released on Wednesday. The economy may have fared better than the dire Q3 PMI readings suggested (0.2% vs flat). Hard data lately often deviated from soft indicators. October inflation most likely picked up again in the EMU. Base effects will make it clear that the current 2% undershoot is temporary at least through the end of the year. UK Chancellor Reeves will present the Budget to parliament on Wednesday. Investors are on high alert after she altered the definition of “debt” to create additional budgetary headroom. The earnings season meanwhile also gains traction: Apple, Amazon, Intel, Microsoft, Meta Platforms, Alphabet and many others report.

News & Views

Rating agency S&P affirmed the Belgian AA rating with a stable outlook last Friday after market close. The stable outlook balances risks from comparatively large budget deficits and increasing general government debt against the potential for stronger economic growth and improvement in Belgium's already-solid external position. S&P is on the optimistic side of the aisle in forecasting that the budget deficit will gradually narrow to 3.4% of GDP in 2027 from 4.2% last year. The government debt ratio stays slightly below a high 100% of GDP through 2027 in such scenario. They add the disclaimer that failure to reduce these larges deficits and debt ratio could prompt a rating downgrade. Political fragmentation will likely complicate the next government’s implementation of economic and budgetary reforms. S&P forecasts Belgium's annual real economic growth to average 1.3% in 2024-2027 on robust consumption and investment activity, and faster European economic growth from 2025. Earlier this month, rating agency Moody’s switched the outlook on the Belgian Aa3 rating from stable to negative. Fitch is expected to resolve its negative outlook on Belgium’s AA- rating (in place since early 2023) at the beginning of next year with a significant risk of a first ever downgrade from the AA into the A category.

The Bulgarian centre-right Gerb party of former PM Borissov remains the biggest in the nations seventh parliamentary election since 2021. The party gained again around 25% of the vote and needs at least two coalition partners to form a government. This risks again being complicated as number two in the polls ran on an anti-corruption platform (anti-Gerb) and number three is the only party Borissov specifically rules out to work together with (pro-Russia, anti-Nato). Borissov was firmly in power in the decade running up to anti-graft protests against him and his party which kickstarted the political stalemate of the past three years resulting in delays to euro-adoption plans and freezing billions of EU aid.

US Jobs Report and Inflation in Focus This Week

In focus this week

Today will be quiet on the data front, with no major releases scheduled

This week is expected to be calm before the storm of the US election. On Tuesday we will have the JOLTs report and the consumer confidence from the US Conference Board. On Wednesday, we receive preliminary estimate of GDP growth for Q3 for both the US and euro area. Thursday, we will receive euro area HICP inflation for October and September unemployment rate. Friday, we will receive job market reports from the US including non-farm payrolls for October. We also get the Swiss CPI.

Economic and market news

What happened during the weekend

In Japan, the ruling coalition lost its Lower House majority at an election yesterday as it lost 64 of its 279 seats in the 465 large House and thus comes 18 seats short. There are no real grounds for a government not including the Liberal Democratic party. That said, the election result implies a lot of political uncertainty, which is also reflected in financial markets. USD/JPY has traded back to the highest levels since July and long-dated JGB yields have increased a couple of basis points. It is also worth noting that the Democratic Party for The People and the Innovation Party, who could now be key to form a government, have both been critical of BoJ hikes. We will keep a close eye on the political negotiations this week.

In the Middle East, Israel retaliated the attacked carried out by Iran on 1 October, striking military sites early Saturday. Israel said it achieved its objective, while Iran said that damages were limited. In early trading Monday, the Brent oil price dropped to around 72.6 USD/barrel.

What happened on Friday

In France, Moody's changed their outlook on France from stable to negative on the back of the fiscal problems. There is a clear risk of the downgrade if the country were to announce a "medium-term fiscal strategy that fails to reverse adverse fiscal trends or lacks credibility about its effective implementation." France has a minority government and the budget for 2025 has not yet been approved.

In Germany, the Ifo index rose more than expected in October like the PMIs yesterday. The assessment of the current situation rose to 85.7 (cons: 84.4) from 84.4 while the expectations component to rose 87.3 (cons:86.9) from 86.4. While the overall level of the index is still low it gives some relief to the German outlook as the PMI survey showed the same development yesterday. The October data gives tentative hopes of a bottoming in activity, but we remain cautious of becoming too optimistic as it is just one month of data.

In the euro area, credit growth continued to rebound with lending to companies up by 1.1% in September, which is the highest rate since mid-2023. Lending to households was up by 0.7% which is the highest level since October 2023. Money supply as measured by M3 increased more than expected to 3.2% (cons: 3%, prior: 2.9%).

Equities: Global equities were lower on Friday and declined last week by more than 1% (down 4 out of 5 days). More notably, cyclicals continued to outperform and the VIX drifted higher, ending north of 20. The primary drivers last week were micro data, particularly the results from Tesla, which propelled the auto sector to the top of the performance table in the US. It is important to note the lack of spill-over to Europe and the very company-specific outlook in that sector. The increase in implied volatility was not so much a result of micro and macro data but rather due to the impending US election. In the US on Friday, the Dow fell by 0.6%, the S&P 500 by 0.03%, the Nasdaq rose by 0.6%, and the Russell 2000 by 0.5%. This morning, we have a mixed picture in Asia, with Japanese stocks climbing as the yen weakened following the LDP coalition defeat. US and European futures starting the week on a stronger note.

FI: The sell-off continued in the US bond market on Friday, where 2Y yields climbed some 6bp from the lows on Friday, while 10Y yields climbed 5-6bp. This morning US yields have also risen in Asian trading hours. The sell-off has mainly been driven by the possibility of a Trump victory and this week we will get the quarterly refunding statement from the US Treasury, which could add pressure to US government bonds. On top of this there is also a string of US economic data.

FX: NOK rose together with GBP, USD and EUR on Friday in an otherwise quiet end to the week. The sell-off in EUR/USD started to meet some near-term resistance around the 1.08 level. EUR/SEK rose to the highest level since September close to 11.50. EUR/NOK held steady around 11.84.

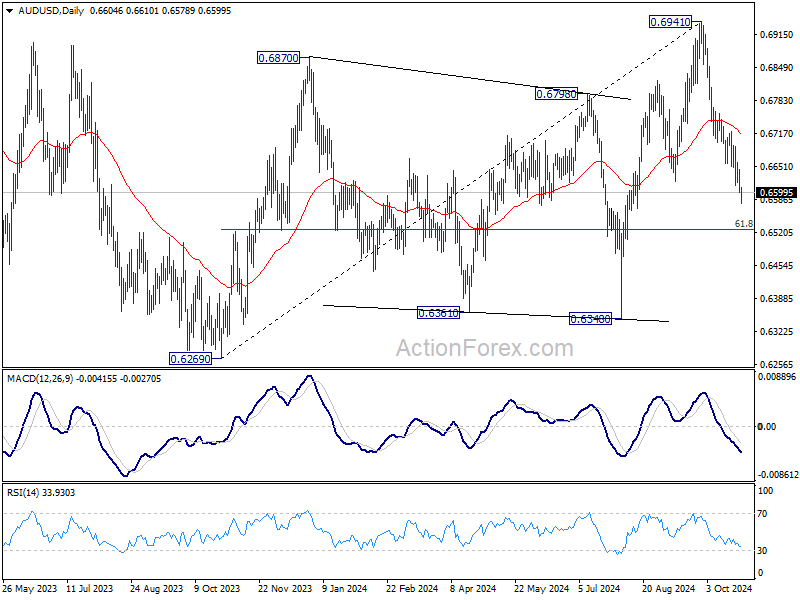

AUD/USD Daily Report

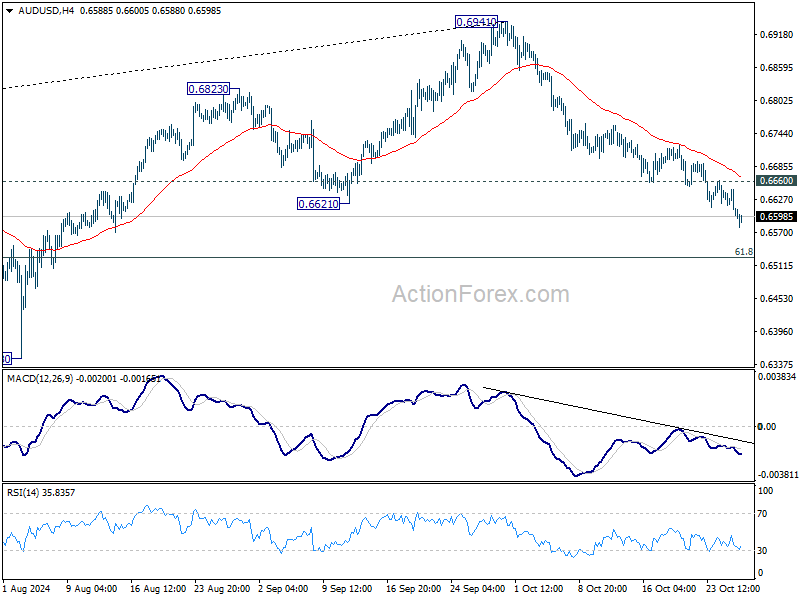

Daily Pivots: (S1) 0.6588; (P) 0.6617; (R1) 0.6634; More...

Intraday bias in AUD/USD remains on the downside for the moment. Fall from 0.6941 is in progress for 61.8% retracement of 0.6269 to 0.6941 at 0.6526. Sustained break there will target 0.6348 support next. On the upside, above 0.6660 minor resistance will turn intraday bias neutral and bring consolidations first.

In the bigger picture, rise from 0.6269 (2023 low) should have completed with three waves up to 0.6941. Corrective pattern from 0.6169 (2022 low) is now extending with another falling leg. Deeper decline would be seen back to 0.6269 as sideway trading extends.

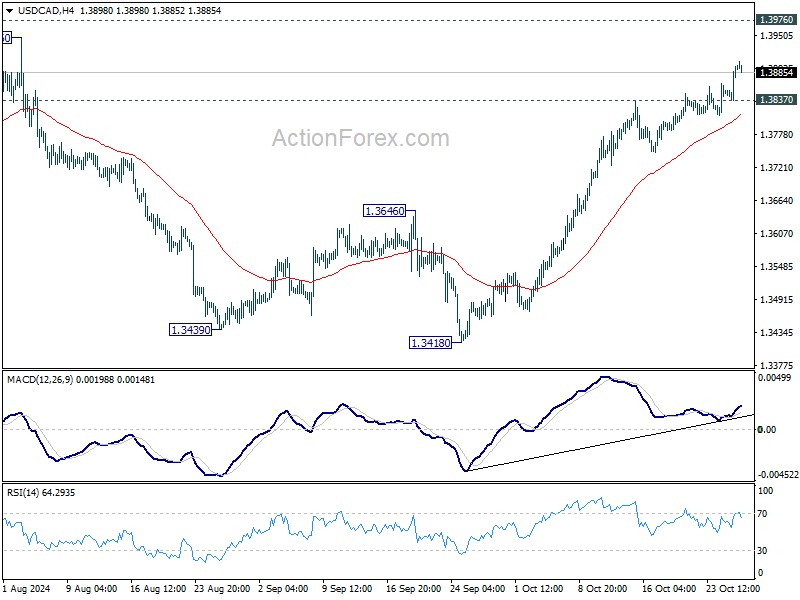

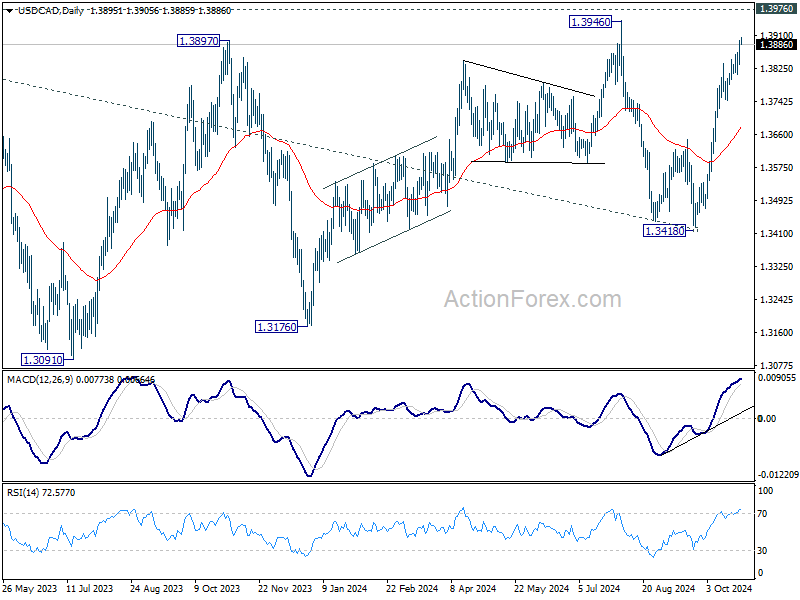

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3854; (P) 1.3876; (R1) 1.3914; More...

USD/CAD's rise from 1.3418 is in progress and intraday bias stays on the upside for retesting 1.3946/76 resistance zone. Decisive break there will confirm larger up trend resumption. On the downside, below 1.3837 minor support will turn intraday bias and bring consolidations first.

In the bigger picture, sideway consolidation pattern from 1.3976 (2022 high) might still extend further. While another decline cannot be ruled out, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage. Decisive break of 1.3976 will target 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391.

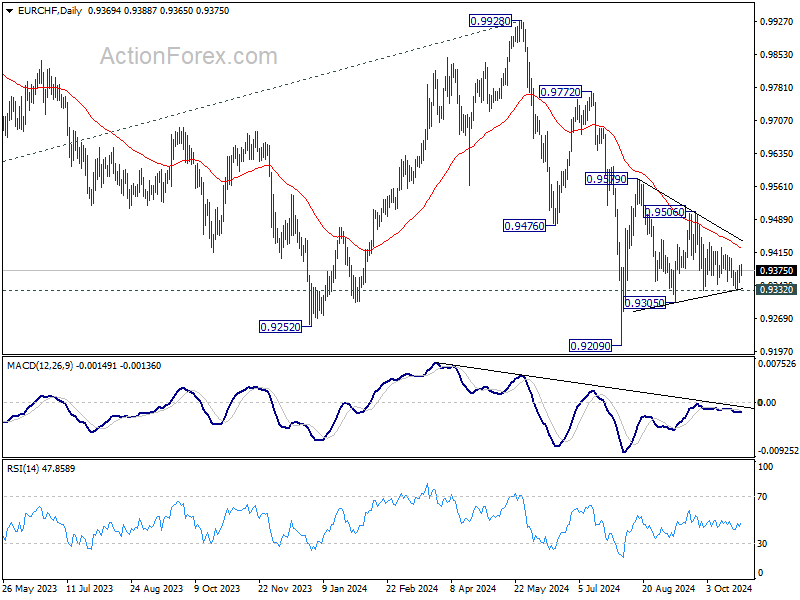

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9343; (P) 0.9366; (R1) 0.9380; More....

Intraday bias in EUR/CHF remains neutral for the moment as range trading continues. On the downside, break of 0.9332 will resume the fall from 0.9579 towards 0.9209 low. On the upside, break of 0.9506 will turn intraday bias to the upside for 0.9579 resistance and above.

In the bigger picture, fall from 0.9928 is seen as part of the long term down trend. Repeated rejection by 55 D EMA (now at 0.9427) keeps outlook bearish for breaking through 0.9209 low at a later stage. Nevertheless, sustained trading above 55 D EMA will confirm medium term bottoming and bring stronger rebound back towards 0.9928 key resistance.

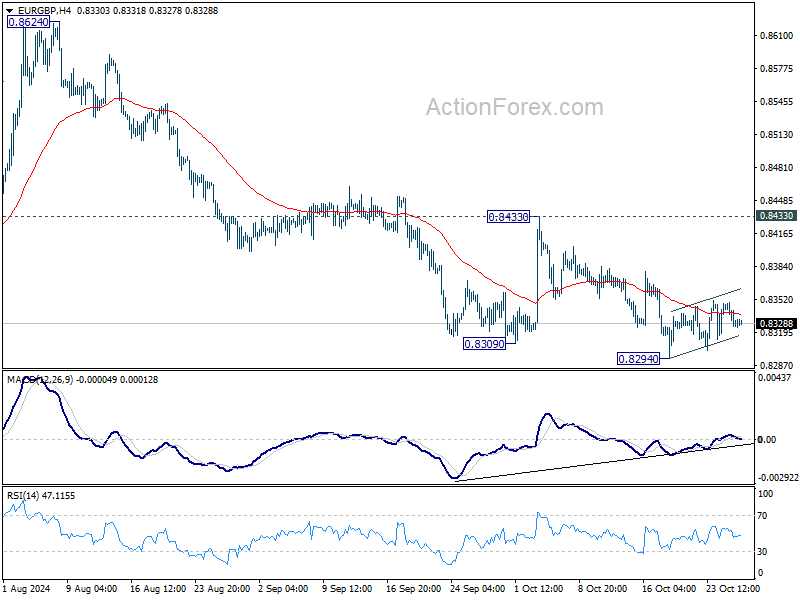

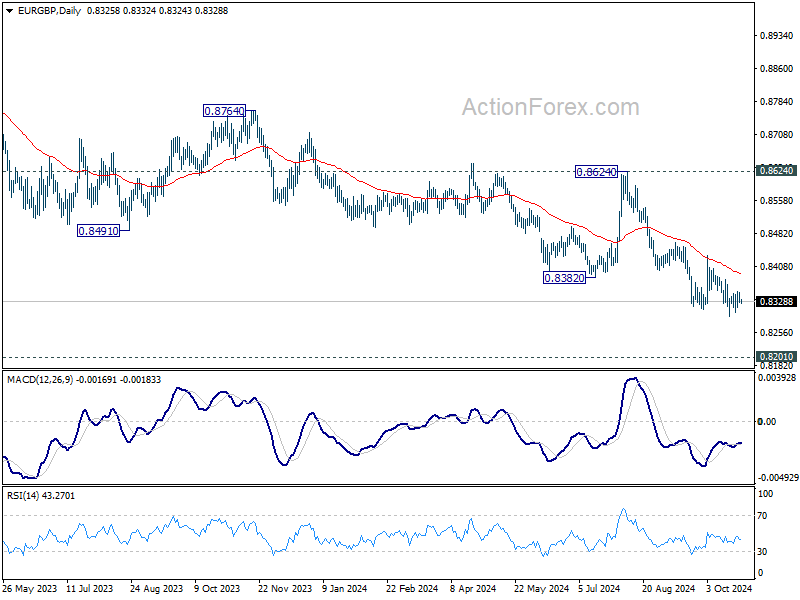

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8319; (P) 0.8337; (R1) 0.8347; More...

Intraday bias in EUR/GBP remains neutral as consolidation from 0.8294 is in progress. Outlook will stay bearish as long as 0.8433 resistance holds. Break of 0.8294 will resume larger down trend to 0.8201 key support next. Strong support could be seen from there to bring rebound.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

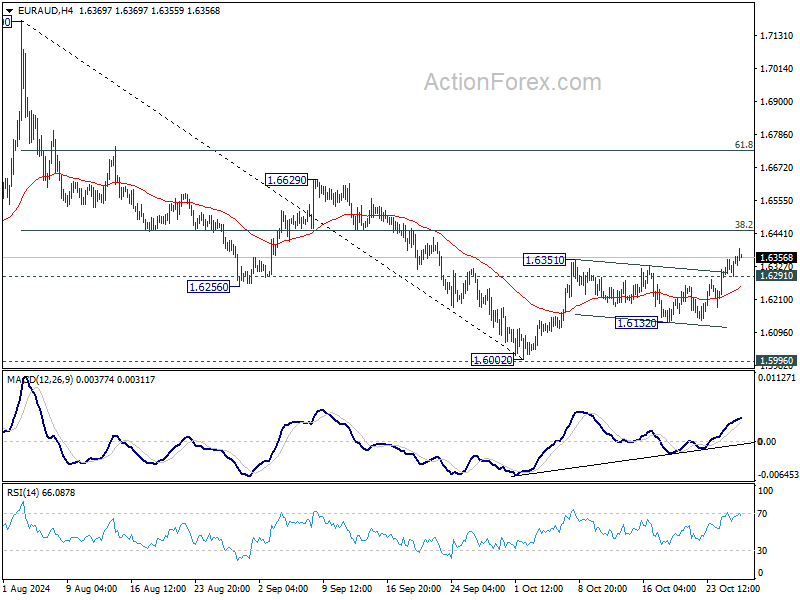

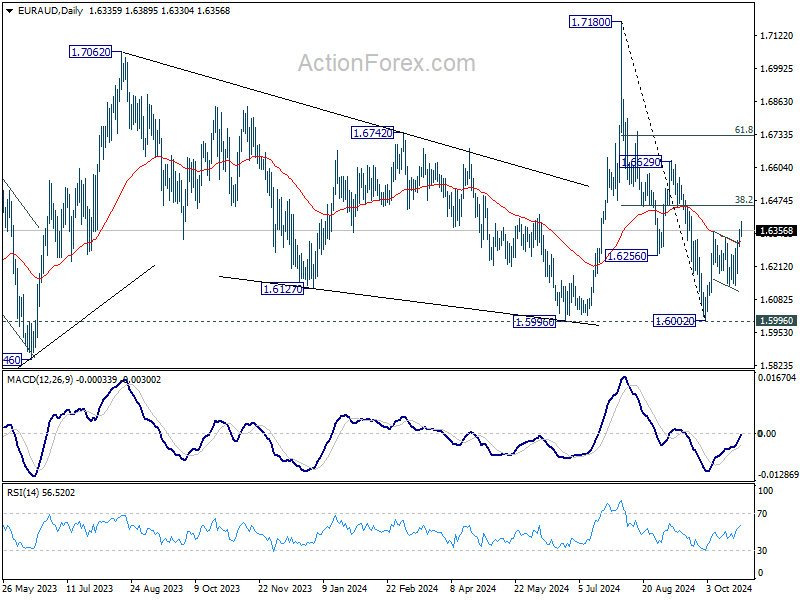

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6306; (P) 1.6334; (R1) 1.6375; More...

Intraday bias in EUR/AUD remains on the upside as rebound from 1.6002 is in progress. Further rise should be seen to 38.2% of 1.7180 to 1.6002 at 1.6452. Decisive break there should confirm that whole fall from 1.7180 has completed with three waves down to 1.6002, after being supported by 1.5996. On the downside, below 1.6291 minor support will turn intraday bias neutral first.

In the bigger picture, as long as 1.5996 cluster support holds (38.2% retracement of 1.4281 to 1.7062 (2023 high) at 1.6000), up trend from 1.4281 (2022 low) is still expected to resume at a later stage. However, decisive break of 1.5996 will argue that the medium term trend has reversed and turn outlook bearish.

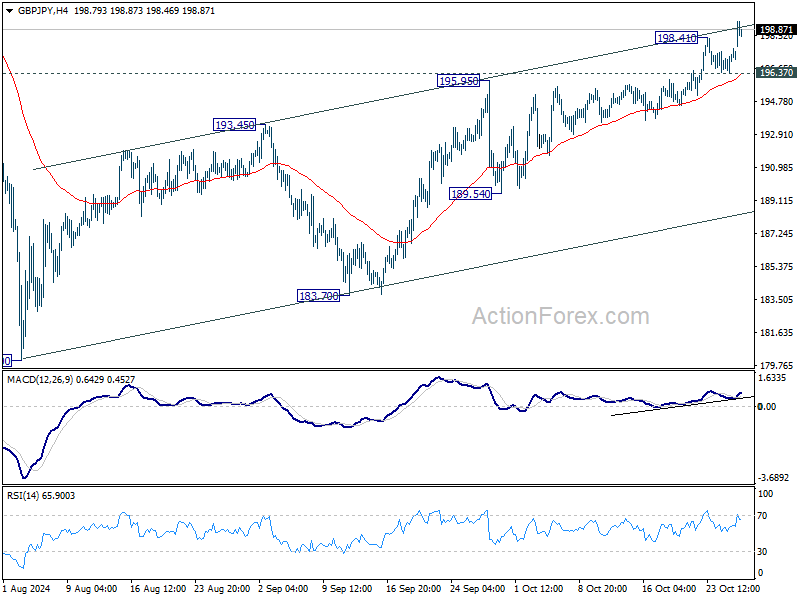

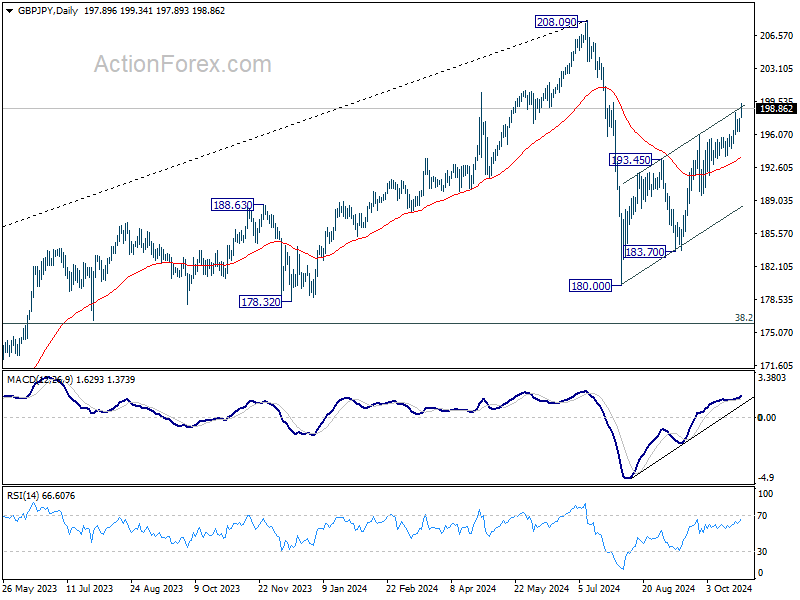

GBP/JPY Daily Outlook

Daily Pivots: (S1) 196.63; (P) 197.21; (R1) 198.03; More...

GBP/JPY's rally resumed after brief consolidations and intraday bias is back on the upside. Current rise from 180.00 should target a retest on 208.09 high next. On the downside, below 196.37 minor support will turn intraday bias neutral again first.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

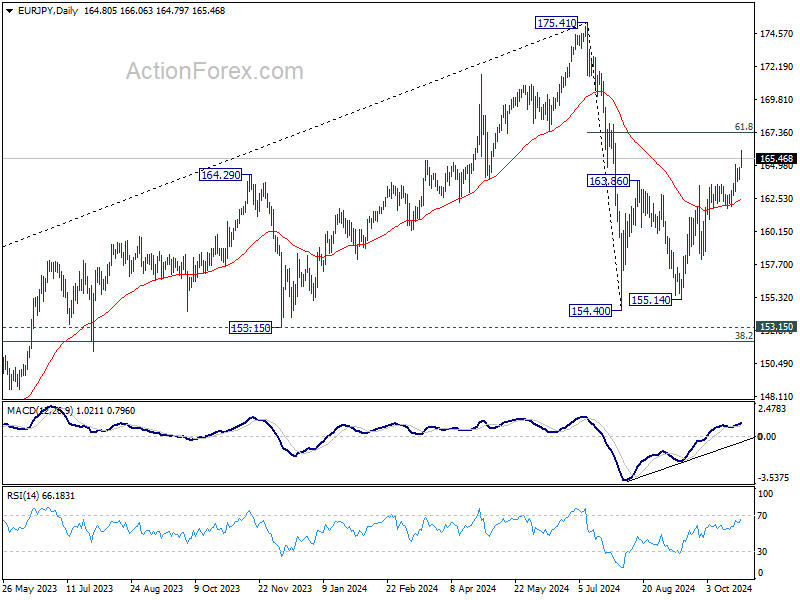

EUR/JPY Daily Outlook

Daily Pivots: (S1) 163.98; (P) 164.39; (R1) 164.83; More....

EUR/JPY's rally resumed after brief consolidations and intraday bias is back on the upside. Current rally from 154.40 should target 61.8% retracement of 175.41 to 154.40 at 167.38. Sustained break there will pave the way to retest 175.41 high. On the downside, below 163.79 minor support will turn intraday bias neutral again first.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.